Introduction

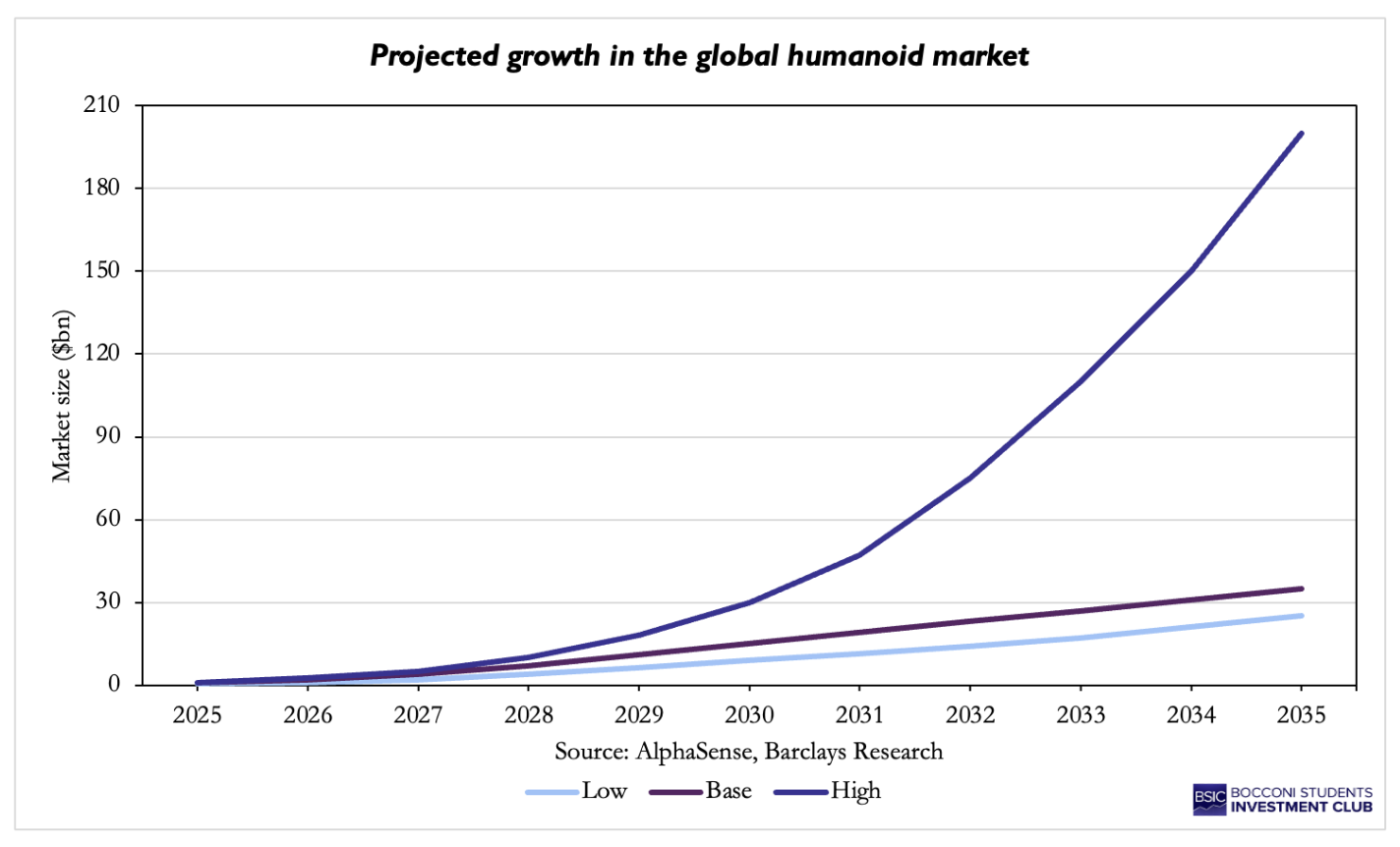

Global humanoid robot shipments totaled approximately 13,000 units in 2025 against $10.3bn in venture funding across over 450 individual rounds. This divergence defines the analytical challenge facing the current robotics cycle. Barclays projects the global humanoid market to reach $35bn under its base case by 2035, and $200bn under its high case; Morgan Stanley puts the 2050 market at $5tn. Physical Intelligence is valued at $11bn, with no disclosed revenue; Figure AI secured a $1bn Series C funding round in September 2025 at a valuation of $39bn, despite having shipped only 150 commercial units. Do these market projections justify the current private valuations of robotics companies?

Why Now? The Macro Thesis

There will be almost 13 million robots by 2030, reaching $57.7bn by 2035, as robots are no longer isolated machines, but part of production, logistics, and maintenance. 2026 shows a transition from hype to deployment, reaching a point of inflection, with investors calling it “Year One” of commercialization. Phyllis Wang, China industrials analyst at UBS Securities, focused on three accelerants for this shift: AI advancements, declining hardware costs, and new model launches. This shows a distinct difference from the first wave of AI, which was mainly focused on software, to one that is now equally focused on hardware.

Looking at one of the main factors that catalyzed the industry, as AI advances, robots’ perception, navigation, and control have improved as well, enabling them to perform a more diverse range of activities rather than just automation, rapidly evolving into the era of physical AI, where humanoids have developed “brains” – the ability to perceive and reason. AI-driven robotics are reshaping industries such as healthcare, manufacturing, defense, and consumer automation. To make a robot truly intelligent, several tech-supported capabilities are required: machine learning, which enables robots to use real-time data and information acquired through their experiences to solve new problems; natural language processing (NLP), a type of AI used to enable a robot to understand human language as it is spoken; and conversational AI or GenAI, which uses machine learning and NLP to take the interaction between a robot and a human to the next level. Manufacturing powerhouses like China and South Korea have expanded the use of robots alongside human labor, improving quality, enhancing worker safety, and increasing productivity. Companies like Physical Intelligence are working to make it easier for robots to learn from inputs and generalize behaviors with less data, using software that allows machines to operate across environments rather than being coded for narrow tasks. Strategic partnerships between tech companies are expected to increase, as vendors increasingly collaborate rather than build everything in-house to remain competitive. One example is Nvidia’s Isaac platform, used by multiple firms to implement AI-based robotics.

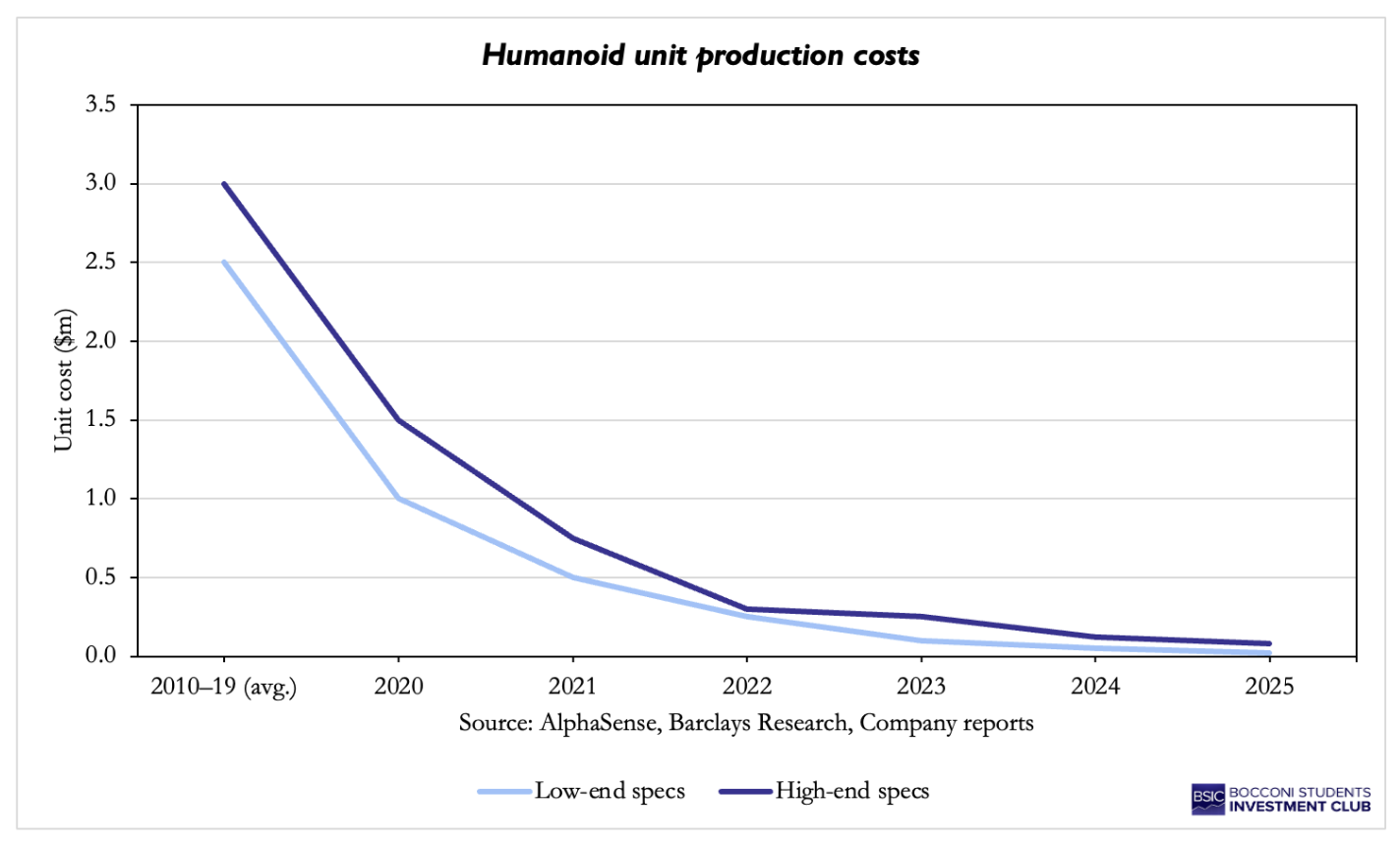

The humanoid supply chain is based on three technologies: brains, as mentioned above; brawn, the system that enables robots to replicate human movements; and batteries, which power humanoids. The improvements in these three technologies have massively reduced the production costs of humanoids, from $3m per unit to $100,000 over the last decade, making them a more realistic option for commercial applications. A key component of AI hardware is batteries. As the market grows, so does demand for copper, lithium, aluminum, and nickel, which are used in battery production. China holds a supply chain advantage, providing over 90% of the magnetic rare earth needed for actuators and monopolizing the supply of minerals. However, global energy storage capacity has increased over the years, and lithium-ion battery prices have dropped, making the integration of batteries into humanoids more practical.

Considering Unitree, a global robot production company, its latest low-cost launch was priced at around $5,700, down from $90,000 for early models in 2023, as it has started mass production and cost curves have kicked in. Given its location in China, Unitree’s pricing strategy is also due to its geographical location; China has two sprawling metropolitan areas that are home to a hive of hardware suppliers, sometimes even allowing replacement parts to be delivered in less than a day for manufacturing. This trajectory mirrors the cost curves seen in the solar panel and electric vehicle markets. In the market for solar panels, costs fell by around 90% due to economies of scale and learning curves, with China dominating because of vertical integration and supply chain density. In the electric vehicle industry, costs fell due to gigafactories, with China again leading due to supply ecosystems. Costs fell as cumulative production rose; solar panels followed it, batteries followed it, so it is no surprise that the robotics industry is following the same law.

The demand side of the industry is affected by labor shortages, driven by aging populations, the concentration of talent in cities, and the reluctance to perform repetitive tasks. China is facing a 30 million worker shortage, and it is projected that by 2050, the share of the global population aged 65 and above will rise to 16%, surpassing 30% in some regions. Bipedal robots can complement human workforces to operate effectively. Labor shortages, which mostly occur in the agricultural, manufacturing, and healthcare industries where demand outstrips supply, mean robotics is no longer seen as a luxury but as a necessity. Companies can treat automation as an operating expense rather than a capital expenditure, thereby lowering overall costs while maintaining production. Thanks to advancements in robotics and brain technology, robots can help fill some labor gaps, working safely alongside humans.

Morgan Stanley estimates a $5tn market by 2050, and Goldman Sachs a $38bn market by 2035. Investment interest in AI-powered robotics is surging, with investors seeking to back robotics start-ups that promise versatile capabilities and develop multi-purpose robots. Have we seen this excitement before? Is this just another financial bubble? China’s National Development and Reform Commission has warned that a bubble is forming in robotics, with too many startups making robots that are too similar to one another, with no promising breakthroughs, and crowding out funding for research. This increase in capital funding isn’t followed by real-world deployments growth, with certain shipments rising little by little. This difference is driving speculation about the market. Startups should focus more on deploying robots at scale in real-world settings, testing them in offices or factories, rather than on impressive prototypes. Whether this is a bubble cannot be answered yet, as we are aware that we need AI for future development. Startups should aim for early revenue streams and partnerships with a clear monetization model as soon as possible.

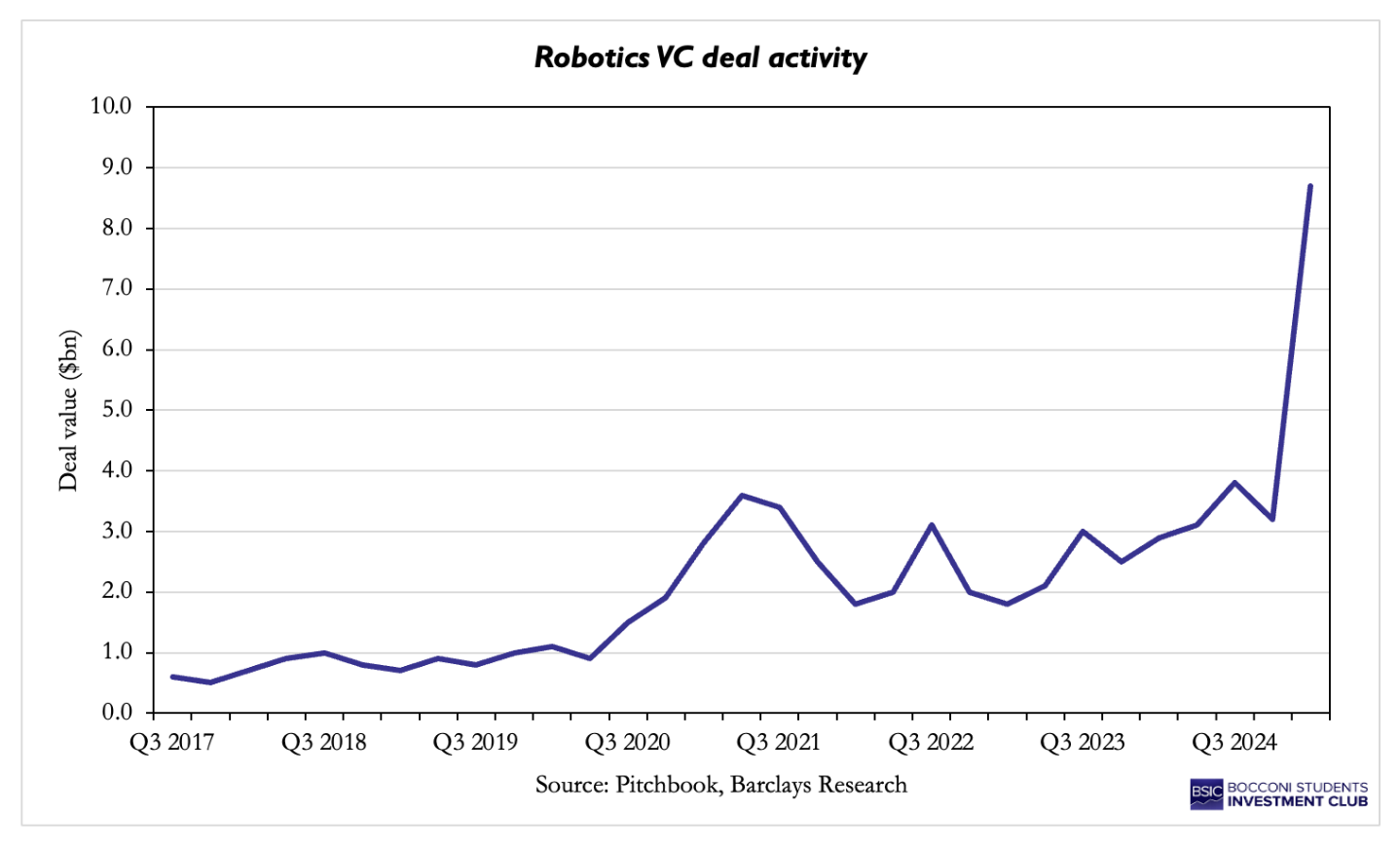

Private Capital: The Mega-Round Era

With major AI-focused tech companies releasing ever-impressive models every quarter, the world is beginning to look more like a futuristic sci-fi movie, with flying cars and robots living among humans. Throughout the history of robotics, machines have been programmed to do specific tasks and perform well in controlled and predictable environments but struggle with unstructured or complex environments. This problem is being solved by many private startups, already commanding significant valuations despite being pre-revenue, and many regulatory hurdles the industry must navigate before large-scale commercial sales will be possible.

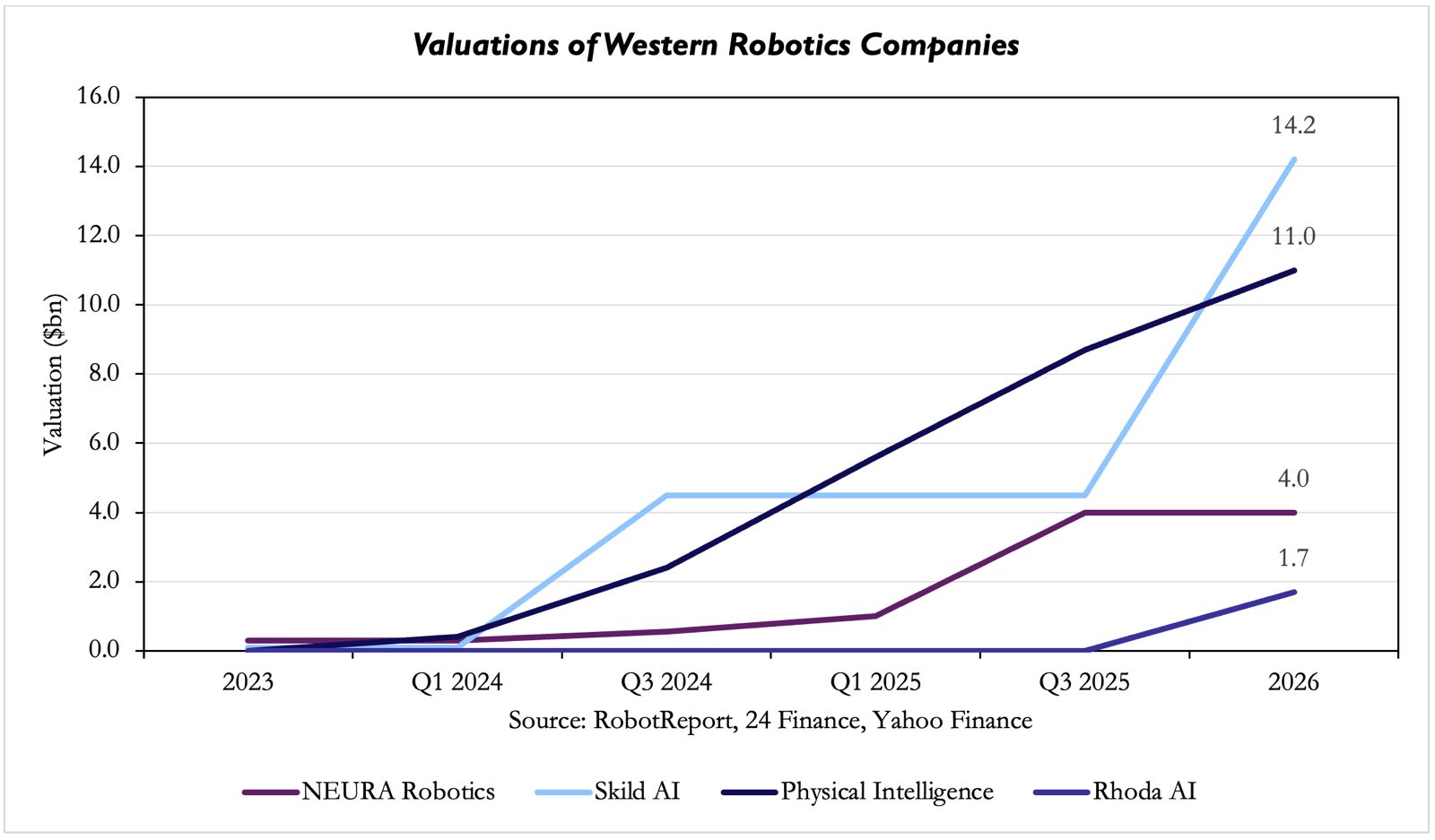

Rhoda AI recently raised $450m Series A funding, valuing the startup at around $1.7bn, despite being pre-revenue. Rhoda trains its AI model on over a million videos, which teach the robot motion, physics, and everyday movements that help it interpret and react to its physical environment. After this general pre-training, the robot is given additional instructions and videos to teach it to perform specific tasks. The goal is to deploy robotic systems that can navigate and adapt to fast-paced commercial and industrial settings in real-world environments. Rhoda has demonstrated controlled-environment tests, showcased its dynamic robotics, and clearly outperformed existing factory robotics.

Another startup in the space, Physical Intelligence, raised around $400m in late 2024, an additional $600m in Series B in November 2025, and is currently valued at around $11bn, with reports of another $1bn funding round. Physical Intelligence aims to build general-use AI models, named Π0 (pi zero), which offer a general-use platform for robots to operate on, rather than training each robot for specific tasks. This will offer more adaptable functionality, potentially making robotic assistants economically viable for common households. Through its series of fundraising rounds, the 2023 startup has been backed by Amazon’s Jeff Bezos, OpenAI, Alphabet [NASDAQ: GOOG], and other leading industry players, indicating significant interest from these players. There are rumors of an additional fundraising round that would value the company at almost $11bn as of April 2026.

Backed by major venture capital firm Sequoia, Phillipe Laffont’s Coatue, Amazon [NASDAQ: AMZN], and Bezos Expeditions, Skild AI has raised about $2.2bn over four total funding rounds, valuing the company at over $14.3bn. Skild AI emphasizes that robotics should not be limited to singular tasks or physical capabilities, given that AI models can solve complex, multi-step problems. Based out of Pittsburgh, Pennsylvania, far from the typical Silicon Valley startup scene, Skild AI uses Nvidia’s Omniverse libraries and chips to build a robotic brain that requires little to no post-training. Unlike many of their competitors, Skild AI has been able to demonstrate its robots adapting to real-world environments outside controlled settings, completing tasks such as hiking through the forest, cleaning dishes, and navigating warehouses with scattered debris. This showcases significant steps towards practical use cases for everyday consumers.

NEURA, a German-based robotics company, raised €120m in Series B funding in early 2025, which it says validates that European tech companies can compete with robotics against the US and China in the global sector. As of March 2026, NEURA closed a €1bn new funding round, with backing from Tether, valuing the company at close to €4bn. NEURA aims to compete in a similar industry with many AI-robotics startups attempting to modernize the hardware-software interaction and build functional, multi-use robot assistants. The firm showcases many robot demonstrations, from domestic cleaning to factory and assembly-line integration.

The IPO Wave

Recently, China has emerged as the dominant player in robotics hardware and deployment. While there are still limited results for truly independent, general-use robots, China dominates use-case robotics, from factory production to automated food production and drone delivery. Unitree, a major Chinese powerhouse, was valued at ¥7bn in a mid-2025 fundraising round; however, it is now rumored to be targeting a ¥50bn, roughly $12bn, IPO in Q4 of 2026. In 2025, Unitree posted ¥1.7bn in revenue and around ¥600m in net profit, with gross margins expanding to nearly 60%, a truly outstanding feat for a growth tech company that usually burns through cash. In 2025, humanoid robots surpassed quadruped robots for the first time, marking a leap forward in functionality. Unitree sold around 5,500 humanoids in 2025 and over 30,000 quadruped robots in 2024, a scale unmatched by any competitor. These robots are all priced between $1,600 for smaller, quadruped models and $90,000 for larger industrial-use machines.

Robotics is seen as a critical industry in China, important for maintaining its competitive cost advantage in manufacturing and mitigating risks arising from reduced production volume due to an aging population and high unemployment. Unitree’s IPO listing would be a big win for China’s financial markets, helping bring them back to life after years of volatility and trade tensions with the United States. Tech giants Alibaba, Geely Holding Group (owner of Smart, Volvo, Lotus, Renault Korea, and more), BYD, and Tencent participated in Unitree’s recent fundraising rounds, partnering to push Chinese tech innovation as Beijing strives for greater tech independence. Unitree aims to expand internationally to help build a stronger reputation and build diversified revenue streams before an eventual IPO. This also helps mitigate one of their biggest risks: significant revenue comes from research institutions and universities, making their products extremely reliant on a single industry. Additionally, international expansion remains constrained by trade-war tensions between the United States and China, with heavy US import tariffs significantly raising the prices of Unitree robots. With President Trump and Chinese President Xi Jinping set to meet soon, a deal would help Unitree significantly as it looks to further its international expansion.

Another Chinese firm, Galbot, recently raised ¥2.5bn (around $362m) with backing from Sinopec, CITIC Group, Bank of China, and the National AI Industry Investment Fund. This significant backing from state-owned entities demonstrates a clear priority in Beijing for China to be a leader in robotics and AI. In March of 2026, it was reported that Galbot underwent a shareholder restructuring, becoming a joint stock company, a critical step prior to a public listing. In 2025, Bloomberg reported that Galbot had selected UBS, Huatai Securities, and Citic Securities to help with share sales and potential listing applications in Hong Kong. These events both point to a potential IPO for Galbot in the future.

SoftBank recently announced they are creating a vehicle, which they plan to take public at a $100bn valuation, called Roze. This combines SoftBank’s existing assets, such as energy, land, and infrastructure, with ABB Robotics, a robotics company they acquired in 2025. This venture aims to create synergies across companies by building data centers and other critical AI infrastructure. By utilizing ABB’s robotics, SoftBank is targeting data center construction automation, significantly reducing the cost and human relocation hurdles data center projects often require. SoftBank is targeting a 2026 IPO; it is likely this could be pushed to early 2027.

M&A: Incumbents Respond

While many current big tech players are heavily investing in AI startups to accelerate industry growth, they are also responding by bringing some development in-house or through long-term partnerships. In March 2026, Amazon acquired Rivr, a Swiss robotics company that specializes in stair-climbing delivery bots, for an undisclosed amount. Rivr spun out of ETH Zurich’s robotics lab in 2023, and Bezos’ family office has been a seed investor in the firm since 2024. Bringing Rivr in-house will help Amazon streamline its last-mile delivery, the most logistically difficult and expensive part of the delivery process. Prior to its acquisition, Rivr was valued at $100m. Amazon has spent years automating parts of its operations. Amazon Robotics was created after Amazon acquired Kiva Systems, a warehouse robotics manufacturer, in 2012 for $775m, and has been dedicated to automating Amazon factories. Amazon has been a significant investor in many robotics and automation companies, and in March, the Wall Street Journal reported that Bezos has been discussing organizing a fund purely to acquire manufacturing companies in different tech sectors, including chipmaking and AI, to help speed up Amazon’s automation.

Boston Dynamics has partnered with Google, utilizing the Gemini Robotics AI model to help their robot dog, Spot, accurately read and analyze complex instruments. This will allow Boston Dynamics’ robots to analyze complex situations in factories and data centers, such as reading gauges or conducting visual inspections, automate factory jobs, and increase safety for many factory workers. In the future, this technology can be implemented into many dangerous tasks such as mining, firefighting, law enforcement, and numerous other jobs.

In early April, Tesla [NASDAQ: TSLA] closed production on the Model X and Model S to make way for its robotaxi line. CEO Elon Musk called it the “end of an era” for Tesla, with the company going all in on full self-driving (FSD) technology across its consumer fleet, new Cybercab robotaxi, and eventual semi-truck rollout. Cybercab production has begun at Giga Texas, while the California plant has been retooled for Optimus, Tesla’s autonomous humanoid robot. In Tesla’s Q4 earnings call, Musk shared a target of producing one million Optimus units, a figure that would dwarf the entire humanoid robot industry’s current output. Earlier this year, Musk’s xAI and SpaceX merged and filed for an IPO targeting a $1.75tn valuation. The synergies across Musk’s empire are becoming increasingly apparent: Tesla is building autonomous humanoids and robotaxis, xAI is competing at the frontier of large language models, and SpaceX is developing the infrastructure for off-planet deployment, including space mining and data centers, which Musk has talked about as the future of SpaceX. With the SpaceX IPO targeting a 2026 listing, autonomous robots capable of performing tasks too dangerous for humans, aboard spacecraft, on Starlink maintenance missions, or in deep-space environments, may not be far behind.

In February 2026, Cadence Design Systems acquired Hexagon’s Design & Engineering division for approximately $3.2bn, a move that embeds precision simulation and industrial software directly into Cadence’s electronic design automation suite, demonstrating a clear bet that the hardware-software co-design layer will be critical as robotic systems grow more complex. In April 2026, Skild AI acquired Zebra Technologies’ robotics division, a deal that hands the $14bn startup an immediate commercial footprint across warehouse and logistics automation. Rather than building customer relationships from scratch, Skild inherits Zebra’s installed base across distribution centers worldwide, dramatically accelerating its path to revenue. As Alan Wang of Freshfields noted, “the bigger, more traditional robotics and industrial automation groups will likely look to acquire some of the more innovative startups as the industry consolidates on the back of the AI boom.” Big tech incumbents acquiring AI-native robotics startups now may be doing exactly what legacy automakers wished they had done with EV software a decade earlier, illustrating an industry facing heightened competition amidst consolidation.

China v. the West: Two Models for an Industry

The field of AI and robotics is quite concentrated geographically; China accounted for 54% of global industrial robot installations in 2024, and Barclays estimated an 85% share of humanoid robot installations in 2025. This scale is also reflected in China’s automation culture, reaching 470 robots per 10,000 manufacturing employees in 2023. While the US and Japan remain in close competition and serve as important innovation hubs, Europe is finding its own edge to specialize in: advancing the physical capabilities that make up the robot’s brawn.

Morgan Stanley’s Head of Industrials Research states that China has the most national support for AI innovation among nations, a major factor driving ongoing capital formation. Since 2014, President Xi Jinping has called for top-level prioritization of robotics development. Robotics was one of the ten technologies identified as a priority under the “Made in China” 2025 initiative, which led to several targets for the robotics industry development in 2025, such as: achieve 20% annual growth in industry revenue, reach a total stock of 1.8 million industrial robots, and double the density of robots in the manufacturing sector. As Beijing launches its new five-year plan in 2026, robotics is even further supported, with China’s leaders being prepared to “invest massively” in the industry. On the supply side, the government has offered over $20bn in subsidies to the robotics industry, through loans, tax credits, and state-backed venture capital funding. On the demand side, China has a significant advantage in local suppliers; numerous policies and programs reduce the cost of purchasing materials from manufacturers, thereby expanding revenue streams for domestic robotics manufacturers.

According to Morgan Stanley research, building a humanoid robot using Chinese suppliers costs one-third as much as using Western suppliers. China’s Ministry of Industry and Information Technology (MIIT) stated that the output of industrial robots increased by 33.2% YoY in Q1 of 2026, following 610 investment deals valued at $7.9bn by the end of 2025, with 140 humanoid robots OEMs and over 330 products launched in one year. Alibaba Group Holding Ltd. is preparing to break into the market with the first four-legged robot. It joins the industry leaders Unitree and AgiBot, the highest-profile companies, aiming to outdo Tesla Inc. and other rivals in the US. Alibaba’s entry into the market signals that the next wave of AI monetization will be physical automation. The market is already crowded, so the next steps for the Chinese market are consolidation, specialization, or exiting. What makes China particularly difficult to compete with is the ecosystems created. All manufacturing processes, from motors and sensors to batteries, are localized within the same country, and sometimes the same region. Companies iterate much faster than competitors, and their push to enter international markets has made China the default supplier of AI hardware.

While China focuses on the hardware part of AI, the US focuses on the software layer. With global companies such as Tesla, Figure AI, and Physical Intelligence, the market is rapidly expanding and estimated to reach over $83bn in 2026. Some of the drivers of this market include strong investments by US hyperscalers in cloud AI infrastructure, advanced computing, and high-performance AI chips. Cloud-based AI platforms and Generative AI are driving the highest revenue growth. There have been some steps toward making physical AI more specialized: Tesla’s Optimus is a general-purpose robotic humanoid developed by Tesla, with the goal of producing up to 1 million humanoid robots annually by the end of 2026. Figure AI is partnering with BMW and UPS to position itself in the industrial-use market. Companies such as Amazon and Toyota are already using the Digit robot from Agility Robotics, increasing warehouse automation for both. Leading companies have specialized in the Intelligence component that drives robots; however, as noted above, market statistics indicate that the robotics industry is expected to reach all-time highs and continue to grow.

Here is where the US loses, due to its dependence on hardware. There are very few US-based alternatives for humanoid components, and every robot developer must purchase components from China; even Tesla has built a China-focused sourcing team to access its specialized components. Figure AI relied massively on Chinese manufacturers for joints, sensors, and motors for early prototypes. Leading companies such as Nvidia and Google were supplied by Unitree for a research project. This gap between the US having the “brains” and China having the “body” reflects the history of government-driven policies. Having factories with high-performance electromechanical components and deep expertise to efficiently use them takes years. China has had policies pushing for a dive into robotics for as long as 10 years, granting it these significant scale advantages. Looking at US policies, with tariffs as high as 145% on Chinese goods, the US is at a disadvantage, widening the gap. While it could be argued that, in the long term, this would increase domestic manufacturing, it would require massive investments, even leveraging partners in other regions, such as Japan or Europe. Even so, this would take years to achieve, and even then, China might remain in the lead.

Europe holds 32% market share, with general manufacturing in Germany, France, and Italy, which together account for 70% of EU robot installations. Investment grew by almost 230% from 2019 to 2024, and the market is expected to exceed $100bn by 2030. Through a portfolio of over 120 research projects, the European Commission has built a solid knowledge base and cooperation across the robotics stakeholder community, including a public-private partnership on robotics called SPARC. While regulations seem to be pushing for the innovation of robotics, Europe is still falling behind China and the US.

Germany, a leader in industrial automation, is expanding into humanoid robotics with companies like NEURA Robotics. Sweden’s Hexagon AB is emerging as well, developing a humanoid robot that is being tested at BMW’s Leipzig plant. Recently, President and CEO Anders Svensson announced financial targets for 2026-2039: average annual organic growth of 4-6%, an EBITDA margin of 24-26%, and an annual cash conversion of 90-100%. The company has reached €3.7bn in revenue and employs 17,000 people. France and Spain are following Germany, seeking to expand into humanoid robotics with companies such as PAL Robotics and Aldebaran.

However, Europe’s industrial robotics factories remain the backbone of automation. The legacy industrial players, such as KUKA and ABB Robotics, dominate the production of automation systems. Still, Europe is at a structural disadvantage, with capital constraints and slow innovation of AI. Europe needs a strategic plan to carve out a more distinct edge and gain market share, such as in sectors that are less robotized and face productivity or labor shortages. The continent’s biggest weakness lies in its market fragmentation; it needs to promote investment and the construction of regional champions to play a prominent role in the race for AI leadership. KUKA CEO Christoph Schell even said that too many European industrial companies are integrating AI too slowly, with factories having systems that either fail or aren’t as efficient as those in other countries. This lack of integration makes it harder to fully deploy robots, which is what’s making it fall behind. Additionally, two of the most successful industrial robot manufacturers, KUKA and ABB, have been acquired by foreign entities, specifically Asian acquirers. KUKA was acquired by China’s Midea in 2016, while ABB is set to pass into SoftBank’s hands in 2025. This shows that while Europe excels at building technology, it lacks the scale of capital required to compete with China and the US. China is focused on hardware, the US on software, and Europe falls in the middle. Without government support through expansionary policies, such as increasing the seven-year horizon budget for 2028-2034 by at least 5% and investing in the robotics industry and AI, Europe will always be behind the main players.

Geopolitical Considerations

On March 26, Senators Tom Cotton and Chuck Schumer introduced the American Security Robotics Act, which bans federal agencies from purchasing and operating ground-based robotic systems manufactured by companies with ties to China, Russia, Iran, or North Korea. The legislative architecture behind this Act is recognizable: Congress imposed equivalent restrictions on Chinese-made drones, and, in December 2025, the Department of Defense was encouraged to designate Unitree as a “Chinese military company”. For now, the Act covers only government procurement, but the relevant question for investors is the trajectory of the Act. Historically, restrictions on federal technology procurement have extended to state governments and defense contractors, eventually making their way into broad commercial enterprise.

That same week, a revealing investigation by the Wall Street Journal highlighted the structural irony created by the American Security Robotics Act. The investigation revealed that America’s most prominent humanoid programs rely heavily on Chinese-manufactured components: Figure AI used Chinese suppliers for joints and motors in early production models; Unitree’s motors appear in robotic research systems built by Nvidia and Google. Bank of America estimates that over 50% of a humanoid robot’s material cost is attributable to drives, which are primarily manufactured in China. Research by Morgan Stanley has estimated the cost differential at $46,000 per unit with Chinese supply, compared with $130,000 without it.

China’s April 4 export restrictions on seven rare earth materials and associated magnets target a specific chokepoint in the robotics supply chain. For example, neodymium-iron-boron magnets—which are embedded in every actuator joint across a machine—are almost exclusively produced in China and have no near-term substitute. Elon Musk has flagged this exposure to Tesla investors, citing potential delays to Optimus’ production scale-up. Furthermore, the 145% US tariff on Chinese goods compounds the problem from another angle: it prices Chinese humanoids out of the US commercial market and raises production costs for US manufacturers reliant on Chinese components. Unitree’s G1 model would rise from around $16,000 per unit to $40,000 for a US buyer.

This new geopolitical layer introduces risks that robotics valuation models have not yet priced. Chinese companies now face increased market access risk. Investors evaluating the upcoming IPOs of Chinese robotics companies must now size the addressable markets across a range of geopolitical scenarios. American companies face supply chain cost inflation and production timeline setbacks, and onshoring the actuator supply chain is a capital-intensive challenge that would take years to complete. Although European companies are less exposed to US-China trade frictions, they are still integrated into the same Chinese supply chains as their US peers.

Conclusion

The structural case for humanoid robotics and the robotics industry is not in dispute. Unit production costs have fallen 30x over the past decade, and labor demographics across every major economy have created structural demand. However, the dispute is whether $11bn for a pre-revenue company and $39bn for a company that has shipped only 150 commercial units are justified. Or are we in a robotics bubble?

Furthermore, geopolitical developments have introduced a variable that valuation models in this sector have not yet accounted for. Chinese and US robotics positions now carry different risk types, not merely different return profiles. Chinese companies face market access issues, and US companies face supply chain cost inflation and production delays. European companies face both without the capital base to absorb either. This does not invalidate the investment thesis for robotics but requires investors to be explicit about which component of the thesis they are underwriting.

0 Comments