The Blackstone Group LP (NYSE: BX) – market cap as of 11/11/2016: $28.95bn

TeamHealth Holdings (NYSE: TMH) – market cap as of 11/11/2016: $3.07bn

Introduction

On the 31st of October 2016 Team Health Holdings Inc. announced that the company has reached an agreement to be acquired by a group of investors led by Blackstone Group LP for about $3.2bn, that together with debt values Team Health Holdings Inc. at $6.1bn. This transaction is the first public-to-private buyout by the firm’s private equity group since October 2013.

Private Equity industry overview

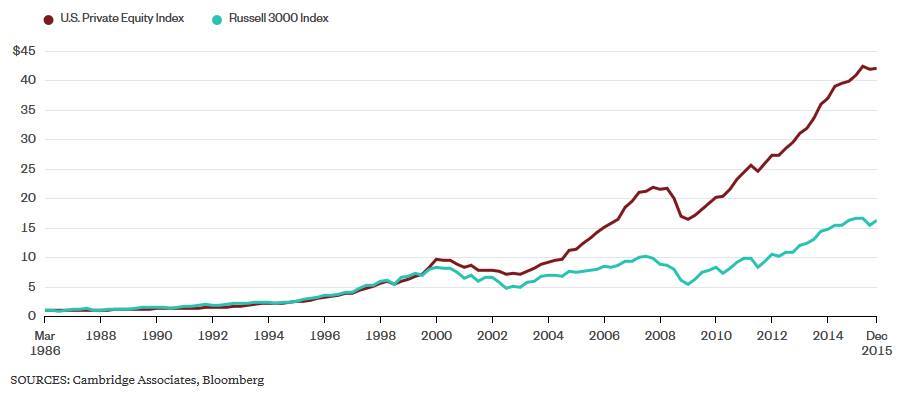

Private equity funds have historically represented some of the most profitable vehicles investors could bet on. US private equity funds have indeed steadily outperformed the American stock market (represented in the graph below by the Russel 3000 Index): PE firms have yielded an average 13.4% annual return over a 30-year period, while the US stock market has been growing at a 9.9% annual rate.

However, the current economic outlook is bringing significant challenges to the PE industry in the form of higher competition from strategic buyers and tighter regulations. Increased competition from strategic buyers comes from the fact that companies now seek high quality external growth opportunities. This drives them to identify targets with unexploited development opportunities and with steady cash flow generation, the same targets that PE funds usually invest in. The main issue for private equity firms is that corporate (strategic) buyers are willing to pay a higher premium because of the synergies they expect to generate, while PE funds cannot afford to pay the target company more than what will guarantee the achievement of the desired IRR. In this way, private equity firms are losing a lot of very good candidates to companies, leaving them with billions of “dry powder”- unspent cash (for instance, Blackstone currently has about $102bn in unspent cash, while Apollo, Carlyle Group and KKR & Co. have $117bn). As far as regulatory risk is concerned, the financial crisis has led to tighter rules regarding credit provision and this negatively impacts the private equity business model.

TeamHealth Overview

TeamHealth is a public company headquartered in Knoxville, Tennessee, that provides administrative and management services to hospitals and other healthcare providers, serving approximately 3,400 facilities and physician groups in 47 states.

Established in 1979, it is now recognized as one of the main clinical-outsourcing operators in the United States, offering a wide range of solutions for emergency medicine, hospital medicine, pediatrics, coding, collections, reimbursement, together with tele-radiology and occupational health services. This result has been achieved both through internal growth (the size of TeamHealth’s clinician community doubled in the last three years and the range of solutions provided gets wider every year) and through strategic acquisitions, such as the purchase of IPC Healthcare in November 2015.

Its businesses are aggregated in four segments: Hospital Based Services, IPC Healthcare, Specialty Services, and Other Services. The company mainly relies on Emergency Department Solutions (EDs), belonging to the Hospital Based segment. More specifically, EDs saw a revenue CAGR of 17% from 2011 to 2015. Furthermore, since the acquisition of IPC Healthcare, Acute and Post-Acute Care facilities acquired a significant strategic relevance.

The company is currently focusing on the development of an excellent team of more than 19,000 affiliated physicians, striving to lead innovation in the clinical-outsourcing sector. Moreover, one of TeamHealth’s strategic imperatives in the latest annual report deals with the generation of strong operating cash flows – a core prerequisite for an LBO candidate.

On a full-year basis, TeamHealth reported about $6bn revenues in 2015, a 25% increase compared to revenues in 2014. The company’s core business, Hospital Based Services, generated $3.2bn net revenues in FY2015. The reported operating income was $149.56m, while net income was $82.75m, both slightly declining because of the expensive acquisition of IPC.

Deal structure

The PE fund is going to pay $43.5 per share for all TeamHealth’s diluted shares outstanding, equal to $3.2bn equity value. Blackstone is paying a 33% premium on the stock’s closing price on the day prior to the announcement that the two companies were in talks for a possible buyout. The total enterprise value amounts to $6.1bn, including the existing debt of $2.77bn.

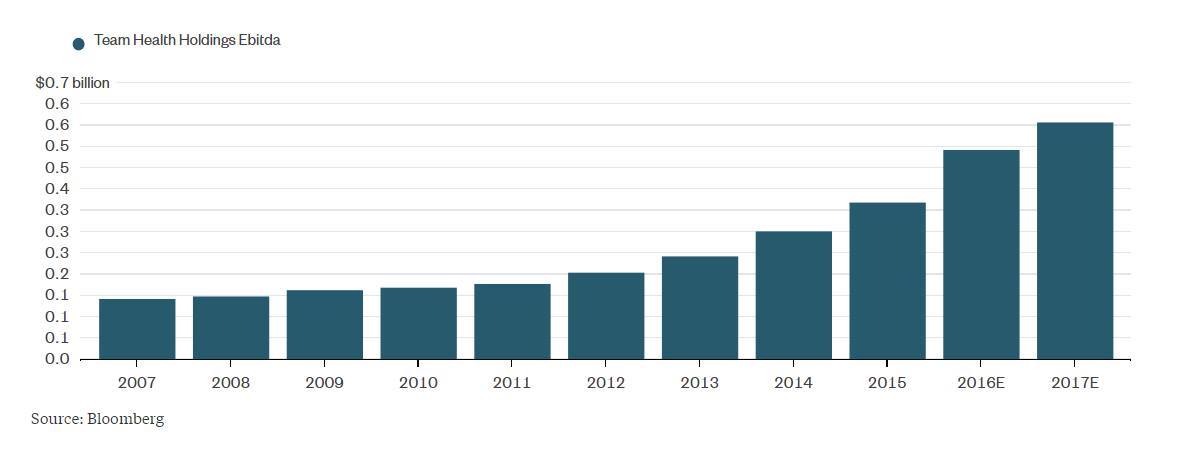

Blackstone will most likely complete the transaction through its Diversified Multi-Strategy Fund (BXDMS) as it already had over 6000 shares in TeamHealth at the end of 2015. While most of the information about the deal structure is kept private, we can make some assumptions. PE firms have historically sought 20%+ IRRs when assessing acquisition opportunities and this correlates with the financing structure and purchase price. The purchase EV/EBITDA multiple that Blackstone agreed on was about 14x LTM EBITDA. Generally, PE firms are looking to sell the company after 3-5 years. TeamHealth’s historical and expected EBITDA growth can be observed on the graph below.

If the target IRR that Blackstone is looking to accomplish is about 20%, and they sell the company after 4 years (like the first time they purchased TeamHealth), we can guess that the financial structure is about 20-30% cash on hand and 70-80% new debt. These figures may vary vastly depending on what exit multiple Blackstone achieves, as well as how conservative the assumptions are.

Strategic rationale

Last year, TeamHealth was approached by surgery centers operational manager – AmSurg – but the company withdrew from the deal after TeamHealth said that the offer valuing its equity at around $5bn was too low.

Afterwards, AmSurg moved towards acquiring Envision Healthcare, leaving TeamHealth with limited possibilities to benefit from the consolidation wave in the industry. This wave, which is persisting in 2016, is fueled not only by the strong deal-making activity in the health-care sector in recent years, but also by the new tightening rules increasing administrative costs, which derived from Obama’s Affordable Care Act.

A deal with Blackstone seems to be the perfect way for TeamHealth to survive in this extremely competitive and ever-changing environment. Blackstone has some experience in the company, as it bought TeamHealth in 2005 for $1bn and eventually took it public in 2009. Thanks to the acquisition, TeamHealth will be able to increase its market share in the fragmented clinical-outsourcing sector and to finalize its integration of IPC privately.

Blackstone owns healthcare businesses such as HealthMarkets Inc., operating in the medical insurance field, thus the private equity giant could potentially generate synergies between these businesses or, at least, share critical know-how and improve companies’ efficiency and services quality.

From an investor’s point of view, the offer is not that exciting, as it represents a 37% discount to AmSurg’s one. On the other hand, it is unlikely that other bids will match AmSurg’s offer because of the significant amount of debt TeamHealth is carrying (its net debt is approximately equal to 4.7x. FY2016 pro-forma EBITDA).

It is interesting to notice that, despite the low purchase price offered, Blackstone’s bid has been endorsed by Jana Partners (the hedge fund which recently disclosed an 8% stake in TeamHealth): the support from such a powerful activist investor can be a positive signal for the market, making TeamHealth’s odds brighter in terms of future bid proposals.

While Blackstone had opted for the IPO as its exit strategy in 2009, it might choose another type of exit for TeamhHealth in the near future. It is indeed likely that AmSurg will try to buy TeamHealth again in a couple years, especially if the company strengthens its performance and the new CEO meets expectations. Reaching the desired targets both in terms of operating and financial performance will imply greater returns for Blackstone and other investors.

Market reaction

Investors reacted positively to the announcement that TeamHealth was in talks for a possible sale to Blackstone. Indeed, the share price jumped 16.5% to $38.2 per share on October 4. When the deal was officially announced on the October the 31st, TeamHealth’s share price rose further by 16.4% aligning with the purchase price offered by Blackstone.

Advisers

TeamHealth is being advised by Goldman Sachs and Citi, while BofA Merrill Lynch is advising Blackstone.

[edmc id= 4328]Download as PDF[/edmc]

0 Comments