Introduction

The yacht manufacturing industry occupies a unique position within the broader manufacturing sector, characterised by an extreme form of high-value, low-volume production where a single commission can reach hundreds of millions of euros. While this may resemble other advanced industrial sectors, the key distinction lies in the nature of the end client and the purpose of the final product. Unlike industrial assets commissioned by corporations or governments, yachts are discretionary luxury goods purchased by private individuals. This industry therefore combines the economics of complex capital-intensive production with the dynamics of luxury consumption.

As yacht manufacturers move beyond the demand cycle which started during the pandemic years, the disclosure of production volumes provides an interesting opportunity to analyse the drivers and the dynamics of this niche market. Over the past five years, key players first experienced a segment-wide boom in demand, driven by low financing costs, high liquidity and an increase in wealth among high-net-worth individuals. This was followed by a period of monetary tightening and stock price contraction which normalised activity in the industry. However, not all yacht segments were affected equally, making the experience of this industry a compelling case to learn more about the dynamics and elasticities of the luxury and ultra-luxury sectors.

Against this backdrop, this article explores the fundamentals of the yacht industry from both a manufacturing and a demand perspective. It analyses the sector’s structure, production cycles, cash flow dynamics, margins, and barriers to entry, before examining how varying drivers across segments impacted both the pandemic boom and the subsequent normalisation. Finally, particular attention is also given to the way this industry developed within concentrated geographical clusters, with Italy emerging as one of the leading regions and therefore deserving of dedicated analysis.

Industry structure and the post-Covid boom

With the global luxury yacht market valued at $10.8bn in 2026 and projected to grow to over $14bn by 2031, the yacht industry is experiencing changes in buyer demographics, market growth and sustainability regulations.

Looking at the four most popular segments of the market, we have production yachts, semi-custom yachts, superyachts and megayachts or gigayachts, each with its own capital intensity and margins. Understanding this segmentation is crucial to analyse the economics of the industry. A production yacht is a standardised model which is mass produced by large manufacturers. Economies of scale can be achieved when producing this type of yacht as each design is fixed, and as such larger production numbers reduce unit costs. Their length is around 10-25 metres, with a price range of €0.5-€5m targeted to affluent consumers. A semi-custom yacht is the middle road between the standardisation of a production yacht and a fully customised one. It has a base design, but it also leaves certain aspects to be personalised by the client. Production is longer, as their typical length ranges from 25 to 40 metres. Prices range from €5m to €15m and are sold to high net worth individuals. A superyacht can be a semi-custom or fully custom design, with this usually being determined by its length. Yachts over 50 metres are built based on the owner’s requirements and can reach €40m, yet the smaller ones are simply customised and priced at around €15m. Their production time depends on the design of the yacht and its length. Megayachts are most of the time custom, since they are over 60 metres long and sold to billionaire buyers. Their price can reach €200m, making it the most expensive type of yacht. They usually take the longest time to produce, due to their size and amenities such as helipads, pools or gyms. Megayachts are produced globally by few manufacturers, meaning lower competition leads to higher gross margins, while UHNWIs whose primary demand is quality also show a reduced price sensitivity.

The boat’s length is a fundamental metric, as an increase in size doesn’t just mean more materials are needed, but it also results in higher engineering complexity. The bigger the yacht, the more advanced the propulsion systems, safety requirements, and interior architecture. Capital intensity rises with size also because longer models require complex infrastructure such as large dry docks and heavy lift cranes, in addition to the longer production time that translates into long-term skilled labour and materials purchased with years to go from the actual delivery. A production yacht, no bigger than 25 metres, takes up to a year to build. However, production of superyachts and megayachts takes over 1.5 years to build and can even reach 4 years for more personalised projects. The most significant differences between the yacht industry and mass-market boat manufacturing are therefore its limited global capacity, unique designs and its long build cycles. These long production cycles lead to a phenomenon called lagged cyclicality, meaning the industry reacts more slowly to changes in the economy. Due to these long production times, the industry is sensitive to changes in steel and aluminium prices, as well as energy costs and shortages of labour. Manufacturers must take care in estimating production costs so as not to destroy margins, and capital requirements must be chosen at the beginning of production, committing to high fixed costs over the years. With such dynamics in place, investors need to place particular attention to the order book rather than just at current-year revenue, as it functions as a good indicator of future performance. In this aspect, the yacht industry resembles much more aerospace manufacturing or large infrastructure projects rather than just consumer goods manufacturing.

Despite the global nature of the demand for yachts and charters, their production is very concentrated, with Italy being one of the leading countries, together with the Netherlands and Germany. In particular, Italy leads the superyacht segment with a 54% market share by volume and a 31% market share by order value. Key players include the Ferretti Group [BIT: YACHT], Azimut-Benetti [BIT: AZM] and Sanlorenzo [BIT: SL]. This cluster allows marine engineers and designers to be highly specialised. The Netherlands is instead most known for its ability to focus on eco-friendly materials and technologies, while maintaining high quality and tailored designs for its clients. Their focus lies mostly in 60+ metres megayachts, leveraging their engineering expertise. Turkey could be said to be a rising star, as it hasn’t always been a main player in the yacht industry but is now establishing itself in the market, favoured by its location between Europe and Asia. The reason why the industry developed and is still concentrated in Europe is mainly due to its waterfront access (94% of summer yacht charters take place in the Mediterranean Sea), which has incentivised generations to pass down specialised skills, resulting in an ecosystem of engineers, designers and naval architects.

In the years immediately following the COVID-19 pandemic, the yacht industry experienced a surprising surge. As global equity markets and cryptocurrencies, among other asset classes, boomed in 2021 HNWIs experienced a significant increase in their wealth. In addition, the low interest rates and quantitative easing implemented by central banks to counter the pandemic recession caused significant increases in liquidity. All these factors positively pushed demand for discretionary luxury assets, such as yachts for HNWIs, higher. Social factors also contributed, as a shift in consumer preferences caused by the pandemic made individuals long for secluded, socially distanced environments to spend their free time. However, given the dynamics presented above, the sudden increase in demand didn’t immediately lead to expanded supply. Rather, order books extended several years in the future, with individuals rushing to secure orders, leading to record-high orders and backlogs.

The economics of yacht manufacturing

As mentioned above, the yacht industry is characterised by long production cycles which can last as long as 4 years. But how many stages are involved in building such a complex product? First, the contract between the client and producer takes place. For the high-end segments this consists of the client requesting the yacht to be built, while for more standardised products manufacturers may already start building the yacht aiming to secure a buyer before construction is complete. The design of the yacht is decided in this phase, as well as interior layout, size and performance characteristics for more custom requests. The formal start of construction is instead marked by the keel laying process, where the foundation of the yacht’s hull is decided – whether it’s made from steel, aluminium or wood. The hull and superstructure are then built, creating the shell of the yacht. Then comes a stage called outfitting, which includes equipping the yacht with electrical and engineering works, on top of interior furnishings. After these stages, the yacht will be transferred from land to water, where it will undertake a sea trial to evaluate its performance and proceed with any eventual adjustment. Finally, the yacht is delivered to its buyer along with documentation and certification. Each of these steps can take up to several months, causing even the smaller boats to take at least one year to be completed. Due to such extended build cycles, many projects will overlap, so companies in the industry need to invest in efficient planning and systematic management.

The cash flow management part of this industry also differs from regular consumer manufacturing, again due to its long build cycles and a commonly chosen milestone-based payment structure. Rather than a single payment at delivery, there are multiple cash infusions throughout the production process. If manufacturers were to fund the entire project upfront, they would absorb an unsustainable amount of their working capital. Costs for prolonged skilled labour, aluminium, steel and electronics can easily reach the millions. Milestone payments improve cash flow and reduce financing needs. Additionally, this method reduces the risk that the buyer might back out of the project while in construction, which could lead to huge losses. Payments are usually based on the completion of production stages. Buyers put down a deposit at the signing of the contract, usually 10% or 20%, and then after the keel laying, the hull completion, the first trial and the final delivery.

Compared to the mass industrial shipbuilding sector, the yacht industry is generally able to earn higher profit margins. The products are mostly sold to HNWIs or UHNWIs, who are willing to pay high prices for bespoke manufacturing. Ferretti, for example, has an EBITDA margin exceeding 16% in 2025 and Sanlorenzo, another Italian yacht manufacturer, had an EBITDA margin of 19% in 2024, showing companies in the industry have high profitability and strong pricing power. For reference, commercial shipbuilding gross margins have been around 45% and EBITDA margins around 11%. These differences in margins across the shipbuilding industries are mainly due to the higher premiums that yacht buyers are willing to spend in order to customise their products and enjoy bespoke designs, allowing builders to charge significant mark-ups over base prices.

The degree of buyer bargaining power in the market depends on the specific segment, as for the less expensive models buyers are more price sensitive and so manufacturers may not be able to charge a high premium. Supplier power is generally quite high, due to the dependence on specialised materials, architects, and engineers.

Overall, the high margins and profitability make the yacht industry quite attractive, however breaking into the market can prove difficult for new entrants, as it requires substantial amounts of upfront capital. Additionally, if macro conditions are not favourable, and borrowing is expensive, many firms might not be able to afford the basic materials to start production. The long production cycles, which carry higher risk and require coordination of production, reinforce the advantage of incumbent firms. In addition to the capital, construction needs to be in proximity to a water access, equipped with specialised docks. Lastly, the demand for reliability and craftsmanship, makes the reputation of the brand a crucial selling point; long established successful brands may attract more buyers, due to their name already being in the market.

Not all luxury is the same

Luxury goods are often defined as goods with an income elasticity of more than one. Put differently, as consumer income rises, the demand for these goods increases more than proportionately. However, not all luxury is the same. There are two main types of luxury. First there is the broader luxury market, also called aspirational luxury, and then there is ultra-luxury.

Aspirational luxury encompasses premium watches, designer fashion and entry-level luxury cars. This segment is characterised by a relatively broad buyer pool that is highly sensitive to changes in disposable income and the availability of consumer credit. During periods of economic expansion, this segment sees explosive growth, however, it is also the first to contract during recessions as consumers trade-down to non-luxury alternatives or defer their luxury purchases. The aspirational base may also rely on credit to fund its purchases. For this group, rising interest rates directly diminish purchasing power by increasing the cost of financing. This makes the segment highly elastic in the short run. Furthermore, these consumers are susceptible to the income effect, where a decrease in real wages or a softening of labour markets leads to an immediate reduction in luxury expenditure.

Ultra-luxury, on the other hand, operates under a fundamentally different set of demand drivers. In this group, the wealth effect is far stronger than the income effect. Consumption here is a function of total net worth and the performance of asset markets rather than annual earnings or salaries. The buyer pool for ultra-luxury is highly concentrated among UHNWIs. For this group, the demand for positional goods like yachts is often influenced by the Veblen effect, where the high price itself is a signal of status and exclusivity, potentially leading to lower short-run price elasticity. Moreover, because purchases are driven more by wealth than by income, the price elasticity for this luxury segment is significantly lower than the price elasticity for the aspirational luxury market.

The differences between aspirational luxury and ultra-luxury are clearly visible in the yacht industry. The mid-market segment, generally defined as yachts below 24–30 metres, represents the entry-level of luxury boating. These vessels are frequently production yachts built to a model, where manufacturing is more volume-driven and standardised. This segment exhibits the highest effective elasticity in the industry. Buyers in this tier are more likely to utilise retail financing, making demand highly sensitive to interest rate hikes and broader credit conditions. Recent data shows that demand for these types of yachts has been decreasing in 2025. The recently published preliminary full-year numbers from Sanlorenzo show that its Bluegame division, which focuses on the sub-24-metre market, reported a 7.4% decline in full-year revenues. Similarly, major manufacturers like Sunseeker and Princess have announced staff reductions in response to weaker demand for smaller glass-reinforced plastic yachts. The contraction is driven by a combination of elevated interest rates in the U.S. and Europe and a normalisation of the post-pandemic buying frenzy. The superyacht segment, particularly the 30–60-metre range, is the traditional stronghold of the Italian yachting industry. These vessels are primarily semi-custom, where a proven naval platform is tailored to the owner’s aesthetic preferences. The demand in this tier is driven by the UHNW client base, which is significantly more resilient than the mid-market aspirational base. This part of the market however still suffered contractions in 2025. The Monaco Yacht Show Market Report 2025 shows that newly bought yachts suffered from a lack of demand, whilst used yacht sales held up well in the first half of 2025. Sanlorenzo’s Yacht division, catering to this segment, reported a revenue decline of 5.4% in 2025. At the pinnacle of the market are megayachts and gigayachts, often exceeding 80–100 metres. This segment represents the extreme concentration of global wealth, where the buyer pool consists of the world’s billionaires. This is by far the least elastic segment of the market, where even a sharp decline in wealth and losing billions on paper is unlikely to deter a yacht purchase of a few hundred million dollars. The Monaco report shows no notable decreases in new yacht sales and slight increases in the used yacht sales. Sanlorenzo’s Superyacht division held steady with a modest 0.5% revenue growth year-over-year, clearly not suffering similar sales contractions as other divisions. Even though megayachts can cost hundreds of millions of dollars, it is unlikely that such a purchase would hurt the financial standing of a multibillionaire. This is a sharp contrast with the mid-market segment of yachts, where purchases are financed through credit. Sharp interest rate hikes as occurred in 2022, make a yacht notably more expensive and financially risky. Hence, the mid-market segment of yachts showcases characteristics that are reminiscent of aspirational luxury products, whereas the megayacht segment is a strong example of ultra-luxury.

Italian excellence in yacht manufacturing

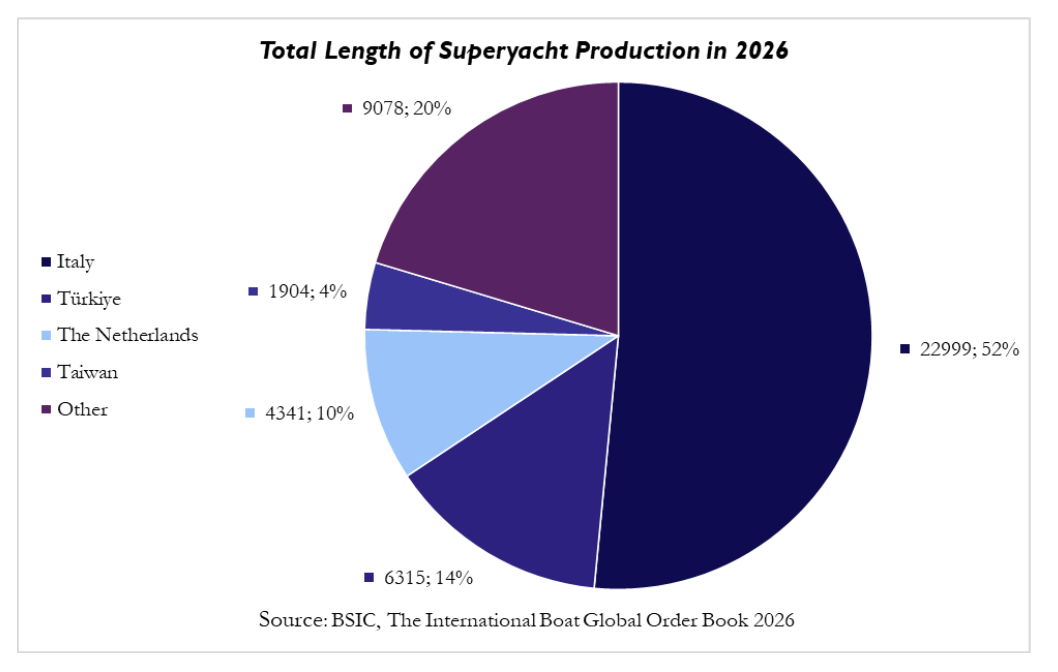

These varying tiers of elasticity create a complex map for manufacturers, particularly in Italy. While the most inelastic gigayacht segment remains dominated by Northern European yards with naval-heavy backgrounds, the Italian industry has established itself as the global hub for the 30–60-metre superyacht. The International Boat Global Order Book 2026 shows that Italy accounts for approximately half of the world’s superyacht production by units, a figure that dwarfs competitors like the Netherlands, Turkey, and Taiwan.

The strength of the Italian industry lies in its dense cluster of shipyards and specialised suppliers, concentrated primarily along the Ligurian and Tuscan coastlines. This regional concentration including Viareggio, La Spezia, and Livorno creates a self-sustaining ecosystem of naval architects, engineers, and artisanal craftsmen. This ecosystem allows for a level of customisation that is difficult to replicate in other regions. Italian shipyards have successfully integrated these suppliers into their production cycles, often bringing strategically high-value activities like steelworking or upholstery in-house to ensure quality and timeline control.

The Italian market is dominated by four major groups, each with a distinct strategic orientation that aligns with the demand dynamics of the ultra-luxury segment. As the world’s leading builder of yachts over 24 metres, the Azimut|Benetti Group manages a dual-brand strategy. Azimut focuses on the 15–35-metre segment with a high degree of innovation and technological integration, while Benetti serves the megayacht market with full-custom steel hulls. Ferretti Group operates a portfolio of iconic brands, including Riva, Pershing, and Custom Line. Their strategy centres on maintaining leadership in composite and made-to-measure segments while pivoting toward larger, more profitable yachts. Sanlorenzo is the brand for true connoisseurs and positions itself as a boutique builder focused on the 30–50-metre segment, which it identifies as the most profitable and resilient part of the market. Sanlorenzo is known to even fully customise smaller yachts in contrast to most of its competitors. Finally, the Italian Sea Group [BIT: TISG] is a pure-play megayacht specialist, focusing on vessels exceeding 50 metres under brands like Admiral and Perini Navi.

Italy is the central hub for yachts between 30 metres and 60 metres in length. Even though it would be highly compelling to cater to the hyper-inelastic ultra-luxurious yachts, gigayachts are currently mainly produced in Northern Europe including countries such as the Netherlands and Germany. Producing a gigayacht is a different ballgame than producing smaller yachts. Yards like Lürssen in Germany and Damen in the Netherlands evolved from building massive naval frigates and heavy commercial vessels. They have the heavy-duty DNA, dry docks, and massive sheds required to build what are essentially private warships in terms of complexity. Having said that, Italian yacht builders are increasingly active in M&A to strengthen their vertical supply chains, with Sanlorenzo acquiring Nautor Swan and TISG acquiring Celi 1920. The acquisition of Nautor Swan by Sanlorenzo is primarily horizontal integration, as it allows Sanlorenzo to expand its product portfolio into the luxury sailing segment where it previously did not compete. However, the acquisition also offers opportunities for Sanlorenzo to integrate a vertical ecosystem of services, including Swan Charter, Brokerage, and the ClubSwan Racing division. Celi 1920 is not a yacht builder but a specialised supplier of high-end custom furniture and bespoke interiors. These acquisitions give the Italian yacht builders more control over lead times, capture the high-margin secondary services like refit, upholstery, and maintenance and allow the Italian yacht builders to offer truly unique, one-of-a-kind products that appeal to the most important clients.

Conclusion

The yacht industry’s recent cycle of boom and normalisation demonstrated how its many product segments are differently correlated with general demand trends, thus making for significantly different risk profiles that must be considered when valuing a yacht manufacturing company. Production yachts and entry-level vessels, often financed and more income-sensitive, have reacted clearly to higher interest rates and weaker consumer confidence, as shown by reported revenue declines in the mid-market divisions of listed companies. By contrast, the 30–60-metre superyacht segment has shown greater resilience, with more stable demand from UHNW individuals and a strong backlog. At the very top, megayachts and gigayachts proved to be the least elastic tier. These observations may seem to challenge the view of luxury goods as highly sensitive to consumer confidence and economic growth. However, given the peculiar nature of the yacht manufacturing industry, they more so demonstrate how this commonly assumed framework tends to break down in extreme scenarios such as when dealing with concentrated demand from a small number of UHNW individuals for €100m+ discretionary goods.

At the same time, the industry’s revenue stability is also supported by its manufacturing fundamentals. Multi-year build cycles, milestone-based payments and large backlogs mean any effects on demand take a longer time to show in the manufacturers’ financials. Firms must, however, remain aware of and plan accordingly for their exposure to input cost volatility and working capital needs.

0 Comments