Introduction

A potential $40bn merger between The Estée Lauder Companies Inc. [NYSE: EL], the skincare giant, and Puig [BME: PUIG], a fragrance-focused portfolio company, is poised to reshape the global beauty industry. On 23 March 2026, early-stage discussions were confirmed between the two groups concerning the creation of a conglomerate housing over 50 brands, including Tom Ford, Clinique, Charlotte Tilbury, and Byredo, generating approximately $20bn in annual sales.

However, widespread market scepticism emerged immediately despite evident synergies. While Puig’s shares surged 15% the day after the announcement, Estée Lauder’s plummeted by 9%, underscoring concerns over execution risk, valuation, and strategic direction. The timing of the deal adds further complexity, given Estée Lauder’s ongoing turnaround efforts alongside declining travel retail performance amid geopolitical tensions.

The deal also comes amid rapid consolidation across the beauty industry and closely follows L’Oréal’s [EPA: OR] recent acquisition of Kering’s [EPA: KER] beauty business. This highlights a broader industry shift towards capturing value in fragrance, beauty’s most dynamic and fastest-growing segment. As a result, Estée Lauder is also under increasing pressure to defend its market share against more aggressive competitors.

If realised, a merger with Puig would mark Estée Lauder’s largest deal to date. It would also represent a decisive repositioning towards fragrance-led growth. However, its success remains uncertain, with the realisation of synergies dependent on the company’s ability to balance its turnaround efforts, manage balance sheet pressures, and achieve effective cultural integration.

Fragrance: Beauty’s Growth Engine

Fragrance has become one of the main growth areas in the wider beauty industry. While overall beauty demand remains stable, growth has become increasingly uneven. In this context, fragrance stands out because it combines premium pricing, strong consumer interest, and relatively stable demand. According to Reuters [NYSE: TRI], prestige fragrance grew 5% by value in 2025, ending the year as the “second-largest category in prestige retail”. Forecasts also predict that fragrances will account for 23% of total beauty growth between 2024 and 2029. This helps explain why major beauty brands are competing aggressively for exposure to the segment. The proposed Estée Lauder and Puig deal therefore does not only have the intention of increasing scale. It is also about securing a stronger position in one of the most attractive segments of the beauty market.

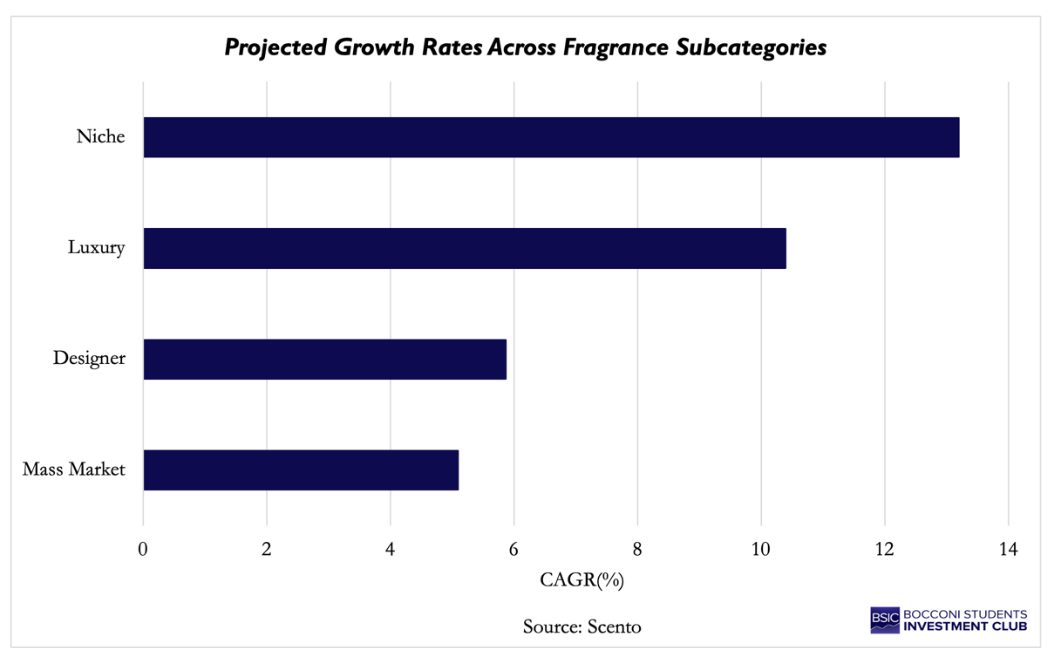

Within the fragrance segment, growth varies across subcategories. Premium fragrance has outperformed the mass market in recent years, with niche fragrance emerging as the fastest-growing part of the category. They account for approximately 20% of the global fragrance market, showing strong growth since the 5% share before the pandemic. This is due to their leading annual growth rate of 13.2%, suggesting that consumers are increasingly moving away from standard designer products and towards scents that feel more exclusive and personal. By contrast, designer fragrances are projected to grow around 5.87%, while the mass-market is expected to grow by 5.1%, which further highlights the strength of niche fragrance. Their appeal is closely linked to their “artisanal quality”, rare ingredients, and limited production, as seen in brands such as Creed, Byredo, and Le Labo. This also helps explain why premium fragrance has become so valuable within the wider beauty industry, as it offers both stronger pricing power and a better sense of brand identity than more standardised products. Regional trends also reflect this strength, with Europe accounting for 33.26% of the global fragrance market, while APAC is expected to be the fastest-growing region.

The main reason for this growth is that fragrance is no longer bought solely as a practical beauty product, but also as a form of identity. Unlike skincare, which is often tied to routine and use, fragrance is closely linked to mood, occasion, and personal image. Social media has played a major role in establishing this idea. For example, platforms such as TikTok have introduced the idea of “fragrance wardrobing”, where consumers collect different scents for different settings or layer fragrances to create something more individual. Thus, consumers no longer want to buy just one signature scent and repurchase it from time to time. Instead, they are being influenced to build a collection of fragrances, resulting in greater sector engagement. Younger consumers show this shift in consumer preferences most clearly. Many of them use fragrance as a form of self-expression. This is why niche and unisex fragrances have grown in popularity, as they allow for more individuality than designer brands do. Product launches reflect this shift as well, with unisex fragrances increasing to 40% of new launches in 2024.

The main reason for this growth is that fragrance is no longer bought solely as a practical beauty product, but also as a form of identity. Unlike skincare, which is often tied to routine and use, fragrance is closely linked to mood, occasion, and personal image. Social media has played a major role in establishing this idea. For example, platforms such as TikTok have introduced the idea of “fragrance wardrobing”, where consumers collect different scents for different settings or layer fragrances to create something more individual. Thus, consumers no longer want to buy just one signature scent and repurchase it from time to time. Instead, they are being influenced to build a collection of fragrances, resulting in greater sector engagement. Younger consumers show this shift in consumer preferences most clearly. Many of them use fragrance as a form of self-expression. This is why niche and unisex fragrances have grown in popularity, as they allow for more individuality than designer brands do. Product launches reflect this shift as well, with unisex fragrances increasing to 40% of new launches in 2024.

However, this stable demand does not guarantee that the fragrance sector is free from risk. One weakness lies in travel retail, which has been a crucial sales channel for premium fragrance. Since the conflict in the Middle East has disrupted air travel, it has also weakened the outlook for airport retail. Furthermore, inflation has made consumers more selective, as they pay closer attention to whether beauty products genuinely justify their price. This is particularly relevant for fragrance, as this is often treated as an “affordable luxury”. However, rising inflation is challenging its accessibility, meaning the “lipstick effect” cannot be fully relied on.

These pressures explain why fragrance has become one of the most contested beauty segments. It is no longer just the largest global groups driving competition in premium fragrance, but also independent niche houses and celebrity-backed brands. Thus, brands are consolidating to protect their position in this increasingly competitive market, while also benefiting from future growth. According to Reuters, the Estée Lauder and Puig deal would raise the group’s share of premium fragrance from 6% to 15%, placing it just behind L’Oréal at 16%. This shows the strategic importance of fragrance within the broader beauty market.

Despite these risks, fragrance remains one of the most attractive beauty segments. Its appeal lies in the fact that it offers growth and premium pricing, while also strengthening a firm’s position in the market. This explains why many firms are consolidating, as seen in the proposed Estée Lauder and Puig deal.

Deal Rationale: A Perfume Powerhouse

On 23 March 2026, Estée Lauder [NYSE: EL] announced merger talks with Puig [BME: PUIG], in a deal valued at approximately $40bn. The combined entity could capitalise across key segments of the beauty industry, such as skin-care innovation and major makeup brands like MAC and Charlotte Tilbury. Although discussions have been confirmed, the final terms are yet to be finalised. The transaction is widely speculated to take the form of a public takeover of Puig conducted by Estée Lauder, financed through a mixture of cash and shares.

The proposed deal comes with increasing uncertainty within beauty due to Middle East conflicts, a slowdown in the Chinese market, and intensifying competition. These factors are encouraging consolidation among larger players. Strategically, the merger would allow Estée Lauder to strengthen its fragrance portfolio by incorporating brands such as Jean Paul Gaultier and Byredo. At the same time, Puig would benefit from access to Estée Lauder’s extensive retail network, supporting the global expansion of its brands, especially in the APAC region. The combined entity would also achieve greater geographic diversification, reducing Estée Lauder’s reliance on the Chinese market from around 50% of revenues to approximately one-third. Fragrances are expected to account for roughly one-third of total revenues, while additional efficiencies could be realised through cost savings in research and development.

Puig Overview

Puig is a family-owned company focused on promoting consumer wellness, confidence, and self-expression. Founded in 1914, it has built its identity around an entrepreneurial spirit combined with creativity and a strong commitment to innovation. The group operates across fragrances, fashion, makeup, and skincare, with a strategy centred on “Love Brands” that drive consumer engagement through storytelling and emotional connection.

Its portfolio includes globally recognised brands such as Paco Rabanne, Carolina Herrera, and Jean Paul Gaultier. Fragrance represents Puig’s core business, accounting for 72% of net revenues and growing at 6.4%, with the company holding an 11.1% market share in this segment despite its highly competitive nature. In FY2025, top-performing brands included Carolina Herrera and Jean Paul Gaultier, alongside strong double-digit growth in the niche segment led by Byredo. Smaller divisions such as makeup and skincare also performed strongly, growing by 13.7% and 8.9%, respectively.

Geographically, Puig generates 55% of its revenues in EMEA, 35% in the Americas, and 11% in Asia-Pacific, with the latter showing particularly strong momentum at 21.7% growth. In FY2025, the company reported $5.04bn in sales, with a gross margin of 75.1% and adjusted EBITDA of $1.04bn, corresponding to a 20.7% margin.

Puig went public in 2024 with a valuation of $16bn, which was one of the largest Spanish IPOs in nearly a decade, and was subsequently included in the IBEX 35 index. However, its valuation has since declined to around $10bn. The company’s growth has also been driven by a series of strategic acquisitions. Beginning in 2011, Puig acquired a 65% stake in Jean Paul Gaultier (45% from Hermès and 10% from the designer himself) and later secured the brand’s fragrance license in 2016. In 2020, it took a majority stake in Charlotte Tilbury, adding a fast-growing makeup and skincare brand aligned with its core values of creativity and storytelling, while enabling global expansion through Puig’s distribution network.

Additional acquisitions, including Byredo, Kama Ayurveda, Loto del Sur, Dr. Barbara Sturm, and Dries Van Noten, have further strengthened Puig’s position as a diversified and globally competitive beauty group.

Estée Lauder Overview

Estée Lauder was founded in 1946 by Estée and Joseph Lauder and has grown into a global leader in skincare, makeup, fragrance, and haircare. The company operates a portfolio of over 20 luxury and prestige brands across more than 150 countries. It remains under the control of the Lauder family, which holds approximately 84% of the voting rights. Key brands include MAC, Jo Malone, and Tom Ford.

The group’s strategy is built around a diversified brand portfolio designed to meet a wide range of consumer preferences, price points, and lifestyles. Skincare is the largest segment, accounting for 49% of net sales, followed by makeup at 29%. Geographically, revenues are relatively well balanced, with the highest contribution coming from Europe, the Middle East, and Africa, generating around $5.4bn.

More recently, Estée Lauder has faced significant challenges, including a $1.15bn decline in net revenues, largely driven by weaker consumer demand and lower conversion rates in the Chinese market. Despite this, the company benefits from a strong global distribution network, with over 1,600 freestanding stores.

In response to market pressures, Estée Lauder has been undergoing a restructuring process focused on brand investment, innovation, and improved in-market execution. Like Puig, the company has also relied on inorganic growth to expand its portfolio. It acquired a 51% stake in MAC in 1994, followed by full ownership in 1998. Jo Malone was acquired in 1999, with the founder agreeing to a five-year non-compete clause and relinquishing rights to her name. More recent acquisitions include Tom Ford for $2.8bn and a majority stake in DECIEM, the parent company of The Ordinary, for $1.7bn, following an initial partnership established in 2017.

A Credible L’Oréal Challenger?

L’Oréal [EPA: OR] has established itself as a global leader in the luxury beauty and fashion industry. It has historically acquired many brands like Aesop (2023), IT Cosmetics, Lancôme, and YSL Beauté. More recently, L’Oréal acquired Kering’s [EPA: KER] beauty division for $4.6bn, gaining access to key brands including Creed, Gucci, Bottega Veneta, and Balenciaga, while agreeing to pay royalties to Kering.

L’Oréal’s competitive advantage lies in its high level of diversification across distribution channels, dermatological categories, and geographic markets. Its scale allows the company to reallocate resources efficiently across segments, providing resilience during market downturns. In contrast, many competitors are more specialised, which enables strong performance in niche areas but can expose them to greater volatility during periods of weakness.

A potential merger between Estée Lauder and Puig could strengthen their competitive position against L’Oréal. By combining their portfolios and leveraging greater scale, the merged entity could enhance its bargaining power in distribution and increase market share, particularly in high-growth regions such as China. Like L’Oréal, the combined group would benefit from a more diversified portfolio across both product categories and geographic markets.

A Sour Scent: Market Scepticism Around the Deal

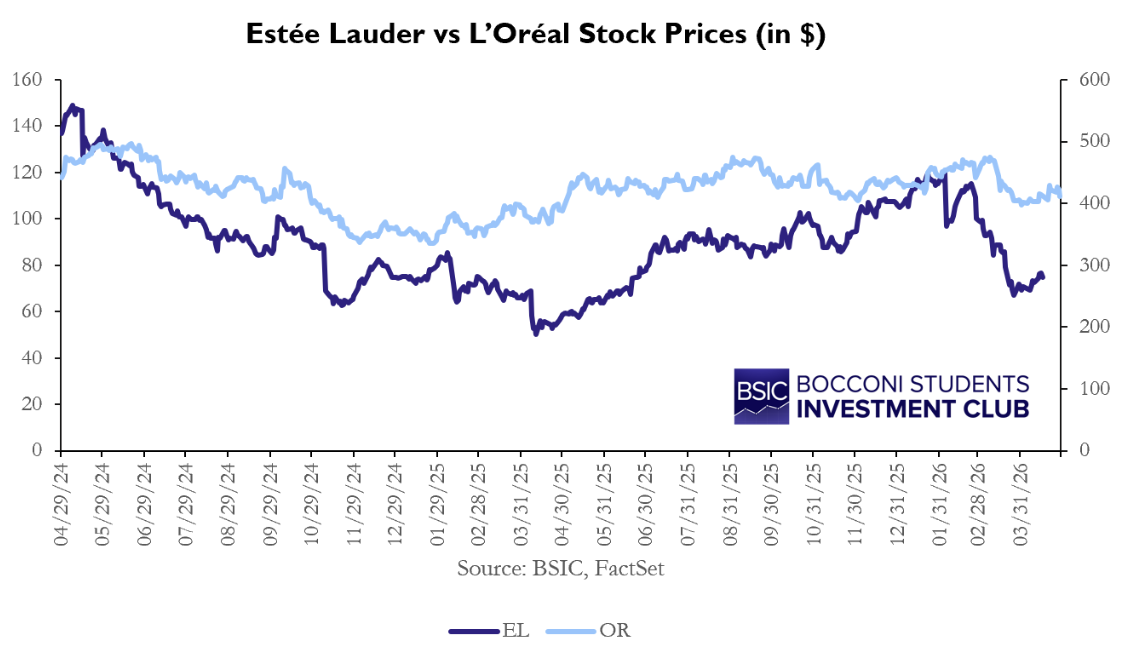

While strategic synergies are evident and, on paper, the rationale behind a potential Estée Lauder-Puig deal seems compelling, the market reaction has been notably negative. The merger discussions triggered a sharp plunge in Estée Lauder’s share price, which is already down roughly 80% from its historic peak late 2021 ($373.44). Moreover, both Moody’s [NYSE: MCO] and S&P Global [NYSE: SPGI] assigned the US company a negative outlook following the public announcement.

The significant investor scepticism surrounding a potential deal is primarily driven by three key risks: timing, financing, and governance. From a timing perspective, investors are concerned that the transaction could disrupt Estée Lauder’s ongoing turnaround efforts. The company experienced three years of declining sales but recently regained the $100 mark for its share price following the launch of CEO Stéphane de La Faverie’s “Beauty Reimagined” plan in February. This turnaround strategy’s focus on “simplifying operations” and “rebuilding profitability” through the following measures: closures of underperforming stores, such as M.A.C., boosting sales in duty-free travel outlets, shifting sales to high-growth e-commerce (TikTok and Amazon [NASDAQ: AMZN]), and accelerating product launches to capture consumer trends.

Thus, a large-scale transaction with Puig rightfully raises execution risks and operational complexity, which could divert management attention at a critical point of company stabilisation. These concerns are amplified given Estée Lauder’s history of weak integration of several smaller brands, such as Too Faced and Smashbox, which are now reportedly in the process of being sold. However, as noted by analysts at Citigroup [NYSE: C], such negative market reactions are not unique, with investor scepticism persistent across large consumer mergers.

For instance, Keurig’s merger with Dr Pepper [NASDAQ: KDP] and Kimberly-Clark’s [NYSE: KMB] separation of Kenvue [NYSE: KVUE] reflects broader structural concerns within the consumer sector. Consumer deals are particularly sensitive to market sentiment given their reliance on brand equity and customer loyalty, which can easily be diluted. Moreover, synergies are often less tangible, and growth remains dependent on demand rather than efficiencies.

Financing of the deal presents itself as the other major concern for investors. While no formal structure has been outlined, JPMorgan [NYSE: JPM] analysts suggest that a transaction would most likely be funded through an equal split of equity and debt. This could require Estée Lauder to raise approximately $6bn in additional borrowing, pushing leverage to around 4.3x before any realised synergies. Moreover, the Puig family maintains tight control over its namesake company, owning approximately 77% of Puig’s outstanding shares. This poses further constraints on deal structuring and increases the risk of overpayment for Puig.

Analysts at Jefferies [NYSE: JEF] estimate that any takeover bid would likely require a significant premium, potentially 30%. Furthermore, as Puig is a European (Catalan) group while Estée Lauder is New York-listed, regulatory hurdles could prevent a share-only transaction, as the companies are not domiciled in the European Union. As such, this would necessitate a substantial cash component, which would further strain Estée Lauder’s balance sheet.

Governance and cultural differences add further risk to a potential deal. While Estée Lauder operates a performance-driven, quarterly focused approach, Puig has historically prioritised long-term brand-building under family control. This divergence could manifest in a severe culture clash post-merger, particularly concerning creative direction and the preservation of brand identity. There is the risk that Puig’s distinctive brand identity and positioning, exemplified by its Jean Paul Gaultier or Byredo fragrances, could be diluted within Estée Lauder’s larger corporate structure, undermining the value the acquisition seeks to capture.

Thus, combined with Estée Lauder’s ongoing turnaround and balance sheet pressures, the deal appears to introduce significant complexity and execution risk when strategic focus and operational discipline are critical to restoring competitiveness.

Conclusion

If the proposed deal materialises, the combination of Estée Lauder’s global distribution network and Puig’s fragrance expertise could position the merged entity as a credible challenger to L’Oréal. The transaction would also accelerate consolidation within the fragrance segment. Greater consolidation of fragrance among a few global conglomerates could mean the gradual erosion of “niche” fragrances as scales begin to dilute the exclusivity that underpins their appeal. In doing so, the deal could redefine and potentially dampen the dynamism of the fragrance segment.

Another point of note is that while the strategic rationale underpinning the deal appears compelling, success is far from guaranteed. While the merger would address Estée Lauder’s underweight fragrance portfolio and Puig’s limited exposure to the APAC region, execution risks may outweigh the anticipated synergies.

More broadly, the Estée Lauder-Puig transaction underscores a shift in the beauty industry, illustrating how fragrance has become the central battleground for growth. Ultimately, the success of such mergers will depend less on scale and more on execution and the preservation of brand equity.

0 Comments