USA

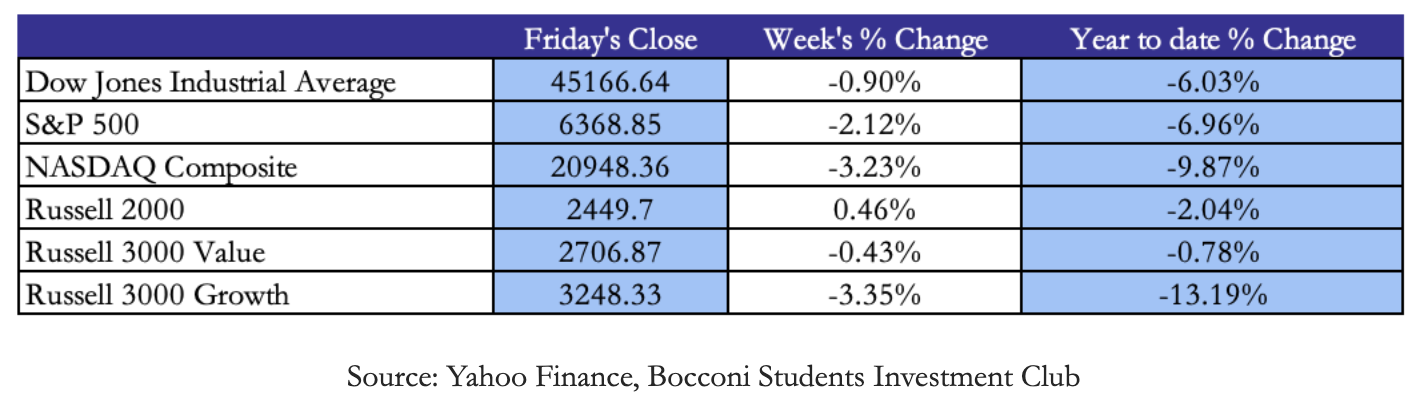

US equity markets closed out the final week of Q1 under sustained selling pressure, as the Iran conflict entered its fourth week with the Strait of Hormuz still closed and no clear resolution in sight. The sell-off was broad-based across all major indices and growth-oriented names bearing the main impact. The Nasdaq and Russell 3000 Growth suffered the steepest declines on both a weekly and monthly basis, reflecting continued investor flight from high-multiple tech positions toward more defensive positioning. The Russell 3000 Value, by contrast, proved notably more resilient, underscoring a clear preference for value over growth in the current risk environment. Small caps, as measured by the Russell 2000, also came under significant pressure, sensitive to rising energy costs and tightening financial conditions.

At the sector level, the week’s narrative was starkly divided. Energy names continued to benefit from surging oil prices, with WTI rising to $101 per barrel again. The primary drag was technology, with the memory chip space hit particularly hard after Google unveiled a compression algorithm that could materially reduce AI memory requirements, sending Micron down over 15% and Sandisk following closely behind. On the bright side, Dell and ARM stood out as notable outperformers, with AI infrastructure demand providing a floor against the broader tech sell-off. Travel disruption winners also emerged, with Avis Budget surging on the thesis that airport chaos was driving demand for car rentals.

Looking ahead, volatility is expected to remain elevated with the start of earnings season approaching and the Iran negotiation deadline set for April 6th.

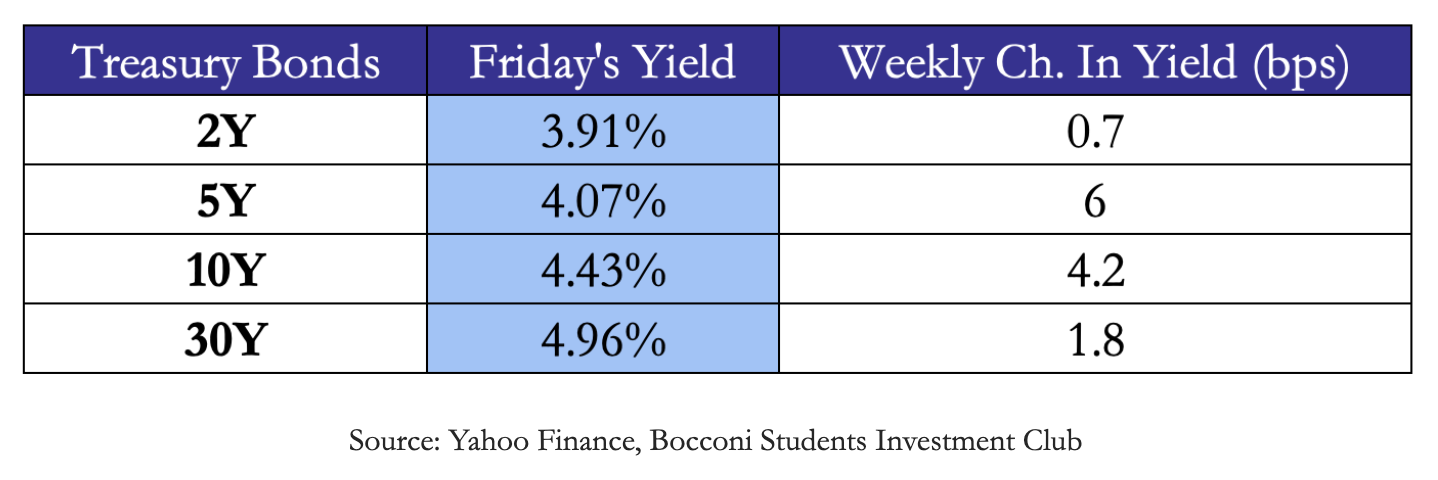

US Treasuries saw some changes across the curve this week, with yields rising most notably in the belly. The 5Y added 6 bps to close at 4.07%, while the short end remained virtually anchored, with the 2Y up less than 1 bp at 3.91%. The long end similarly showed restraint, with the 30Y adding under 2 bps to close just below 5%. The resulting yield move reflects a market caught between two forces: persistent inflationary pressure and a Fed that continues to signal patience, keeping the short end pinned. With the front end pricing only a marginal probability of a hike at the April meeting, the curve dynamic suggests markets see the oil shock as a medium-term inflation risk rather than a trigger for imminent action.

US Treasuries saw some changes across the curve this week, with yields rising most notably in the belly. The 5Y added 6 bps to close at 4.07%, while the short end remained virtually anchored, with the 2Y up less than 1 bp at 3.91%. The long end similarly showed restraint, with the 30Y adding under 2 bps to close just below 5%. The resulting yield move reflects a market caught between two forces: persistent inflationary pressure and a Fed that continues to signal patience, keeping the short end pinned. With the front end pricing only a marginal probability of a hike at the April meeting, the curve dynamic suggests markets see the oil shock as a medium-term inflation risk rather than a trigger for imminent action.

Europe and UK

Europe and UK

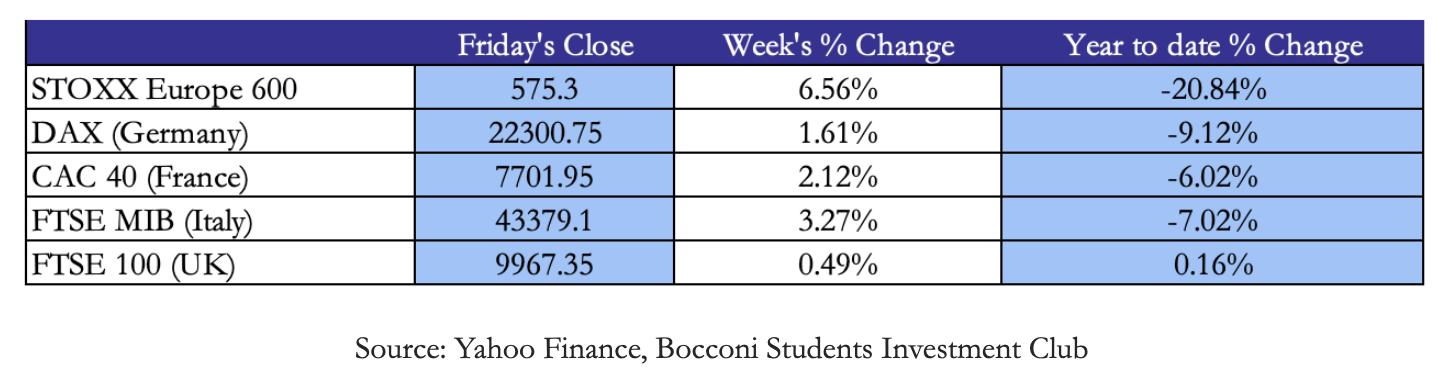

European equities endured a volatile week, with the STOXX 600 swinging sharply in both directions as investors analysed contradictory signals on Middle East peace negotiations. Monday brought a rebound after Trump signalled a potential de-escalation, with travel and leisure stocks leading the recovery, only for Thursday to reverse those gains as investors struggled to decipher mixed messages on the status of peace talks. By Friday, the STOXX 600 closed 0.9% lower, with the CAC 40 down 0.9% and the DAX off 1.3%, while the FTSE 100 closed just below the flatline. The UK’s relative outperformance on Friday was driven by energy heavyweights benefiting from elevated oil prices, though the broader domestic picture remains clouded by persistent inflation and subdued growth expectations heading into the Bank of England’s next meeting.

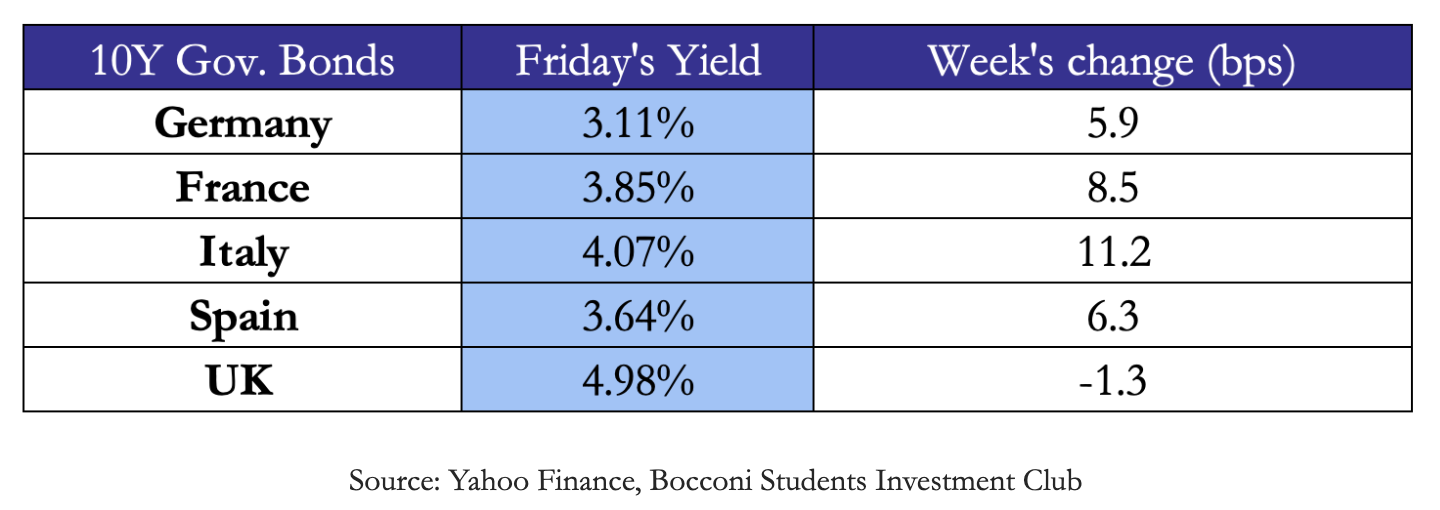

European sovereign bond yields rose across the board this week, reflecting the persistent inflationary pressure from elevated energy prices. The move was broad-based but uneven, with Italian BTPs leading the sell-off adding over 11 bps to close at 4.07%, while French OATs followed with 8.5 bps. German and Spanish Bonds saw more contained moves of around 6 bps each, closing at 3.11% and 3.64% respectively. The widening gap between core and peripheral yields reflects a classic flight to safety, as investors grow increasingly reluctant to hold Italian bonds amid fears of slowing growth and rising inflation. The notable outlier was the UK Gilt, which bucked the trend and tightened marginally by 1.3 bps to close just below 5%. This divergence is consistent with a market that sees the Bank of England as increasingly constrained, with weak activity data, softening consumer confidence and cautious MPC communication all pointing to limited room for further tightening, even as inflation risks persist.

European sovereign bond yields rose across the board this week, reflecting the persistent inflationary pressure from elevated energy prices. The move was broad-based but uneven, with Italian BTPs leading the sell-off adding over 11 bps to close at 4.07%, while French OATs followed with 8.5 bps. German and Spanish Bonds saw more contained moves of around 6 bps each, closing at 3.11% and 3.64% respectively. The widening gap between core and peripheral yields reflects a classic flight to safety, as investors grow increasingly reluctant to hold Italian bonds amid fears of slowing growth and rising inflation. The notable outlier was the UK Gilt, which bucked the trend and tightened marginally by 1.3 bps to close just below 5%. This divergence is consistent with a market that sees the Bank of England as increasingly constrained, with weak activity data, softening consumer confidence and cautious MPC communication all pointing to limited room for further tightening, even as inflation risks persist.

Rest of the World

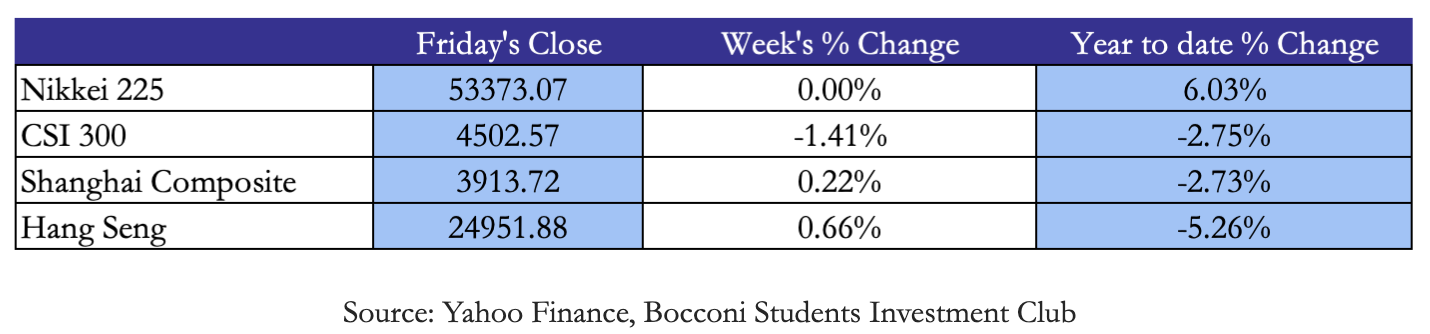

Asian equity markets ended the week on a mixed but broadly cautious note, again driven by uncertainty around the U.S.-Iran conflict. Japan’s Nikkei 225 was essentially flat for the week, closing at 53,373.07, a significant recoil from the record highs above 57,000 reached in February. The Nikkei had rallied earlier in the week after Japan’s headline inflation eased for a fourth consecutive month in February, aided by stabilising food prices and fuel subsidies. In the Chinese the CSI 300 fell 1.41% as persistent deflationary pressures weighed on sentiment, while the Shanghai Composite went up 0.22% and the Hang Seng gained 0.66%, strengthened by a 15.2% jump in China’s industrial profits for January-February versus a year earlier. China’s decision to set its 2026 GDP growth target at 4.5%-5%, the lowest on record, reflects Beijing’s acknowledgment of deflationary headwinds and ongoing trade tensions.

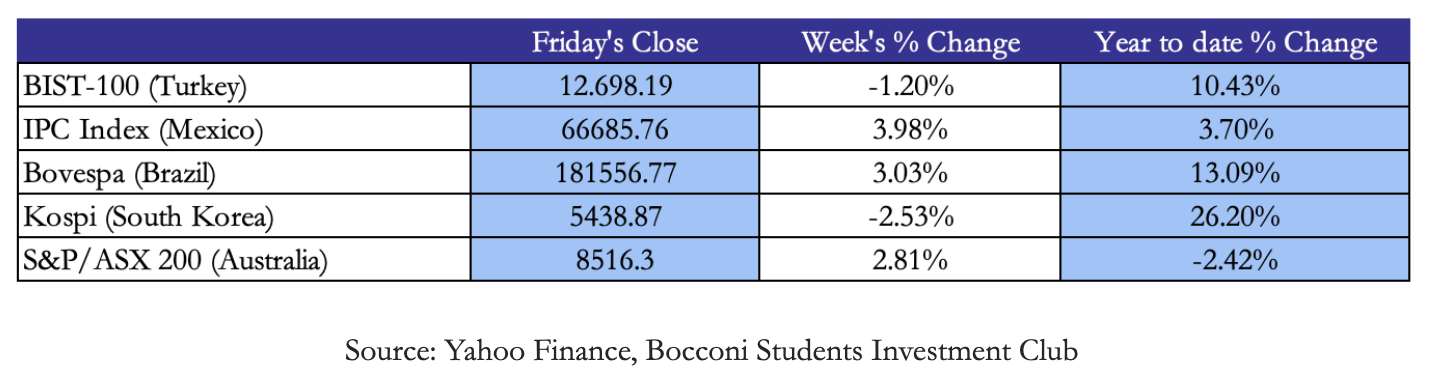

Latin American markets put in a notably strong week, resisting the global risk-off trend driven by Middle East tensions. Mexico’s IPC and Brazil’s Bovespa gained 3.98% and 3.03% respectively, extending a remarkable year-to-date increase. The MSCI EM Latin America Index has now surged over 20% in 2026, its strongest start since 1991, driven by a surge in overseas buying across Brazil, Colombia and Mexico. The key catalyst this week was the U.S. Supreme Court’s ruling striking down Trump’s sweeping global tariffs, which investors viewed as a boost for the region’s equity revival. Turkey’s BIST-100 slipped 1.20% as domestic inflation concerns persisted, while South Korea’s Kospi fell 2.53%, pressured by tech sector weakness and elevated energy import costs. Australia’s ASX 200 recovered 2.81%, supported by commodity-exposed miners benefiting from increased oil and metals prices.

FX and Commodities

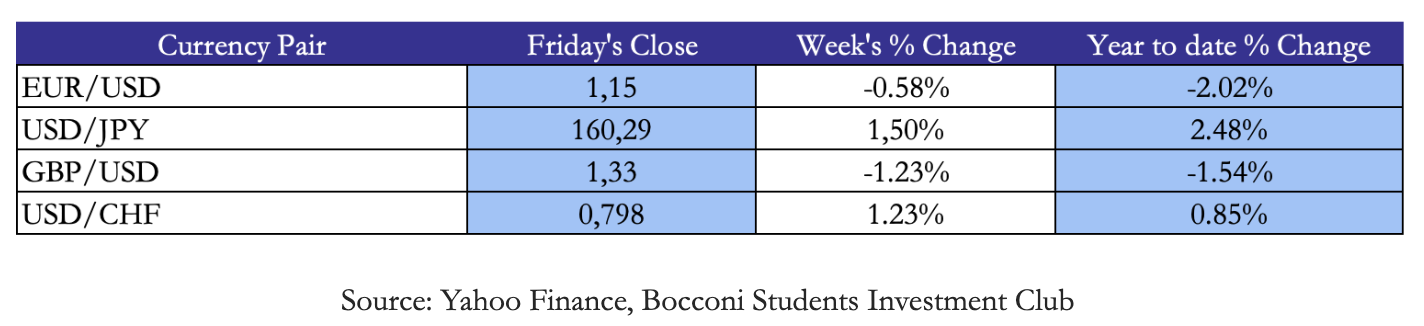

The U.S. dollar strengthened broadly this week, with the DXY holding near 100 as Iran conflict uncertainty and persistent inflation kept safe-haven demand elevated. EUR/USD slipped to 1.15 and GBP/USD fell to 1.33, while the yen weakened further to 160.29, weighed down by the continuous U.S.-Japan yield differential.

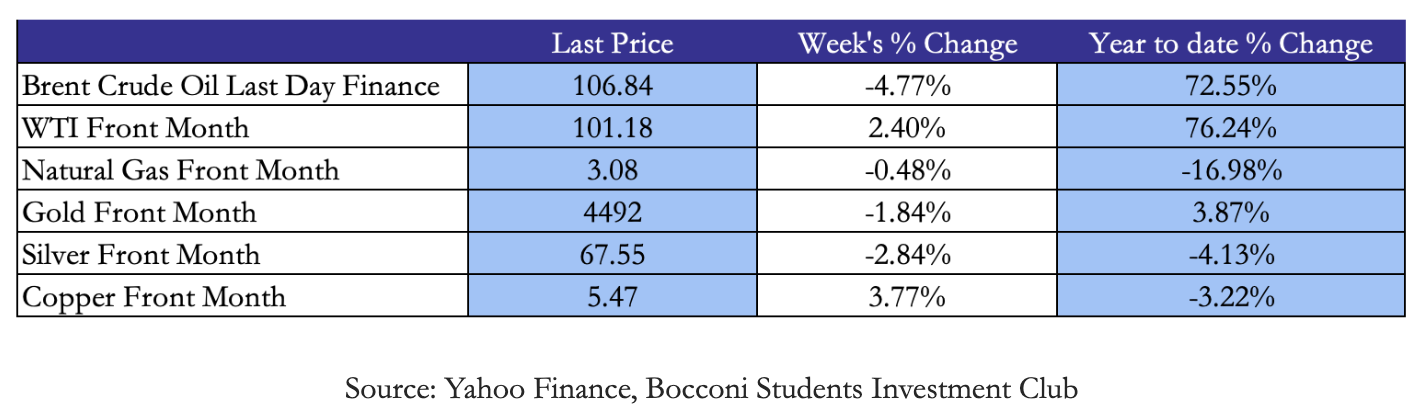

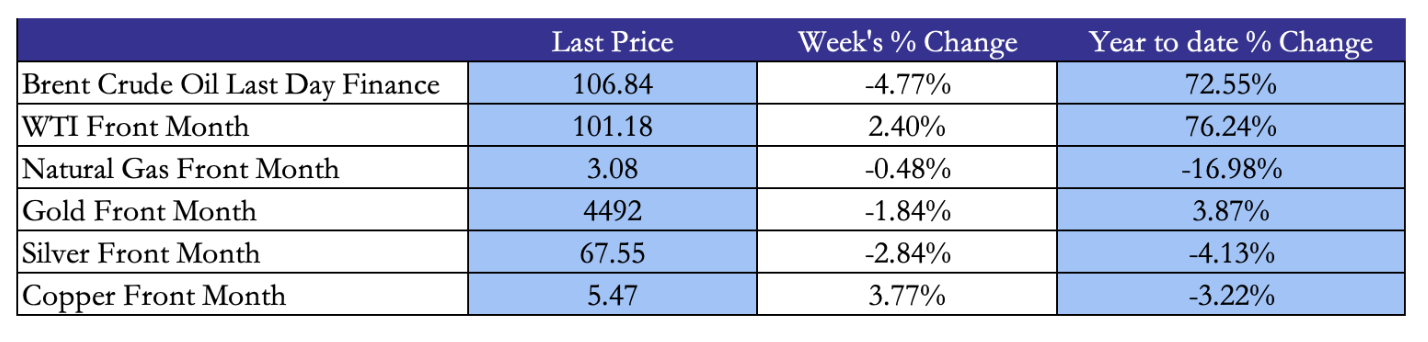

Brent at $106 and WTI at $101 reflect an astonishing 70%+ year-to-date surge, as the effective closure of the Strait of Hormuz continues to remove meaningful supply from global markets. Although President Trump extended the strike deadline for Iranian energy infrastructure to April 6 market scepticism remains high. Natural gas edged down 0.48% to $3.08, defying the broader energy complex’s upward trend. Precious metals retreated, with gold falling 1.84% to $4,492 and silver down 2.84%, as the Fed’s hawkish hold and dollar strength weighed on the space. Copper was the exception, gaining 3.77% on resilient industrial demand signals out of China.

Brent at $106 and WTI at $101 reflect an astonishing 70%+ year-to-date surge, as the effective closure of the Strait of Hormuz continues to remove meaningful supply from global markets. Although President Trump extended the strike deadline for Iranian energy infrastructure to April 6 market scepticism remains high. Natural gas edged down 0.48% to $3.08, defying the broader energy complex’s upward trend. Precious metals retreated, with gold falling 1.84% to $4,492 and silver down 2.84%, as the Fed’s hawkish hold and dollar strength weighed on the space. Copper was the exception, gaining 3.77% on resilient industrial demand signals out of China.

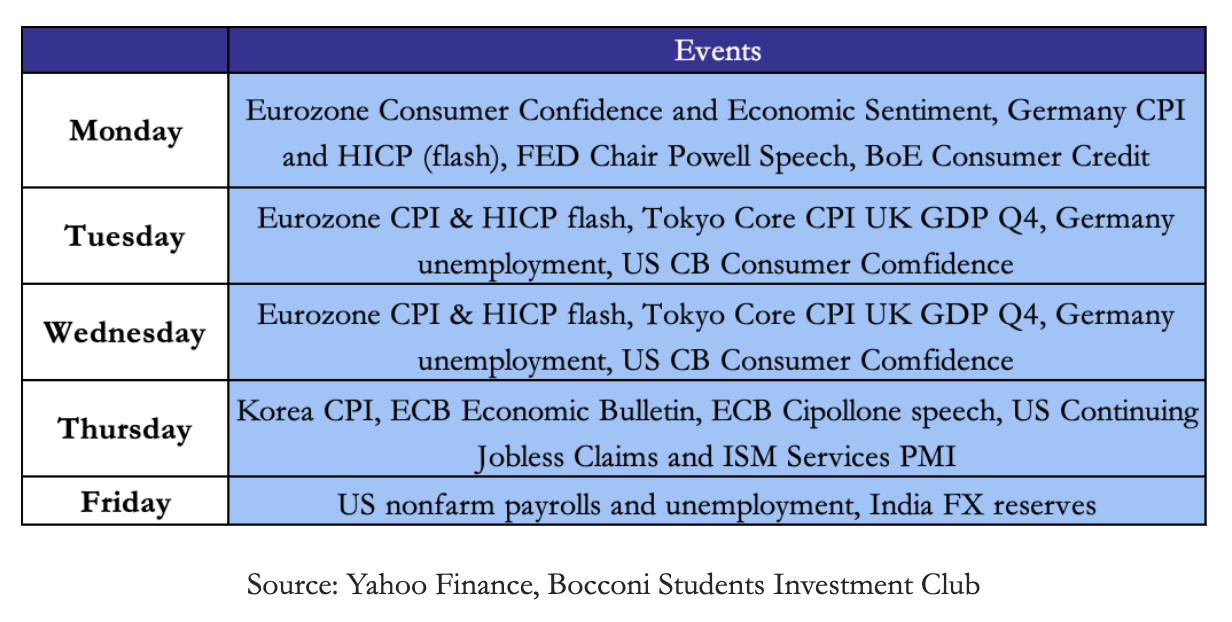

Next Week’s Main Events

Next Week’s Main Events

As markets close out Q1, attention will shift from central bank signaling to hard data, with inflation prints and labour market figures set to define the macro narrative heading into Q2.

Brain Teaser #43

A plane flies from point A to B and then back from B to A, with constant speed and no resistance. Later, the plane flies the same distance there and back, but with wind blowing from A to B, increasing the planes speed from A to B equally much as it reduces the planes speed from B to A. Does the full trip take longer, shorter or equal amount of time on the second fare?

Solution:

The answer is longer.

Let distance = d, base speed = v, wind speed = w.

- No-wind total time: 2d/v

- With-wind total time: d/(v+w) + d/(v−w) = 2dv/(v²−w²)

Since v²−w² < v², the with-wind trip takes longer. The time lost fighting the headwind always exceeds the time gained with the tailwind, because the plane spends more time at the slower speed.

Brain Teaser #44

100 tigers and 1 sheep are put on a magic island that only has grass. Tigers can eat grass, but they would rather eat sheep. Assume: A. Each time only one tiger can eat one sheep, and that tiger itself will become a sheep after it eats the sheep. B. All tigers are smart and perfectly rational, and they want to survive. Will the sheep be eaten?

{kind=link}

0 Comments