History

Unilever’s [LON: ULVR] corporate structure has historically been defined by the coexistence of food and personal care businesses, which originated from the 1929 merger between Margarine Unie and Lever Brothers. The rationale for this consolidation at that time was largely based on scale and distribution synergies, but also geographic diversification, and resulted in a consumer goods conglomerate with the capacity to span both staple consumption and discretionary categories across global markets. For the majority of the 20th century, this model proved structurally sound and remained robust. Through high penetration in developed markets and expanding demand in emerging economies, the food division, built around known brands such as Knorr, Hellmann’s and Lipton, delivered consistent and high-quality cash flows. At the same time, the personal care and home (“HPC”) segment provided organic growth, underpinned by strong brand pricing power and continuous product innovations. Furthermore, the crucial ability to allocate capital dynamically across divisions allowed Unilever to smooth cyclicality by deploying resources toward whichever segment offered the most attractive short-term returns while the other provided ballast. This resulted in a relatively stable return on invested capital profile across economic cycles, precisely the structural argument for maintaining the conglomerate model in the first place.

However, over the past decade, the underlying economics of these segments have diverged materially: personal care and beauty have benefited from a trend towards premium products, including higher gross margins and stronger pricing power, substantially driven by brand equity and consumer willingness to trade up. On the other side, the food segment has been confronted with structurally lower growth, amplified by greater private label competition and further margin pressure from input cost volatility. As a result, bundling these businesses together made it increasingly difficult for investors to see and price the superior quality of the personal care business, which subsequently contributed to Unilever trading at a persistent valuation discount relative to more focused competitors.

Why is Unilever doing this? The Debate over Foods

Unilever’s decision to divest its food business is not due to a sudden strategic pivot, but rather the culmination of a long-term debate within the firm that has been ongoing for years.

A key driver in this decision has been the role of activist investor Nelson Peltz. Peltz, who joined the company’s board in 2022, has spent years advocating for a break-up of the soap-to-sauces conglomerate. His investment fund, Trian, held a 1% stake in the business and argued that the food business was compressing the group’s growth profile and valuation.

From a growth perspective, Unilever’s Beauty & Wellbeing and Personal Care divisions grew by 4.3% and 4.7% respectively in 2025, versus just 2.5% for Foods. This disparity is also evident over a longer period, with Unilever’s HPC sales growing at a rate of 5.3% CAGR compared to Food’s 2.5% CAGR in the last five years.

From a valuation standpoint, pure-play HPC-focused companies tend to command higher earnings multiples than food businesses. Unilever’s comparable HPC companies, P&G [NYSE: PG], Colgate [NYSE: CL], and L’Oréal [EPA: OR], trade at 19.4x, 21.0x, and 27.0x earnings, respectively, while, by contrast, the company’s peer food companies, Nestlé [SWX: NESN] and Kraft Heinz [NASDAQ: KHC], trade at lower multiples of 17.5x and 10.7x earnings. If Unilever is viewed less as a mixed consumer goods conglomerate and more as a pure-play HPC-focused company, the group could trade more in line with the higher-rated peer group, unlocking a higher valuation.

Attempts to reposition through acquisitions, with the most notable example being the failed £50bn bid for GSK [LON: GSK] Consumer Health in 2022, proved that investors’ view of Unilever’s future was clear. The negative reaction to that bid reinforced the view that value creation would more likely come from focus and simplification, rather than expansion. Since the mid-2010s, Unilever has gradually reduced its exposure to food. In 2018, the firm sold its global spreads business to KKR for ~€6.8bn, a way to sharpen and focus its portfolio on key areas of growth. Just three years later, in 2021, it sold its global tea business, which had been deemed non-core, to CVC Capital Partners for €4.5bn. Most recently, in 2024, Unilever announced its decision to separate its ice cream business by spinning it out as an independently listed entity called The Magnum Ice Cream Company [AMS: MICC]. All three of these transactions highlight Unilever’s strategic attempt to reduce its dependence on slow-growth Food businesses and become a more focused HPC company. The appointment of Fernando Fernandez as CEO in 2025 brought new urgency to the process. His strategic priorities have been explicit from the outset: sharpen the portfolio around higher growth categories. The seriousness of his intent can be seen in the talks he held with Kraft Heinz in early 2026 regarding a potential merger, including parts of Unilever’s food business. While the discussions didn’t end up leading to a transaction, they set the seeds for Unilever’s eventual deal with McCormick [NYSE: MKC].

Headline Overview: Price, Financing

In March 2026, Unilever agreed to separate and combine its food business with McCormick through a Reverse Morris Trust (“RMT”), enabling a tax-efficient divestment while transferring control of the asset to a strategic acquirer. The transaction implies an enterprise value of around $44.8bn, consisting of a split between $15.7bn in cash and roughly $29.1bn in McCormick equity. Upon completion, Unilever shareholders will own around 65% of the combined entity while existing McCormick shareholders retain 35%. The scope of the transaction therefore deserves close attention. Notably, Unilever’s food business in India is excluded, which is primarily due to its ownership by the separately listed Hindustan Unilever Limited [NSE: HINDUNILVR]. This detail deserves closer attention: India represents one of Unilever’s strongest and fastest-growing food markets, so the headline valuation applies to a reduced asset base, complicating direct comparisons with peers and prior transactions. At first glance, the implied valuation reflects only a modest premium to sector multiples, despite the significant brand strength of assets such as Knorr and Hellmann’s. While the muted premium could be read as a sign of limited competitive tension, or simply a consequence of the constraints the RMT structure imposes on deal pricing, the picture is not quite that clean. Unilever had held earlier discussions with Kraft Heinz over a potential food combination, which suggests that there was a competitive dynamic in the process. The premium more likely reflects a combination of structural limitations of the deal format and investor caution toward the growth profile of the food segment. From a financing perspective, McCormick is expected to fund the cash component through new debt. This results in a pro forma leverage of approximately 4.0x EBITDA, representing a significant increase relative to historical levels and further implying an extended period of debt paydown following completion.

Reverse Morris Trust: Tax-Free Asset Disposals

A Reverse Morris Trust is a structure that emerged from a 1966 precedent that allowed a US company to spin out one of its subsidiaries tax-free. In the original version, called the Morris Trust, the parent company would split its wanted business into a NewCo, transfer shares of that NewCo to its current shareholders, and then merge the remaining unwanted business held by the parent with an acquirer, effectively splitting the two businesses. Due to the tax-free treatment of reorganisations and restructurings by the US tax code, for a long time, this sequence of transactions was not deemed a divestiture and remained tax-free. After the structure started being abused by corporations all around America, the regulators cracked down and established a set of limitations, restricting the free use of the Morris Trust. That is how the Reverse Morris Trust was born in the 1990s. The key idea is still the same – using a restructuring-like series of transactions to allow a company to dispose of its unwanted business segment without triggering corporate taxes. As the name suggests, the new structure resembles a reverse version of the original one. First, the parent establishes an empty subsidiary, often called a SpinCo, and transfers the asset it wants to dispose of into that subsidiary. Next, the parent distributes shares of the SpinCo to its shareholders, after which the parent no longer owns the business – shareholders do. Then, the SpinCo merges with the acquiring company, which might be quite counterintuitive, as it is in fact the acquirer that is the surviving entity. After the merger, if the SpinCo shareholders maintain a more than 50% ownership stake in the new entity, the transaction is considered a continuation of ownership instead of a sale and therefore does not trigger corporate tax. At the same time, the parent has economically exited the business. An important caveat, and risk of RMTs, is that for the tax-free effect to remain, the inevitable disposal of shares by shareholders must not be considered a “part of the plan” to sell, which means that it takes between one and two years for shareholders of the parent to fully liquidate their exposure to the newly formed entity.

How does the RMT Apply to the Unilever Deal?

In the case of Unilever, the food business, with the exclusion of the India subsidiary, will be placed in a newly established SpinCo. Unilever will receive $15.7bn in cash from McCormick upfront to cover transaction costs and a 9.9% stake in the combined entity. Unilever’s shareholders will hold another 55.1%, bringing the total to 65%, well above the 50% threshold. As mentioned in the theoretical walk-through, McCormick is a listed company, and therefore, it will be the surviving entity after it merges with SpinCo. After the RMT is completed, Unilever will end up free of the food business, except the 9.9% stake it intends to sell over the next twelve months as per its latest press release. Importantly, the tax-free nature of the transaction is confined to the US jurisdiction, and due to the dual listing of Unilever in the UK and the USA, as well as the international nature of the business, some leakage is unavoidable, and the RMT will effectively be a tax-reduction strategy rather than a full-fledged zero tax guarantee.

Implications for Unilever

In principle, the transaction is a materialisation of the long-term calls of both company leadership and shareholders, including activists like Nelson Peltz. From a strategic perspective, the deal will be a value unlock, making Unilever the world’s leading pure-play home and personal care business instead of a complex and diversified conglomerate. The pro forma portfolio of Unilever’s beauty, personal care, and home care products delivered a CAGR of 5.4%, superior to that of the food business. With more structural tailwinds such as science-led innovation and premiumisation, the remaining divisions present a more attractive growth profile, with improved exposure to digital commerce, a rapidly expanding channel. This should allow for better capital allocation opportunities and ultimately, a better ROIC for the company.

On the cost side, the company expects around $500m of stranded costs related to the transaction over the next 2-3 years, which seems minuscule compared to the potential long-term benefits. In the long run, a re-focused and narrower portfolio will allow for more targeted R&D and better cost-structure management, which the company views as a mid-to-long-term margin expansion opportunity. While the growth story improves, the risk profile shifts too. The other side of the coin is that after the transaction, 62% of revenue will be coming from emerging markets, which grow faster, but are also more volatile and riskier. That, of course, creates more exposure to downturns and macroeconomic shocks. Furthermore, the 9.9% stake in the new McCormick that Unilever will retain on the corporate level, and the 55.1% its shareholders will hold, creates a significant exposure to a business with large integration risks that will be 4.0x levered coming out of the transaction. On top of that, McCormick shares are denominated in US dollars, introducing FX risk in what is already a volatile macroeconomic and political environment. Exposure to McCormick’s equity is likely the largest point of contention in evaluating this transaction and comes with the greatest uncertainty, as the true realised value for Unilever’s shareholders heavily depends on the performance of McCormick in the years following the transaction.

In the short run, Unilever will benefit from the almost $16bn cash infusion, which is expected to cover all transaction-related costs and fund $6bn share buyback as well as debt paydown to reach a 2.0x leverage ratio as indicated by management. From a strategic point of view, this is a very attractive structure for Unilever as it repositions the business while also unlocking cash, allowing it to delever, and limiting taxes. The continued exposure to the spun-out business and uncertainty about the valuation at which it is being sold are important downsides that prevent an unanimously positive evaluation of the transaction from the perspective of Unilever’s shareholders. In essence, while certainly good from a business strategy perspective, the deal leaves a lot to be desired from a financial engineering point of view.

Implications for McCormick

Considering the transaction from McCormick’s angle, the case is truly transformational, whereby the coin has, as per usual, two sides. The company is acquiring meaningful scale, a significantly broader geographic footprint, and on top of everything, two of the most globally recognised food brands in Knorr and Hellmann’s. Simultaneously, it is taking on a degree of operational complexity and financial leverage that is, by any measure, well outside of its historical comfort zone. This results in the fact that the investment case hinges less on strategic rationale, which is broadly in line, but more on execution, which remains untested at this scale. The most significant strategic logic is thereby visible through the geographic repositioning. McCormick has traditionally been concentrated in developed markets, meaning strong positions in North America and parts of Europe, but limited exposure to higher-growth emerging economies. The acquisition of Unilever’s food business materially changes this profile, with Knorr in particular having deep and established distribution across Asia, Africa, and Latin America. This offers McCormick immediate access to structurally faster-growing markets. It also means that the acquisition initiates a fundamental shift in the company’s revenue mix, with a larger share of growth now tied to emerging market consumption trends. This geographic expansion, however, also introduces new layers of risk. This starts with the fact that emerging markets bring significantly greater currency volatility and range from input cost sensitivity to regulatory complexity, as well as more fragmented competitive landscapes. Management of these dynamics requires capabilities such as localised supply chains and pricing strategies, which McCormick has not needed to develop at scale from a historical perspective. The upside is clear, but so is the execution risk.

The transaction significantly changes McCormick’s risk profile, also from a financial perspective. The above-mentioned pro forma net leverage of approximately 4.0x EBITDA places the combined entity at the upper bound of investment grade tolerance, which reduces its financial flexibility and increases sensitivity to both operational underperformance and macroeconomic conditions. Taking the current rate environment into account, this translates into tighter interest coverage and a constrained ability to absorb shocks. The deleveraging plan is therefore central to the equity story: conditional rather than guaranteed, relying on stable earnings and successful integration. While necessary to support the transaction economics, the synergy case demands particularly careful examination. Cost synergies, which are primarily reached through procurement efficiencies and manufacturing optimisation, as well as overhead rationalisation, look credible in principle, especially since a significant scale overlap in supply chains is in place. This is, however, an oversimplification, since the integration of such large, geographically dispersed operations introduces several risks across systems, logistics, organisation, and execution. Delays or simple inefficiencies could materially erode expected savings. Revenue synergies are even less certain. McCormick’s deep expertise in flavourings and seasonings, sitting on top of Unilever’s vast emerging market distribution network, is intuitively appealing. The story changes when we take into account the duration of commercial integration, local market adaptation, and sustained investment that such synergies require, which usually takes multiple years if not decades. In practice, these requirements are difficult to quantify ex ante and rarely deliver in line with initial projections.

More fundamentally, the transaction raises a strategic identity question. McCormick has historically operated as a focused category leader in flavourings and spices, where it benefited from multiple attributes: strong brand equity, pricing power, operational discipline, and a relatively narrow segment. The post-transaction entity, however, will operate a much broader set of food categories. These include condiments and meal solutions, which are each characterised by different competitive dynamics, including greater exposure to private label and stronger retailer bargaining power. The diversification may provide scale, but at the same time, it risks diluting the company’s traditionally consistent margin profile. From a capital markets perspective, the transaction effectively redefines McCormick’s equity story from a defensive, category-focused compounder to a leveraged integration and execution case. This shift has implications for both valuation and investor base. While synergy realization and disciplined deleveraging could define a successful integration and support multiple expansion over time, the margin for error is limited. Any early signs of integration challenges or earnings volatility could lead to an amplified reaction and be penalised disproportionately, considering the elevated leverage and scale of the strategic transition.

Is this deal good for Unilever and its investors?

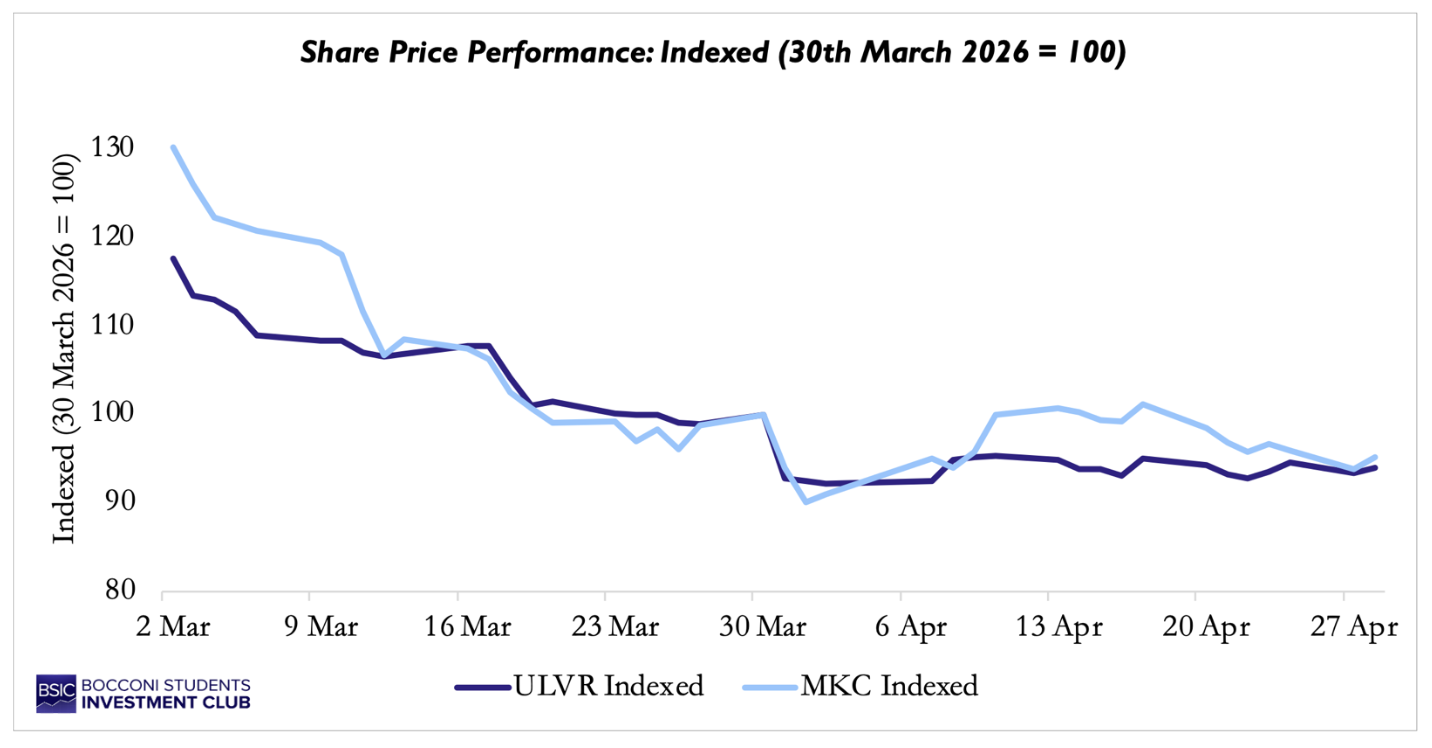

The deal announcement was met with a negative reaction from investors from both companies, with Unilever shares falling by ~7% following the news, wiping off ~£5.3bn in its market value. This sell-off truly began in mid-March, when rumours of the spin-off first began to circulate, and investors’ scepticism began to build. One of the root causes for this bearish outlook was due to the structure of the transaction, with Unilever shareholders being paid with McCormick stock, ~55.1% worth, with only $15.7bn consideration in cash. There was negative sentiment surrounding this because McCormick was already underperforming. The other backlash came from the fact that Unilever shareholders will not be able to vote on the transaction. The graph below illustrates the market’s reaction.

On the other side, McCormick shareholders face a different concern, which explains the sell-off post announcement. With McCormick already highly leveraged, the company used bridge loans to fund the cash component of the deal, resulting in the new combined entity having a debt-to-EBITDA ratio of ~4.0x, which sits at the very high end of leverage for a consumer staples business. Management responded by stating it would deleverage swiftly, expecting to reduce net leverage from 4.0x to 3.0x within two years, but whether this trajectory is true, and whether this deal creates long-term value, remains the question for investors.

On the other side, McCormick shareholders face a different concern, which explains the sell-off post announcement. With McCormick already highly leveraged, the company used bridge loans to fund the cash component of the deal, resulting in the new combined entity having a debt-to-EBITDA ratio of ~4.0x, which sits at the very high end of leverage for a consumer staples business. Management responded by stating it would deleverage swiftly, expecting to reduce net leverage from 4.0x to 3.0x within two years, but whether this trajectory is true, and whether this deal creates long-term value, remains the question for investors.

Fundamentally, the market’s scepticism raises the question: was the deal price actually fair value for such an asset? The deal values Unilever Foods at an EV of $44.8bn, implying an EV/EBITDA multiple of 13.8x on Unilever’s and a 3.6x EV/Sales multiple. Against our trading comparable peer group (see table below), including food companies: General Mills [NYSE: GIS], Nestlé, Conagra [NYSE: CAG], Kraft Heinz, Hormel Foods [NYSE: HRL] and Mondelez [NASDAQ: MDLZ], the peer group average EV/EBITDA is 11.1x, implying a standalone valuation of ~€36.1bn on Unilever Foods’ 2025 EBITDA. Looking on an EV/Sales basis, the peer average is 1.9x, far lower than the deal’s implied 3.6x. Given that Unilever Foods has stronger EBITDA margins than the comparable set, we believe our EV/EBITDA multiple is a more informative valuation lens for assessing the deal.

Although a ~24% premium may seem respectable, when considering the world-class brands in Unilever Foods such as Hellmann’s and Knorr, and global distribution presence, the deal could command a far higher premium above the broad food sector. Thus, Unilever did not sell cheaply in absolute terms, but due to its superiority over similar businesses in brand quality and presence in emerging markets, it could have demanded a higher premium above its peers, and the peer group distorts the true valuation of the food division.

Examining the rationale behind the RMT structure more closely, via separating Foods, Unilever transformed from a diversified consumer conglomerate to a focused pure HPC business. HPC businesses, especially with Unilever’s margin profile and financials, command higher multiples than diversified staples companies, and avoid exposure to the commodity costs and weak pricing power that food businesses are faced with. Thus, Unilever has the potential to experience a valuation uplift, which could create more value than the deal premium itself.

From a shareholder perspective, the structure means they are compensated with a 55.1% majority stake in McCormick, so they remain exposed to the food sector. The benefit of holding these shares is that the combined McCormick is a dominant food company with a high concentration of renowned food brands, and Unilever Foods gives the new entity exposure to emerging markets, thus McCormick’s share price could rise in the coming years. The RMT structure used also has tax benefits, as a sale of the Foods business would have triggered a substantial capital gains tax, which would limit proceeds to shareholders.

Therefore, by examining the sum of both parts, a higher-rated HPC Unilever and an increasingly dominant McCormick could be worth more than the conglomerate was in the long run. However, execution risk plays a vital role in order to achieve this. On one side, it is dependent on whether the market re-rates Unilever based on it being a pure HPC business, and on the other side, McCormick has to absorb a business twice its current size, while integrating its operations and culture, and handling the increased debt burden.

Aside from the strategic validity of this deal, the transaction itself presents a few significant issues. Around 65% of the transaction value is McCormick stock and not cash. Since McCormick is a New York-listed company, this deal exposes the shareholders of Unilever, which is London-listed, to significant FX risk as they are primarily UK and European institutional investors. The deal is not set to close until mid-2027 due to McCormick shareholder approval requirements and regulatory clearance. Therefore, during this period, value for Unilever shareholders derived from the deal partly depends on fluctuating USD/GBP and USD/EUR exchange rates, with major moves in the exchange rate having the capability to erase significant deal value.

Additionally, as previously mentioned, the high percentage of the deal value that Unilever shareholders receive in McCormick stock exposes them to McCormick’s performance. This has already led to a loss of deal value as McCormick’s shares fell to $48.38 on April 1st, a seven-year low. This is both a significant drop from the $57.84 share price at the time that the deal multiple was set and a 16% decrease in deal value before the deal even closed. Furthermore, McCormick itself is acquiring a business that is more than twice its size, which makes integration difficult. Before the deal, McCormick had ~$6.8bn in revenue, and it now adds ~$13.3bn in revenue from Unilever Foods.

Meanwhile, the operational synergies of $600m annually across manufacturing, logistics, and SG&A are aimed to be achieved by year 3 post-close. This target is aggressive and has historically been met only rarely. Aside from the deal structure’s high leverage, McCormick itself is a slow-growing company that is a potential turnaround. However, the company’s success depends on its ability to achieve meaningful organic growth with Unilever’s Hellmann’s and Knorr, considered mature mega-brands with limited potential for growth, a situation further exacerbated by structural factors such as more health-conscious consumers and GLP-1-driven demand reduction.

Another potential issue is the fact that a core strategic rationale for the deal is that McCormick wants to leverage Unilever’s footprint in emerging markets to scale its own brands. However, emerging market growth for Unilever’s products has slowed, and the US domestic McCormick management team has little expertise to achieve the push into emerging markets. As a result of the deal structure, instead of only owning shares in a pure-play personal care company, investors are also exposed to a US-listed, highly leveraged, slow-growth company.

To further investigate whether this transaction will ultimately create or destroy value for Unilever’s shareholders, we carried out a sum-of-the-parts valuation, combining the firm’s standalone HPC business with a separate valuation of its food business. Since we assume to be looking at two separately listed entities, we used traded comparable companies to value both business lines. As previously mentioned, by using comparables in the food sector, this division of Unilever has an enterprise value of ~€36.1bn, while for the HPC division, the sector average EV/EBITDA multiple is 13.5x (see below), which was found by using the following as comparable companies: L’Oreal, Colgate, Procter & Gamble, Kenvue [NYSE: KVUE], Beiersdorf [XETRA: BEI-DE], and Kao Corporation [TYO: 4452].

The implied enterprise value based on the average market multiple and a pro forma EBITDA of ~€8.1bn is ~€109.7bn (~£95bn). By adding the two businesses, we obtain a combined enterprise value of ~€145.7bn (~£126.2bn), which translates into a sum-of-the-parts market capitalization of ~€120.7bn (~£104.6bn). Compared to this equity value, the market capitalization of ~€114.8bn from March 30th (before the deal was announced) reflects a conglomerate discount of €5.8bn (almost 5% of total equity value). This confirms the claim that the market was pricing, at least partly, the strategic tension resulting from trying to grow two increasingly diverging businesses inside the same company and under the same governance, and suggests that investors may benefit from their separation, as it would allow each segment to be valued based on its underlying growth and profitability profile.

However, only time will tell if the theoretical benefits arising from this separation will be realised. As previously mentioned, Unilever’s investors will transition from owning a fully controlled food business to owning a majority stake in a standalone player facing significant integration and execution risk. To understand the potential impact of these risks on the stock portion of the transaction consideration, we conducted a simplified scenario analysis of the combined entity’s performance and its equity valuation. After its acquisition of a majority stake in a long-standing joint venture called McCormick de Mexico for $750m in 2025, McCormick’s pro forma EBITDA is ~€1.3bn. To this, we added Unilever’s contribution from the food division (excluding Hindustan Unilever Limited), which we derived to be ~€2.9bn.

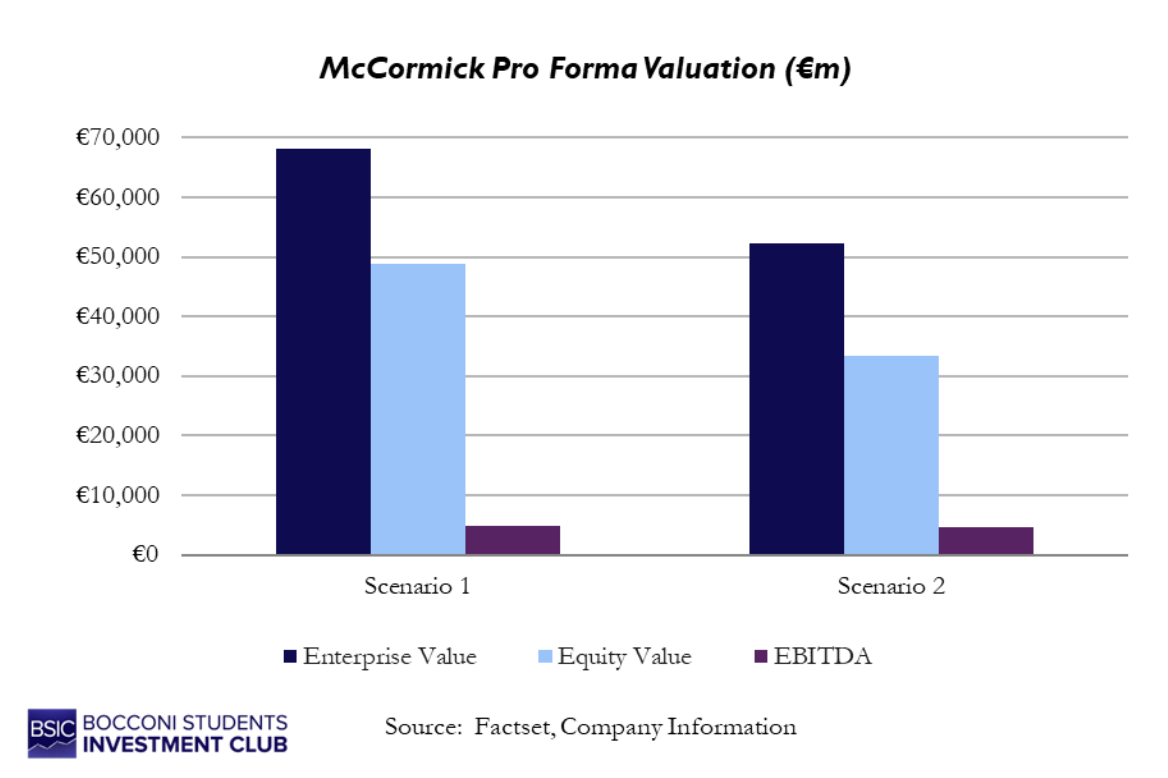

With the combined entity’s EBITDA, we were able to draw two simplified scenarios of the value of McCormick one year post close (FY 2028, considering the expected mid-2027 close), based on management’s ability to realise synergies and on the market’s perception of the quality of the business. In our optimistic scenario (Scenario 1), management realises 25% of the $600m of run-rate cost synergies by year one (~€133.5m) and, with a 5% growth rate from 2026 to 2028, we expect total EBITDA to reach ~€4.9bn, a 24.4% margin. Then, we assumed that McCormick would be well perceived by investors and would trade at an EV/EBITDA multiple of ~14.0x (on par with competitors such as Nestlé and Hormel Foods). With these assumptions, and by referring to a post-close leverage of 4.0x, we are able to value the whole business at an enterprise value of ~€68.1bn and at an equity value of ~€48.7bn, which translates into a stake value of ~€31.7bn for the 65% (~€26.9bn for the 55.1% ultimately owned by Unilever’s shareholders) and an increase of 22.3% compared to the value of the initial equity consideration.

On the other hand, if we consider a scenario (Scenario 2) where management is unable to realise any cost synergies in the first year, and we assume that the market will price McCormick at an industry average multiple of ~11.1x, the situation is different, and the investment is less appealing. In this case, we expect total EBITDA to be closer to ~€4.7bn. The company’s enterprise value would be closer to ~€52.2bn, and the market capitalization would be ~€33.4bn (see below). This would bring the value of the 65% stake to ~€21.7bn (~€18.4bn for the 55.1%), which would mean that the stake would be worth ~16.2% less than the original consideration.

Overall, the transaction offers a credible path to value creation. However, the risks related to the performance of the combined McCormick entity, as reflected in the equity portion of the total consideration, introduce an element of uncertainty to the overall outcome of this deal. Therefore, Unilever’s shareholders will have to trust the ability of McCormick to successfully integrate their former food division and position itself as an efficient and successful player in the sector.

0 Comments