Introduction

“Content is where I expect much of the real money will be made on the Internet, just as it was in broadcasting.” Bill Gates wrote that in January 1996, in an essay better remembered for its three-word title, Content is King, than for the prediction itself. Three decades on, the prediction has aged well; what has surprised observers is who ended up making the money. What Gates did not anticipate, and few did at the time, was where the value would accumulate. The platforms hosting the content capture a share, but the largest economic surplus has flowed to a new class of media owner: the creators themselves. And three decades later, the businesses they have built on top of YouTube channels and online communities are large enough, and stable enough, that a second group has joined them as co-owners: private equity sponsors looking to institutionalise what creators built informally.

What used to look like one person filming in a bedroom has become something corporate finance recognises: a media business with an audience, a brand, and a set of cash flows that, in the right hands, look more like consumer staples than like entertainment. Two examples make the point. Feastables, the chocolate brand launched in January 2022 by the YouTuber Jimmy Donaldson, better known as MrBeast, reached an estimated $250m in gross revenue by 2024 with effectively no paid marketing budget, and is now sold across more than 5,000 US retail stores. It competes for shelf space with Hershey [NYSE: HSY], a company founded in 1894 that spends roughly 10 to 15% of revenue on advertising to defend its 30%-plus share of the US chocolate market. Pinkfong’s “Baby Shark Dance,” meanwhile, has accumulated more than 16bn views since June 2016, averaging close to 1.3 plays for every person on Earth, and Pinkfong now operates as a fully-fledged children’s IP business, with Nickelodeon-co-produced TV, Netflix specials, live tours, and a feature film in development. Neither result was achieved by outspending an incumbent on media. They were achieved by owning an audience the incumbent had to rent.

Gates’s analogy to broadcasting still holds, but the centre of gravity has shifted. Broadcast television remains an enormous business in absolute terms: Fox News averaged 2.4m primetime viewers in 2025, the last Super Bowl drew over 120m US viewers, and YouTube itself paid out around $36bn in advertising revenue to its content partners and rights holders that year. What has changed is the unit of value. Broadcasters sell scheduled access to a passive audience, paid for by advertisers buying thirty-second windows of attention. Creators sell something closer to a relationship: a recurring, opt-in connection with a community that follows them across formats, products, and platforms. That relationship monetises on different terms. Sportico reported in late 2024 that MrBeast charges in the region of $3m for a sponsor placement inside one of his videos, roughly double what advertisers paid for a 30-second spot during the NFL’s Thanksgiving games, and his videos continue to accumulate views, and sponsor impressions, for years after upload. The same logic applies further down the food chain: niche creators with audiences in the low millions routinely command CPMs that broadcasters with twenty times the reach cannot match, because the audience trusts the source. It is this trust premium, scaled across an entire economy of channels, that has caught the attention of institutional capital.

The macro numbers tell the same story. Goldman Sachs estimates the creator economy could approach $480bn by 2027, while the IAB projects US creator-directed ad spend at $37bn in 2025, up 26% year-on-year. Inside those totals sits a growing slice that no longer behaves like social media at all: digital-first children’s franchises, education channels, automotive networks, gaming-and-lore studios. These are businesses that look less like influencers and more like the next generation of media companies, with IP, recurring revenue, and operating leverage waiting to be unlocked.

It is this last piece that has pulled private equity in. The same features that make a creator business compelling, namely loyal audience, low capital intensity, and monetization upside well beyond platform ads, also make it look, from a sponsor’s seat, like an underbuilt company. The opportunity, at least on paper, is to turn channels into companies, audiences into diversified revenue streams, and personality-led brands into IP that survives its founder. The harder question is whether that conversion is actually possible: whether businesses built on one person’s authenticity can be professionalised, scaled and exited without breaking the very thing that gave them value in the first place. The rest of this article works through how PE has been trying to answer it.

Why creator businesses fit the PE mould

A primary reason for private equity’s move into creator businesses is that, when they are mature, they have inherently and unusually attractive business characteristics. Firstly, demand within an established creator’s audience tends to be sticky, reinforced by the large organic audiences and deep niche communities these businesses build. The business model is also asset-light and requires minimal physical capital expenditures. That is to say, creator businesses combine low-cost commitments with comparatively low revenue volatility, underpinned by high audience engagement. Monetization channels are oftentimes already in place (more on this later), and as past ventures have demonstrated, audience loyalty is a versatile and valuable asset that sponsors can repeatedly monetize.

That is not to say creator businesses are objectively the most sponsor-attractive assets to have existed; however, they may very well be among the most attractive available today. There exists a tremendous oversaturation in the private equity industry. From there being more PE-backed US companies than there are public ones, to KKR co-founder Henry Kravis’ rhetoric on how the LBO model has fundamentally evolved since the 1980s, it is fair to say that competition for high-quality assets has become fierce. The corollary is that investors have had to diversify their capital allocation, and creator businesses have presented themselves as ample opportunities.

In terms of which segments are the most attractive, it can be observed and rationalized that kids’ content, education and science, gaming and lore, automotive, hobbies and lifestyle, and consumer-product-driven creators lend themselves best. The reason being that private equity firms look for businesses with low cash flow volatility. The less alienating and the more brand-safe the content, the easier it is to generate continued cash flows from all monetization streams.

In terms of which segments are the most attractive, it can be observed and rationalized that kids’ content, education and science, gaming and lore, automotive, hobbies and lifestyle, and consumer-product-driven creators lend themselves best. The reason being that private equity firms look for businesses with low cash flow volatility. The less alienating and the more brand-safe the content, the easier it is to generate continued cash flows from all monetization streams.

To capitalize on the recognition of this opportunity, PE funds have applied a familiar model.

The creator business model

For YouTubers, their business model is built on the YouTube Partner Program (YPP), a valuable program that offers creators access to several revenue streams, support, and exclusive events. To be eligible for the YPP, creators must have 500 subscribers, 3,000 watch hours on their long-form videos, or 3 million views on YouTube Shorts. These requirements give them access to fan funding features and personal product promotion. Once a creator reaches 1,000 subscribers, 4,000 watch hours, and 10 million Shorts views, they become eligible to earn revenue from ad shares, among other benefits.

Here are a few ways that YouTubers can earn revenue through the YPP:

- Ad revenue sharing: Creators earn 55% of ad revenue from long-form videos and 45% from Shorts.

- Fan funding: Creators can monetize their fan base through channel memberships, super chats, and other features.

- Shopping: Creators can sell their own products (e.g. merch) or affiliate products through their content.

- YouTube Premium revenue sharing: Creators earn a share of the revenue from YouTube Premium subscribers’ views.

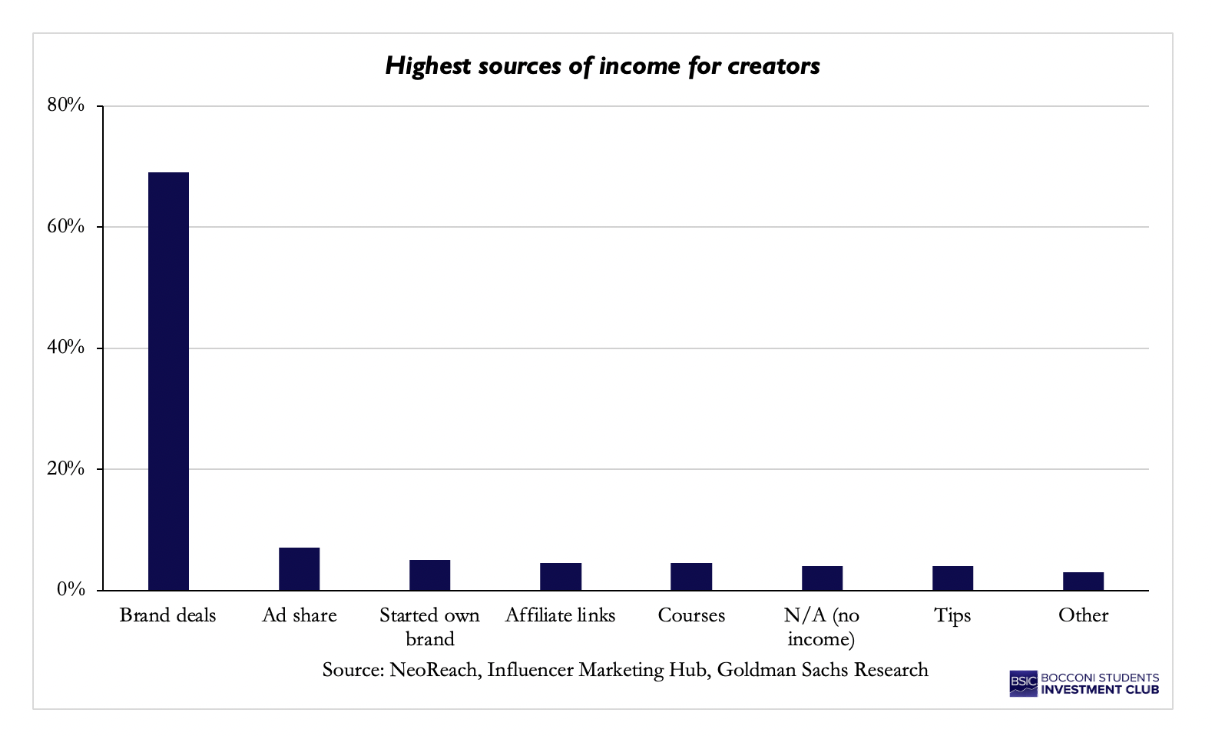

This provides a financial base for most creator businesses to build upon; however, the YPP is a structurally weak revenue stream in isolation. Over the period between 2021 and 2025, YouTube paid out over $100bn to creators, artists, and media companies. This confirms the scale of the video-sharing platform’s monetization engine, but also highlights its concentration risk. Any change in algorithm, advertiser CPMs, or a demonetization event (e.g. the 2017 “Adpocalypse”) will significantly reduce a channel’s income. Thus, any creator or channel that attracts institutional capital is one that has used platform reach as an acquisition funnel rather than solely a revenue stream. This can be seen in that, in 2024, brand deals accounted for 68.8% of creator revenue, while ad revenue sharing comprised only 7.3%.

A truly diversified creator business typically layers five to six revenue streams on top of its ad revenue base. As mentioned above, sponsorships and branded content account for the largest share of creator revenue, reflecting advertisers’ willingness to pay for creator audiences’ trust and specificity. Affiliate marketing represents the third layer, a commission-based revenue stream with low friction but low margin and non-recurring. The next layer consists of merchandise and consumer products: these are direct-to-consumer products with higher margins than ad revenue and are platform-agnostic, meaning they generate value regardless of which platform distributes them.

At the top end of the revenue stack, we have paid memberships, subscriptions, and digital products such as courses and newsletters. For creators, these represent recurring revenue and higher-quality cash flow: for example, YouTube channel memberships pay creators ~ 70% of fees. The highest-quality cash flow layer consists of licensing and intellectual property (IP): character IP, format rights, and music rights generate recurring revenue such as royalties without the need for ongoing creator output. Finally, live experiences and events, such as CoComelon On Tour, command high revenues per attendee but are extremely capital-intensive and operationally complex.

For creator business models, diversification is the core financial point. On one end of the spectrum, single-revenue creator businesses that rely on shared ad revenue and ad hoc sponsorship deals demonstrate lumpy, non-recurring revenue that is heavily dependent on continued creator output. These businesses are priced as media assets at the lower end of the valuation range. On the other end of the spectrum, we have diversified creator businesses that generate recurring cash flow, carry IP that can be licensed separately, and are less dependent on active output. The prime example of the latter business model is CoComelon, whose owner Moonbug Entertainment was acquired by Candle Media, a Blackstone-backed vehicle, for ~ $3bn in 2021. Candle Media was not acquiring a YouTube channel, but a character IP franchise that monetized a number of channels: streaming licensing, music, toys, live experiences, and international adaptations. The takeaway is that character-based IP is platform-agnostic and, therefore, commands a higher valuation multiple than personality-based content tied to a human face that can age or generate controversy.

It is between these two extremes that PE firms see the value-creation opportunity that they have been attempting to capture. The goal is to convert attention and audience loyalty into recurring, IP-based revenue that commands a higher multiple due to its stability and scalability.

The buy-and-build playbook

The PE playbook is one we’ve seen before: buy companies within an asset class, benefit from economies of scale, build out the businesses, and exit.

The first step in the playbook is the acquisition. We’ve primarily observed growth equity and majority stakes, and rarely classic LBOs. The reason being that obtaining high leverage requires a proportionately large amount of tangible assets, which most creator businesses lack. Furthermore, the cash flows, while less volatile than other assets in the media industry, are still too volatile to support the leverage required for an LBO. (Perhaps as the asset class matures further, we could eventually see a risk profile acceptable to private credit issuers.)

Once the sponsor has acquired its stake, it is essential that they keep the creator engaged. Reason being that the underlying asset is the audience’s relationship with the creator. This is both the greatest strength and the greatest risk of the investment: it is fundamentally dependent on one person. To bridge this difficult predicament, a playbook best exemplified by the YouTube creator Veritasium is used. Veritasium was bought out by Electrify Video Partners in 2023 (more on that later). Since the majority investment, Derek Muller, the face behind the channel, has appeared progressively less in videos. The pace was deliberate: slow enough to preserve the audience’s relationship with the channel, fast enough to gradually shift Veritasium from a persona to a wider brand. This acts not just as a hedge against the whims of the founder but also allows content output to scale beyond the constraints of one person.

This leads nicely onto the third step of the process: business expansion. Sponsors install professional management and operating infrastructure to build out content production. This is where economies of scale between businesses come in. On the sponsor side, this is obviously massively beneficial in terms of cash flow generation; however, it should be noted that this has been known to lead to a certain degree of homogeneity between content, a negative factor for audience loyalty to be considered over the long run.

That being said, the content buildout is essentially a build-out of the underlying platform. This platform is monetized through advertising, sponsorship, and add-on ventures, which we expand upon in the following section.

Value creation levers

We group the value creation levers into three buckets.

- Revenue diversification and growth: While platforms like YouTube generate built-in ad revenues, far more money is to be made through professional sponsorships. Not only do these pay more per viewer, but they also make for longer-dated cash flows. That is, however, only one facet. The other, and arguably more compelling, is the ability to create spin-off businesses with a customer base that exhibits uniquely inelastic consumption behaviour. This creates a plethora of knock-on effects in terms of pricing power, lower barriers to entry, etc., which the sponsor can leverage to create ventures with uniquely stable cash flows.

- Operational efficiencies: Alongside the business acumen PE sponsors tend to have in expanding operating margins, we once again return to the concept of economies of scale across a sponsor’s portfolio. In the back end, they have the ability to centralize finance, legal, and HR. Consumer-facing, shared production resources and pooled ad operations also lead to cost synergies.

- Multiple expansion: This is more of an implicit lever; however, it is a tangible driver of returns. As the creator business shifts away from its dependency on the original creator, its comp set is lifted from media businesses to IP and consumer products companies. This means that by the time the sponsor exits, the business is fundamentally changed and justifies a noticeably higher exit multiple.

In summary, the goal is to convert a personality-dependent, ad-revenue-dependent channel into a diversified, professionalized IP business and arbitrage the multiple expansion that comes with that re-rating. We analyze the effectiveness of this playbook in the following examples.

Case studies

Recurrent Ventures and Donut Media. In 2021 Recurrent Ventures acquired the independent digital media company Donut Media as part of a broader roll-up strategy. Donut Media’s popularity was largely due to its successful YouTube channel, through which the company had achieved a premium position in automotive entertainment. Donut represented an attractive investment as a vertical media asset, as it managed to combine engaging formats, sponsorship opportunities and high merchandise potential.

Furthermore, the company was particularly attractive from a financial standpoint due to the quality of its audience. Generally, automotive viewers are valuable to advertisers because they represent a clearly identifiable consumer segment. Moreover, compared to broader entertainment audiences, niche and loyal communities can attract higher sponsorship prices, as advertisers are often willing to pay more for brands with specific audiences, because they know more precisely their target population.

Therefore, the value creation proposition was based on introducing a more structured and efficient business model to increase monetization opportunities. By integrating Donut into a larger digital media platform, Recurrent could improve advertising sales, expand branded content by introducing merchandise and use shared infrastructure across its media portfolio. In fact, this creates operating leverage: with a stable audience, additional revenue streams can be layered onto the same brand without a proportional increase in costs.

However, Donut Media’s investment presents one of the central risks of the creator economy. The more attached audiences are to the specific culture of the brand, the higher the risk of lower engagement once standardized products and business image are introduced. In fact, professionalization can improve margins, but when it becomes too excessive it can damage the authenticity that made the asset valuable in the first place.

Electrify Video Partners and Veritasium. Later on, in 2023 Electrify Video Partners decided to invest in Veritasium for similar reasons. The brand’s popularity is largely attributable to its creator, Derek Muller, able to explain complex scientific, engineering and mathematical concepts through engaging videos on YouTube. The investment opportunity lied in the very characteristics of the segment where Veritasium is active: similarly to Donut Media, the channel operates in a niche with loyal and more stable audiences, and videos explaining physics, engineering or probability can benefit from a long-tail effect, as they continue generating views long after publication, making the content more durable and revenues potentially more predictable.

Therefore, the company’s attractive valuation came from the quality and durability of its cash flows. In addition, the brand’s positioning allowed it to have a high growth potential by introducing educational products, courses, books and partnerships with institutions or scientific companies. Electrify’s role was to build infrastructure around the creator by introducing sponsorships, partnerships and new monetization channels to increase revenue without changing the creative identity of the channel. This makes this specific investment closer to equity growth, as creator businesses are volatile, exposed to algorithm changes and highly dependent on individual talent.

However, this leads to the central risk of this very investment: Veritasium’s credibility was closely linked to Derek Muller’s expertise, communication style and reputation, so the sponsor had to adapt a strategy to maintain authenticity, while scaling the business and building a more institutional platform. As previously mentioned, Electrify was able to hedge this risk by allowing for a gradual shift from a founder-led channel into a broader science media brand.

Lunar X and Theorist Media. In 2022 the startup Lunar X acquired Theorist Media, a media company founded by Matthew and Stephanie Patrick, active on YouTube through channels such as Game Theory, Film Theory, Food Theory and GTLive. Its popularity was mainly due to its characterizing video format analyzing various topics, ranging from video games and films to food or internet trends, combining entertainment and knowledge.

From an investment perspective, the company was particularly attractive because it had already moved beyond the issue of a key-person dependency. Rather than a personal YouTube profile, Theorist Media had a replicable content format that could easily be applied across different topics, hosts and channels. Even before the takeover by Lunar X, the company was working with a more scalable model, leveraging its recognizable framework, rather than the owners’ popularity; its ability to operate as a standardized platform was proved when Matthew Patrick stepped back from hosting a few years later.

Overall, multichannel networks may represent more attractive assets because they provide a higher degree of revenue diversification and the possibility of introducing secondary hosts, while benefitting from shared operational infrastructure and a wider audience base. However, this model does not hedge all possible issues of creator-led businesses. For instance, succession risk remains a key concern. If viewers remain strongly attached to the main host’s figure, extending the same framework to other creators under the same brand might lead to a loss of authenticity perceived by audiences.

Candle Media and Moonbug. Lastly, Moonbug Entertainment represents an interesting case for a larger scale platform. In 2021, Blackstone [NYSE: BX] established Candle Media, an entertainment company led by Kevin Mayer and Tom Staggs aimed at acquiring and operating creator businesses. The same year, they announced the acquisition of Moonbug, the owner of some of the most well-known children’s brands, including CoComelon, Blippi, and Little Baby Bum. Moonbug extends beyond a popular YouTube channel: rather than an influencer business, it is more similar to a media IP company, whose content can be extended across various platforms, products and formats. From the same underlying IP, each brand can generate revenue through multiple channels, all increasing lifetime value per viewer. For instance, one of Moonbug’s most famous shows, CoComelon, is monetized through YouTube views, streaming platforms (such as Netflix), toy licensing, live events and music rights at the same time.

Therefore, the investment’s rationale was broader: Candle Media’s goal was to turn successful content into a larger entertainment franchise. In this process, YouTube itself is one of the most valuable growth levers. Views, comments and engagement help the company understand the most popular formats, songs and characters. This feedback can then be used to develop improved products and new licensing agreements to further scale up the business. In such way, YouTube functions as a distribution platform and a testing engine at the same time.

However, one of the main risks of these types of investments lies in the exit complexity. In fact, while IP assets can be extremely valuable, combining them into a unique platform does not always allow for synergies. Investors want to make sure that the overall company structure deserves a premium, rather than simply being a collection of individual brands. The holding company must prove value creation beyond what each asset would achieve individually. In fact, creators do not always represent the most valuable assets in the creator economy. Sometimes, the key source of interest can be the intellectual property owned by the brand, which makes it more scalable and less dependent on certain individuals, platforms or formats.

Financial analysis

The four main variables driving dispersion in creator business valuations map directly onto two structural risks the market is discounting: platform dependency and key-person risk. Platform dependency refers to the exposure of cash flows to the policy decisions of a third-party distribution platform (e.g. YouTube). Key-person risk refers to the degree to which revenue is contingent on a creator’s continued individual participation and output. Revenue growth and EBITDA margins are the entry-level financial screens. For example, a channel growing revenue at 20% annually with improving margins (e.g. sponsorship income scaling above fixed production costs) is a different asset from a business that has plateaued at YouTube ad income with no margin expansion path. Above these initial financial screens sit subscriber count and engagement quality: a highly engaged audience in a commercial niche, albeit smaller, will command better sponsorship and convert into merchandise purchases more reliably than a larger, general audience. As stated before, the inflection point for creator business valuations lies in revenue diversification and IP ownership. A business reliant on YouTube monetization and continued creator output is worth less than one with contracted distribution, IP-based revenue, and institutional management.

According to Quartermast Advisors, a boutique M&A firm that tracks creator economy transactions, creator businesses command valuation multiples ranging from 8.0x to 17.0x EBITDA, with a median enterprise value of 11.5x EBITDA. The wide range in which creator businesses trade reflects the market pricing of structural risks that conventional media assets do not carry with the same intensity. Within the 8.0x–17.0x EBITDA range, dispersion reflects the degree to which the creator business has escaped those risks.

The investment thesis for PE rests on multiple expansion, structured into three phases. At entry, a PE firm is buying a creator business as a media asset. Platform dependency remains high, and the business is heavily reliant on the creator’s continued output, given its non-diversified revenue stream. As is usually the case with private equity, value creation rests on operational efficiency: professional management and centralized finance and legal infrastructure allow the creator to stop being an operational bottleneck. PE also steps in to professionalize sponsorship sales, capturing higher advertisement revenue; merchandise and consumer products are either launched or scaled. All of these reduce the key-person risk associated with the initial acquisition, transforming the creator business from a pure media asset into a diversified business model. In April 2023, the global media business Electrify made a strategic investment in Veritasium, a leading science channel with over 20 million subscribers on YouTube. Following this investment, the founder of Veritasium, Derek Muller, reduced his working hours from 60 per week to 60 per month. Moreover, the team behind the channel tripled in size to 12 people, and the channel gained over 2 million subscribers. The Electrify/Veritasium case demonstrates the synergistic nature of PE investment in creator businesses, where the creator focuses on content and the investor on operations. Thanks to these operational changes and the transformation of the creator business, the PE firm can exit to a strategic buyer (a streaming platform, toy company, or media conglomerate) or through a secondary PE transaction at a higher multiple, reflecting a diversified consumer and IP platform rather than a single-creator asset.

Despite the PE tradition of highly leveraging its portfolio companies, classic LBOs are structurally ill-suited to most transactions in the creator economy. The reason for this is that creator cash flows are usually hard to predict, algorithm-sensitive, and reliant on an individual’s continued output. Applying huge amounts of leverage to these cash flows may amplify downside risk: a creator exit, a demonetization event, or even audience backlash may leave no room for recovery when coinciding with debt obligations. Hence, the more appropriate structure for creator transactions is either growth equity or a majority investment with founder rollover. This provides the capital for operational improvements that drive multiple expansion and avoid the high leverage that can lead to a solvency event. Electrify’s model of strategic investments that allow the creator to retain equity in the business is the best example of this structure achieving the intended outcome.

Risks and limitations

The same characteristics that make creator businesses attractive to private equity are also what make them structurally fragile. Although risks have been identified throughout this article in their relevant contexts, two warrant a closer look here because they are particular to creator-led media and have been illustrated by recent post-acquisition outcomes.

The first is key-person and talent-retention risk. The investor owns the brand, the IP, and the back catalogue. The audience, however, follows the people on camera, and in a creator business the two cannot be cleanly separated. The post-acquisition trajectory of Donut Media is the clearest available illustration. When Recurrent Ventures acquired the channel in November 2021, the entire on-camera roster was retained as part of the deal. Less than three years later, all three of the channel’s most prominent hosts had announced their departure. Jeremiah Burton and Zach Jobe left in June 2024 to launch a new channel called BigTime; James Pumphrey followed in August to start an independent channel called Speeed. Contemporaneous reporting attributed the exits to the broader cost-cutting and commercialisation pressures that followed Recurrent’s $300m financing arrangement with Blackstone and the deteriorating economics of the parent group’s e-commerce strategy. Donut still exists, and Recurrent still owns the IP, but a substantial share of the audience relationship has effectively migrated with the talent to new, independent channels that the sponsor has no claim on.

The second is reputational risk transmitted through brand extensions. The MrBeast Burger litigation illustrates this clearly. In 2023, MrBeast filed suit against Virtual Dining Concepts, the licensing partner that operated his ghost-kitchen burger venture, alleging that quality control failures had caused “material, irreparable harm” to his brand. The relevant point for investors is structural rather than legal: even where the creator is not operationally responsible for a venture, reputational damage flows back to the only name on the package, and the partner has no comparable brand of its own to absorb it. Brand extensions are a primary value-creation lever for sponsors of creator businesses, and they amplify upside, but they also concentrate downside on the very asset whose authenticity the deal was built around.

Conclusion

Creator businesses are increasingly becoming an investable asset class, attracting private equity firms aimed at exploiting the combination of loyal audiences, low capital intensity and significant monetization upside to transform channels into proper companies. Opportunities arise from expanding beyond platform revenue into sponsorships, consumer products, live events and broader IP monetization.

However, the same features that motivate such investments also represent the underlying risks of the industry. Once the businesses take off, the main challenge is to preserve the very keys to their own success: audience trust, transparency and identity are fundamental to maintain creators’ popularity, while excessive commercialization can quickly damage the brands’ credibility.

As a result, in a market where value creation depends on safeguarding the qualities that made these businesses valuable in the first place, the winners will be investors who can professionalize creator businesses without standardizing the audience experience and making viewers feel like the creator has simply become a product.

0 Comments