Introduction

Over the past decade, software became the number one business model for start-ups and the go-to solution for entrepreneurs chasing success. The asset-light business model characterized by recurring revenue and high operating leverage attracted investors from all over the financial markets. It was particularly attractive to private equity firms, who invested heavily in the sector, with credit investors underwriting much of the leverage needed for the SaaS buyouts. The story was clear: high growth and cash generation potential down the line will drive superior LBO economics. Public market valuations reflected that confidence. Bessemer’s Cloud 100 data shows average revenue multiples peaked in 2021 and, despite subsequent compression, still stand at roughly 20x in 2025, approximately 41% below the peak. The first clouds in the sky appeared after markets realised that Large Language Models (LLMs) can produce code very cheaply. While still fairly clumsy, the LLMs are getting better and better at code generation and investors are becoming increasingly more aware of the threats this poses to software companies and, therefore, their portfolios. This article will explore the threat that AI poses to the software business model and how this impacts asset quality among alternative asset managers.

The AI Replacement Debate

With the wave of releases of more and more sophisticated LLMs in the last two years, public market investors started reckoning with the consequences AI will have on the entire software sector. Since the stock market is often the first to react, below we discuss multiple examples of how AI is affecting stock market valuation and what we can expect to follow in the private markets.

- Chegg [NYSE: CHGG]

Chegg is the cleanest public-market example of AI acting as a direct substitute. Chegg’s all-time high close was US$113.51 (12 Feb 2021) and is now sitting at US$0.66, translating to a market capitalisation of about $60m. This erosion is driven largely by depletion of demand, as generative AI replicated the core value proposition of step-by-step help, explanations, and Q&A at zero or near-zero marginal price for users. Discovery traffic weakened as search shifted away from links, especially with Google’s AI Overviews, which matters massively for a business built on inbound traffic and conversion funnels. In fact, Chegg recently filed a lawsuit against Google, alleging that the search platform’s AI-generated summaries and overviews are diverting traffic away from Chegg’s website by providing direct answers within search results, thus reducing click-through rates, undermining its ability to acquire subscribers, and extracting value from its content without compensation. In its Q3 2025 results, Chegg reported revenue of $77.74m (down ~49% YoY) and subscribers of 2.65m (down ~43% YoY). Additionally, non-subscriber traffic fell 49% YoY in January 2025, which Chegg explicitly tied to AI-driven changes in search behaviour. For 2025, Chegg reported total net revenues of $376.9m (down 39% YoY) and a net loss of $103.4m (down 87.6% YoY). Chegg’s product was, when simplified, only answers and explanations, which LLMs deliver instantly, conversationally, and often for free, making the platform fundamentally obsolete, with no apparent hope for an eventual recovery.

- Duolingo [NASDAQ: DUOL]

Language tutoring is one of the clearest generative AI use cases. A large language model can simulate conversation, explain grammar rules, and provide instant correction, including through spoken communication. In theory, that could bypass a dedicated language-learning app entirely. After impressive Q3 2025 earnings, Duolingo shares fell roughly 20–25% following softer-than-expected bookings guidance for Q4 and slower growth of their paid, specifically AI-enabled Max, tiers. The market’s concern around whether AI tutoring tools could slow long-term monetisation or reduce willingness to pay is very evidently being priced in, despite strong performance otherwise. Duolingo’s operating performance remains robust. In Q4 2024, the company reported 116.7 million Monthly Active Users, up 32% YoY, and 40.5 million Daily Active Users, up 51% YoY, with a FY2024 gross margin of 72.8%. Momentum continued into Q3 2025, when revenue grew 41% YoY, Daily Active Users exceeded 50 million, and gross margin remained stable at 72.5%. Much of the volatility centres on doubts regarding Duolingo’s position relative to AI. Rather than competing against generative tools, the company has embedded AI directly into its premium tier, enabling roleplay conversations, personalised explanations of answers, and more adaptive content generation within its structured learning framework. These features enhance perceived value and are monetised inside the subscription framework. Although AI increases compute costs modestly, gross margins remain strong above 70%, implying that integration is only incremental and sustainable. The competitive risk is always present in the long term. If AI interfaces someday become the de facto distribution channel for tutoring, Duolingo could face pricing pressure and break similarly to Chegg. However, at present, AI appears to be boosting engagement and product depth rather than draining away demand.

- Adobe [NASDAQ: ADBE]

Adobe is the most important test case in the AI replacement debate. If generative image and video tools can commoditise creative production, Adobe, being an incumbent in the industry, should be structurally vulnerable. In this case, AI introduces two significant risks:

- Low-end pricing pressure, as casual creators shift to cheaper/free AI-first tools

- Monetisation timing risk, if AI usage grows faster than Adobe’s AI revenue capture

Adobe’s stock has, in response, repriced materially from its November 2021 all-time high at $688.37 to a range in the mid-200s, down approximately 60%. The decline is indicative of multiple compression, as investors have reassessed long-term growth durability and priced in competitive risk from AI-native creative tools. Despite the valuation compression, Adobe’s core financial metrics remain stable. In FY2025, the company reported revenue of $23.77bn, up 11% YoY, with ending ARR of $25.20bn, an increase of 11.5% YoY. Operating cash flow exceeded $10bn, emphasising continued cash generation and balance sheet strength. Growth has moderated from pandemic-era highs but is still strong in double digits, and there is no evidence of revenue or margin contraction. This resilience is due to Adobe’s proactive integration of AI into its product offerings, reinforcing its ecosystem rather than collapsing in response to disruption. In fact, its proprietary model, Firefly, is embedded directly into Creative Cloud and Experience Cloud products through key integrations such as in Photoshop, Illustrator, Premiere Pro, and more. Firefly has reportedly surpassed 16 billion generations, evidence of meaningful adoption across the installed base. Importantly, these features sit inside paid subscriptions to help Adobe soften revenue loss from casual users shifting to AI-native alternatives. Therefore, Adobe sits squarely within the article’s central debate: while parts of its offering touch commoditised creative tasks that generative AI can replicate, its strength as an incumbent lies in owning integrated workflows, proprietary data, distribution, and a full-stack offering for creatives, where AI is only an enhancement reducing production time and increasing creative throughput.

AI Threats In the Private Markets

In recent months, the fears that have for long been visible in the public markets, started to surface among private markets investors. Bain estimates technology accounted for 25% of global buyout value in 2021 ($284bn), with software representing the majority of that exposure, while PitchBook data shows software comprised roughly 18% of US PE deal value in 2025 (around $203bn). Software is also estimated to represent approximately 40% of PE-backed leveraged loan exposure. In several large private equity funds, tech and software together accounted for more than 30 percent of invested capital. Given the multi-year holding periods typical in buyout strategies, a meaningful portion of current unrealized NAV across 2019 to 2022 funds remains exposed to SaaS business models underwritten at elevated multiples.

Questions About the SaaS LBO Thesis

Software industry has continuously stood out as one of the most prominent sectors for private buyout strategies in the last few years. According to Bloomberg, in the peak period spanning 2019 to 2021, the technology sector accounted for one third of global private equity deal value, with the software sector standing out as the majority share of this bracket. These firms had structurally attractive business models for rapid growth and exit, with strong margins (often >70%) and recurring revenues. Compounding on this, it is important to note that reported exposure should be adjusted to reflect the real concentration of private capital deployment in this sector. For instance, vertical SaaS software could be employed in firms that are classified as healthcare, food, industrials, etc., whilst fundamentally these firms are using software revenue models. Therefore, the negative impact of AI on software economics can span various sectors and may be larger than implied by sector figures. Traditionally, SaaS LBOs relied on projections of double-digit growth, with stable exit multiples. During the decade of low interest rates, private capital investors entered buyouts with high revenue and EBITDA multiples, relying on these projections of growth. Therefore, these investments relied on the assumption that projected growth would persist, leading to disruption with the entry of the AI threat. In fact, according to Bloomberg, these transactions embedded the majority of their enterprise value being tied to cash flows expected in the more distant future. This period is exactly where AI creates uncertainty. Considering product replacement, generative models could bring down development costs, lowering bargaining power for the SaaS industry and shifting it to model providers. This would bring Terminal Value assumptions down, hurting exit multiples for the private sector. The leverage, strongly applied to most of these transactions, will heighten the damage to ROE brought forward by small multiple compressions. This risk is compounded by refinancing dynamics. According to UBS estimations, one fifth of outstanding SaaS related leveraged loans will require refinancing by 2028. Most buyouts were set forward by zero-rate regimes, but the current base rates and credit spreads are higher, eroding profitability of exit multiples through higher interest expense. The risk arising from AI itself is likely to increase financing demands. According to the Financial Times, private credit managers are already facing greater investor withdrawals and more selective underwriting as concerns around AI-driven obsolescence risk intensify. Therefore, refinancing brings doubts about both the availability of capital and its resulting costs, which are likely to increase significantly. The downward adjustment of enterprise values, combined with higher interest expense, implies leverage metrics will mechanically deteriorate. Bloomberg highlights that software companies tend to exhibit weaker interest coverage ratios relative to many traditional industries, particularly when earnings are adjusted for stock based compensation or other non-cash items. Coupled with reduced growth, this lower coverage weakens deleveraging capacity. As a result, sponsors may need to inject additional equity or accept lower recovery outcomes at exit.

Another factor is exit optionality. The IPO market, which has suffered a recent drought in western countries, remains selective for SaaS, with investors allocating most capital in AI infrastructure. Moreover, sponsor to sponsor deals, one of the most prominent liquidity channels, now incorporate deeper technological diligence around AI defensibility. The assumption that broad exposure to the software sector guarantees secular growth has fallen; now, investors must distinguish between products based on their vulnerability to substitution by AI agents.

For private equity & credit, this marks a strategic shift in their investment process. For future transactions, competitive advantage in this sector will depend on technology judgement, rather than their historic multiple arbitrage. Highlighting this, the institutions able to assess whether companies possess proprietary data and have durable switching costs, are the most likely to preserve flexibility and value in their investments. Meanwhile, those relying on sector momentum will likely face volatility in returns across vintages and portfolios.

Simultaneously, this volatility may create investment opportunity. Limited partners may seek liquidity following overexposure to software, creating discounted entry multiples in the secondary market. Moreover, the previously mentioned repricing of the public markets may reopen the possibility of “take-private” transactions at reasonable entry valuations, especially for the case of firms whose core business model remains intact but whose share prices have compressed excessively from AI pressure. Furthermore, the uncertainty and stress brought onto capital structures may generate distressed investing opportunities at attractive risk-adjusted returns, which are core to Private Equity & Credit firms like Elliot Management. Overall, it’s important to consider that the adjustment brought forward by AI to the SaaS sector has shifted investments rather than purely eliminating them.

Reckoning for Private Credit

The SaaS concentration is equally visible in private credit. Public disclosures from major direct lending platforms show that technology and software represent a significant share of portfolio fair value. Blue Owl’s direct lending vehicles have reported technology exposure in the mid to high teens as a percentage of total investments, while Ares Capital has disclosed comparable exposure levels across technology and software-oriented borrowers in its quarterly filings. These allocations are not marginal. In diversified credit portfolios, a mid teens percentage in a single sector is material, particularly when that sector is characterized by duration-sensitive valuation dynamics and relatively low tangible asset backing. Because these exposures sit at current NAV rather than new commitments, repricing risk translates directly into mark-to-market pressure within both closed end funds and semi liquid credit vehicles. The recent credit volatility began with the bankruptcy of First Brands Group, a sponsor-backed industrial borrower whose restructuring raised broader questions about leverage tolerance in the direct lending market. Shortly thereafter, Jamie Dimon publicly warned about the appearance of “cockroaches,” suggesting that one default may signal others beneath the surface. His remark catalysed a shift in sentiment toward private credit more broadly. This narrative then became relevant to software exposure, when media coverage began highlighting the potential for AI-driven disruption in application layer software. As a result, investor scrutiny moved toward technology heavy direct lending portfolios, with the risk of cashflow disruption. Specifically, Blue Owl was largely affected due to the scale of its direct lending platform and disclosed exposure to technology borrowers. In fact, Blue Owl was forced to raise its redemption limit to 15% of NAV to manage the scale of investor sentiment shift. Other listed alternative asset managers with significant private credit exposure experienced abrupt double-digit share price declines over the period of rising uncertainty. Despite investor panic, leadership of credit funds calls for a rational approach to the issue. Blue Owl’s CEO claims that for now they don’t see any red or even yellow flags in the financials of their portfolio companies. Furthermore, he points to the relatively high margin of safety with reported average LTVs measured at 30% of Enterprise Value. While reassuring, this must be taken with a grain of salt, as the buffer only depends on the EV durability. If these valuations are based on the previously mentioned peak multiples of the SaaS industry, the effective leverage ratios would be higher when adjusted. Addressing this, Bloomberg’s recent opinion analysis on private credit and AI argues that software debt is particularly sensitive to shifts in growth expectations because a large share of value is tied to future expansion rather than tangible asset backing.

Overall, it is clear that risks exist and key fundamentals that were underlying most of the SaaS LBO underwriting have shifted. While current financial indicators show scarce evidence of impairment among SaaS assets, a more nuanced and less backwards-looking analysis of the disruption AI is bringing to the sector is warranted.

How will AI Actually Disrupt SaaS: a historical perspective on disruption

The first point that ought to be addressed in order to argue our view on the structural shifts in the software business is that of defining what does “disruption” actually mean. On a high level, it is a fundamental change in the technology or process underlying an entire sector or the entire economy. Historically, disruption took on many forms, and while history never repeats itself, it rhymes. Thus, before addressing the question of software, let us examine some lessons learned from the past.

Kodak [NYSE: KODK] was one of the most dominant companies of the 20th century, until a digital camera was invented. Kodak’s 2024 revenue is $1.04bn; a mere fraction of its peak $16bn in 1996. Without the benefit of hindsight, one would be compelled to conclude that the invention of a digital camera took place around that time. Far from the truth. In fact, the first digital camera was invented in 1978 and the first filmless electronic camera was marketed to consumers in 1986, meaning that Kodak thrived for 10 more years after the “killer” of their product was widely adopted by the consumer.

Many software bull theses are centred around showing stable revenue growth in the last couple of quarters and arguing that there is no sign of disruption. Kodak’s case clearly invalidates this reasoning and shows that the backward-looking approach is baseless given the lag major disruptions often come with. A refined version of the argument is that the diffusion of AI is much quicker than that of digital cameras and even the internet, which was the fastest diffusion in history of disruption. That argument does not make much sense either. True, AI is diffusing fast, but diffusion pace has no strong relationship with impact. For example, in 2006 many thought the internet was already mature and the disruption it could cause was mostly done and priced-in. Since then, the internet enabled mobile apps, streaming services and is now helping the diffusion of AI.

The first takeaway is that due to the unpredictable nature of disruption, the usage of backwards-looking financials is nowhere near good enough to justify any view on AI and software. The second takeaway is that disruption is not an overnight displacement of the legacy product. In reality, it comes in two more nuanced forms. The first is gradual replacement, whereby the new product directly substitutes the old one. An example of this is the digital camera, which eventually replaced Kodak’s legacy product. But this doesn’t always have to be black-and-white. Pottery is a great example. The advent of Industrial Revolution and the industrialisation of the production process dramatically decreased manufacturing costs and made handmade products uncompetitive. Did this mark the death of pottery? No. It just shifted the value proposition from a mere utility to a form of art, in which pottery is thriving to this day. The second form in which disruption comes is enablement, whereby the new technology drastically improves an already-existing process or product. Again drawing on the Industrial Revolution, introduction of textile machines enabled production on a mass scale and decreased the capital requirements, democratising the production process.

Is Software Dead?

From the two types of disruption – replacement and enablement – it is the latter that prevails in the software space. An examination of hourly rates for junior developers shows that the price of producing code is dropping quickly. But code itself is not being replaced, it is just the barriers to entry that are coming down. It is therefore clear that as the cost of code drops, prices will trend downwards, certainly changing the current power dynamics. But not all of the segments will be affected equally. Multiple embedded anti-disruption mechanisms exist which will make the change easier or more difficult depending on the specific subsegment of the software business.

- Systemic Barriers: Switching Costs and Network Effects: Most companies have extensive and complicated operating structures built on tried-and-tested systems. The clearest example would be Excel, which is the go-to tool in finance. If all bankers have models in Excel, all auditors have their audits in Excel, and regulators require Excel for disclosures, how much better and cheaper would a competing tool have to be to convince the entire financial system to migrate? This is even more pronounced in internal management platforms. Imagine a product like ServiceNow which connects and streamlines workflows between different systems in a company: an entry of a new employee in the onboarding software triggers a new email creation in the cloud accounts, an accounting entry in the payroll system, and a myriad of other necessary adjustments. With a platform built on top of a set of smaller platforms, one can imagine it is costly both in dollar terms and in terms of time to migrate the entire ecosystem onto a new solution. If on top of all that, the necessary condition that all counterparties follow suit in order to enable network effects, it is easy to imagine the bar for inducing change is very high.

- Human Nature: Value Added and Inertia: A common subconscious heuristic of humans is inertia – the tendency to choose to do nothing if taking action doesn’t provide disproportionately better outcomes. While mainly behavioural, it should be known by now that actual business practice often deviates from the theory of efficient capital allocation. Inertia goes back to the question: just how good do these new tools have to be in order to force everyone to migrate? While the above-mentioned barriers related to systems design are key, human nature will only further slow-down the transition. It is likely that only the truly best-in-class solutions that offer undeniable cost-savings will gain traction and market-wide adoption while the rest will remain in the “cool tool” category without ever penetrating institutional markets.

The interplay of these barriers has significant implications on who is likely to be disrupted and who is here to stay – at least for the medium-term. The most exposed group is B2C software. Almost no switching cost exists and there are no systemic conditions or complex backend systems that require tech stack overhauls. Furthermore, the quality bar is lower compared to institutional software: personal-use apps for calendars or language learning are relatively uncomplicated compared to institutional software. With tools such as Lovable or ElevenLabs that bring production cost close to zero, it is logical to think B2C software is the first domino to fall. The market seems to agree, with consumer-centric software companies like Duolingo (down 33% YTD) facing investor pressure.

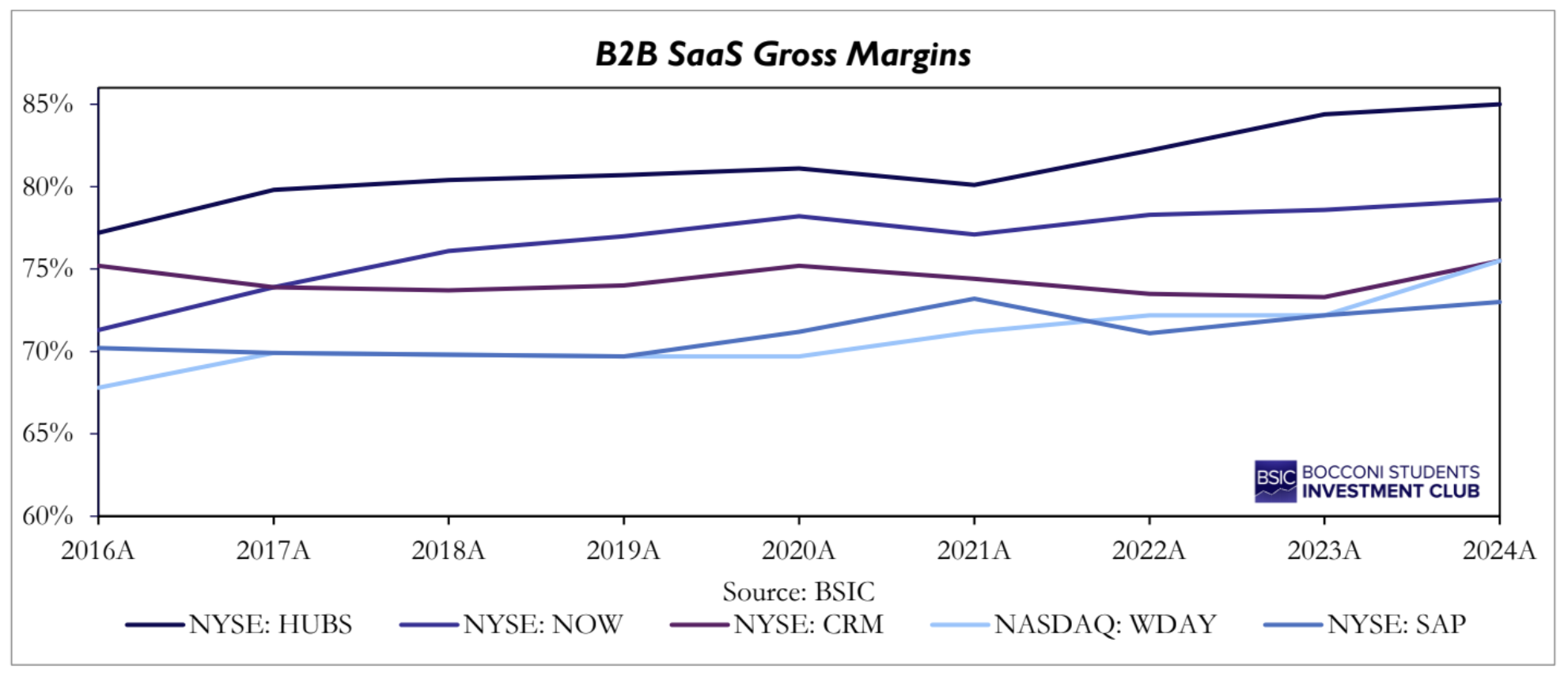

Business-to-Business software, on the other hand, is much more sticky and less susceptible to the AI disruption. Of course, the strength of the anti-disruptive forces depends on the specific product offering. Some products like DataDog (NASDAQ: DDOG), offering observability and backend management tools, derive their moats from being deeply embedded in the tech stacks of their clients. Products like Adobe [NASDAQ: ADBE] or the Microsoft [NASDAQ: MSFT] Suite are entrenched in the path dependency of employees being trained using these specific tools and the opportunity cost of re-educating the entire employee population to migrate to new software. Some benefit from both. Specifically, the Microsoft suite which is not only the go-to tool for slide-making and other fundamental corporate functions, but often serves for accounting, reporting, and other financial purposes in less sophisticated businesses. Thus, it is clear that B2B software will not disappear overnight. However, its lucrative business model that worked for the last 15 years might no longer be attainable as the pricing power will shift. In the last 10 years, B2B software companies could raise prices every year, not only passing-through inflation but also expanding margins.

Now that the cost of software production is much lower, the price dynamic should revert. If software companies keep their pricing strategy, with every price hike the inertia and switching cost arguments will erode, leading to higher churn. In fact, there’s a visible trend of migration away from the lucrative subscription-based pricing onto a flat platform fee model, which is more attractive to clients and helps alleviate the AI pressures. This model switch will inevitably put downward pressure on revenue growth and margins. On the flip-side, incumbents can seek to offset this dynamic by cutting their own costs; after all, the software production cost dropping should allow them to make their structures more lean and efficient. Overall, however, it is clear that the lucrative business model of B2B SaaS that attracted investors over the years is no longer attainable and margins will keep compressing from now onwards.

Contrary to the headlines about “SaaS-Pocalypse” and investor panic about software being completely displaced, markets seem to be pricing the situation fairly rationally. Multiples of large software players have been on a steady compression trend in the last 12 months. For example, Adobe’s [NASDAQ: ADBE] LTM P/E dropped from the 35x-40x range in 2024 to around 15x as of today. Similar path was followed by SalesForce [NYSE: CRM] stock which trades around 25x earnings, compared to above 50x just months ago. It is thus clear that investors understand that the anti-disruptive forces of B2B software will keep the legacy giants afloat, at least in the medium-term. The true apocalypse may come, but only after switching costs are brought down to zero, which seems to be a rather distant vision.

Conclusion

AI introduces a structural risk to parts of the software sector, as value may shift away from application-layer products toward models that can replicate core functionality at negligible marginal cost. Public markets are already differentiating between businesses that primarily package information and those that control critical workflows, proprietary data, and distribution. In private equity, underwriting based on durable pricing power, low churn, and stable cash flow become fragile if AI erodes a company’s value proposition faster than leverage can be amortised. However, incumbents that embed generative AI into their products continue to report revenue growth (Adobe, Duolingo), stable gross margins, and expanding ARR, indicating that AI can reinforce rather than replace established software or workflows when integrated effectively. The central question is therefore how quickly value migrates within the stack and whether PE portfolios are presently structurally exposed to those layers most susceptible to substitution. In the medium-term, we see best-in-class B2B Software Companies as challenged on the pricing and growth front, however, stable overall. Less entrenched and consumer facing products, however, are at an immediate threat, which poses some risk to the exposed private equity and credit portfolios.

0 Comments