Heineken N.V. (AMS:HEIA) – market cap as of 3/3/17: €45.05bn

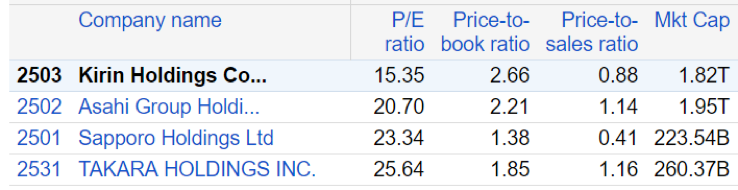

Kirin Holdings Co. Ltd. (TYO:2504) – market cap as of 3/3/17: ¥1.82tn (€15.05bn)

Introduction

On February 13, 2017, Japanese brewer Kirin Holdings Company has agreed to sell its Brazilian beer business to Heineken for ¥77bn (€664m). The deal will make Heineken the second-largest beer company in Brazil, the world’s third largest market for beer. With a 17% market share, the Dutch brewer will be able to shake the dominance of rival Anheuser-Busch InBev in its oldest market. The acquisition, dependent on approval by Brazil’s antitrust agency, is expected to close in the first half of the year.

About Heineken N.V.

Heineken N.V is a Dutch brewer company founded in 1864 by Gerard Adriaan Heineken. Today Heineken is the number one brewer in Europe and the second largest brewer by volume in the world. It sells beer in 170 countries, produces beer at more than 160 company-owned breweries and employs more than 73,000 people all around the world.

The company’s beer portfolio includes several international as well as regional brands, among which the two largest are Heineken and Amstel.

Heineken N.V., whose biggest market is Europe, has recently increased its focus on international expansion. With recent acquisitions in Africa, India, Asia and Latin America it is continuing to increase its presence in emerging markets which will contribute to its ongoing growth.

Despite a tough economic environment and significant currency fluctuations, Heineken managed to deliver strong results in 2016. In FY 2016 the company reported €20.79bn in revenues (1.4% YoY growth), operating profit of €3.54bn (4.7% YoY growth) and net income of €2.1bn (2.4% YoY growth).

About Kirin Holdings Co. Ltd.

Kirin Holdings is a Tokyo-based beverages company operating in over 8 countries, with ¥2.07tn (€17.13bn, down 5.5% YoY) in revenues during 2016, and an operating margin of 9.6% (up 1.20% since 2015).

Kirin is organized into (1) Japanese beverages business, (2) Overseas beverages business, and (3) Pharmaceuticals and Bio-chemicals business. The Japanese group entered the Brazilian market in 2011 with a $3.9bn acquisition of the family-run brewery Schincariol in a deal that proved troublesome as family members initiated a legal battle over the change of control in the transaction.

Brasil Kirin is a subsidiary of Kirin Holdings. The company operates 12 breweries in the country and runs its own distribution network. Its regional presence in Brazil is focused on the North and Northeast regions, and it holds a 9% market share nationally. On top of its most popular brands (Schin and Devassa), Brasil Kirin also owns premium beer brands such as Baden Baden, and Eisenbahn. For the past year, the company has reported revenues of R$ 3.71bn (€1.12bn, 0.2% YoY growth) and operating losses of R$262m (€79.15m, a 18.6% YoY improvement).

Industry Overview

The alcoholic beverages industry is a fiercely competitive one, in which only top performers can achieve satisfying profit margins. The top players in the global beer industry are AB InBev-SAB Miller, Heineken, and Carlsberg, whose combined produced volumes account for c. 47% of beer production worldwide. The brewing industry is segmented basically into three segments: developed markets, in which growth is sluggish due to shifting consumer preferences and changing demographics; developing markets, which present substantial growth opportunities as the disposable income of consumer rises; and the premium, craft beer market, in which competition is driven by differentiation, and the (usually small) brewers enjoy appealing margins and high growth rates.

The industry has experienced a consolidation drive in the past years, as shown by AB InBev’s merger with SAB Miller, announced in 2016. The merger of the two largest players in the industry hinders the prospects of competitors, since the combined AB InBev-SAB Miller will be able to squeeze suppliers and offer customers lower prices while keeping the same margins, or even better ones. Following this consolidation trend, Heineken has been pursuing its own expansion strategy, which includes, in addition to the Brasil Kirin deal, the acquisition of the shares Heineken did not already hold in Asia Pacific Breweries, a Singapore-based brewery company operating in high growth markets like Vietnam.

Deal structure

The total consideration to be paid to Kirin for Brasil Kirin’s equity is €664m, corresponding to an implied enterprise value of €1.025bn. For Heineken, these figures indicate a sharp (nearly 75%) discount from the $4bn that Kirin paid for the assets in 2011.

The massive discount stems from Brasil Kirin’s operating problems. Indeed, the company reported losses for €79.15m last year.

Given the company’s negative earnings it is hard to provide a meaningful valuation with the multiple approach. Nonetheless, Brasil Kirin’s 2016 revenues ((€1.12bn) imply a P/Sales multiple of 0.59 which is considerably lower than both its parent figure and the industry average.

Following the transaction completion, Brasil Kirin will be consolidated with Heineken. Completion of the acquisition is subject to customary regulatory approvals and is expected in the first half of 2017.

Source: BSIC

Deal rationale

The transaction will allow Heineken to become a potential threat to AB InBev, for which the Brazilian market is of major importance. The acquisition of Kirin’s beer business will increase Heineken’s share in the Brazilian market from 7% to c. 17%.

The transaction is aligned with Heineken’s strategy of becoming one of the largest players in all the countries it covers. Although 17% is still a small portion compared to the 67% market share of AB InBev in Brazil, this transaction indicates that Heineken has set out to conquer its share of the world’s third largest beer market. On the news of AB InBev’s disappointing results for 2016, during which it lost market share and had margin reduced, Heineken’s challenge to the beer giant in one of its most prized markets is a credible one.

Moreover, the company expects to deliver significant cost synergies from the acquisition through production efficiencies, including optimization of logistics, and through better use of selling channels. This optimization is expected as the deal will make Heineken big enough to develop its own distribution system and reduce its dependence on Coca-Cola’s bottler network in Brazil.

Finally, the company believes that the acquisition strengthens its platform to further develop its premium brands portfolio, particularly in regards to Heineken and Sol. In addition, Heineken expects the transaction to be dilutive to its margin in 2017, however it did not provide more detailed transaction guidance including the necessary accounting adjustments yet, nor the quantification of potential dilution.

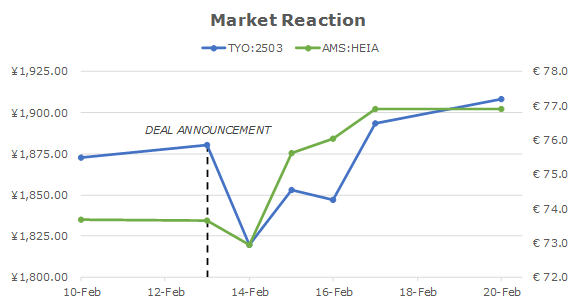

Market reaction

On the day after the announcement of the transaction, Heineken’s stocks experienced a modest loss of 0.96%, whereas Kirin experienced a 3.24% stock price decrease. However, one week after the announcement date, Heineken had a 4.4% gain compared to the price on February 13th, while Kirin’s stock rose only 1.49% during the same period.

Source: BSIC

Financial Advisors

Heineken was advised by Credit Suisse Group AG, whereas Mitsubishi UFJ and Morgan Stanley advised Kirin.

0 Comments