Introduction

The success of GLP-1 drugs, most notably Ozempic and Mounjaro, has made peptides one of the most commercially attractive therapeutic areas in the world and, therefore, a key pillar in Big Pharma’s strategy moving forward.

Peptides, short chains of amino acids between traditional small-molecule drugs and larger biologics, have been gaining popularity in the pharmaceutical space. This is largely due to their unique structure which enables them to mimic naturally occurring hormones and signalling molecules in the body, leading to targeted and greatly beneficial therapeutic effects. Historically, peptides have been plagued by a number of issues including short half-lives and poor oral bioavailability which explains their historically limited use. However, over time, breakthroughs in formulation, delivery technologies, and molecular engineering have significantly improved their potential. In the present day, they are being developed to tackle a wide array of diseases such as metabolic issues, oncology, endocrinology, and gastrointestinal disorders.

However, while peptides have gained credibility in the pharmaceutical sector, they have also appeared through consumer grey market channels, where they are being actively promoted on social media platforms and sold through telehealth providers, wellness clinics, and unregulated online marketplaces.

The peptide boom is therefore not a single market but rather both a clinically validated pharmaceutical revolution and a rapidly expanding consumer ecosystem operating in tandem, with the success of the former fuelling the growth of the latter.

Peptides Enter Big Pharma’s Core

Peptides, which were once regarded as a niche, technically constrained class of therapeutics, have undergone a structural transformation within the pharmaceutical industry. Peptides have gone from being a peripheral asset to a central pillar of Big Pharma’s strategic and capital allocation priorities due to clinical validation, technological innovation, and industrial scalability. From a historical perspective, peptides were limited by pharmacokinetic hurdles, including poor oral bioavailability, which confined their use mostly to injectable therapies. However, advances in peptide engineering, formulation technologies, and delivery mechanisms, especially within the areas of stabilized analogues and oral peptide platforms, have significantly expanded therapeutic potential, enabling applications across fundamental disease areas like metabolic disorders and oncology. The commercial breakthrough of glucagon-like peptide-1 (GLP-1) receptor agonists, led by Novo Nordisk [NYSE: NVO] and Eli Lilly [NYSE: LLY], has been highly influential in driving this transformation. The drugs have not only demonstrated strong clinical results for diabetes and obesity, but also the ability to generate sustainable revenue streams through long-term therapy, repositioning peptides as scalable assets within an ecosystem, rather than single-product innovation.

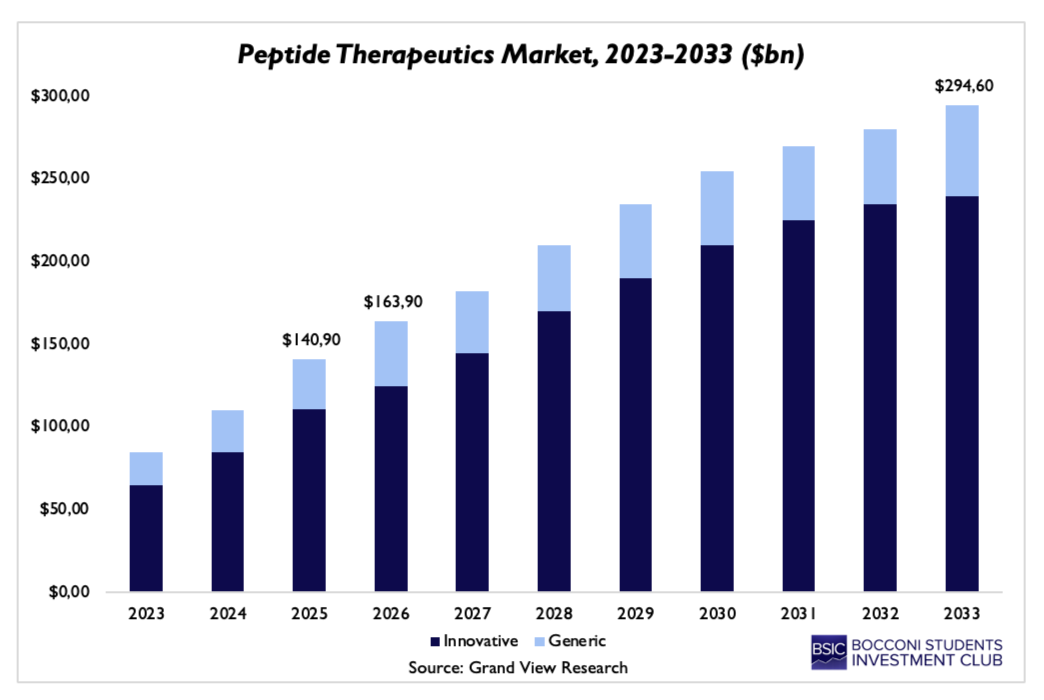

The economic results of this shift are reflected in the rapid expansion of the global peptide therapeutics market, which is expected to grow from around $100bn in the mid-2020s to almost $300bn by 2033. This trajectory highlights how peptides have moved into the core of pharmaceutical value creation.

It is important to mention that this growth is not uniform but rather disproportionately driven by innovative peptide therapeutics, which demand higher margins and benefit from stronger intellectual property protection. By taking a unique position between small molecules and biologics, peptides combine the specificity and safety profile of the latter with the manufacturability and scalability of the former, making them particularly valuable for an industry highly focused on precision medicine. The ability to selectively target certain receptors while minimizing unwanted effects at the same time can significantly improve clinical results and regulatory success rates.

It is important to mention that this growth is not uniform but rather disproportionately driven by innovative peptide therapeutics, which demand higher margins and benefit from stronger intellectual property protection. By taking a unique position between small molecules and biologics, peptides combine the specificity and safety profile of the latter with the manufacturability and scalability of the former, making them particularly valuable for an industry highly focused on precision medicine. The ability to selectively target certain receptors while minimizing unwanted effects at the same time can significantly improve clinical results and regulatory success rates.

From a strategic position, the appeal of peptides to Big Pharma can be understood through three interrelated dimensions, ranging from therapeutic breadth to economic stability and structural defensibility. First, peptides have a very broad use base, where applications span some of the largest and fastest-expanding therapeutic areas. The global burden of obesity and diabetes continues to grow, thus creating a billion-dollar opportunity that peptides are well-positioned to address. Beyond metabolic solutions, peptides are also very useful in oncology due to their ability to act as targeting ligands to deliver cytotoxic agents directly to tumor cells. Additionally, for endocrinology and rare diseases, peptides can provide the groundwork for the adjustment of complex patterns with a high level of precision. This increase in the addressable market for peptide-based therapies makes peptides an optimal long-term investment for pharmaceutical companies that seek sustainable growth.

Additionally, a large number of peptide therapies are conducted chronically, creating predictable and scalable recurring revenue streams. Peptides, therefore, exhibit favourable economic characteristics that are in line with the evolving business model of the pharmaceutical industry. For example, the success of GLP-1 drugs, where patients often get persistent treatment for extended periods, increases the lifetime value per patient. Furthermore, as synthesis technologies improve, production costs can be reduced, enhancing margins over time. The complex manufacturing process, particularly for longer or modified peptides, also creates significant entry barriers, limiting competition and enhancing pricing power. In an industry with patents on key drugs expiring, big pharmaceutical companies are desperate to find products offering high demand, recurring revenue, and defensible margins.

The rise of peptides has transformed manufacturing from a supporting factor into a strategic capability, prompting substantial capital investment across the industry. Pharmaceutical companies, as well as contract development and manufacturing organizations (CMDOs), are therefore investing heavily in peptide production capacity expansion, which in turn again reflects a broader shift toward the industrialization of peptide therapeutics. As an example, private equity-backed CordenPharma has committed over €900m to expanding its peptide manufacturing capabilities across Europe and the U.S., with a target of around €3bn in future contracts. In a similar case, Novo Nordisk has announced a $6bn investment in Denmark for its active pharmaceutical ingredient (API) production capacity, which includes peptides, to meet the jump in global demand. These investments are not isolated but rather part of a broader trend. Manufacturing infrastructure is increasingly becoming a critical determinant of competitive advantage.

Peptide industrialization is further reinforced by a growing emphasis on supply chain resilience and geopolitical risk mitigation. Global production of APIs has been historically concentrated in China, which creates clearly visible vulnerabilities, apparent in the context of geopolitical tensions and disruptions connected to the pandemic. Western pharmaceutical companies are actively attempting to diversify their supply chains by investing in domestic manufacturing capacity. While this shift enhances supply chain security, more importantly, it aligns with broader regulatory and political goals to improve domestic pharmaceutical production capabilities.

At the same time, technological innovation is increasing the realm of possibilities with peptide therapeutics. Oral peptide delivery systems have the potential to dramatically increase patient loyalty and further increase the total addressable market for peptide-based drugs. This is a stark contrast to conventional therapies that are limited by the requirement for injection, which reduces patient compliance and restricts use. Recent partnerships, such as Merck’s [NYSE: MRK] $493m licensing agreement with Cyprumed, aim to overcome these limitations by enabling oral intake for peptides. Successful partnerships like this can lead to a further acceleration in the adoption of peptides across broad platforms, increasing their relevance in the pharmaceutical landscape.

The Parallel Boom: Consumer, Wellness, and Grey Market Peptides

Alongside the institutionalization of peptides within pharmaceutical channels, a parallel, far less regulated market has emerged. Driven by consumer demand for performance and aesthetic optimization, individuals are increasingly seeking interventions to enhance their physical or cognitive performance. Spurred by a cultural shift toward biological modification, including anti-aging and preventative health, peptides sit between supplements and pharmaceuticals.

As is often the case, social media has played a powerful role as a demand engine. YouTube and TikTok have reduced the gap between early-stage research and consumers, with influencers self-experimenting with peptides and subsequently sharing their “protocols” and outcomes. Through this feedback loop, demand has increased substantially, fuelling further content and normalization. Unlike highly regulated conventional pharmaceuticals, this ecosystem operates with minimal to no oversight, allowing claims around efficacy and safety to quickly spread without scientific validation.

The absence of clinical examination is a key characteristic of the subsector. While many peptides stem from legitimate research contexts, most have not undergone the required regulatory process for approval for medical use. However, adoption persists, driven by perceived benefits and accessibility, highlighting a fundamental divergence: pharmaceutical markets are constrained by regulation, while consumer markets are driven by perception and availability. Distribution channels further reflect this fragmented structure, with telehealth platforms and wellness clinics providing unmonitored access to peptides. Online vendors market peptides as research chemicals, thereby formally disclaiming human use while effectively targeting consumers.

The clinical success of peptide-based drugs has legitimized this broader-based category with two effects: reduced perceived risk and increased consumer interest. Simultaneously, high prices and limited access to approved treatments create demand spillovers, which in turn push consumer demand toward alternative sources. Big Pharma’s growth into peptides is actively fuelling the expansion of a consumer-driven, grey-market segment operating alongside it.

The Feedback Loop: How Pharma Success Is Fuelling the Grey Market

The GLP-1 boom gave the grey market a gift it could not have earned on its own. When semaglutide and tirzepatide became among the most prescribed drugs in the world, they handed the broader peptide category a degree of public credibility that would have taken years to build through conventional scientific communication. Grey-market vendors understood the commercial value of that faster than most regulators did.

Shortages made that connection concrete. Between 2022 and early 2025, Novo Nordisk [CPH: NOVO-B] and Eli Lilly [NYSE: LLY] simply could not manufacture fast enough to meet demand. Compounding pharmacies took the gap and turned it into a market worth roughly $1bn a year by 2024. When tirzepatide came off the FDA shortage list in October 2024 and semaglutide followed in February 2025, compounders were told to stop. The demand did not follow. Grey-market imports from China reached $328m in the first nine months of 2025 alone, nearly double the $164m recorded over the same period of 2024.

Consumers accustomed to lower-cost compounded alternatives did not switch to branded products at full list price. They sourced what they needed from online vendors that shipped vials labelled “not for human use”, many of them drawing from the same Chinese API suppliers that had been serving regulated compounders months before. That migration was frictionless, in part because the underlying supply chain was largely the same.

China produces an estimated 45 to 50 percent of global peptide API output, with Jiangsu province home to a dedicated industrial park of 27 specialised manufacturers. Several of these facilities run parallel commercial arrangements, one side feeding pharmaceutical customers and another serving compounders, grey-market distributors, and direct-to-consumer platforms. The grey market, in other words, is not a shadow network operating independently of legitimate pharmaceutical production. Much of it runs off the same equipment as a legitimate API, just without the GMP controls and validated testing that define a regulated product on the other end. Lab analysis of grey-market vials has turned up contamination and dosage errors that a certified facility would have flagged before anything was shipped.

Peptide content on TikTok has cleared 50 million views. A pre-print on BPC-157 tissue repair can reach consumers through an influencer’s affiliate links within days of publication, before any regulatory body has looked at the data. This is the information arbitrage the grey market runs on.

Figures like Joe Rogan, Andrew Huberman, and Peter Attia have made self-experimentation with compounds such as Thymosin Alpha-1, CJC-1295, and Ipamorelin sound like a reasonable health decision for a certain kind of affluent, health-focused consumer who takes their own longevity and health seriously. Chinese vendors have built e-commerce presences calibrated to this audience precisely, shipping vials for as little as $5 with product pages indexed to the exact search terms the longevity community uses. Every pharmaceutical advance in peptide science creates a corresponding spike in grey-market demand. The supply chain has consistently responded faster than any regulator.

Regulation Struggling to Keep Up

The regulatory problem with peptides is not one of enforcement capacity. It is one of classification. A compound like BPC-157 turns up as a prescription drug in one context, a compounded preparation in another, a research chemical with a not-for-human-use label on a third website, and something marketed as a wellness supplement on a fourth. Each version is governed by different rules, pursued through different legal mechanisms, and requires a different standard of proof for the FDA to act.

What followed the FDA’s 2023 Category 2 decision is worth tracing. The FDA moved 19 widely used peptides to its restricted list that year, cutting compounding pharmacies off from legal production. Many clinicians and compounding trade groups contested the decision, with the common view being that no specific adverse event signal justified restrictions on most of the listed compounds. BPC-157, GHK-Cu, CJC-1295, Ipamorelin, AOD-9604, and others were no longer available through licensed compounders. People sourced them elsewhere, leading to direct imports from China roughly doubling between 2024 and 2025.

The agency did respond. More than 55 warning letters went to online sellers of compounded GLP-1 products in September 2025, 22 percent of them targeting GLP-1 formulations specifically. Import volumes grew regardless. Removing the regulated supply channel while leaving the unregulated one open did not reduce consumption. It relocated it.

The policy reversal arrived in an unusual form. On the Joe Rogan Experience in February 2026, HHS Secretary Robert F. Kennedy Jr. announced that roughly 14 of the 19 Category 2 peptides would return to Category 1, restoring legal access through licensed compounding pharmacies under physician prescription. Kennedy said directly that the Category 2 restrictions had created the grey market. Kennedy did not soften the framing. On a podcast, he said that the FDA’s own restrictions had pushed consumers into the market the FDA was trying to control. Among the compounds expected back are BPC-157, GHK-Cu, Thymosin Alpha-1, CJC-1295, Ipamorelin, and AOD-9604.

No formal updated Category list had been published by early April 2026. The fact that the announcement came through a podcast rather than the Federal Register tells you something about how the administration communicates major policy positions. Compounding pharmacies and prescribing physicians have been operating in legal uncertainty for over six weeks.

The wider picture is not coherent. In February 2026, the FDA restricted GLP-1 APIs in non-approved compounded products, tightening enforcement in one area while, at the same time, Kennedy’s announcement committed to loosening access across 14 others. State-level enforcement has added a third layer, with several jurisdictions pursuing independent actions against wellness clinics and medical spas administering grey-market compounds without adequate physician oversight, none of it coordinated with federal action. The core problem is speed: by the time the FDA evaluates a peptide compound, classifies it, and publishes guidance, social media has already built a consumer market around it worth tens of millions of dollars. This gap between the pace of pharmaceutical innovation and the pace of regulatory response is not a temporary administrative lag. It is the structural condition in which the peptide industry currently operates.

The Future of the Peptide Industry

The future of the peptide industry is going to be determined by how the interaction between the two conflicting markets presented above evolves over time.

In the short term, both the pharmaceutical and the consumer grey markets are likely to continue their rapid growth due to strong demand, continued investment into the space, and broader applications for peptides.

Taking a more long-term outlook, there are two possible scenarios that could unfold.

Under the first scenario, it is likely that elements of the grey market will be integrated into the pharmaceutical ecosystem via increased clinical validation and regulatory approval. Big pharmaceutical companies could expand their operations downstream as well by including elements of direct-to-consumer distribution while, at the same time, maintaining strict and extensive oversight to ensure that the quality and safety of their products doesn’t decline.

Another possible scenario is continued bifurcation, in which the divide between the highly regulated pharmaceutical market and the consumer grey market ecosystem persists. Both of these markets would continue to grow separately and attract different consumers.

Some potential risks that could affect both scenarios include regulatory crackdowns, safety concerns arising as the grey market continues expanding, supply chain constraints, and a possible situation where desire for peptides could outpace their actual clinical potential in certain applications.

Conclusion

The peptide boom represents not just the emergence of a new group of therapeutics but also a broader shift in the way in which pharmaceutical innovation interacts with consumer health culture.

Over the next five years, the industry is likely to continue to grow as pharmaceutical giants, through technological innovation and capacity expansion, fight to gain market share in an industry projected to grow at 10% compound annual growth rate. Looking further into the future, the key question revolves around how the relationship between the two parallel markets will develop.

Peptides are no longer exclusively part of the pharmaceutical industry. They are becoming a bridge between highly regulated pharmaceutical innovation and an increasingly influential consumer health ecosystem, with consequences that neither companies nor regulators fully control.

0 Comments