Introduction

Athleisure is the 21st century trend defined by the unique combination of athletic comfort and the fashion quotient of leisure apparel, creating a contemporary style of clothing. It mainly refers to apparel designed for athletic and fitness activities, as well as casual wear at workplaces or at social events. Unlike traditional activewear, which mainly serves the purpose of performance, athleisure occupies an intermediate space between sport and lifestyle, emphasizing a variety of characteristics such as versatility, comfort, and aesthetic appeal. The global market was estimated at $439.6bn in 2025 and is projected to reach $623.5bn in 2030, driven by a 7.24% CAGR. Four main drivers can be identified at the basis of the popularity of athleisure: health and wellness awareness, versatility, influencer and celebrity endorsement, and the casualization of fashion.

Pioneered by brands such as Lululemon [NASDAQ: LULU] at the start of the last decade and subsequently embraced by giants including Nike [NYSE: NKE], ASICS [TSE: 7936], and Columbia Sportswear [NASDAQ: COLM], along with digital-native challengers like Gymshark, the market has become both expansive and highly competitive. To the aforementioned brands are added other significant players, including Adidas [XETRA: ADS], Athleta, Authentic Brands Group, H&M [STO: HM-B], Puma [XETRA: PUM], and Under Armour [NYSE: UAA].

Market Drivers and Restraining Factors

The recent rise in athleisure demand is mainly driven by a change in usage occasions. Consumers increasingly want clothing that is comfortable, stylish, and functional, and that can be worn for workouts as well as daily life (errands, commuting, travel, and even “smart-casual” work settings). Grand View Research explicitly links growth to the shift toward “casual and adaptable attire” and to the ability to transition between gym sessions and everyday activities.

A second driver is the growing focus on health and fitness awareness. “Active lifestyle” habits have made athleisure relevant to a much wider group of consumers, and as exercise becomes increasingly relevant in everyday routines, more people are looking for clothing that is comfortable yet still performs well. This shift has led to a higher willingness to pay for athleisure products, contributing to the recent market growth.

There has also been a gradual shift in workplace norms toward comfort, further reinforced by remote and hybrid work. This has broadened the ‘acceptable’ range of clothing for work settings, especially for people who commute and regularly move between home and office settings. COVID-19 was a major offset to this shift, as this was the first time people worked remotely at scale and became accustomed to dressing for comfort during the workday. Even after restrictions ended, these habits partially remained.

This shift is amplified by social media, as it increases athleisure’s online visibility. Platforms such as Instagram and TikTok show consumers how athleisure can be styled in everyday life, allowing them to picture the same products in their own routines. This visibility also emphasizes the importance of community-building as a competitive advantage. Brands like Alo Yoga expand through product quality, but also by creating like-minded communities through pop-ups, wellness events, and digital engagement. This positions such brands as more than activewear labels, but rather as brands that build loyalty through positive and relatable experiences. When athleisure is bought as part of a lifestyle, this brand experience encourages repurchases and supports premium pricing, even when competing products are similar.

However, these demand drivers do not eliminate the market’s main restraining factors but rather make it more competitive. The expansion of athleisure intensifies competition, and changing trends expose the market to supply chain risks. Since the market is relying heavily on global sourcing and long production timelines, an increasing difficulty arises in responding to sudden demand changes. This is especially relevant in the athleisure market, as product ‘newness’ matters. This market growth is attracting both incumbents and new entrants, causing brands to increasingly compete through performance features, product breadth, and distribution, which pushes for further innovation. As a result, differentiation becomes costly, due to not only requiring investments in fabrics and design, but also in marketing and distribution.

As consumers are expecting more transparency about materials and supply chains, increasing pressures around sustainability and inclusivity pose another challenge. Many brands are thus expanding their size ranges and inclusive assortments, raising production costs and inventory risk. Regulations regarding labour practices and supply chains reinforce these expectations. An example of this is the Corporate Sustainability Due Diligence Directive (Directive (EU) 2024/1760), which took effect on July 25, 2024, increasing the need for companies to address human rights and environmental impacts across their operations and value chains.

Counterfeit products are another significant challenge for firms, especially premium brands relying on their pricing power. According to the OECD, the most targeted sectors are footwear and leather goods, accounting for 62% of seized counterfeit items in 2021. The relevance for athleisure lies in the fact that many products are relatively easy to replicate visually, and consumers struggle to assess fabric and performance quality claims online.

Product Segmentation

The athleisure market can be broadly split into mass and premium segments, which can be further segmented by type and end-user.

Difference between the Mass and Premium Segments

The mass segment’s demand is primarily driven by affordability and accessibility. Mass athleisure accounted for about 66% of revenue in 2023, indicating the category’s scale is based on products reaching a wide consumer base through mainstream distribution. Frequent online purchasing, quick design turnover, and fast restocks also greatly contribute to the segment’s dominance. In contrast, premium athleisure is more about pricing power. It is projected to be the fastest-growing segment, with an expected 10.5% CAGR from 2024 to 2030. This reflects consumers’ willingness to pay more for product differentiation and quality. Premium brands are becoming increasingly dependent on brand loyalty and consumer satisfaction to justify their higher prices, which again links back to the community-building practices mentioned above.

Differences in Type

Based on type, the athleisure market is segmented into topwear, bottomwear, footwear, and other items. Within this structure, bottomwear has historically accounted for a large share of the market and dominated it in 2020, due to the frequent wear of leggings and joggers during COVID-19. While topwear as a whole is not as dominant in the market, product-wise, shirts led the market with a 38.5% revenue share in 2023, tying back to the idea that core items drive a large part of category scale. These products are not just bought for training, but also for commuting, travelling, and casual settings, leading to more frequent purchases than more technical items. Footwear is the fastest-growing category within athleisure, because it works both as a functional product and as an everyday item. Shoes, specifically sneakers, are also a strong brand signal. An example of this is Nike [NYSE: NKE], as its shoes are easy to recognise. This increases brand visibility, especially because sneakers can also be worn outside of training. Furthermore, consumers are willing to pay higher prices for shoes, relative to other clothing items, making footwear strategically attractive to brands seeking to increase customer value. The ‘other items’ segment is smaller. It includes accessories and secondary categories such as socks, caps, and bags. Although these products do not drive market growth on their own, they can reinforce brand identity. This, again, is crucial for premium brands.

Differences in End-User

The athleisure market can also be segmented into products for men, women, kids, and unisex. Among end-users, women remain the largest segment. They led the market with the largest revenue share of about 47% in 2023, which reflects both the category’s historical development and the breadth of women’s athleisure assortments. However, growth is also increasingly coming from expansion in men’s and kids’ categories. Brands have started to offer more options and frame athleisure as everyday clothing. With this, the men’s segment has been growing too, as seen in both product design, with more neutral pieces, and in brand positioning. The children segment is also expected to grow at a CAGR of 8.3% from 2024 to 2030. This is mainly driven by increasing participation in sports and growing awareness around health outcomes, such as childhood obesity. Nonetheless, the market is not that youth-skewed. Weekly athleisure wear is led by millennials, who make up 39% of weekly wearers, followed by Gen X at 33%, Gen Z at 22%, and baby boomers at 6%.

Geographical Presence and Outlook

The athleisure market is segmented into five regions: North America, Europe, Asia Pacific (APAC), South and Central America (SCA), and the Middle East and Africa (MEA). North America is currently leading the market, with approximately 41% of revenue share in 2023. This is due to high consumer spending and athleisure already being widely adopted in society. However, because it is the most established region in terms of scale, it is also the most competitive one, as brands compete on performance features and brand positioning.

At the same time, APAC is expected to be the fastest-growing region, with a revenue projected to reach $170.4bn by 2030, and an 11.1% CAGR from 2024 to 2030. This growth is mainly linked to APAC’s demographic scale and the increasing demand for athleisure, as well as to supply-side advantages. Additionally, many APAC countries, such as China, India, and Bangladesh, already have large textile and manufacturing locations, making fabrics widely available, thus allowing faster distribution and growth for brands. This distribution potential can be seen in the strategic partnership between Decathlon and Myntra, announced in November 2024. Decathlon’s sportswear became accessible on Myntra across tier 1,2, and 3 cities, covering almost 98% of deliverable locations.

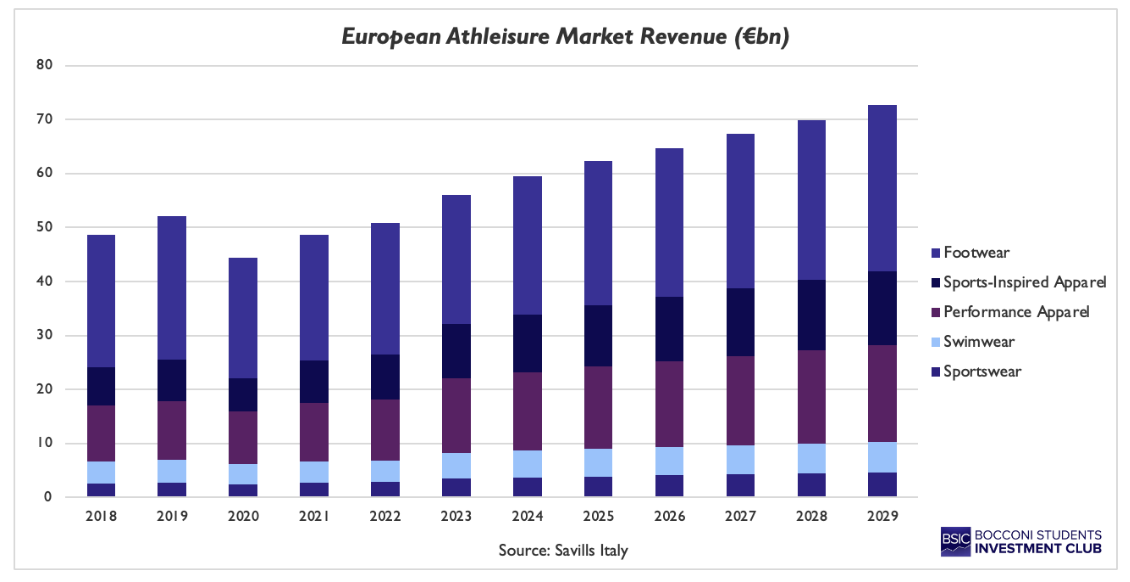

Europe has also become increasingly relevant, with premium and emerging brands opening more stores across major cities. The European athleisure market was estimated at €59.5bn in 2024, with an expected CAGR of 4% between 2024 and 2028.

Athleisure’s growth in Europe can also be explained by brands’ market strategies, because many tend to follow a clear path. First, they build brand awareness online and then expand through partnerships with established retailers. Only later do they invest in flagship stores in prime locations. As flagship stores are not just about sales, but also about visibility and community, they contribute to consumers’ brand experience. Opening these stores only once a certain brand loyalty has been established is thus logical, especially because athleisure is increasingly bought as part of a lifestyle, for which brand experience matters. This can be seen in recent store expansions by brands such as On and Alo Yoga. Both have increased their physical presence in European cities, using prime locations to strengthen brand awareness and credibility.

Athleisure’s growth in Europe can also be explained by brands’ market strategies, because many tend to follow a clear path. First, they build brand awareness online and then expand through partnerships with established retailers. Only later do they invest in flagship stores in prime locations. As flagship stores are not just about sales, but also about visibility and community, they contribute to consumers’ brand experience. Opening these stores only once a certain brand loyalty has been established is thus logical, especially because athleisure is increasingly bought as part of a lifestyle, for which brand experience matters. This can be seen in recent store expansions by brands such as On and Alo Yoga. Both have increased their physical presence in European cities, using prime locations to strengthen brand awareness and credibility.

SCA and MEA remain smaller in overall scale, but they still represent long-term growth opportunities as fitness participation increases and athleisure slowly becomes more mainstream. In these regions, demand growth is often shaped more directly by affordability and distribution coverage. Premium strategies can also be more exposed to challenges such as counterfeits and bad retail infrastructure, making it harder to scale consistently across countries.

In addition to those regional dynamics, distribution channels also play an important role in how athleisure brands grow. With 33.5% of total revenue in 2023, sporting goods retailers remain the main distributors, with their specialist focus reinforcing perceptions of technical credibility and product quality. However, the online segment is becoming increasingly important too and is expected to grow at the fastest CAGR of 11.5% from 2024 to 2030. This is due to companies being able to maximize brand exposure and experiment with brand reception, without having a physical presence. Many brands combine these channels by scaling digitally, while investing in flagship stores in prime locations, as is the case in Europe.

Celebrity Endorsement

Athleisure marketing heavily relies on celebrities wearing and promoting a specific brand. This trend is not recent; it has been ongoing for years, and marketing strategies have adapted to changes in the consumer audience. The movement initially started with high-profile athletes, whose global recognition translated into strategically valuable sponsorship opportunities. These sponsorships associate their products with discipline and hard work, making it an honor to wear the same clothes as your idols. On that note, one of the biggest sports sponsorship deals in history was the partnership between Michael Jordan and Nike, valued at $1.3bn, that started in 1983 and made Nike’s Air Jordan sneakers among the best-selling shoes in history. Other deals with similar impact include Lionel Messi and Adidas for $1bn and Roger Federer and Uniqlo for $300m.

The turning point occurred around 2016, when Instagram rapidly reached over 500m users and introduced new key features such as Instagram Stories and Instagram Lives. Celebrities started promoting sport brands, not as gym wear but as day-to-day fashion. They were being seen wearing leggings and yoga pants while shopping and going out. Two main partnerships catalyzed this shift. In 2016, Beyoncé collaborated with Topshop for an athletic streetwear label, launching Ivy Park. The joint venture was promoted on Instagram, with coordinated drops and fan engagement. Having a non-athlete with strong influence in fashion as Beyoncé promote sportswear as a lifestyle drastically changed the way athleisure was viewed. Additionally, promoting it on Instagram led to reaching a higher, younger audience, while athleisure became easily shareable, eventually turning into a trend. Similarly, Rihanna’s collaboration with Puma [XETRA: PUM] merged high fashion with athletic wear, featuring multiple runway shows during fashion weeks across the world. Puma’s sales rose 16%, and the share price reached $200 after Rihanna’s involvement. Rihanna also used Instagram to announce the collaboration, reaching 2.4m likes on her post about the collaboration, and Puma gained access to Rihanna’s 63.6m followers. Both collaborations drastically influenced clothing trends, making athleisure a lifestyle, increasing its demand.

The rise of social media led to the rise of influencers. Studies have shown that more than half of Gen Z prefer to do their searches on TikTok, so brands must promote their products in under 15 seconds to capture viewers’ attention. An ad showing the benefits of using their products is increasingly insufficient, and a more personal recommendation is needed. This is where influencers assume strategic importance; seeing real people use and introduce the product in their everyday lives builds reliability. A recent survey in Europe showed that younger audiences are more likely to buy products they’ve seen on influencers rather than celebrities. Creator economy is expected to be worth $480bn by 2027, with influencers making billions for brands around the world; advertisers are swapping traditional actors and celebrities for influencer sponsorships. Fabletics, a stylish activewear brand founded in 2013, has a marketing influencer program that collaborates with all sorts of influencers across the media; Alo Yoga uses Kendall Jenner to star in their “ Luxury is wellness “ campaign; Skims, the billion-dollar company owned by Kim Kardashian, has collaborated with over 45 influencers and partnered with Team USA for the Winter Olympics in Milan.

Celebrity endorsements are strategically placed for market segmentation and not just brand visibility. There has been an increase in marketing for menswear, showing that expansion into menswear is relevant for growth and diversification. Athleisure has mostly been skewed towards women, with most of these brands starting from yoga or pilates apparel, an activity also skewed towards women. The men’s sector is starting to grow as there is increased male participation in wellness lifestyles and hybrid work environments. A brand that took the first step in expanding into menswear is Lululemon [NASDAQ: LULU], which recently made F1 legend driver Lewis Hamilton their ambassador. This allows the company to reduce its dependence on a single sector and compete better against other brands.

Luxury Collaborations

In recent years, collaborations between sportswear and luxury fashion brands have advanced from occasional experiments into one of the most effective forms of brand reinvention, extending the market reach for both parties. Both the increase in demand for athleisure and the casualization of fashion have led luxury houses to assess their relevance in a market where consumer preferences are shifting toward experiences and value-driven brands.

Luxury brands have used limited exclusive drops to attract attention to their new partnerships. Pieces are listed on resale sites for double the price at which they are being sold, causing a fear of missing out among consumers. The hype around products creates a desire to acquire the piece before it completely disappears from the market, and the scarcity model used by brands can lead to them charging higher prices. Some collaborations help up-and-coming designers gain recognition, while others make luxury pieces accessible to a broader audience. Some argue that this dilutes the exclusivity of luxury brands; however, this is a strategic move for both brands: the luxury brand reaches a new audience and maintains relevance while the sports brand taps into a new market, selling sportswear at much higher prices, improving brand image through exclusivity.

Some collaborations include Nike x Jacquemus, an alliance between the French brand’s iconic, feminine, and minimalist style blended with Nike’s vintage models. The collection is much cheaper than most of Jacquemus’s products and can be worn in multiple settings. Jacquemus is mostly known for elevated pieces and mixing this with Nike’s basic sportswear results in luxury athleisure. Adidas x Gucci followed the trend and created a retro, sporty look, with Adidas reinforcing itself in the high fashion world and Gucci breaking into the sports market.

Lululemon Struggles in 2025 and Emerging Brands

Lululemon was founded in 1998, in Vancouver, Canada, and opened its first store in 2000. In the vast majority, Lululemon’s advertising comes from social media platforms such as TikTok and Instagram. The company’s profits really boomed after the pandemic, when hybrid work took over, and people were looking for comfortable clothing. The company continues to diversify into various categories and even acquired a tech and in-home exercise startup, Mirror, for $500m, in June of 2020. The company’s growth has slowed down recently, raising concerns for the future competitiveness of the brand.

The market is becoming increasingly saturated and fragmented, with multiple competitors joining the market, such as Alo Yoga and Vuori (valued at $5.5bn in 2024). Moreover, according to retail analyst Neil Saunders, there is a lack of quality control in the Canadian company, with a scandal regarding their leggings being see-through. For a company that charges almost $200 for a pair of leggings, consumers expect the highest quality. Additionally, the company’s CEO recently stepped down, and as of now, no successor has yet filled the gap. The US tariffs have also subdued consumer spending, with a 5% decrease in sales in North America in November 2025, compared to the same period last year, when sales increased by 4% in the same region. Shares of the company have also fallen by 45% in the past year and are now valued at $24.8bn ($186 per share as of February 27, 2026). Lululemon still holds the second largest share in the market (21.2%) after the giant Nike (31.6%).

Lululemon’s ability to keep its relevance in the market depends on its capacity to increase investment in innovation and stop bringing bad press to its name. The company has already taken some steps to fight the decline in growth: expanding men’s apparel by appointing Lewis Hamilton as ambassador; promoting their “Like New” resale program and smart fabric R&D aimed at aligning with sustainability targets; all while maintaining a 58.85% gross margin and using AI-driven demand forecasting. The athleisure market is no longer only about quality, but also about price, cultural relevance, and values. Lululemon’s decline in growth is not necessarily a concern, as it is post-pandemic boom, as long as it’s not long-term and Lululemon appoints creative leaders to maintain relevance.

Conclusion

Athleisure’s expansion reflects more than a cyclical fashion trend; it signals a structural realignment of consumer preferences toward versatility and comfort. As there is an increasing blur in the boundary between everyday wear and performance, the segment has evolved into one of the dynamic ones within the global industry, supported by the rise in work-from-home options and digital influence.

However, sustained growth does not eliminate competitive pressure. The industry suffers pressures from market fragmentation, supply chain risks, rising marketing intensity and regulatory scrutiny. Both established giants and emerging local brands are competing for consumer attention: the former innovate to retain their market share, while the latter are gaining traction by offering unique products.

In a market projected to surpass $600bn by 2030, comfort may be the defining driver of demand, but strategic execution will determine who captures its economic value. The active and health-conscious consumer base seemingly has an insatiable appetite for athleisure, and it is a group that analysts predict will continue to grow in the coming years. Brands that can pivot to exciting new shapes and categories by elevating and diversifying their offer while building strong narratives with customers will be the ones to leverage that demand.

0 Comments