Introduction

Venezuela sits on top of the world’s largest proven oil reserves, encompassing over 300bn barrels. Nevertheless, its citizens suffer under one of the most severe economic collapses of the 21st century, where GDP has contracted around 65%, hyperinflation has reached millions of percent, and over 8m citizens have emigrated. That such an extreme implosion could occur in a country of such extraordinary resource endowment is not a paradox, but a case study that illuminates how institutions, governance, and political economy interact to determine whether natural wealth becomes a foundation for development or a mechanism for its destruction. How has Venezuela ended up in this dilemma and what structural or economic developments are necessary to rebuild the country?

Oil Boom to Institutional Collapse: The Evolution of Venezuela’s Petrostate

From Agriculture to Oil: The Structural Transformation

For most of the 19th and 20th century, Venezuela’s economy was focused on coffee and cacao exports, being run by a modest merchant class with ties to European commodity markets. Various civil wars (Federal War (1859-1863), Legalist Revolution (1892), Liberating Revolution (1901-1903) – just to name a few) contributed to the government’s weakness, its chronic indebtedness, and its instability.

The discovery of oil and the beginning of commercial drilling changed all of this, triggering Venezuela’s entry into the global age. The drilling began in the 1910s around Lake Maracaibo under the rule of dictator Juan Vicente Gómez, a man with little interest in industrialization, taxation, or state-building. Instead of reinvesting the proceeds of oil exports into the economy, he handed concessions to foreign companies, including Royal Dutch Shell [NYSE: SHEL] and the predecessor of ExxonMobil [NYSE: XOM], with the payments flowing directly to the central government, bypassing the domestic economy. By 1929, oil composed over 75% of Venezuela’s export revenue, making the country the world’s largest oil exporter. As a result of the large currency inflows, the exchange rate appreciated sharply making domestic non-oil sectors, such as agriculture and manufacturing, less competitive on the global market.

The political economy consequence of this transformation was profound and long-lasting. As the state learned that it did not depend on revenues from productive activity by its population (income/trade/property taxation), it could afford to bypass them and govern without accountability. As a result, the country’s political and social institutions were not built alongside the oil economy, but bypassed it, only benefiting a small proportion of the population. Even today, this lesson has not fully been learned by the government.

Oil Nationalism and the Birth of PDVSA

Venezuela was a founding member of OPEC in 1960, an institution originally created to give producer governments better information and higher bargaining power against the oil majors. As a result, Venezuela’s royalty terms improved significantly throughout the following decade. The decisive disruption to the country’s oil industry came through the oil crisis of 1973. As a producer, the government benefited from quadrupled prices overnight, motivating a political push towards nationalization to benefit from the higher revenues. In 1973, the country elected Carlos Andrés Pérez who passed the Hydrocarbons Reversion Law and, in January 1976, formally nationalized the oil industry in the form of Petróleos de Venezuela, S.A. (PDVSA).

Originally, this model, and the company itself, were functioning well. PDVSA was insulated from political interference, as the management was composed of foreign staff, engineers were professionally trained abroad, operating revenues were reinvested (20-25% in the 1980s), and it maintained joint ventures with foreign majors. The company even operated refineries in the Caribbean and on the U.S. Gulf Coast and tried to develop new techniques to upgrade projects for the exploration of the extra-heavy crude oil of the Orinoco Belt.

PDVSA’s operational performance was not the problem, but rather what its success did to the rest of the economy. This phenomenon is labelled as the Dutch Disease in economic theory. In summary, as a country experiences large foreign currency inflows from a commodity export, its real exchange rate appreciates. As a result, other exports become more expensive and imports are cheaper, hurting the tradable sector. Secondly, the labor and capital markets migrate towards the booming sector, and the non-tradable goods orient themselves around it, resulting in a structural narrowing of the economy, as industries such as agriculture get crowded out. In Venezuela’s case, by the 1980s, non-oil exports fell to less than 5% of total export revenues, manufacturing contracted, and agriculture declined as a share of GDP and employment. The existing private sector was largely dependent on subsidized fuel, cheap imported goods, and government contracts, but lacked significant entrepreneurial activity.

The government’s wealth, because of the oil crisis, funded a large increase in public spending over the following decade, but when prices fell sharply in the 1980s the government was in difficulty. Borrowing, devaluation, capital controls, and ultimately help from the IMF, peaked in an austerity package from President Pérez (returned to power in 1989). Instead of the prosperity he promised, he raised fuel prices and public transport fees, resulting in three days of rioting, looting, and government repression that left hundreds dead. These riots, called the “Caracazo”, are the pivotal transition in Venezuela’s modern history, as they delegitimized the political class, and laid the foundations for the rise of Hugo Chávez.

Chávez was elected in December 1998 (having twice attempted to seize power by force before), indicating the political verdict of the Caracazo, as the people elected a radical military officer who promised to redistribute oil wealth to those who had been excluded from it. Initially, his policies were not immediately radical, but the turning point arose in 2002/2003, when a large part of PDVSA’s engineers and managers went on strike to force him out of power. This failed and as a consequence, 18,000 employees were dismissed (a large part of its experienced workforce), hollowing out its technical capabilities, and replacing them with loyalists. Production had already begun to fall, from a peak of approximately 3.5m barrels per day in 1998 to around 2.8m by 2002, partly due to underinvestment in the late 1990s. After the 2003 purge, the ability to reverse this decline was permanently compromised.

From 2003 onward, PDVSA was systematically redirected from an operational oil company into an instrument of social policy, with billions in revenues channeled directly into programmes covering literacy, healthcare, food subsidies, and housing. This bypassed the formal budget, removing fiscal accountability, and starving the company of the capital reinvestment that a long-cycle extraction business requires. Simultaneously, Chávez forced renegotiation of joint ventures, which nationalized the operations of major foreign oil companies, and reshaped the legal framework to maximize state control and short-term revenue extraction, driving out the proprietary upgrading technology needed to develop the Orinoco Belt.

Still, timing was on Chávez’s side as total oil revenues continued to increase throughout the 2000s, even as production fell by over 1m barrels a day until 2008 (prices rose from roughly $25 per barrel in 2002 to a peak above $140 per barrel in mid-2008). This appearance of success collapsed briefly in 2008 as prices fell below $40 in six months, forcing the government to draw on reserves and cut spending. Instead of changing the model though, Chávez “learned” that oil prices will always recover and the model remained viable in his administration’s eyes.

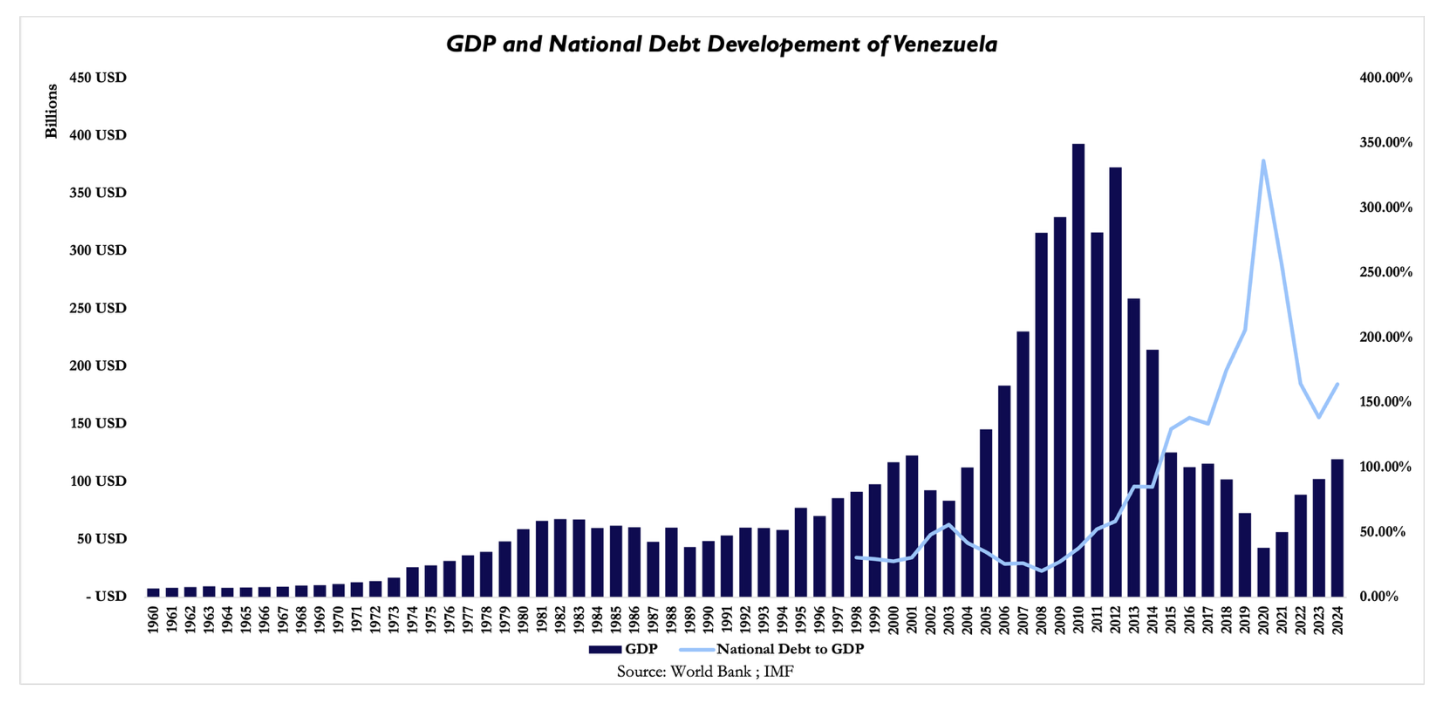

The collapse of Venezuela from 2013 to 2019 was overdetermined: no single factor caused it, but each amplified the others into a compound catastrophe. Firstly, Brent prices fell below $30, once again revealing the fragile fiscal architecture, as the government faced an immediate and brutal trade-off between servicing external debt and maintaining food and medicine imports. Macroeconomic mismanagement under Maduro transformed the fiscal crisis into a hyperinflationary catastrophe, as he started printing money, and triggering an inflation rate, which the IMF forecast at over 1,000,000% in 2018. The implementation of price controls further eliminated the economic incentive to produce or import food, medicine, and basic goods, resulting in severe shortages. GDP contracted by roughly 65% between 2013 and 2020 and an estimated 7m to 8m people (disproportionately the skilled professionals) emigrated from the country, making any recovery difficult.

Institutional Structure and Macroeconomic Constraints

State control over key sectors and its role in resource allocation

Venezuela’s economic governance is built around a highly centralized state which has historically owned, directed, or politically controlled the main channels through which foreign exchange, fiscal revenue, credit, and imported inputs are allocated. Although oil is at the center of this system, the model extends into electricity, heavy industry, telecommunications, banking, and parts of agriculture and mining. Over time, this shifted resource allocation away from the free market forces, and toward administrative discretion and political priorities.

A key institutional instrument is PDVSA, the national oil company that has long operated as the state’s main source of revenue and foreign exchange. The company is 100% state-owned, and the current governance structure does not clearly separate regulator and operator: the Ministry of Petroleum and PDVSA share leadership, concentrating oil policy, regulation, and commercial execution within the same political chain of command. In this framework we see weak oversight and accountability, and lower credibility of long-term contracting. It also means that investment decisions in the oil sector are judged inadequately on commercial return, and instead tied to fiscal needs, political objectives, and external constraints.

This concentration matters especially in Venezuela where oil revenues largely determine resource allocation across the economy. A long-standing feature of the system is that most foreign-currency supply is effectively centralized, since PDVSA’s foreign-exchange earnings are sold to the central bank in exchange for local currency. In practical terms, the state controls the principal source of dollars in an import-dependent economy, granting the executive enormous leverage over imports, subsidies, credit conditions, and the survival of firms that depend on access to foreign currency or imported inputs.

The broader consequence is a structurally distorted private sector. Once the state dominates energy rents, foreign exchange, and major utilities, firms become less able to compete on productivity and more on access to dollars, permits, public contracts, tax preferences, or political protection. This is the opposite of efficient capital allocation, rewarding proximity to the state over efficiency, and makes the business environment unstable as commercial viability hinges on discretionary decisions that can change quickly. The result is lower investment, weaker competition, and a persistent bias toward short-horizon, defensive business activity.

Consequences of fiscal reliance on oil revenues

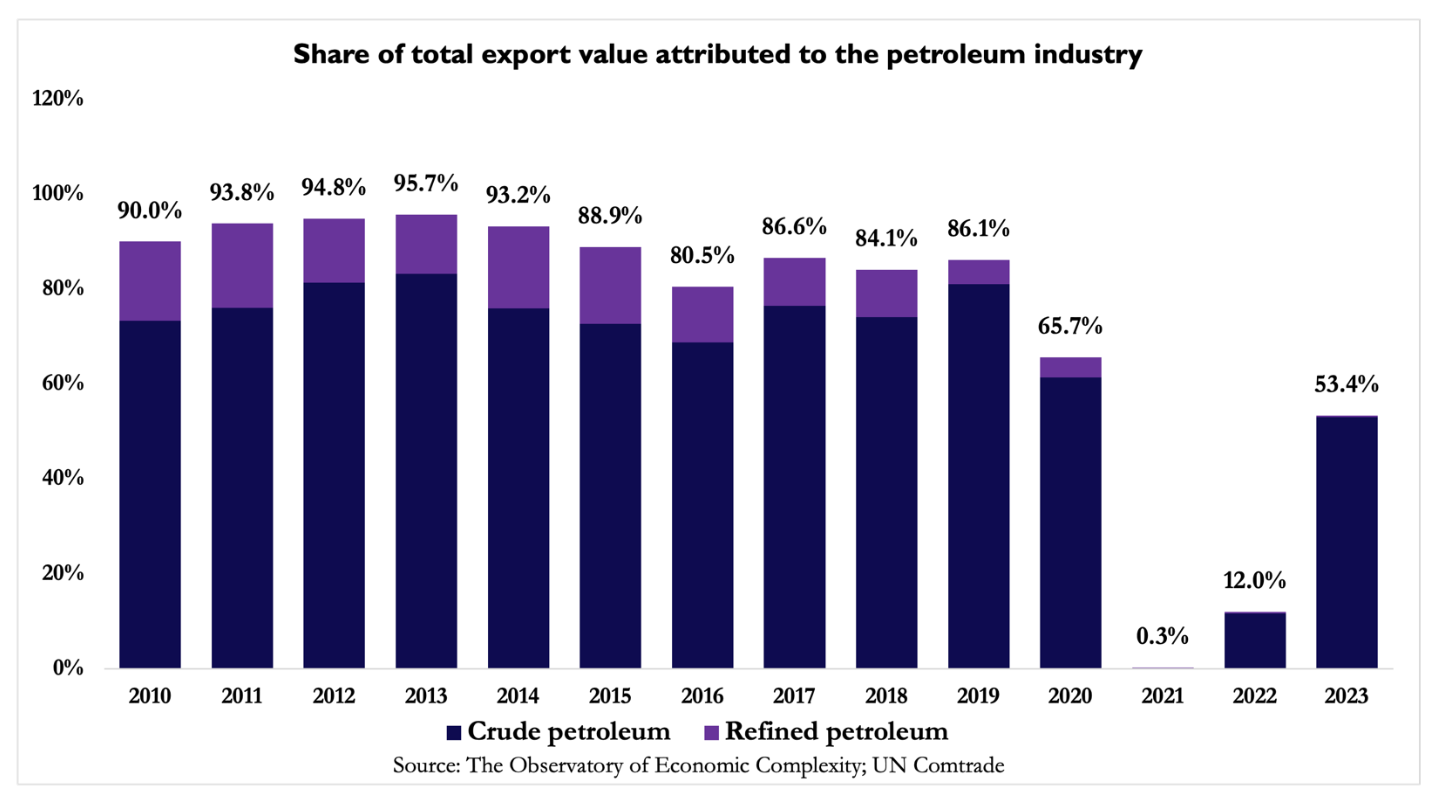

Venezuela’s fiscal system is unusually exposed to oil. According to the Natural Resource Governance Institute, oil and gas account for virtually all government revenue, while more conservative estimates place oil financing around 58% of the 2024 budget, indicating that fiscal capacity is tightly tied to a single volatile export commodity.

This dependence has two direct governance consequences. First, policy becomes inherently procyclical. When oil prices or export volumes rise, the state can expand spending, imports, and transfers without developing a broad domestic tax base. When oil receipts fall, adjustment is abrupt, as the government lacks diversified and stable revenue sources. As a result, Venezuela may hold the world’s largest proven reserves and still face acute macroeconomic stress when production, prices, or market access weaken. Second, heavy reliance on oil weakens the fiscal contract between the state and society. Governments funded through broad taxation are typically pushed toward more predictable administration, better information systems, and greater accountability. In contrast, petrostates rely on external rents rather than domestic taxpayers, reducing the need to build institutional capacity or maintain a stable relationship with the private sector. More fundamentally, this structure undermines the state’s ability to commit to long-term policy. When public finances depend on volatile and externally constrained export receipts, the state cannot sustain stable exchange-rate regimes, infrastructure spending, subsidy reform, or private investment incentives. In Venezuela, sanctions, declining production, and deteriorating infrastructure have made oil revenues uncertain in both timing and usability, restricting the country’s ability to convert its vast reserves into stable and predictable fiscal capacity.

Monetary governance and constraints on macroeconomic management

Venezuela’s monetary system has been constrained by three structural weaknesses: no central bank credibility, chronic fiscal dominance, and a shortage of dependable foreign exchange. The basic problem is that monetary policy has not operated as an independent stabilization framework. Instead, it has been subordinated to the fiscal and exchange-rate needs of a state dependent on oil dollars and struggling to fund spending through other, more credible channels. The IMF explicitly linked Venezuela’s collapse to its large fiscal deficits, record-high and long-lasting hyperinflation, massive currency depreciation, and debt distress. Official data show inflation easing from 2022-2024, however, recent estimates foresee a rebound, with inflation closing around 400% last year and projected somewhat conservatively at 387.4% for 2026 by the IMF. In response, the authorities have relied increasingly on monetary repression and exchange management:

The BCV has used very high reserve requirements and administrative liquidity controls to suppress credit creation. A February 2025 policy circular raised the penalty for reserve-requirement deficits from 28% to 60% per year and aimed to push the effective reserve requirement back toward the regulatory 73% level. That may help contain bolívar liquidity, but it also crushes intermediation, creating a banking system that cannot lend and therefore not support investment, working capital, or private-sector expansion.

The exchange-rate market shows a similar trend. Because the state controls most formal dollar supply, the BCV intervenes to defend the official market, though unable to fully meet demand. By early April 2025, the Financial Times reported the parallel exchange rate had moved to 101 bolívars per dollar, versus an official rate of 70.59, following U.S. policy tightening and reduced dollar supply. This gap is economically very significant because it fragments pricing and accounting, complicates import decisions, and increases uncertainty surrounding real costs and margins. Partial dollarization, covering 50-60% of transactions, has eased immediate pressures but does not substitute for a coherent and credible monetary framework.

Impact of institutional features on capital formation and economic efficiency

The most important economic effect of Venezuela’s institutional structure is not simply lower growth, but lower-quality growth. Capital formation remains weak as investors face overlapping uncertainty over property rights, contract enforcement, regulation, convertibility, and market access. Furthermore, a 2025 Swiss government report highlights Venezuela’s market opacity, limited access to foreign currency, weak legal security, and regulatory volatility as core constraints on attracting long-duration investment.

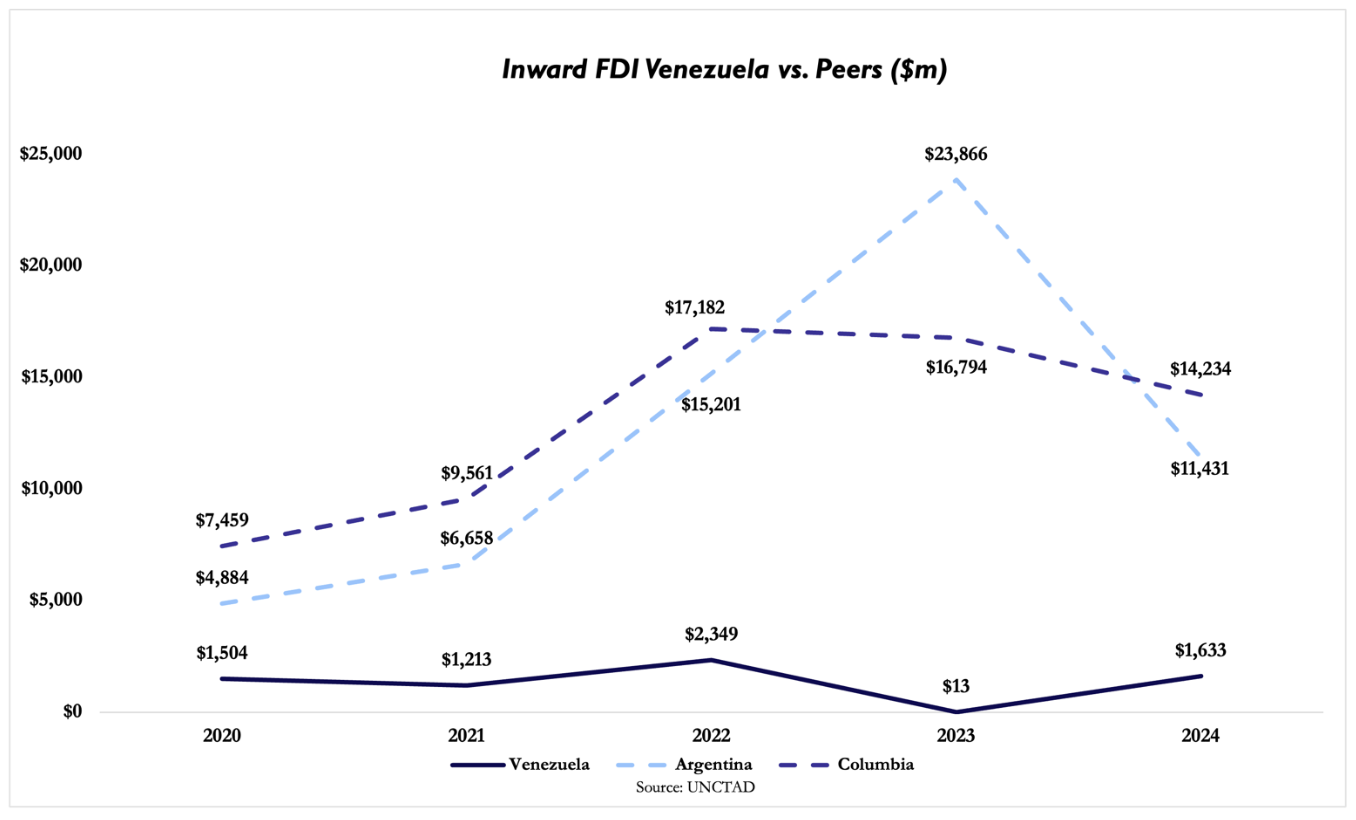

Recent UNCTAD investment data confirms this fragility with FDI inflows remaining broadly stagnant over 2020-2024, lagging significantly behind its growing regional peers. More tellingly, announced greenfield investment fell from $563m in 2023 to $94m in 2024, an 83.3% decline, signalling weak confidence in new productive capacity and long-horizon projects. Where capital does enter, it is concentrated in short-cycle activities, selective oil-linked exposure, or politically protected niches rather than broad industrial investment. This is a rational response to such an institutional framework, and results in persistent underinvestment in infrastructure, utilities, manufacturing, and formal finance, constraining productivity growth.

The core institutional constraint is structural, as the state acts simultaneously as owner, allocator, financier, regulator, and foreign-exchange gatekeeper, without the transparency or policy credibility required to perform these roles efficiently. This allows oil wealth to translate into solidified administrative control rather than drive productive investments. As long as this framework remains intact, any recovery or developments are likely to be partial, volatile, and dependent on temporary relief rather than durable improvements in capital formation or investor confidence.

Venezuela’s Oil Sector: Vast Reserves, Limited Output

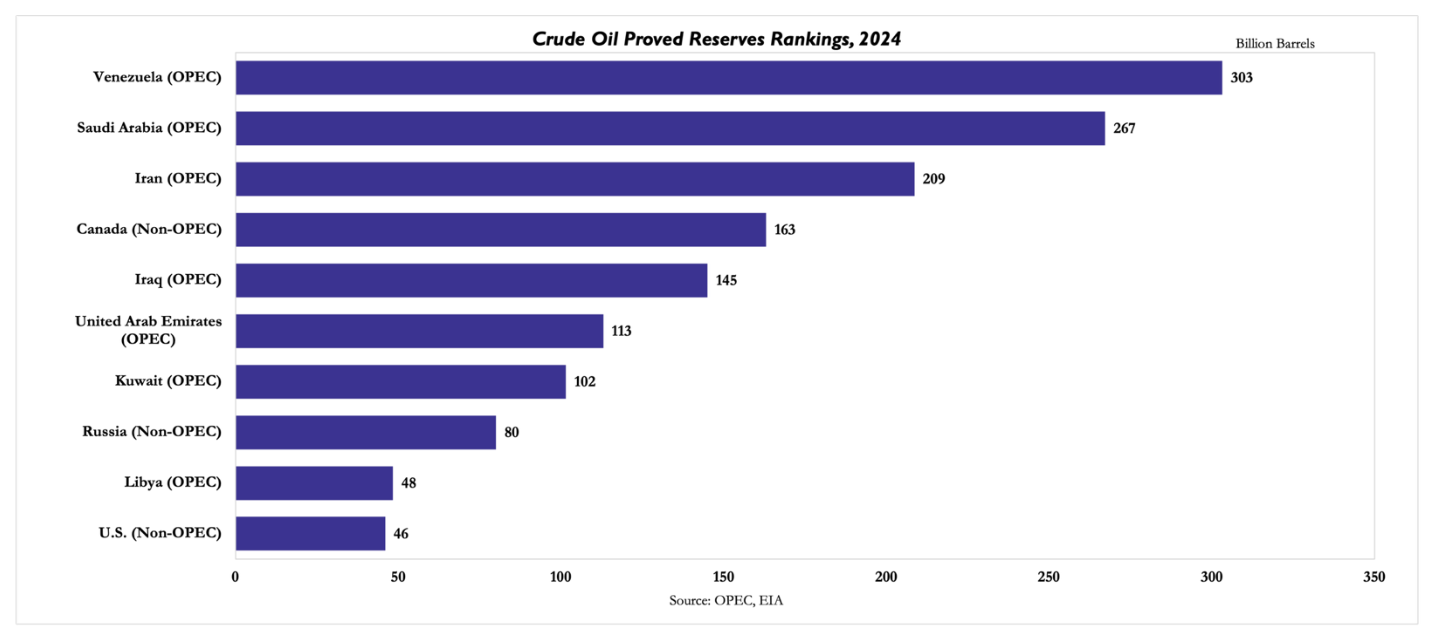

Venezuela ranks as the holder of the world’s largest proven crude reserves according to the main international estimates. EIA and OPEC report 303bn barrels for 2024, equivalent to roughly 17% of global reserves. This figure, while relevant for resource geopolitics, must be read with a clear distinction between the proved volume and the ability to convert it into exportable flows. In Venezuela, the average barrel quality is a constraint: the predominant share of proved reserves is extra-heavy, with high viscosity and density, which requires the use of diluents for transport and export and imposes blending and compatibility limits on global refining capacity.

Financially, the quality constraint directly affects the netback. This refers to the value realized per barrel after blending and processing costs. It raises upstream costs, increases dependence on diluent imports, and increases sensitivity to the availability of “complex” plants that can process heavy crude. For this reason, even with large proven reserves, the Venezuelan supply function is more rigid and more dependent on external capital and know-how than that of producers with lighter crudes. This dependence also gives U.S. policy unusual leverage over Venezuelan oil, since sanctions and licensing rules directly affect access to diluents, shipping, and the commercial channels for crude oil exports. This structural dependence becomes clearer once the focus shifts from aggregate reserves to the part of the sector where those barrels are concentrated and how they are actually brought to market.

The Orinoco Belt is what gives the reserve base its strategic weight. Spread across the Boyacá, Junín, Ayacucho, and Carabobo areas, it contains the extra-heavy crude base on which Venezuela’s long-run oil future rests. This extra-heavy crude oil often requires dilution and upgrading to a lighter synthetic crude before it can enter broader refining markets. This technical requirement is central to understanding both the limitations and the continued relevance of Venezuelan output.

Even at reduced output, these barrels still matter because heavy, sour crude has been relatively tight in recent years, particularly for refineries configured to process it, especially those on the U.S. Gulf Coast. This creates a structural demand niche that Venezuela is still positioned to serve, despite its lower production levels. Beyond refinery-level demand, Venezuela’s current production is too low to set the global oil balance. However, its reserve base still matters for Atlantic Basin heavy-crude supply and refinery economics, while also preserving strategic leverage for U.S. policymakers over future export flows. In a market still sensitive to OPEC supply discipline and to shipping risk through the Strait of Hormuz, a large heavy-crude reserve base outside the Gulf retains strategic value as a potential source of supply diversification. This disconnect between large reserves and limited output makes production dynamics the key variable in assessing Venezuela’s actual role in the oil market.

Production is where the distance between Venezuela’s resources and state capacity becomes visible. EIA estimates Venezuelan crude output at approximately 3.2m barrels per day in 2000 and 846,000 barrels per day as of February 2026. That amounts to a 73% cumulative decline from 2013 levels alone. This sharp contraction reflects not a single shock but a sequence of overlapping institutional, financial, and external disruptions.

The collapse unfolded in phases. The first break came after the post-2001 mass firing of nearly half of PDVSA’s workforce, which left the state-run company with severe maintenance deficiencies and a reduced ability to run operations. A second phase followed in 2006 under chronic underinvestment, growing fiscal extraction from PDVSA, and the deterioration of field services and infrastructure.

A third phase came with sanctions escalation from 2017 and the January 2019 U.S. sanctions on PDVSA, which shut the main U.S. market and complicated trading, payments, and fuel-swap arrangements. The modest rebound from 2021 onward stemmed from narrower mechanisms: Iranian diluent shipments, technical support on specific fields, the return of some service providers after partial debt settlements, and the November 2022 U.S. waiver that let Chevron [NYSE: CVX] restart exports to U.S. refineries in January 2023. Export data show the same fragility. Reuters reported that exports rose from 498,000 barrels per day in December 2025 to about 1m barrels per day in March 2026 as stored barrels were released and licensed traders resumed liftings. That rebound reflected reopened channels as much as healthier upstream operations. Those phases explain how the collapse unfolded, but not on their own why production still struggles to recover.

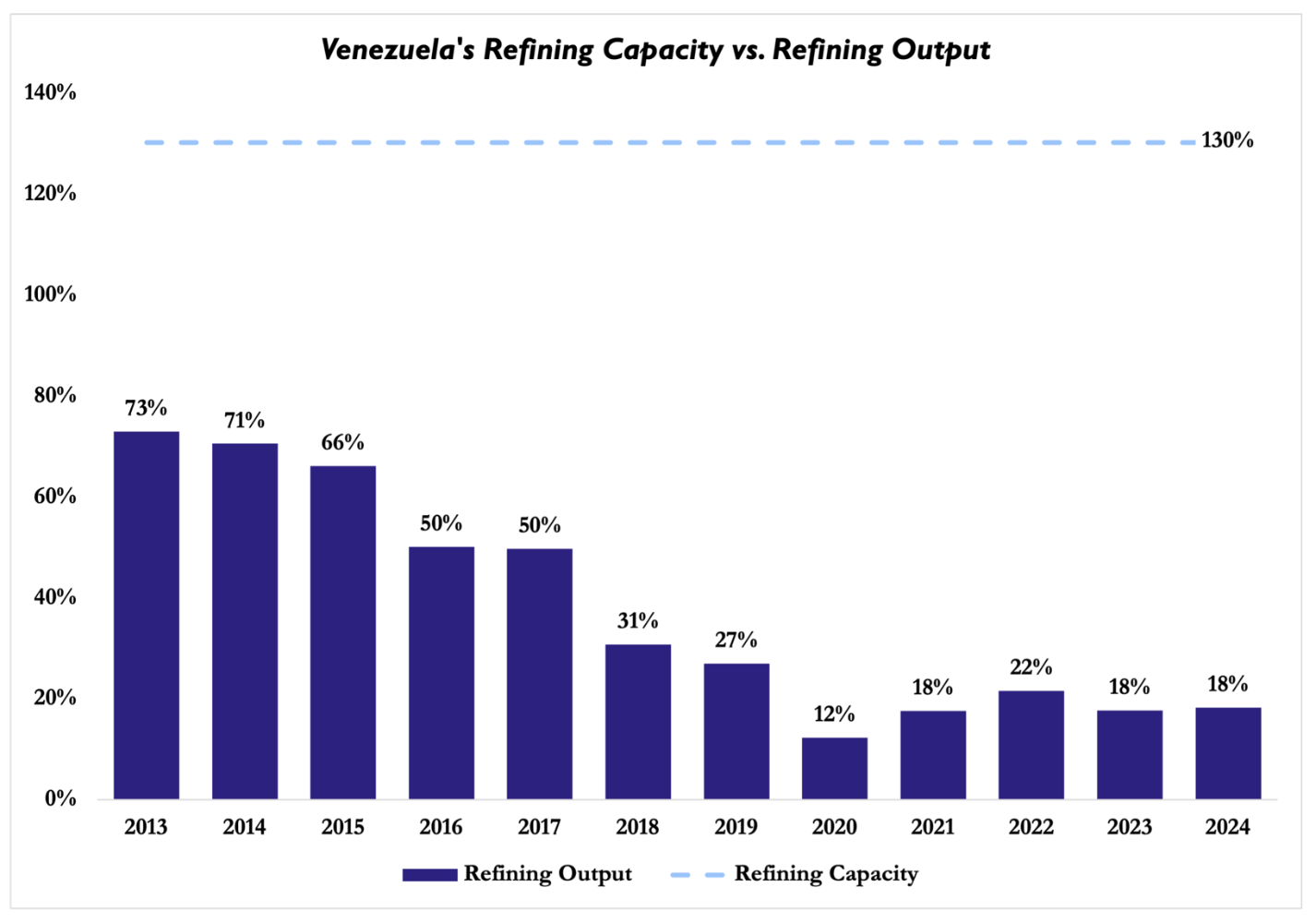

The first reason output remains capped is the interaction between geological quality and operational weakness. Venezuela’s extra-heavy crude needs diluent to be transported and processed, and shortages translate quickly into lower field output. That was visible in 2023, when EIA linked lower production to diluent shortages. The second reason is that nominal capacity has lost much of its meaning. IEA’s March 2026 report put sustainable crude capacity at only about 1m barrels per day, with effective spare capacity of 140,000 barrels per day in February. Downstream figures are even more misleading. PDVSA’s refineries still total about 1.36m barrels per day of nameplate distillation capacity on paper, yet EIA reported throughput below 300,000 barrels per day and operating rates at the core Paraguaná complex around a tenth of nameplate capacity in late 2023. Installed capacity, actual production, exports, and effective refining capability are therefore four different numbers, and in Venezuela they diverge sharply. Together, these factors explain why nominal capacity figures overstate Venezuela’s ability to translate resources into sustained production.

More broadly, the constraint set is systemic rather than isolated. Power outages, storage congestion, weak port logistics, and poor domestic fuel supply add to the ceiling. Outstanding debt and sanctions-related payment frictions then made it harder to retain service providers and source equipment. These problems feed on each other. When export channels narrow, storage fills up, and production must be cut. When diluent is unavailable, extra-heavy output stalls. When refineries underperform, the domestic fuel system becomes a further drag on upstream operations. This is why Venezuela can add barrels at the margin but struggles to sustain multi-year growth. This interaction of constraints is what ultimately defines Venezuela’s production ceiling.

PDVSA still occupies the center of the sector in legal form. It was created after nationalization in the 1970s, remains the state oil company, owns the domestic refineries, and controls most of the major midstream infrastructure. Under the pre-2026 mixed company framework, foreign firms could invest, but PDVSA generally had to retain a majority stake. That formal architecture still matters because legal title, licensing, and relations with the state continue to run through PDVSA. Yet formal control is no longer the same as operational strength. EIA notes that the Venezuelan state used PDVSA as a fiscal vehicle, imposing heavy levies and diverting cash that might otherwise have been reinvested. The company remains strongest on paper in the parts of the chain where performance is weakest in practice, especially refining and infrastructure management. Where production has stabilized, it has usually done so through joint ventures, imported inputs, foreign technical know-how, or partner-led field rehabilitation. The result is a widening gap between formal ownership and the operational capacity needed to sustain production, which is why external partnerships now sit at the center of the sector.

Chevron is the clearest example of that dependence. Chevron’s official Venezuela page lists five projects, including Petropiar in the Orinoco Belt and four non-operated joint ventures with PDVSA. EIA estimated in late 2023 that ventures associated with Eni [BIT: ENI], Repsol [BME: REP], and Maurel & Prom [EPA: MAU] could add about 50,000 barrels per day in the near term. Maurel & Prom’s 2025 annual results provide one of the few disclosures available: its production at Urdaneta Oeste averaged 8,194 barrels per day in 2025, up 34% from 2024. Repsol told investors in March 2026 that its 2026-2028 outlook excludes Venezuela, suggesting that any upside there depends less on booked base operations than on fresh permissions and workable commercial terms. Public partner-level reporting remains limited, and that lack of transparency is itself part of the sector’s investment problem. Incremental gains in output are therefore coming less from PDVSA acting alone than from projects where foreign partners provide the capital or commercial channels. That growing dependence on external operators leads directly to the question of who actually controls the sector.

Legal ownership still sits with the Venezuelan state. The January 29, 2026, reform remains useful as a benchmark because it preserved state ownership of hydrocarbon reservoirs even while allowing private companies to assume full management of project activities at their own expense and risk, subject to approval by the Oil Ministry. Operational management is therefore becoming more private and more project-based. A barrel only reaches the market if someone can lift it, insure it, ship it, finance it, pay for it, and route the proceeds through a permitted channel. In that sense, sovereignty over the reservoir does not amount to sovereignty over the sale. Under the current sanctions regime, the divide between legal ownership and effective commercialization becomes even sharper.

After the January 2026 U.S. intervention and Maduro’s capture, Washington replaced the earlier carve-out model with a broader but tightly conditioned licensing regime. In practice, U.S. entities were allowed to buy, transport, refine, and market Venezuelan-origin oil, selected foreign partners were allowed to operate in oil and gas projects, and U.S.-origin diluents, technology, and new investment contracts became permissible under Treasury-defined conditions. The change was large in operational terms, but it was not a return to unconstrained trade. It was a move from prohibition to managed permission.

The conditions attached to those licenses also show where commercial control now sits. Payments owed to PDVSA or the Venezuelan state had to go into Treasury-designated accounts under a mechanism created by Executive Order 14373. Maurel & Prom noted that its agreements with PDVSA had to be governed by U.S. law, with payments routed through channels set by U.S. authorities. Reuters later reported that the first completed sales were being held in U.S.-controlled accounts. Venezuela still owns the oil but turning it into revenue now depends on external legal and financial controls.

Considering these operational and legal shifts, the 2026 opening improved market access without restoring a normal investment case. On February 20, 2026, the United States ended the additional tariff actions attached to the March 2025 order on countries importing Venezuelan oil. At the Venezuelan end, the January 29 reform improved the legal offer to investors by allowing private management, independent arbitration, and a royalty cap of 30% with project-level flexibility. Those are material changes. Yet the gap between announced reform and implemented capacity remains wide. What has been implemented so far is the licensing architecture and the first externally supervised sales. What remains partly prospective are the larger field expansions. Reuters reported in March 2026 that Chevron and Shell were nearing major new production deals, but public company reporting has not yet translated that into booked output. Repsol’s own guidance still treated the Venezuelan upside as outside the base case.

For investors, that means the improvement is tactical before it is durable. Venezuela still offers reserve depth that few jurisdictions can match, and the 2026 reforms lowered some of the legal and operational barriers that had kept capital away. Yet the investability case remains conditioned by factors outside the reservoir and partly outside the country: OFAC licenses, U.S.-controlled payment channels, externally acceptable counterparties, foreign law and arbitration, degraded infrastructure, and thin project-level transparency. For policymakers, the same point cuts into the sovereignty question. The right to commercialize Venezuela’s resources depends on foreign operators, imported inputs, licensed traders, and payment structures designed abroad. The country still has oil. What it lacks is full control over the chain that turns oil into cash.

Rebuilding Venezuela’s Oil Sector: Costs and Constraints

There is no credible pathway for a rapid return to Venezuela’s historical oil production levels. Even under favorable assumptions, restoring output would take years, and more ambitious scenarios of production increases are modeled on timelines exceeding a decade.

From the perspective of required investments in the sector, a distinction must be made between short-term stabilization and full recovery. In the near term, production can increase through the rehabilitation of existing wells, pipelines and facilities. CapEx estimates for this first phase are in the $10bn–20bn range: they include restarting idled fields and restoring basic infrastructure. This could increase production by a few hundred thousand barrels per day, targeting roughly 1.4–1.5m barrel/day within a few years. However, this is just the cost for stopping the more recent decline, not for rebuilding the sector. A return to higher production levels requires a much more ambitious investment cycle. Internal PDVSA planning documents, which had been circulated in 2021, estimated that around $58bn would be required to restore production to late-1990s levels, while a broader modernization programme covering production, transport, storage, and refining would require closer to $77.6bn. Worse still, third-party estimates are significantly higher: energy consulting company Rystad Energy estimated in early 2026 that, over a timeline going until 2040, approximately $98bn are needed to reach production of 2.2m b/d, around $110bn to approach 2.5m b/d without full modernization, and up to $180bn–$200bn for a comprehensive modernization and expansion of the Venezuelan oil industry. The majority of investments is required in upstream projects, with more than $69bn (from PDVSA’s own document) which needs to be allocated to crude production infrastructure. However, given the broader deterioration of the system, midstream and downstream components (pipelines, gas injection systems, terminals and refineries) require additional $7.6bn according to PDVSA, which nowadays even appear to be downward-biased estimates.

Beyond infrastructure CapEx, Venezuela’s return to sustained production is hindered by its heavy crude, which requires blending with lighter hydrocarbons, such as naphtha (currently mainly imported from Russia and China), to be transported and processed. At higher production levels, this creates a structural dependency on imports of diluents; this, however, could be solved by reestablishing a trade relationship with the U.S.

The sequence of investment is also important to consider. Initial gains can be achieved by smaller operators capable of restarting marginal fields with limited capital. However, this would not be sufficient to materially alter Venezuela’s position in global oil markets. A sustained recovery would require large-scale and long-term investment that only major international oil companies could undertake. Estimates from Rystad’s analysis suggest that $30bn–$35bn of external capital would need to be committed within the first few years to support a credible recovery path.

The real constraint to Venezuela’s oil production recovery, however, is that the required investments might just not make sense financially. If investments coming from Venezuela’s government might be justified when accounting for all the related externalities on the domestic market (heavily dependent, even fiscally, on oil production), such considerations do not apply for the over $30bn of required external capital, and the project economics of oil production in Venezuela are discouraging. The heavy, sour and highly viscous nature of Orinoco Belt crude causes it to trade at a discount to benchmark grades. Even before considering the risk of infrastructure degradation and geopolitical tensions, these characteristics place Venezuelan production in the higher end of the global cost curve. Operational conditions add another layer of complexity. Frequent power outages, infrastructure failures and distortions in the domestic financial system also disrupt the continuity of operations and increase costs. In particular, the heavy oil extraction processes needed in the region are particularly sensitive to interruptions, as they often require continuous steam injection and stable operating conditions.

These factors are reflected in estimates of break-even oil price. Recent assessments place Venezuelan heavy oil projects at a break-even above $80 per barrel, with some estimates extending toward $90 depending on fiscal terms and project structure. This represents a material increase from Rystad’s 2020 estimates in the $40–$60 range, indicating that the deterioration of infrastructure and operating conditions has pushed Venezuela into a significantly less competitive cost position even over a short period of time.

This has direct implications for investment decisions. Venezuelan projects must compete against alternatives that are often both cheaper and less risky. Break-even levels in Guyana are estimated around $35 per barrel, while in the U.S. Permian Basin they are below $50. Gulf of Mexico brownfield projects and Canadian oil sands developments also offer competitive cost structures under more stable operating environments. Investments in Venezuela, in fact, carry additional risks related to contract stability, regulatory uncertainty and political continuity. Large-scale oil projects require decades to generate returns, making long-term legal and contractual stability a crucial prerequisite. The historical record of contract renegotiation, expropriation and unpaid obligations of Venezuela goes directly against this.

The recent escalation in the Middle East has materially changed the context in which Venezuelan oil is being assessed. The disruption of flows through the Strait of Hormuz, through which roughly one-fifth of global oil supply transits, triggered a sharp spike in prices (Brent crude exceeding $100 per barrel). In this context, Venezuelan oil also acquires a strategic dimension. From a geopolitical perspective, expanding output in Venezuela could serve not only economic but also security objectives, reducing exposure to politically unstable suppliers. However, the simple reasoning of the currently higher oil price being a justification for investing in Venezuela does not work. The environment we are currently observing reflects a severe but potentially short-lived disruption. Oil markets have already shown significant volatility as conditions in the Strait evolve, with prices falling sharply once flows partially resumed. This creates a mismatch between short-term incentives and long-term investment requirements. Additionally, high oil prices can improve the investment case, but they do not resolve the underlying constraints. A sustained price environment around $100 per barrel would make more projects viable, particularly those with higher upfront costs, but heavy crude would still trade at a discount, operational inefficiencies would persist, and political and contractual risks would remain.

Beyond Oil: Economic Outlook and Limits to Diversification

Even if oil production were to recover only gradually, the broader question is whether Venezuela’s economy can generate sustainable growth from other sectors and thus move away from being a petrostate. Starting from 2021, Venezuela has returned to economic growth, albeit moderate, after a period of severe depression. Data disclosed by the central bank of Venezuela point to a 7.1% y-o-y increase in GDP in Q4 2025, supported by both oil and non-oil sectors. However, independent estimates point to a weaker figure and inflation remains among the highest in the world. Price increases exceeded 400% in 2025 which, despite signs of deceleration, continue to distort other economic signals and reduce real purchasing power. Additionally, much of the recent expansion reflects the reactivation of idle capacity accumulated during years of economic contraction, rather than new investment or productivity gains.

Economic signals after the U.S. intervention in January are still positive. Towards the end of Q1 2026, oil production has recovered to above 1m barrels per day, supported by improved export conditions. This, in turn, helped Venezuela manage its foreign-currency balance, beginning to stabilize parts of the economy. The inflows from increased oil exports are also accompanied by spillover effects, supporting activity in manufacturing, trade and services, and driving demand in construction through infrastructure needs linked to oil projects. Yet, the current recovery remains moderate, highly dependent on oil, and largely cyclical.

Beyond oil, Venezuela possesses significant but underutilized economic potential across multiple sectors. The country’s natural resource base is particularly large. In addition to hydrocarbons, it holds substantial deposits of gold, iron ore, bauxite and coal, as well as a range of industrial and strategic minerals including nickel, copper, zinc and coltan. Estimates point to billions of tons of coal and iron ore reserves, alongside meaningful gold resources. Despite this, much of the mining sector remains underexploited, with limited industrial-scale production and declining output over the past decade as investment and operational capacity deteriorated. This sector could become a new area of growth: coal production has been restarted in late 2025, with ambitions of significantly increasing its exporting capacity. At the same time, newly-passed legislation aims to open mining to private investment, offering longer concession periods and improved legal guarantees. The declared objective is that of differentiating the tale of the Venezuelan economy from just its oil reserves and production.

Construction represents another key area of expansion, although it is linked to developments in the oil sector and mostly functions as a transmission channel for it. Manufacturing, trade and services also show signs of recovery. These sectors historically accounted for a significant share of GDP and employment, and recent improvements in the availability of foreign currency have supported their reactivation. However, much of this expansion reflects a general improvement of economic conditions rather than sector specific investments or upgrades. The agricultural sector is experiencing a more uneven path, but its outlook is not necessarily grim. The coexistence of large commercial farms and small subsistence operations highlights a fragmented structure, with significant scope for productivity improvements through its modernization.

Overall, it is clear that Venezuela’s economic potential does not need to be limited to its oil sector. The country benefits from abundant natural resources, a strategic geographic position, and a relatively young, low-cost labor force. Hydroelectric capacity and widespread access to electricity also provide a potential industrial base, even if infrastructure requires substantial work. Once again, however, a history of misguided policy decisions means that the potential remains largely latent. Mining is underdeveloped, agriculture operates below potential, and industry remains vulnerable to fluctuations in demand and import competition. These sectors might appear as investment opportunities with large margins for growth, but historical factors which led to the current state of the economy persist to this day. Mostly, macroeconomic instability and uncertainty over the political regime. Inflation remains extremely high, exchange-rate dynamics are unstable, and there are significant foreign-currency shortages for what concerns the macroeconomic conditions; at the same time, legal uncertainty, inconsistent regulatory frameworks, and a history of expropriations have undermined investor confidence. On top of this, Venezuela ranks among the weakest globally on corruption and economic freedom indicators. This has led to a sharp decline in foreign direct investments, with many multinational companies that exited the market or scaled back operations.

The recent policy changes suggest a tentative shift toward liberalization, particularly the new hydrocarbons and mining laws which reduced state control and improved operational autonomy, but implementation remains incomplete and their credibility is far from proven. The U.S. intervention, in a way, functioned as a catalyst for foreign investors to start reevaluating the potential for investments in Venezuela. The major financial newspapers have reported recent on-site visits by asset managers, hedge funds and private equity groups; however, they were mostly exploratory as investor interest remains cautious. Nonetheless, it is a signal that Venezuela’s recovery is generating renewed attention from global investors, particularly those specializing in distressed or frontier markets. What stands true is that large-scale institutional capital, in order to flow into the country, will first require significant improvement in the investment framework and legal protection.

Overall, Venezuela’s economic outlook is defined by a clear tension. The country combines an extraordinary resource wealth and discrete sector potentials with historically weak infrastructure and institutions. The transition from a cyclical, oil-driven recovery to an investment-led growth model will therefore depend on the credibility of its measures to create the conditions that would allow much-needed external capital to flow into the country.

0 Comments