Introduction

Revolut and Stripe were born within a decade of each other, yet both companies embody radically different visions of financial disruption. While one seeks to become a fully-fledged digital bank by replacing the primary customer relationship, the other one builds infrastructure, optimizing the rails of an already dominant system. This divergence is not technological, but rather structural: in the U.S., FinTech firms emerged within a deep, market-based financial ecosystem defined by strong incumbents and developed capital markets whereas in Europe FinTech arose from a fragmented, bank-centric system that got weakened by the sovereign debt crisis and later reshaped by regulatory intervention. The aftermath of 2008 and introduction of PSD2 did not merely accelerate digital finance, but reconfigured competition itself, which raises the broader question of why the U.S. produced specialized financial infrastructure champions, while Europe produced neobanks aiming to replace the bank altogether. The answer to this question lies between institutional trust and regulatory design as well as financial architecture. By examining the structural differences between the two systems and the regulatory choices subsequent to the financial crisis, we can better understand why firms such as Revolut emerged in Europe and why their model struggles to replicate in the U.S.

Post 2008 and Regulation as a Catalyst: PSD2 and Open Banking

The divergence in FinTech models across the Atlantic cannot be fully understood without looking at the institutional rupture of the financial crisis 2008. While both the U.S. and Europe experienced severe financial distress, the aftermath unfolded asymmetrically. Aggressive recapitalization through the Troubled Asset Relief Program (TARP) initiative and swift consolidation restored relative stability and through which American banks emerged fewer in number but significantly stronger in capital buffers and profitability. By contrast, the crisis in Europe unfolded into a sovereign debt emergency that exposed the structural fragility of a framework characterized by a monetary union without a fiscal union. The consequence of this manifested itself through a prolonged period of austerity and persistently high youth unemployment in especially peripheral economies. Here a vicious cycle of failing state finances and unstable domestic banks poisoned one another, effectively choking recovery.

Trust is a central input in retail banking, which deteriorated through continued macroeconomic instability. Banking relationships, which rely heavily on the three pillars of perceived safety, brand credibility, as well as long-term stability, weakened and switching costs declined. This environment became a fertile ground for consumers willing to experiment and opened doors for digital-first entrants, who did not have to overcome entrenched loyalty, but only needed to offer transparency and convenience. This vacuum is now filled by European neobanks. Additionally, smartphone penetration accelerated and a new generation that had entered the labour market during crisis years exhibited lower attachment to traditional institutions. On one side, this revealed the technological layer that enabled digital finance, but on the other side the sociological layer which made it acceptable. However, technology alone does not explain FinTech acceleration in Europe. The decisive catalyst in this case was regulation, with the European Union adopting the revised Payment Services Directive (PSD2) in 2015, which fundamentally changed the competitive structure of retail banking.

PSD2 requires banks to provide licenced third-party providers with access to customer account data through standardized Application Programming Interfaces (APIs), which are subject to customer consent. This meant that, for the first time, incumbents no longer held exclusive control over transaction data, which is arguably the most valuable asset in retail finance. Since retail banking has always depended on informational asymmetries the significance of this shift lies not merely in transparency, but rather in the economics of intermediation. Visibility into salary inflows, spending behaviour, repayment history, and liquidity cycles allows banks to price risk and cross-sell products, while retaining customers with low churn. By mandating data portability, PSD2 weakened this informational advantage that functioned as a structural moat, which led to customer information ceasing to be a proprietary asset embedded within vertically integrated institutions. Instead, it became a transferrable input into a broader financial ecosystem. Through API connectivity in open banking, FinTech firms could now effectively manoeuvre data scarcity and access verified banking data immediately, which significantly compressed time to price credit and design products.

Digital technology amplified this institutional redesign, whereby cloud computing reduced fixed IT costs and transformed infrastructure from capital expenditure into scalable operating expenses. With API frameworks enabling interoperability between financial institutions and third parties, thus reducing integration friction, the economics of launching a product shifted from physical distribution towards software deployment. Data, however, remains subject to increasing returns: the larger the transaction volume observed, the more accurately the risk can be modelled and the more precisely services can be tailored. A growing user base moved to the centre of attention. This dynamic helps explain why European FinTech firms evolved rapidly from niche specialists into multi-product platforms that we know today, since remaining narrowly focused was strategically suboptimal. Payments expanded into foreign exchange, FX into trading and trading into crypto and lending.

Electronic Money Institution (EMI) licences allowed firms to issue electronic money and provide payment services with significantly lower capital requirements than full banking licences, reducing the minimum efficient scale required to enter the market. Simultaneously, passporting rights within the European Union enabled firms authorized in one member state to operate also across borders without the need of duplicating regulatory processes, transforming a fragmented system into a scalable regulatory bloc. In effect, Europe regulated competition into existence.

Looking at the other side of the Atlantic, the U.S. followed a materially different path. While open banking discussions initially emerged through the Consumer Financial Protection Bureau (CFPB) and the Dodd-Frank Act, no comprehensive federal mandate comparable to PSD2 was implemented. Subsequently, data sharing evolved through private contractual agreements and screen-scraping agreements facilitated by intermediaries such as Plaid, rather than through standardized regulatory compulsion, which means API developments remained market-driven instead of being imposed by the regulator. American banks, therefore, retained greater control over the timing and architecture of data access, effectively preserving much of their data-based competitive advantage.

This resulted in FinTech firms adopting complementary strategies, layering products on top of regulated bank balance sheets through Banking-as-a-Service (BaaS) models, whereby the underlying customer relationship often remained attached to the incumbent infrastructure.

The divergence in regulatory philosophy has shaped how competition emerged on both sides of the Atlantic. In Europe, mandated data portability and lighter licensing regimes lowered structural entry barriers and therefore enabled firms to compete directly for the primary banking relationship, while in the U.S., where no federal open-banking mandate was imposed, data access evolved through private agreements and intermediary platforms. The greater control over customer interfaces and balance sheets exerted by American Banks in turn encouraged FinTech firms to integrate alongside incumbents rather than displace them, resulting not in two business models, but different competitive equilibria. To understand why the U.S. and European financial systems evolved so differently, it is necessary to look beyond policies and technological differences of modern FinTech and analyse the architecture of the traditional financial markets, one market-based and capital driven, the other bank-centric and fragmented, which they were built upon.

Two Financial Systems, Two FinTech Models

The U.S. has always been a market-based economy where companies specialize in raising money through capital markets, whether through the issuance of bonds or equity offerings. As the U.S. is responsible for one-third of the total dollar value of all outstanding global bonds and credits, traditional bank loans play a less important role relative to Europe. Strategically, this helps banks to offload large proportions of risk from their balance sheet into the financial markets and focus on holding bank loans which provide them with a comparative advantage. As a result, U.S. banks have developed into well-capitalised, profitable incumbents who have already invested in digital channels and financial infrastructure, with little potential for fundamental industry disruption.

These market conditions have shaped the development of U.S. FinTech. Instead of trying to replace the existing mega banks and reshape the financial system from the ground up, the young companies decided to specialize in individual profit pools. The logic: unbundle the financial service offering, develop an expertise in a particular revenue stream, optimise it. For example, Robinhood [NASDAQ: HOOD] focused on brokerage, Chime on deposit accounts, and Stripe specialized in payments. Stripe is an evident success story, developing a new technological layer on top of the existing banking infrastructure through its APIs and today powering 90% of the Dow Jones Industrial Average and 80% of the Nasdaq 100 companies. Instead of trying to disrupt and replace the incumbents, it has positioned itself as infrastructure for them. FinTech in the U.S. are further supported by the interchange economics model the country operates on. On the surface, companies offer zero-fee banking, but when taking a closer look, the entire business model runs on the card network underneath. Every time a consumer swipes a credit or debit card, the merchant’s bank pays a small fee, typically around 2% of the transaction value, to the cardholder’s bank. As roughly 74% of all American adults own a credit card and spending exceeds $6tn each year (expected to increase as credit card acceptance increases), these fees form an enormous and predictable stream of revenue. Thus, a lot of FinTech such as Chime or Brex, provide corporate/credit/debit cards to their customers to tap into this market. But again, as seen before, the economics were already there; the innovation was in the distribution.

What further accelerated U.S. FinTech’s growth was the sheer scale available to any company that cracked the domestic market. Unlike Europe, the U.S. is a single regulatory entity with no/limited cross-border compliance layers to navigate. A payments product that works in California works in Texas, New York, and Florida without modification. As a result, U.S. FinTech can achieve enormous scale quickly and re-invest returns into R&D, products, and infrastructure. The neobank business model only becomes viable if its fixed costs can be amortized over a sufficiently large, homogenous user base. 330m Americans are exactly that.

What further accelerated U.S. FinTech’s growth was the sheer scale available to any company that cracked the domestic market. Unlike Europe, the U.S. is a single regulatory entity with no/limited cross-border compliance layers to navigate. A payments product that works in California works in Texas, New York, and Florida without modification. As a result, U.S. FinTech can achieve enormous scale quickly and re-invest returns into R&D, products, and infrastructure. The neobank business model only becomes viable if its fixed costs can be amortized over a sufficiently large, homogenous user base. 330m Americans are exactly that.

In contrast, Europe is a bank-based financial system as European companies lean on banks for funding. Why do they do this? Because they must. European equity markets represent only 81% of GDP (227% in the U.S.), bond markets are 3x smaller than their cross-Atlantic counterparts, and Venture Capital (a key fuel for FinTech formation) only receives roughly 1/5th of the U.S. funding (slightly varies by year). To counter this, the EU launched the Capital Markets Union in 2015, aiming to ease the raising of capital across borders, free up bank balance sheets and expand market-based credit, set up pan-European VC funds, and reduce regulatory hurdles. Unfortunately, adoption and integration have remained slow, and markets are still fragmented to this day.

Europe, being a patchwork of different nations, has historically struggled to operate under a single legal and regulatory market. Varying insolvency regimes, tax laws, and contract laws, coupled with the abundance of languages and cultural differences, act as a major hurdle to pan-European expansion, as the U.S. economies of scale are harder to achieve. Banks historically focused on national licensing and national balance sheets, creating a continent of financial silos with little integration. These problems become evident in the lack of profitability of European banks. A price-to-book ratio below 1 and ROE below COE (estimated at 8-10%) for much of 2015-2021 hindered investment into the digital transformation and forced banks to focus on survival, whilst managing their decline.

Thus, European FinTech found their mandate in solving a variety of the continent’s problems such as punishing FX spreads for anyone moving money across borders, inconsistent digital interfaces, underserved migrant and mobile populations that no national bank had a structural incentive to serve. But instead of following the U.S. model funded by interchange fees, European FinTech had to innovate as the EU caps these fees at 0.2% for debit and 0.3% for credit cards. The answer: layering using a freemium model which offers a current account for no fees to acquire a broad customer base, aiming to sell premium services through subscriptions (e.g. Revolut Premium, Monzo Plus, N26 Metal (30% of N26’s revenue stems from subscription products).

Thus, European FinTech found their mandate in solving a variety of the continent’s problems such as punishing FX spreads for anyone moving money across borders, inconsistent digital interfaces, underserved migrant and mobile populations that no national bank had a structural incentive to serve. But instead of following the U.S. model funded by interchange fees, European FinTech had to innovate as the EU caps these fees at 0.2% for debit and 0.3% for credit cards. The answer: layering using a freemium model which offers a current account for no fees to acquire a broad customer base, aiming to sell premium services through subscriptions (e.g. Revolut Premium, Monzo Plus, N26 Metal (30% of N26’s revenue stems from subscription products).

Overall, the ambition was categorically different from the US model: not to unbundle the bank and extract one profit pool efficiently, but to accumulate enough product breadth in a single super app (banking, FX, investing, crypto, insurance) to become a better bank altogether.

Revolut: The Cross-Border Case Study

Launched in 2015, Revolut was built to solve a key problem many frequent travelers face: expensive foreign exchange fees and difficulty dealing with your bank over international expenses. Founders Nik Storonsky and Vlad Yatsenko set out to solve this problem by establishing a virtual bank in which customers can exchange currency with little to no fees, directly on their phones. The neobank grew rapidly through the 2010s reaching approximately 11.4m customers by 2020, expanding to the U.S. and Japan in the same year. By January of 2026, Revolut reached 70m users and is projected to pass 80m users by the end of 2026.

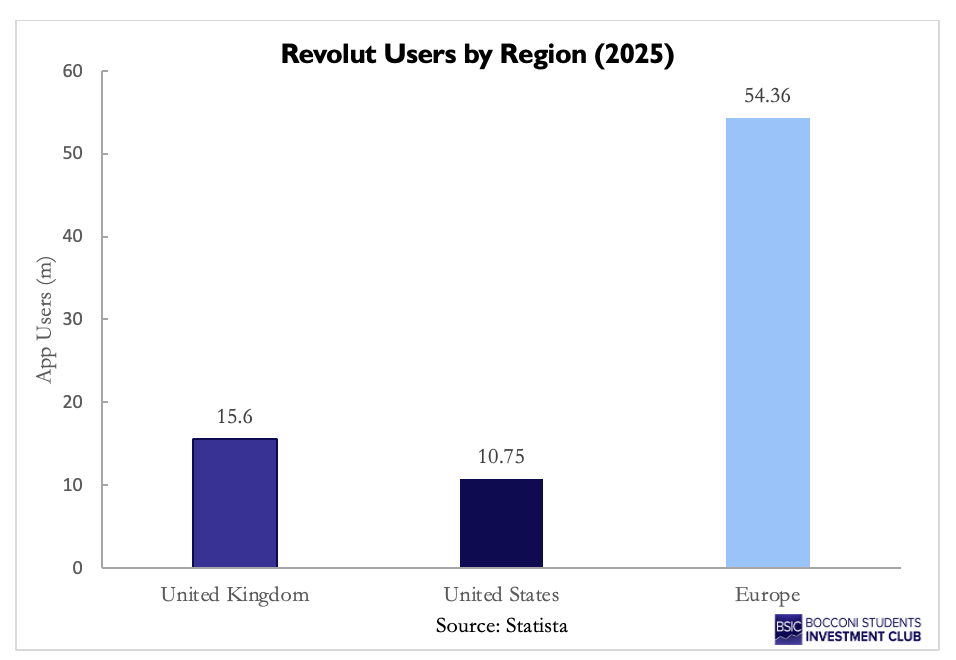

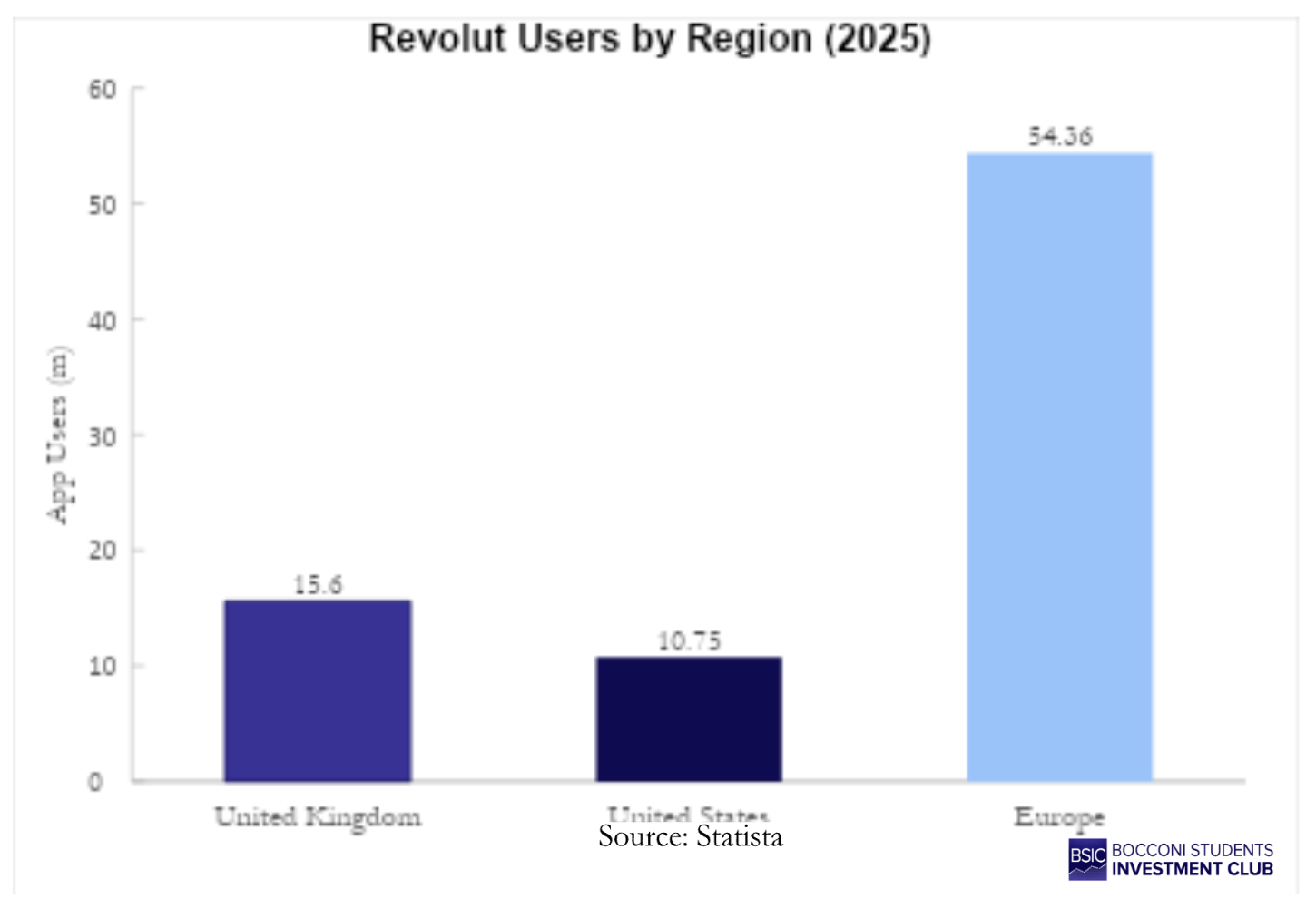

Revolut’s feature density is unrivaled in the space. From in-app currency exchange, three tiers of membership each with different benefits, peer-to-peer transfers to crypto exchanges and stock investing, the app is an all-in-one package when it comes to personal finance. With over 70m users in 2026 and revenues of approximately £3.1bn in 2024 alone, the digital bank has grown substantially since 2015 as it looks to IPO in the near future. However, this growth has been stunted by one major asterisk: the United States. While as of January 2025, nearly 11m Americans downloaded the app, compared with more than 15.5m users in the UK and over 50.2m in the top 10 European countries, Revolut’s American market lags, especially when considering the overall size of the U.S.

Revolut launched in the U.S. in 2020 with aggressive growth targets, however the London-based FinTech was met with far less enthusiasm than expected. The app only surpassed 1m downloads in 2023, demonstrating the difficulty of gaining traction in the American market. Revolut’s core strategy of offering a suite of digital banking services, aims to differentiate itself from domestic single solution apps. However, this mission has faced significant headwinds since the expansion began.

The neobank originally planned on applying for a de novo banking license, however this process was impeded by slow markets following the pandemic and regulatory complexity. Instead, Revolut pivoted, hoping to acquire a smaller community bank inside the U.S. to streamline the license application process. However, by early 2026, the company scrapped its M&A approach, instead refocusing on applying for an American banking license, hoping that the current administration will provide more efficiency towards approvals. While Revolut still offers services in the U.S., it remains unable to function as the “all-in-one” digital bank it was designed to be.

Revolut also faces the threat of looming competition on the horizon. Brazilian neobank, Nubank, a subsidiary of Nu Holdings [NYSE: NU], aims to enter the American market and capture significant share in a market it believes is still outdated and looking for a shake up. The digital bank, having over 131m customers with 113m in Brazil alone, also hopes to acquire an American banking license in the near future. Meanwhile, other players in the industry such as Starling and American FinTech Chime are also racing for the top step of the podium in the market of almost 345m Americans.

However, Revolut and other FinTechs face fundamental cultural challenges beyond the competitive landscape. Unlike in the European market which has gravitated towards “super-apps,” Americans seem to prefer a “best-in-class” ecosystem, using multiple specialized apps rather than one, complex application. Americans already use Robinhood [NASDAQ: HOOD] to invest, Venmo, or its parent company, PayPal [NASDAQ: PYPL] to send money, and Coinbase [NASDAQ: COIN] for cryptocurrencies. Additionally, traditional American banks have significantly improved their digital interfaces, allowing customers to complete basic functions online and providing easy access to 24/7 customer service assistance. These services have built a defensive moat that makes it increasingly difficult for incumbents to enter the market.

A fundamental reason for Revolut’s challenges in the U.S. is that it was designed and built to solve uniquely European challenges. With the same currency used across all fifty states, the majority of Americans do not face the currency exchange issue Revolut addresses. On the other hand, it is far more likely that Europeans and European businesses need to complete cross-border transactions on an ongoing basis. Additionally, American apps were slow to expand into Europe, such as Robinhood which only became available in the UK in 2024 and in Europe in 2025, created a massive vacuum which Revolut was primed to fill. While Revolut’s in-app services were miles ahead of the competition, U.S. banks were much quicker to follow than their European competitors, pointing to another reason the European market welcomed Revolut’s services with open arms. While Revolut’s in-app experience and all-in-one service offer many superior functions compared with its competitors, it is fighting to solve a problem that is not so existential in the U.S. market.

Despite the challenges faced by Revolut, the bank announced in early March of 2026 that they officially submitted the application to become a full-service digital bank in the United States. This decision marks a significant move as FinTechs battle for market share in the U.S. While Revolut has not yet commandeered a broad user base in the U.S., this does not speak to its overall business model and substantial success across international markets. A Revolut IPO, anticipated for 2026, would mark a significant moment for the FinTech sector. Internally, Revolut is targeting a $150bn valuation once public, implying that it will surpass the value of significant established banks such as Barclays ($79.2bn) and Deutsche Bank ($63.5bn). NuBank, which went public in 2021, is now worth $72.7bn adding to the credibility of digital banks commanding valuations surpassing those of traditional banks. With a large IPO, Revolut’s listing would serve as a catalyst for other FinTechs. Starling has been weighing whether to IPO on the LSE or in the U.S.. If Revolut leads a rush of U.S. IPOs amongst FinTechs, this will massively hurt the UK market which has branded itself as a haven for FinTech services.

Conclusion: From Asymmetry to Convergence

The transatlantic divergence in FinTech ultimately reveals something broader about financial innovation, which is that technology does not disrupt finance uniformly. It rather adapts to the incentives, profit structures and unavoidably constraints already embedded within each system. Where capital markets dominate, as seen in the U.S., digital firms tend to refine and monetize existing infrastructure, while innovation is more likely to target the primary relationships itself where banking systems are fragmented and politically contested, as seen in Europe. Yet neither model is structurally complete, since the American model faces mounting regulatory scrutiny and increasing pressure on fee-based revenues, whereas the European model must prove that customer acquisition and product bundling can translate into durable margins under full banking supervision. Therefore, in both cases, we can see the era of “growth at all costs” fading. The next chapter of FinTech may consequently be less about disruption and more about integration, with digitizing incumbents and tightening regulators, while capital is becoming more selective. Hence, the distinction between bank and FinTech is gradually blurring and the whole landscape is reshaped. If the first phase of FinTech was defined by structural asymmetry between the U.S. and Europe, the second may be defined by convergence, and in this case, not of products, but economics. The lasting question is not which region built the more ambitious digital bank, but more which ecosystem can sustain innovation while preserving profitability and regulatory stability.

{kind=link}

0 Comments