Introduction

For some simply a winter activity, the skiing business is one of the most structurally interesting and unique operations in the global leisure industry. Geographical scarcity, high cyclicality, weather dependency and capital intensity have motivated the once dispersed industry to consolidate in recent decades. Global players such as Vail Resorts [NYSE: MTN] and Compagnie des Alpes (CDA) [EPA: CDA] have emerged with two opposing business models: one focused on vertically integrated, subscription-based scale and shareholder-driven expansion, the other on concession-based operations embedded within regional tourism ecosystems and public governance structures. This poses the question of how two companies operating on similar slopes, both facing climatic and cost pressures, can arrive at such fundamentally different versions of alpine capitalism.

Structural Economics of Ski Resorts

The ski industry has undergone significant changes in its underlying economic model over the course of the last decade. In the United States, in particular, companies such as Vail Resorts and Alterra Mountain Company have transformed skiing into a business model based on season passes such as Epic and Ikon. The primary logic is quite straightforward: you collect payment before the season starts, thus stabilizing cash flow and minimizing the financial risk of a poor snowfall year. At the same time, the season passes build up a base of loyal regular visitors who return again and again during the season. This creates a clear compromise between guaranteed, stable income and weather risk protection through the sale of season passes on the one hand, and high profits during the peak season through high-margin day passes on the other. Ultimately, striking this balance is crucial to the financial performance of modern ski operators.

Today, U.S. ski resorts are designed to be a sophisticated business model that aims to maximize customer spending at every stage of their stay. The modern ski industry has evolved from simply selling lift passes to creating an interconnected ecosystem that revolves around the skier, with most of the revenue generated outside of the ski lift. Once guests arrive the resort turns into an enclosed ecosystem. First-timers not only purchase a lift ticket, but also pay for ski lessons, rent equipment, and often make purchases on-site. Because alternatives are limited and convenience plays a major role, ski schools, rental shops, and retail stores obtain attractive margins and keep spending within the resort, rather than losing it to independently-owned businesses. Spending also occurs off the slopes. Mountain restaurants and lodging are often owned by the resort operator, especially in the U.S., creating a model of complete guest lock-in where visitors eat, sleep, and relax within the same corporate ecosystem. In addition, the existing resorts are located on very scarce land, as new, prime ski areas in the U.S. are highly limited due to land constraints. As a result, ski resort operators develop and sell luxury apartments and hotels in order to finance new lifts and infrastructure.

In Europe, the structure looks quite different. Many resorts operate under the system in which municipalities own the mountains and lease operating rights to privately held companies. Accordingly, the business becomes somewhat similar to a utility company, with an emphasis on stable, high-volume, and highly efficient operations. Despite these structural differences, the outcome is very much the same on both continents. Ski resorts benefit from geographic scarcity, high barriers to entry, and vertically integrated services. This creates a business model that combines recurring revenue, locked-in demand, and limited competition, resulting in a strong competitive advantage.

From a cost perspective, ski resorts are marked by high fixed costs and extreme seasonality. The core infrastructure, such as ski lifts, snowmaking and slope grooming equipment require significant upfront investment and ongoing maintenance, irrespective of the number of skiers visiting the resort. Another significant cost factor is staffing. From lift operators and ski instructors to reception and security staff, many employees must be hired and trained before the start of the peak season. This poses a challenge, as revenues are generated over a period of approximately four to five winter months, while costs, such as depreciation, debt servicing, land leases, insurance, and administrative expenses are incurred throughout the entire year, even after the snow has melted. Added to this structural imbalance is the weather risk. A mild winter or low snowfall can reduce visitor numbers and put a strain on pricing power. As unpredictable and shorter winters become more common due to climate change, artificial snowmaking has become a strategic necessity rather than an option for most operators. Ski resorts invest heavily in advanced snowmaking technologies to ensure an early start of the season and capture the peak holiday periods. Yet these systems consume large amounts of energy and water, further amplifying the high fixed costs of the business. The result is a model with strong operating leverage in favorable seasons but significant downside risk once the conditions turn unfavorable.

Altogether, a clear picture is emerging. Ski resorts have to cope with an inflexible cost base, a seasonal calendar that concentrates revenue into a few winter months, and a growing need for investment in snowmaking equipment as winters become less and less reliable. Yet geographical differences emerge. In the U.S., conglomerates have built vertically integrated ecosystems that monetize the full ski experience and secure revenue upfront via season passes, while in Europe fragmented operators and concession-based governance structures reduce lock-in and pricing power, leading to materially lower day-ticket prices.

U.S. vs. Europe: The Pricing Paradox

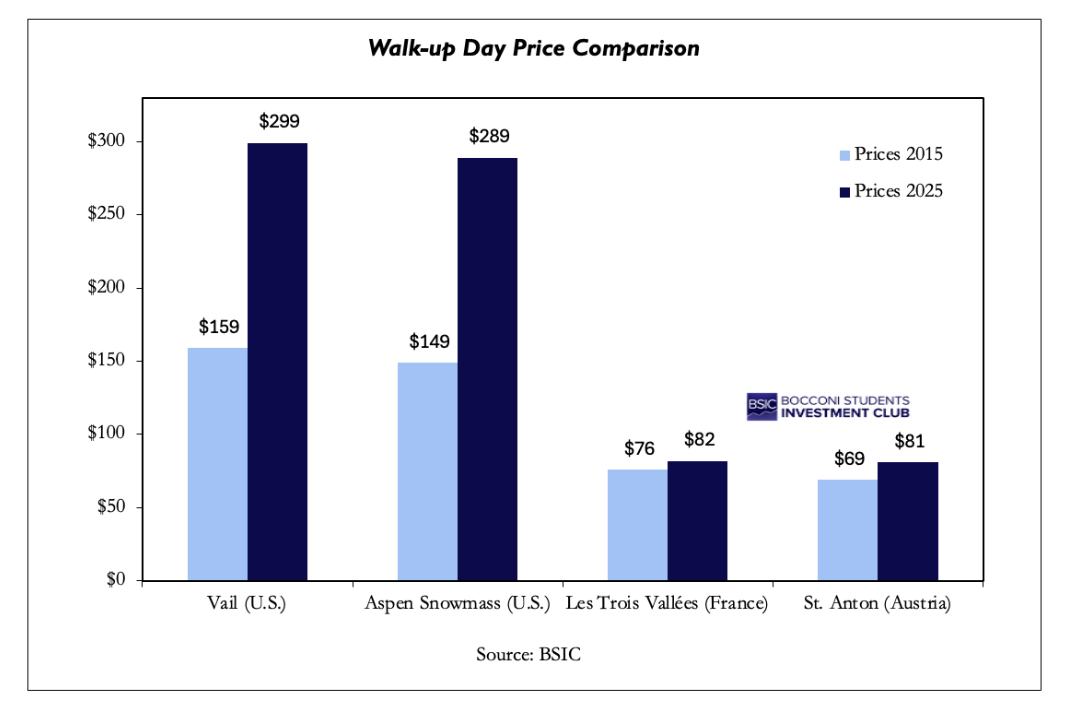

A skier driving two hours from Denver into the Rockies will likely encounter a striking number at the ticket window, with a single day lift ticket at a major U.S. destination resort frequently exceeding $250 and approaching or surpassing $300 in peak periods. In contrast, a day pass in the French or Austrian Alps is typically priced at approximately €70. American consumers may pay roughly four to five times more for seemingly the same product, even after currency conversion, a ski pass providing access to lifts and terrain. This divergence is not a result of snow quality, infrastructure conditions, or climate risk. Both regions operate in capital-intensive, weather-dependent environments with high fixed costs and short revenue seasons. The pricing gap is rather reflected by differences in ownership structures, market concentration, geographic competition, and contract design. The “pricing paradox” is institutional rather than operational.

In much of continental Europe, ski lift infrastructure is the result of a public or quasi-public framework. Taking France as an example, many large resorts operate under municipal concession agreements known as délégations de service public (DSPs). Operators manage lift systems on behalf of local authorities under long-term contracts. Compagnie des Alpes, one of the largest operators in the French Alps, is approximately 43% owned by Caisse des Dépôts, a French state financial institution. While these entities still value profit, their governance structures also prioritize regional development, tourism policy, and long-term concession stability. Lift systems are viewed as economic infrastructure for mountain communities. In the U.S., by contrast, the dominant destination resorts are controlled by publicly listed corporations with explicit mandates to maximize shareholder value. Investor communications emphasize metrics such as revenue per skier visit, yield management, and advance commitment. Pricing strategy is framed in terms familiar to hospitality and subscription businesses rather than regional economic policy. Ski infrastructure is not treated as quasi-public but rather positioned as a premium consumer product.

These incentives are reinforced by market structure. The Alpine market remains highly fragmented. Hundreds of operators compete across France, Austria, Italy, and Switzerland, often within dense geographic clusters. Skiers can substitute between nearby domains with relative ease, particularly for day trips. Even large, interconnected areas operate within broader competitive ecosystems. The U.S. industry has consolidated significantly over the past decade. A small number of multi-resort operators control a large share of destination mountains. Competition increasingly occurs at the level of national pass networks rather than individual resorts. From an industrial organization perspective, this shift moves the market closer to an oligopoly. Greater concentration, particularly in destination locations where consumers incur travel and lodging costs, enhances pricing power. Geography compounds this effect. The Alpine landscape allows for tighter regional competition; consumers can often choose among multiple nearby resorts within a single trip.

The most important structural difference, however, lies in contract design. The rise of large multi-mountain season passes in the United States has fundamentally reshaped ski economics. Products such as the Epic and Ikon Pass collect revenue months before the season begins. They transfer part of the weather risk from operator to consumer, smooth demand across mountains, and encourage loyalty within a closed network of resorts. Economically, this resembles a two-part tariff: a substantial upfront fixed payment in exchange for very low marginal cost per visit. Within this framework, the high walk-up day ticket price plays a strategic role. It acts as an anchor, encouraging advance commitment and subscription behaviour. The day ticket is no longer the central product but rather a fallback option, which is often priced at a premium. Access becomes cheapest for those who pre-commit and ski frequently. Europe lacks an equivalent continent-wide mega-pass system of comparable scale and dominance. While multi-day and regional passes exist, day tickets remain a primary access mechanism, and pricing remains flatter across user types. The absence of large-scale subscription lock-in reduces the incentive, and arguably the ability, to impose extreme walk-up pricing.

The distributional consequences are significant. In the U.S., skiing remains relatively affordable for committed, higher-frequency participants who purchase passes in advance. For occasional or spontaneous participants day pricing can be prohibitive. With lift ticket inflation outpacing general CPI in recent years, the perception that skiing is shifting from broad recreational activity toward premium leisure consumption has been intensifying. In Europe, more moderate day pricing sustains broader participation and preserves skiing’s mass-market character.

The result is not simply a difference in price levels but a divergence in economic philosophy. The American model prioritizes yield optimization, capital market performance, and network effects. The European model, shaped by public ownership structures and dense regional competition, emphasizes accessibility within a tourism ecosystem. Both operate in the same mountains, under similar climatic pressures. Yet their pricing reflects two distinct versions of alpine capitalism.

Case Study: Vail Resorts vs. Compagnie des Alpes (CDA)

To highlight the economic and cultural divergence of skiing between the U.S. and Europe we can analyze the business models of Vail Resorts and Compagnie des Alpes. Both face the same pressures mentioned before: high fixed costs, climate change resulting in shrinking seasons, and rising labor and energy expenses that compress margins and increase operating leverage.

Vail has spent the last decades building an empire of over 40 resorts worldwide. World famous resorts such as Beaver Creek, Park City Mountain, and Heavenly in the U.S., former 2010 Winter Olympics venue Whistler Blackcomb in Canada, Perisher, Falls Creek, and Hotham in Australia and European champions such as Andermatt-Sedrun-Disentis (majority stake) and Crans-Montana in Switzerland (acquired recently in 2022 and 2023). Their business model is based on the logic that each new resort added to the Epic Pass increases its attractiveness and justifies a higher value for customers, thus a higher price. In 2025, Vail Resorts alone generated almost $1bn in upfront payments via its Epic Pass, with season passes accounting for approximately 64% of total lift revenue. This money is collected before a single lift turns, absorbing the traditional weather risk a lot of European ski resorts struggle with.

Vail has perfected vertical integration. Lift tickets can be seen as the anchor product, but Vail covers the entire value chain of skiing from season pass sales to ski and snowboard schools, equipment rentals and retail shops, on-mountain dining and après-ski venues. It is even possible to live in Vail’s lodging properties, vacation rentals, and hotels during your stay or purchase your personal home through their resort property management. Furthermore, they have also expanded into summer mountain activities and events, such as mountain biking, alpine coasters, hiking access, zip lines, scenic gondola rides, concerts, festivals, and corporate or private events, to counter the seasonal cyclicality of their business model. In comparison, European venues benefit from many smaller, local offerings creating a competitive market to serve a variety of prices and preferences. For example, the ski resort may be owned by the local municipality, the ski school and a restaurant by a larger Swiss/Austrian/Italy company, and the hotel by a private individual.

Before analysing Vail’s financials, it is important to note that their fiscal year runs from August 1st to July 31st to capture an entire ski season and improve understandability. In 2025, net revenue increased by 2.7% to $2.96bn of which 89% resulted from their main operations (lift revenue, ski school, dining, and retail), while the rest was made up from housing services such as Lodging and Real Estate. During the year the price of the Epic Pass was increased by 7%. This was the main contributor to the increase in revenue as total skier visits and pass units sold decreased for the consecutive year, raising questions about the future of the business model. Overall, this translates into a comfortable EBITDA margin of 30% and net income of $280m in 2025 (+21% from 2024). In comparison, CDA’s revenue is more diversified into three divisions: Ski Areas and Outdoor Activities, Leisure Parks, and Distribution & Hospitality. Ski Areas contributed €600m to the €1.4bn in revenue in 2024 (o/w ski lift operations accounted for 95%), operating at a 37% EBITDA margin, and seeing an increase in skier-days to 13.9m (+100k) from the prior year. Thus, CDA’s concession-based lift operations generate higher EBITDA margins than Vail’s but group margins appear lower due to the Leisure Park operations that operate at structurally lower margins. Still, they are an important leg of their business model as they supplement the loss in revenue in the summer for the company, a strategy Vail might consider adopting to diversify revenues further and reduce cyclicality.

A major difference in the operation of the two companies can be found in their capital expenditures. In 2025, Vail totalled CapEx of approx. $249–25m. This is split between $198–203m in core maintenance and resort investment (e.g. lift replacements and snowmaking) and $51m of European growth and real estate projects. It can be estimated that especially investments in snowmaking infrastructure will increase due to climate concerns in the next years/decades. Since 2015, the company has already invested over $100m across its operations. CDA’s CapEx is more diversified with only €106m flowing directly into ski areas and the majority of €135m being invested in summer operations in leisure parks (e.g. new attractions at Parc Astérix and Futuroscope). Thus, it is evident that the two companies are investing in fundamentally different things: Vail is spending to defend and deepen the Epic Pass value proposition, with technology and guest experience as the connective tissue, while CDA is allocating capital across two structurally distinct businesses. It focuses on long-term reinvestment, as its growth is constrained by state-linked governance and a more conservative financial culture forcing debt reduction and dividend payments.

The divergence in business models, governance structures, and growth trajectories between Vail and CDA is ultimately crystallised in the way capital markets price each company. Vail currently trades at an EV/EBITDA multiple of approximately 8.8x on a trailing basis, with a market capitalisation of $4.8bn and an enterprise value of $7.6bn. CDA, by contrast, trades at an EV/EBITDA of approximately 4.9x, with a market capitalisation of roughly €720m and an enterprise value of €1.5bn Vail Resorts, Inc. This is a discount of nearly half, applied to a company that, within its ski areas division alone, generates higher EBITDA margins than Vail’s mountain segment. This valuation gap could be explained by the limited number of free float shares in CDA (43% owned by Caisse des Dépôts) but is better supported by the concession model. On one hand this provides long-term revenue stability, but it also caps upside to the company. Markets seem to reward Vail’s theoretically unlimited capacity to buy new resorts, adjust prices, and expand aggressively. Overall, this gap reflects not just different businesses but two different theories of what a ski operator can ultimately become.

Conclusion: When the Snow Stops

The structural and financial analysis above assumes one critical input that neither company controls: that the mountains will remain skiable. Increasingly, that assumption demands scrutiny. In the Alps, snowpack duration has shortened by approximately 8.9 days per decade across monitored stations between 1970 and 2015, and a warming of just +2°C is projected to cut the ski season in Switzerland by approximately 20%. This is a global threat to the operating environment of both Vail and CDA, which must be mitigated by investment decisions made today. Changes in weather will not affect all resorts equally due to differences in latitude, terrain, and most importantly elevation. Nevertheless, continuous investments in snowmaking infrastructure will further suppress margins posing challenges even for financially resilient companies. It will only become evident in the next decades, which business model, Vail’s or CDA’s, will prove to be more resilient to the challenges and dangers posed by global climate change.

0 Comments