Introduction

“Taxes are the price we pay for a civilized society.” – Oliver Wendell Holmes Jr.

One of the first lessons in any basic economics course covers trade and specialization. The idea is simple: people are more efficient when focusing on one range of tasks, and exchanging the benefits of their own labour can be mutually beneficial. A fisherman and a farmer can trade to avoid the inherent inefficiencies of each conducting both activities. As societies developed, this form of specialization also began to be expressed through taxes as a fee to join an economic system (country). I need to protect my crops from invaders; thus, I trade my goods (nowadays money) for protection through national armies. The rationale for why this trade (taxes) is a legal obligation rather than a voluntary one is that it is a societal good. For example, countries need laws. Laws are only applicable if they are enforced. Taxes are required for the enforcers of these rules: the police. This logic works only when people are required to collectively pay for key services that allow a society to function. Without a legal obligation, people stop paying because they believe someone else will foot the bill, ultimately dooming the service the tax was intended to fund. The tax is a fee for access to basic societal services. Even the staunchest free-market economists (unless they are anarchists) agree that some form of taxation is necessary due to this very example. Of course, beyond these key services where collective payments are required, taxation becomes fiercely debated. Should the state provide goods such as healthcare, or is the private sector more efficient? Is efficiency even the yardstick we should use, or is it financial equity? These questions have been answered and implemented differently across countries’ tax codes. With the rise of a more global workforce, these approaches have directly impacted migration and led to phenomena such as Brain Drain. If workers are unhappy and feel that they can receive a better bargain for societal goods in another country, they can easily leave. In this article, we will explore the key drivers of Brain Drain, how various tax approaches have fuelled it, and how several European countries are using inventive tax schemes to address it.

A Primer on Brain Drain

Brain drain is the emigration of highly skilled workers from their home countries and is a defining concept in Europe over the past fifteen years, since the sovereign debt crisis. The drivers are easy to grasp: higher income, more opportunities, lower taxation, etc., but the push factors, why certain countries lose more of their talent than others, are more complex. Underfunded research sectors, tax burdens, low-paid contracts, and generally rigid labour markets are common culprits and tend to cluster in Southern and Eastern Europe. When you add high taxes to governments that are not delivering, you create an environment where educated people feel they are simply not getting a fair return. Free movement within the EU makes the mechanism run smoothly, meaning that once those conditions emerge, emigration becomes the obvious response.

European brain drain began in earnest with the sovereign debt crisis. Between 2007 and 2013, unemployment in Greece and Spain surged to around 28% and 26% respectively, with Portugal and Italy not far behind. This hit younger, educated workers hardest, many of whom left rather than sit in stagnant labour markets. Greece was the worst affected, with over 200,000 people leaving between 2010 and 2015, the large majority holding degrees. Italy followed a similar path and has since been left with an ageing population and a shrinking base of working-age professionals. Few cases illustrate the scale of this more than Romania. Working-age emigrants now exceed 2.6 million people, roughly a fifth of the country’s working-age population, and the emigration rate among the highly skilled is even higher. Over a quarter of Romanian doctors and nearly a quarter of nurses are now working abroad. Romania has also developed a class of digital emigrants who work remotely for foreign employers, pay little meaningful local tax, and have effectively opted out of the social fabric without ever leaving the country.

The brain drain is self-reinforcing. As the most qualified young people leave, growth slows, tax revenue shrinks, public services weaken, and more talented people leave. Shrinking tax revenues either force higher rates on those who remain or trigger cuts to the services that justified high taxes in the first place. Countries like Romania and Italy have been living this cycle for years.

What used to be a problem confined to poorer, peripheral economies has now spread. Even developed countries like Germany and France are losing professionals, particularly in technology and AI, to large firms abroad. The issue here is the inability to match the salaries, capital, and innovation ecosystems available elsewhere. Future unicorn companies leave the EU for the US at a rate around 120 times faster than the reverse, according to LSE research, and European venture capital, while improving, remains a fraction of its American counterpart.

The UK is perhaps the most compelling example, as it was once the destination for European talent and has now become a source. Approximately 7,500 millionaires left in 2024, and in 2025 that number rose to around 16,500, partly driven by the abolition of the non-domicile regime, which had allowed UK residents with foreign income to shelter overseas earnings from British tax, alongside broader tax increases under the Labour government. It is vital to note, though, that tax hikes are not a driver of brain drain on their own. They become one only when high taxation is not matched by the benefits or broader value that would justify it.

The Middle East has become a destination for global talent, particularly in Dubai and Abu Dhabi, for high-net-worth individuals and entrepreneurs. The zero-income tax offer, against the 40-50% rates common across Europe, is the obvious headline, but there is more. What the UAE has built is the infrastructure that makes long-term relocation genuinely viable, through the education system, hospitals, visa programmes, and top professions. The absence of inheritance tax and capital gains tax has also started attracting a different type of migrant: entrepreneurs thinking about building and transferring wealth across generations, rather than just earning a salary, and, in many cases, is now attracting wealthy citizens as well as those who are not. It is also worth noting that the current situation in Iran is posing safety concerns in the region, and while not affecting all areas equally, it has become a factor people are increasingly aware of when considering relocation, so we may see a slowdown in its attraction compared to the last 10 years.

The Differing Tax Philosophies of the World

To understand the root of this problem, we need to look at why European taxes are so high, where this came from, and why a model that worked for decades is now starting to fracture. The EU’s model of taxation is built on a social contract. Governments collect high tax revenue, and in return, citizens receive healthcare, universities, unemployment benefits, and pensions. The countries with the highest tax regimes, Denmark, France, and Austria, are also those with the most comprehensive welfare states. For most of the post-war period, citizens accepted this.

So, what changed? First, the globalisation of information, with citizens now seeing clearly what others earn abroad. Second, remote work broke down the link between location and employment, allowing citizens to be more mobile and to choose the region in which they pay tax. Finally, and more specifically for Southern and Central Europe, real wages have stagnated even as tax burdens have stayed high, and citizens now don’t have to accept this. The European model functions best when the government is efficient, and the services provided are genuinely high quality, as in Scandinavia, where citizens broadly accept high taxes because they believe revenues are being put to good use. However, in Italy, France, and Greece, the same level of taxation funds governments perceived as inefficient or bureaucratic, and the quality of public services simply does not justify the cost. This is the critical point: high taxes alone do not cause brain drain. High taxes combined with poor delivery do.

The US has a fundamentally different philosophy. The government plays a more limited role, and higher earners keep more of their income. The top federal rate sits around 37%, below the 40-50% common across Europe, and corporate tax is lower, allowing businesses to attract talent through equity and compensation structures that European firms struggle to match. We are also witnessing a growing divergence, driven by America’s booming tech sector and Europe’s relative stagnation in innovation, with European venture capital still lagging far behind. The American model works well for those in top professions, but leaves the bottom percentile significantly more exposed, with a thinner safety net than most of Europe. The benefit of this model, therefore, very much depends on where you sit in the income distribution.

The most unambiguous of the three models is the Gulf model. The UAE, Qatar, Kuwait, and Bahrain do not levy personal income tax. Oil revenues fund what European taxes pay for, and the absence of inheritance tax and capital gains tax is increasingly attracting entrepreneurs thinking about building and passing on wealth, not just earning it. For the Gulf, the strategy is essentially to build a wealth hub by investing heavily in infrastructure and quality of life, and deliberately using fiscal policy to attract global talent and capital. It is working, but it comes with limitations. Political freedoms are restricted in ways that matter to many of the people these countries are trying to attract, and there are genuine questions surrounding the long-term durability of this model, particularly given recent geopolitical tensions in the region and the future of oil revenues in this century.

The key point across these models is that taxation alone cannot determine the movement of talent; it is the relationship among taxation, opportunity, and the quality of state services that matters.

Europe’s Playbook on Brain Drain

European targeted tax incentives attract mobile, high-income, or lifestyle migrants, but they do not retain the broader skilled cohort nor reverse national outflows; they are a substitute for reforms that raise post‑tax lifetime earnings and confidence in institutional systems, hence are not fully able to act as a plug to brain drain.

The decisive variables in emigration are lifetime opportunity wage growth, job quality, promotion velocity, and institutional friction, while tax remains a second‑order price. However, this relationship weakens for high-income, internationally mobile workers, for whom low-tax jurisdictions such as the UAE can offer higher immediate returns despite weaker long-term career structures.

Italy, Spain, and Portugal have built inpatriate regimes that lower personal tax burdens, but these regimes operate on the margins of a much larger mobility system, so their macro effects are bounded, while their distributional footprint is large.

Italy’s 2024 inpatriate regime taxes only 50% of eligible Italian-source employment and professional income (a cap of €600,000) for the year of arrival and the four years thereafter. Eligibility requires high qualifications, non-residence for the three prior tax years (six or seven if returning to the same employer/group), and a minimum four-year stay; otherwise, benefits are clawed back. The exemption is further sweetened if the migrant has or gains a minor child, such that only 40% of the income is taxable. Italy also offers a separate flat-tax regime for HNWIs on foreign income, but this is not relevant for salaried workers.

Spain’s “régimen especial impatriados” taxes inbound workers as non-residents for the year of arrival plus five years; since 2023, it requires only five prior non-resident years (down from ten), expands eligibility to remote workers and certain entrepreneurs/professionals, and sets withholding at 24% on employment income with a higher rate on annual pay above €600,000.

Portugal’s (now closed) Non-Habitual Resident (NHR) status provided a 10-year window and applied specific tax treatment to high-value-added activities under Annex L. Hereby, entrants could suspend and later resume within the 10-year horizon. From January 1st, 2024, Portugal revoked NHR for new applicants and shifted to IFICI, a replacement incentive positioned towards scientific research and innovation.

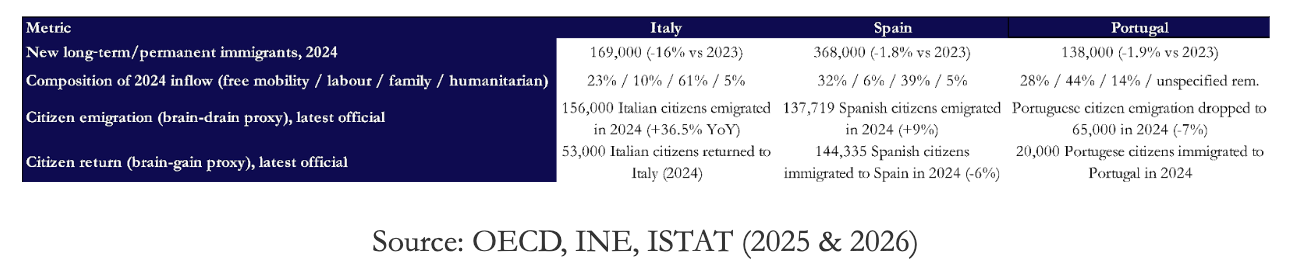

Coming to the key question, do these schemes move the needle on brain drain? The flow data says no. Italy received 169,000 long-term/permanent immigrants in 2024, down 16% from 2023, and most importantly, only 10% were labour migrants, while 61% were family migrants. At the same time, Italy’s outward movement accelerated: total emigrations reached 191,000 in 2024 (+20.5% YoY), including 156,000 Italian citizens emigrating (+36.5%). A tax break that applies to a capped income base and a narrow eligibility group cannot offset an emigration surge of that scale. Hence, we only see it create a small counterflow.

Spain’s large migration inflows mask a fundamental misalignment between migration and labour market needs. In 2024, only 6% of entrants arrived through labour channels, while the majority arrived via family reunification (39%) and EU free movement (32%), which are rights-based rather than demand-driven. As a result, migration is weakly targeted at sectors with persistent shortages, such as healthcare, engineering, and digital occupations, and cannot be expected to resolve them. This helps explain why positive net migration (+6,616 Spanish citizens returning to Spain) and even the coexistence of return flows of Spanish citizens with ongoing skill bottlenecks do not change the issue: it is not the scale of migration, but its composition. In this context, Spain’s immigrant regime operates at the margins, competing for a narrow pool of high-earning mobile workers rather than functioning as a tool for labour market adjustment.

Portugal’s inflow composition shows why the NHR never matched the brain drain. Portugal received 138,000 long-term/permanent immigrants in 2024 (–1.9% YoY), with 44% labour migrants and 28% free mobility, while Portuguese emigration stabilized at 65,000 in 2024 (-9% YoY). The most accurate evidence on Portugal’s “tax migration” response is concentrated among retirees. A Portuguese government working paper finds substantial international mobility following Portugal’s 2013 grant of a full exemption for foreign-source pensions, with responses concentrated among wealthier and more educated pensioners. The NBER summary confirms the mechanism by which retiree inflows dropped sharply when Portugal introduced a 10% pension tax in 2021. This again points to tax-driven migration rather than a fix to brain drain. In this way, Portugal experiences demographic and consumption inflow, often coupled with housing pressure, which explains why the NHR was ultimately revoked for new entrants from 2024.

Overall retention is the unmeasured variable that weakens the policy logic of Europe’s inpatriate regimes. While Italy, Spain, and Portugal define eligibility, tax treatment, and duration, no country tracks what happens after incentives expire. Italy enforces a four-year minimum stay through clawback but provides no evidence on post-benefit retention. Spain specifies entry conditions and tax benefits, but does not measure whether beneficiaries remain after those benefits expire. Portugal allows flexible use for up to 10 years, but does not publish exit behaviour once the regime ends. This creates a fundamental asymmetry in which countries evaluate policies based on inflows, while their success depends on long-term contribution. In practice, these regimes are calibrated around fixed time horizons and therefore induce time-bounded residence strategies among highly mobile workers. Hence, without retention data, it is impossible for us to distinguish between human capital accumulation and temporary fiscal arbitrage, leaving the core objective of these policies empirically unverified.

Finally, taxes compete with institutions and wages. Governance capacity varies across these countries. The World Bank WGI Control of Corruption percentile ranks place Portugal above Spain and Italy (Portugal ~74, Spain ~72, Italy ~68 in the latest compilation). When institutional confidence and career ladders diverge, tax discounts cannot compensate for perceived friction. That is why Spain can grow its labour force through migration alongside strong macro performance, while Italy’s outward pressure persists despite repeated tax tweaks.

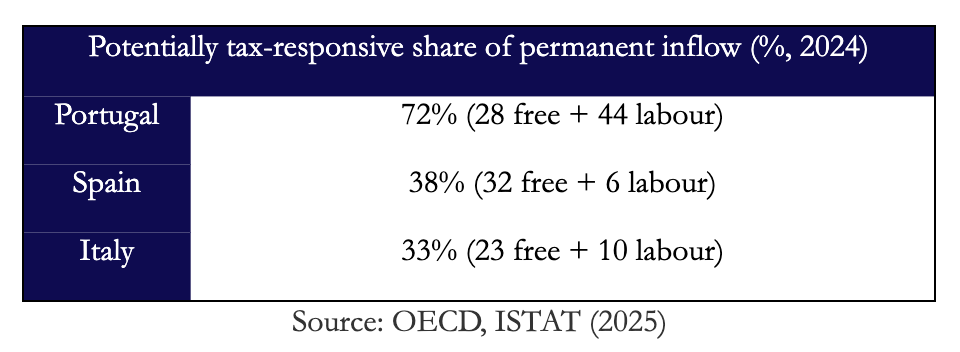

While European countries continue to attract significant numbers of long-term migrants, the composition of these inflows limits the effectiveness of tax-based policies. A large share of migration is driven by family reunification or other non-economic factors, while the segment most likely to respond to tax incentives, labour, and free-mobility migrants, represents only a fraction of the total. As a result, even well-designed tax regimes operate on a relatively narrow base, constraining their ability to influence overall migration dynamics. In Spain, over €105 million in tax expenditure was concentrated on just over 11,000 taxpayers.

While European countries continue to attract significant numbers of long-term migrants, the composition of these inflows limits the effectiveness of tax-based policies. A large share of migration is driven by family reunification or other non-economic factors, while the segment most likely to respond to tax incentives, labour, and free-mobility migrants, represents only a fraction of the total. As a result, even well-designed tax regimes operate on a relatively narrow base, constraining their ability to influence overall migration dynamics. In Spain, over €105 million in tax expenditure was concentrated on just over 11,000 taxpayers.

Tax Scheme Implications and Recommendations

A brain-drain policy based on personal tax discounts fails because it targets the wrong constraint. The binding constraints, as seen, are the domestic career ladder and state capacity, which determine whether skilled workers remain.

Hence, from the evidence put forward in the recommendations, follow:

- Countries must stop treating inflows as brain gain: Countries must require schemes to report retention KPIs (renewals, exits at year 6/10, etc., and post-benefit residence) as a condition for continuation, as today’s data on these KPIs are largely unpublished.

- Reallocate from individual tax discounts to sector-targeted labour instruments: As seen in Spain’s migration system, it is poorly aligned with labour demand, with only 6% of inflows occurring through labour channels, while the inpatriate regime concentrates fiscal resources on a narrow pool of high-earning individuals without directing them to shortage sectors. This combination limits both scale and impact. Redirecting comparable budget toward firm- and sector-linked tools, such as wage co-funding in shortage occupations, would target binding constraints directly, expanding effective labour supply where it is needed rather than subsidizing untargeted inflows. For example, Portugal’s newer IFICI ties tax benefits to employment in research and innovation, thereby shifting incentives from attracting mobile income to targeting scarce, high-skilled human capital.

- Clamping down on Arbitrage: Italy’s longer non-residence requirement for the same employer/group is the right anti-gaming architecture and should be adopted across the board.

- Countries can’t tax-cut their way out of weak institutions: Governance quality determines the retention of high-skill migrants; hence, incentives only work at the margin when trust and state capacity are already credible. Schemes must work in unison with institutional quality, i.e., credible governance, low administrative friction, and predictable enforcement.

Targeted tax schemes in Italy, Spain, and Portugal do not solve brain drain. They buy incremental, time-bound inflows of tax-sensitive migrants, while outward pressure is driven by wages, career structures, and confidence in the country’s institutions. All in all, regimes also institutionalize inequality by privileging newcomers over residents and by converting the tax system into a mobility subsidy.

A key argument against the evidence presented is that fewer but higher-income migrants could offset brain drain, which misunderstands the nature of the problem. Brain drain is not a shortage of tax revenue, but a loss of domestically trained human capital. Tax incentives may attract globally mobile high earners, but these individuals are, by definition, the most likely to relocate again. Their presence does not compensate for the continuous outflow of locally educated workers, nor does it rebuild the domestic talent pipeline.

Conclusion

Taxes are fiscal instruments that reflect a country’s approach to providing public goods. As previously discussed, the rise of a more global workforce and economic system has also made taxes reflect migratory policy. Tax systems have faced a reckoning. Consumers and workers need to feel that the price they pay for government goods and services matches their actual usefulness, or else they leave. The various schemes Europe has employed have been successful, but raise a key question. Is this simply a Band-Aid for a larger issue? If the hull of a ship has a leak, simply pumping out water isn’t an effective plan for the long-term viability of the ship. These tax schemes may be successful in the short term, but they fail to address the underlying issues that led people to leave. If Europe wants to truly fix Brain Drain, it must utilise these tax schemes while also increasing incomes and opportunities, and reform rigid labour structures. If this isn’t accomplished, the only lasting legacy of these programs will be lost tax revenues and increased financial inequity.

0 Comments