Anadarko Petroleum Corporation (NYSE: APC) – market cap as of 29/05/2019: USD 36.61bn

Occidental Petroleum Corporation (NYSE: OXY) – market cap as of 04/05/2019: USD43.34bn

Intro

On April 29, 2019, US oil and natural gas producer Anadarko was on course to accept a takeover offer from its national rival Occidental, which gatecrashed an already established offer of $50bn from major US oil producer Chevron. Occidental would offer an enterprise value of $57bn, evenly splitting the payment in cash and shares of stock. The higher valuation given seems to please Anadarko’s shareholders, who stated that Occidental’s offer increases indicative valuation, terms and conditions in the final contract. The deal is one of many more transactions in a trend of consolidation, especially around the Permian Basin, the heart of the US oil boom, where Anadarko is one of the major holders of shale acreage. A combination of the two companies would ultimately determine a strong competitive advantage and savings of $3.5bn in operating and capital costs.

About Anadarko Petroleum Corporation

Formed in 1959 as an initial subsidiary of Panhandle Eastern Corporation Pipe Line Company, after the discovery of large quantities of natural gas in the Anadarko Basin between the states of Texas, Oklahoma and Kansas, it became an independent and public company in 1986 after a corporate spin-off. Today, Anadarko, with its HQ in The Woodlands, Texas, is recognized as one of the largest US oil and gas exploration companies with a traditionally integrated value chain, as it acquires, explores, develops, produces and markets oil and natural gas globally.

The company expanded itself through several acquisitions of local energy companies in the states of Colorado, Utah, Texas, Wyoming and established the largest number of floating facilities in the Gulf of Mexico. In addition, it enlarged its horizons by going offshore with operations in Africa and South America. It has also been at the center of multiple environmental cases, which included the infamous DeepWater Horizon Oil Spill, as Anadarko had a 20% minority stake in the BP owned Macondo Prospect, and the largest environmental contamination settlement in America with a fine of $5.15bn for the former chemical company Tronox of the subsidiary Kerr McGee.

In terms of main products, Anadarko supplies natural gas, natural gas liquids (NGLs), oil and liquified natural gas (LNG). These are the results of multiple business operations organized in Upstream, Midstream and Downstream, which mainly deals with the marketing of the products.

As for the Upstream of the value chain, Anadarko successfully runs operations in many US and offshore countries, holding thousands of net acres in the DJ Basin of Colorado, where it has established itself as the largest oil producer of the state. The company is also one of the major operators in the Delaware Basin, Texas, with a potential of more than 4 billion barrels of oil equivalents (BOE) in recoverable resources and the Powder River Oil Basin in Wyoming. As of natural gas resources, Anadarko possesses large holdings in the Uinta Basin, in Utah and it operates one of the largest complex of floating facilities in the Gulf of Mexico, with 10 deep-water facilities. Regarding offshore lines of business, the company has established operations in Algeria, Ghana, South Africa and Mozambique, where it launched one of the most important natural gas discoveries in the last 20 years, with potential 75 trillion cubic feet of recoverable natural gas in the Offshore Area 1, intended to supply one of the largest facilities of LNG production. Lastly, Anadarko holds interest in developing deep-water exploration blocks offshore Colombia, Peru and Guyana. Regarding the distribution of volumes of sales, 86% were generated by the US operations in 2018. Of the total proved reserves, 45% are oil reserves, 37% are covered by natural gas and 18% by natural gas liquids.

As of Q1 2019, Anadarko generated $3.1bn in revenues but recorded net losses of $15m, determining a profit margin of -0.48%, which has been falling since Q3 2018. In annual terms, the company ended 2018 on a positive note, as it generated $13.1bn of net revenues and a net profit of $615m, with an increasing profit margin of 4.71%, the first positive margin since 2015, due to net losses that shrank in the years thanks to a recovery of oil prices. Operating cash flows amounted to $5.9bn even though it was burnt through investing and financing outflows of $9.159bn.

About Occidental Petroleum Corporation

Founded in 1920 and headquartered in Houston, Texas, Occidental is one of the largest oil and gas exploration and production companies in the world. As its major competitors, the entire business is based on an integrated value chain, as the company controls upstream operations, midstream and marketing segments when it comes to purchases, markets, processes, storage and transportation. Besides oil and natural gas, the company operates a chemical business through its major North America chemical manufacturer OxyChem.

Besides crude oil and natural gas, Occidental produces and supplies a variety of basic chemicals, vinyls, performance chemicals, NGLs, condensates and carbon dioxide. Operations of the upstream includes exploration and production activities centered around the United States, Latin America and the Middle East. Indeed, the company is primarily focusing on the Permian Basin of West Texas and South East of New Mexico, one of the most active oil basins, accounting for approximately 30% of total US oil production. Occidental controls nearly 2.7 million net acres and 10% of oil production of the region through two subsidiaries: Permian Resources and Permian EOR (Enhanced Oil Recovery).

Occidental is also a large investor in the Middle East, with operations in Oman, Qatar and the UAE. In fact, it is the largest independent oil producer in Oman, with more than 6 million gross acres and more than 3,280 new wells. It is also the second-largest oil producer offshore Qatar, in addition to taking part to the Dolphin Gas Project with a 24.5% interest in the local Dolphin Energy, a project which aims at suppling natural gas from Qatar to the UAE and Oman. Occidental is also a major partner in a 30-year joint venture with the Abu Dhabi National Oil Company in one of the largest natural gas developments in the Middle East.

In terms of its recent financial performances, Occidental generated net revenues of $4.8bn in Q4 2018 and a net income of $706m, determining a profit margin of 14.83%, still positive but lower than its Q3 2018 performance. Focusing on an annual basis, the company generated revenues of $17.8bn in 2018 with an increase of 42.5% if compared to 2017. Net income is also growing as the company generated a profit of $4.1bn, a substantial increase from 2015, when Oxy recorded a net loss of $7.8bn. Its profit margin for 2018 was 23.18%.

Industry Overview

2018 was the most active year for M&A in the US upstream oil sector ever since oil prices collapsed in 2014, with total deal value reaching $84 bn. Last year’s Q3 saw a record $32 bn of transactions, with several billion-dollar acquisitions including Penn Virginia, WildHorse and Newfield. Deal activity slowed down in Q4 2018 as the price of oil slumped by over 40% and plunged investors into uncertainty. However, since the beginning of 2019, oil prices have stabilized and reinvigorated the appetite for consolidation. The Anadarko deal could be the start of a new wave of M&A in U.S shale oil, building on a movement started in 2018 of acquiring companies like RSP Permian and Energen, which have a strong presence in the Permian basin.

Figure 1. Sources of crude oil production in the U.S., 2000-2050 (Source: Energy Information Administration)

Shale oil, also known as tight oil, is a type of unconventional oil that lays between layers of shale rock. Oil companies must hydraulically fracture these rocks to extract the oil. As the figure 1 shows, shale oil represented only a small fraction of the US crude oil production until the 2010’s but is expected to reach two-thirds of total oil production by 2020.

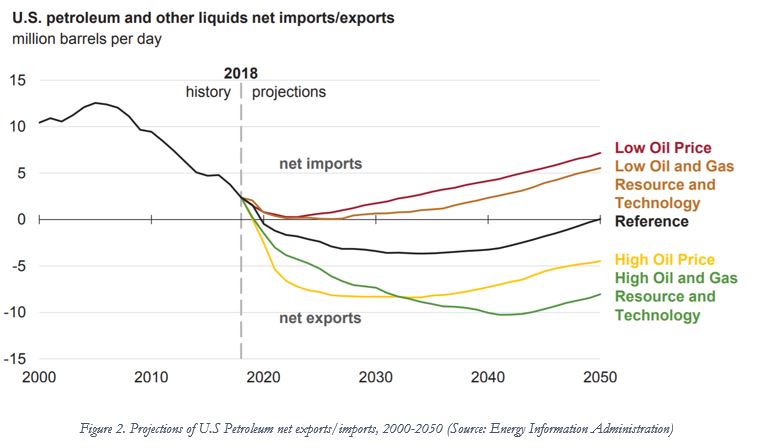

The shale boom has transformed the US into the world’s biggest producer of crude. The Energy Information Administration expects the U.S. to produce 13.2m barrels a day by 2020, shooting ahead of Russia and Saudi Arabia by a clear margin. In a stunning reversal from its past history, the U.S. is set to become a net exporter of oil and gas. Forecasts predict that these exports will continue to grow steadily, as can be observed in figure 2, provided high oil prices and sufficient technological progress.

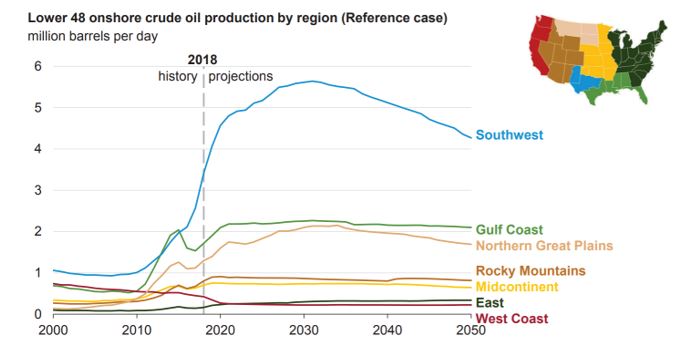

Shale oil is a key area of focus for U.S. oil companies because of its abundance, its short development cycle, and low risk profile. The Permian basin is particularly coveted. The blue line in figure 3 shows how American oil is becoming increasingly dependent on this basin, which spans about 75,000 square miles across west Texas and south-eastern New Mexico.

Figure 3. U.S. Crude Oil production by region, 2000-2050 (Source: Energy Information Administration)

The Permian basin is seeing a new era of consolidation within its fragmented landscape of shale producers as Big Oil companies try to swallow their smaller counterparts. Smaller oil companies are struggling to remain profitable as they run into the challenges of pipeline bottlenecks, more expensive labor, and rising materials costs. Their larger rivals are stepping in and remaining profitable thanks to their economies of scale and their superior financing. Indeed, oil giants see consolidation as a way to achieve better efficiency and synergies. All in all, the “bigger is better” mantra adopted by many oil producers, the solid financial health of these companies, and the fair valuations of potential targets make for a what will likely be a fertile M&A environment in the Permian Basin in 2019.

Deal Structure

On 24 April 2019, Occidental offered to acquire Anadarko in a cash-and-stock transaction. Occidental’s offer values Anadarko’s equity at $38 billion, which represents a bid premium of 62% over Anadarko’s closing share price on April 11th, the last trading day before Anadarko received Chevron’s offer. The total value of the transaction is $57 billion, including the assumption of Anadarko’s net debt and book value of non-controlling interest.

Occidental offered to pay $38 in cash and 0.6094 shares of Occidental for each share of Anadarko, which amounts to $76 per share of Anadarko. This 50-50 split between cash and stock should be more attractive to Anadarko shareholders than Chevron’s 25% cash and 75% stock offer. However, this comes at a cost to Occidental: in order to obtain the cash needed to finance the transaction, the company must take on more debt, which puts the company’s credit rating at risk. Indeed, Moody’s is reported to have put Occidental’s debt rating under review for a downgrade.

Initially, Occidental planned to sell between 10 and 15 billion dollars of assets over the next 1 to 2 years to finance the transaction. Occidental would get rid of Anadarko’s deep-water operations and its LNG project, as they have little synergies with Occidental’s existing businesses. Bank of America Corporation and Citigroup Inc. were to finance the rest of the transaction. However, six days after Occidental’s announcement, Warren Buffett offered to provide $10 billion to finance the deal. In exchange, Buffett would get $10 billion dollars in new preferred shares, which will pay an 8% dividend and a warrant to buy up to 80 million shares of common stock. Occidental’s CEO stated the company was “thrilled to have Berkshire Hathaway’s support” even though this would undeniably be an expensive source of financing for the oil firm.

The deal is not yet confirmed and is subject to approval by shareholders. Unlike Chevron, Occidental’s offer would require a shareholder vote from both the target and the acquiring companies. Occidental’s shareholders must approve the deal because the company would be issuing more than 20% of its existing number of shares in the deal. Buffett’s proposal however could allow Occidental to restructure its cash-and-stock deal in order to avoid a shareholder vote. Nevertheless, under the terms of the Anadarko-Chevron merger agreement, Anadarko would owe Chevron a break-up fee of $1 billion if it reaches a takeover deal with another company.

Deal Rationale

Earlier this month, Anadarko and the oil giant Chevron

reached a deal whereby the former committed to acquire Anadarko through cash

and stock for a total of $50bn, paying a 39% premium and thus valuing its

shares at $65.

In Chevron’s view, buying Anadarko would solidify the company’s position in the

booming shale-producing regions of southern U.S., especially in the Permian

Basin. Indeed, American oil output has more than doubled over the past decade

as a result of rapid technological advances in drilling and an increasingly

large demand driven by the late 2015 lift of the 40-year ban on exporting oil.

Moreover, Anadarko’s assets could offer Chevron the chance to enhance its

drilling operations in the Gulf of Mexico, as well as give access to an

attractive liquefied natural gas project in Mozambique.

However, Anadarko announced on the 29th of April its plans to enter

merger talks with Occidental Petroleum, which made a hostile takeover bid

valuing the company at $57bn. Occidental seeks to acquire Anadarko’s valuable

assets in the Gulf of Mexico and the Basin of Colorado, a promising project in Mozambique,

and, most importantly, a precious shale acreage in the Permian Basin of Texas

and New Mexico, the heart of the US oil boom. This transaction could

enhance Occidental’s position as the largest producer in the Permian Basin with

533,000 barrels of oil per day of production. The Permian Basin, which

stretches across West Texas into New Mexico, is the world’s most productive oil

field. Moreover, the current construction of several oil and gas pipelines

serving the Permian are expected to increase fourfold Gulf of Mexico’s oil

exports to eight million barrels a day by 2022.

Occidental, already a large producer in the Permian region, argues that, though its production expertise and with the existing infrastructure, it can save annually $3.5bn by 2021 in operating and capital costs. Indeed, the company expects to save $2bn in annual pre-tax run-rate cost synergies, and $1.5bn in capital reduction, with the potential for further upside. The combined entity is expected to produce a stronger and more competitive business, with over 1.4 million barrels of oil per day of current production. Furthermore, the deal would help Occidental Petroleum fulfill its longtime priority of increasing its dividend at the same time as reducing the burden of making those payments, though it would make the company more highly leveraged.

The Anadarko board wants to be certain that the takeover would not run into resistance due to shareholder’s disapproval. Chevron was able to provide that confidence since its stockholders are not entitled to a vote on the matter. On the contrary, at least one major Occidental shareholder, T Rowe Price, already objected the deal and shares have slid since news of interest in Anadarko was revealed. Securing shareholder approval for Occidental Petroleum may not be straightforward. However, Buffet’s capital injection could give Occidental the means to make the offer more attractive and win the backing of the Anadarko board by increasing the cash component of its bid.

Market reaction

On April 29th, the news of Anadarko entering merger talks with Occidental Petroleum triggered a fall of about 2% in Occidental’s shares, while Anadarko’s share price was unchanged. This can be understood by the events that happened before the announcement.

On April 13th, Anadarko’s shares skyrocketed following the announcement of an acquisition of Anadarko by Chevron, jumping 32% to close at $61.78 on the NYSE. However, Chevron’s shares fell 4.94% to close at $119.76 on the NYSE as investors deemed that the 39% premium on Anadarko was excessively high.

Moreover, he Chevron-Anadarko agreement became the subject of scrutiny from US regulators, with the SEC filing an order to seize assets of unnamed traders who purchased Anadarko’s call options in the weeks prior to the Chevron deal. In the lawsuit, the SEC stated that this was a case of insider trading involving one or more unknown traders who made $2.5m in illicit profits. Apparently, Anadarko calls were highly suspicious, timely, and lucrative according to the SEC and the investors placed their trades through accounts in the UK and Cyprus.

On April 29th, the news of Anadarko entering merger talks with Occidental Petroleum triggered a fall of about 2% in Occidental’s shares, while Chevron and Anadarko were unchanged.

Financial advisors

Credit Suisse Securities (USA) LLC acted as financial advisor to Chevron, while Evercore and Goldman Sachs & Co. LLC are acting as financial advisors to Anadarko. Bank of America Merrill Lynch and Citi are acting as Occidental’s financial advisors.

0 Comments