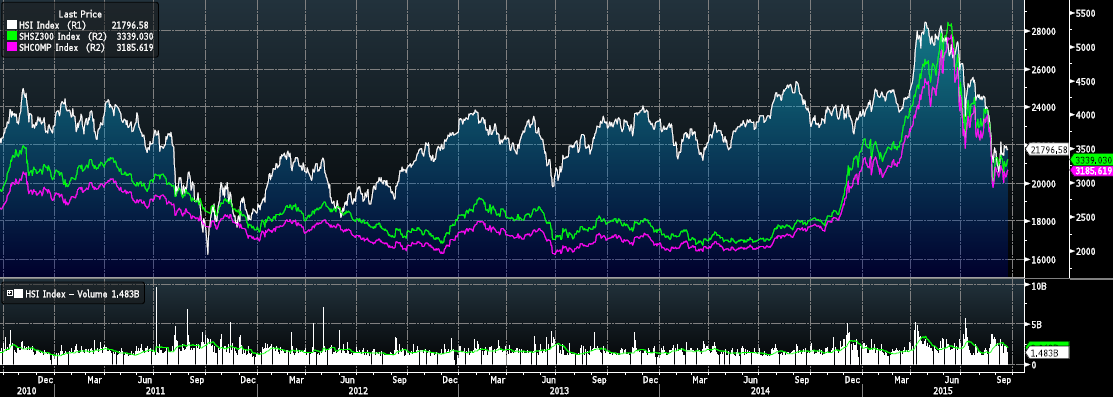

In our May article (https://bsic.it/chinese-divergence-real-vs-financial/), we underlined how many difficulties China faced. We also analysed the development of a stock market bubble in the Shanghai Composite equity index (SHCOMP) and in the Shenzhen CSI 300 (SHSZ300) equity index. This summer saw that bubble bursting. The SHCOMP was trading at 3,185 as of September 22nd, a drop of around 40% from its high of 5,200 in early June. The Shenzhen CSI 300 dropped around 40% to 3,339 as of September 22nd.

Source: Bloomberg

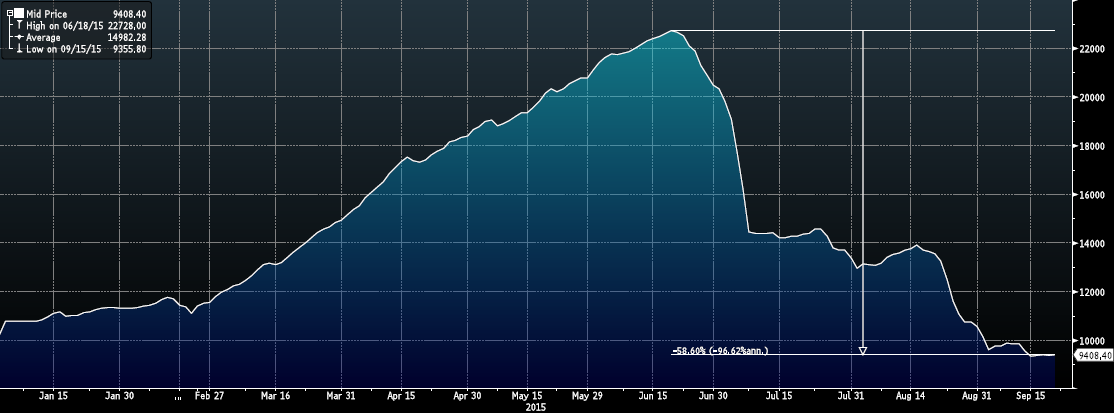

As we projected in May, the SHCOMP further gained until mid-June, inflated by rising margin trading and speculation about a continued support by the Chinese authorities. Afterwards, the stock market frenzy driven by retail investors buying stocks on the margin has reversed sharply, amid fears of a worse than expected economic slowdown in the Chinese economy. The total outstanding balance of margin transactions as reported by Bloomberg has decreased by 60% from its high registered in mid-June, coming back to levels registered back in 2014. This means that retail investors have hastily unwound margin trades amid widespread panic in the Chinese stock market.

China Margin Trading – Total Outstanding Balance of Margin Transactions – Source: Bloomberg

The situation got worse when the Chinese authorities started acting in order to artificially prop up stock prices. Among other measures, authorities obliged investors who short-sold securities to buy them back. However, investors lost confidence in the ability of the Chinese authorities to support the stock market. Therefore, after a slight rebound in July, both the SHCOMP and SHSZ300 dropped in August. On Monday 24th August, the infamous “Black Monday”, the SHCOMP fell as much as 8.5% in one day, triggering sharp declines in global stock markets. On Tuesday, the PBoC decided to cut the one-year benchmark lending rate 25bps to 4.6% and the Required Reserve Ratio (RRR) for large banks 50bps to 18%, effective September 6th. This move was intended to support the economy and stop the stock market rout. However, the SHCOMP lost again more than 7.5% in a single day.

Two weeks earlier, the PBoC decided to decrease the band within which the renminbi (CNY) is allowed to trade against the dollar (USD). The so-called daily fix was lowered in a single day by 1.9% and in the next days by another 2%. Furthermore, the way the daily fix is determined has been shifted from being set daily by the PBoC to being based on “the closing rate of the interbank foreign exchange market on the previous day” (Financial Times). As Chinese PM Xi recently confirmed, China does not intend to use competitive devaluations to support its trade, claiming that the move was intended to bring the CNY to a level that reflects its real value.

CNYUSD X-Rate – Source: Bloomberg

However, we view this move as a mean to support the waning exports and, in general, the competitiveness of the Chinese economy in a moment when other measures do not seem to be effective. Trade volumes decreased significantly, with the trade surplus increasing only because imports were down more than exports, especially due to the slowing demand growth for imported commodities such as crude oil, copper and iron ore. In August, imports fell 14.3% YOY in CNY terms, the 10th consecutive monthly decline as reported by the Financial Times. Exports were down 6.1% YOY in August.

This had deep consequences on global markets. Commodities have been negatively affected by this further slowdown in Chinese activities. After a slight rebound up to $60/barrel until the end of June, the WTI benchmark dropped again in July and August, reaching a low of $38/barrel in August. Now, it has recovered some of the lost ground and it is up again to $45/barrel, bringing the annual decrease in price to 49.34%. Copper dropped 24.37% in the last year and the pace of the fall increased after May. China is one of the biggest importers of commodities in the world and the drop in Chinese demand deeply and negatively affect prices of all industrial commodities.

An interesting graph explaining the effect of the recent bubble and burst on the Chinese stock market is represented by the AH premium index. This shows the spread between the A-shares of companies listed on the mainland Chinese stock exchanges (Shanghai and Shenzhen) and the H-shares of the same companies listed on the Hong Kong Hang Seng index (HSI). When the index trades at 100, it means that A-shares are trading on average at par with their respective H-shares. We can clearly see that this spread skyrocketed during this year’s bubble, leaving its 5-year trend of average parity. This represents a further proof of overvaluation in mainland Chinese equity markets relative to the HSI. Despite this summer drop in both SHCOMP and SHSZ300, the AH premium index remains at historical highs due to an accompanying decrease in the level of the HSI.

AH Premium Index – Source: Bloomberg (see first chart)

Looking at the current environment, we see a prolonged period of weakness in both the Chinese stock markets and economy. We want to take a position in order to exploit our views on the relative performances of the SHCOMP and SHSZ300 with regards to the HSI. If we consider the AH Premium Index chart, we see that on average the spread between the A-shares and the H-shares has been null. The only exception was back in 2011, when HSI overreacted to poor economic data from China and US. Nevertheless, the overreaction was then strongly corrected and the spread returned to historical levels close to 100 on average. Now, as we underlined before, the spread widened due to the recent bubble in China. We expect that the AH premium will reduce to historical levels. Therefore, we want to bet on the narrowing of this spread by shorting futures on A-shares (SHCOMP and SHSZ300 as proxies) and going long futures on H-shares (HSI). Since the A-shares and H-shares represent two different claims on the cash flows of the same companies, the current premium valuation of A-shares over H-shares does not seem justified.

[edmc id= 2846]Download as PDF[/edmc]

0 Comments