In this article we analyze the so called “sector rotation”, which can be seen in the US stock market since the second half of 2018 and we try to exploit this phenomenon by identifying some interesting investment opportunities in the undervalued sectors. More specifically, in the first part of the article we give some basic information explaining what sector rotation is and why it is happening now in the market. In the second part we compute some indicators showing the presence and the magnitude of sector rotation in the US stock market. Finally, in the third part we try to identify within the cyclical sectors some stocks that have been particularly penalized by the rotation and seem to be good investment opportunities.

Part 1: What Is Sector Rotation and Why It Is Happening in the Market

In general, sector rotation consists in switching the portfolio exposure from some sectors of the economy to others. There are quite complex investment strategies based on different schemes of sector rotation (see for instance Chong and Phillips (2015) and Sassetti and Tani (2006)). However, most of the times sector rotation refers to the increase and reduction of the exposure towards cyclical and non-cyclical (also called defensive) sectors.

Defensive sectors represent those segments of the economy which are quite stable regardless of the stage of the business cycle you are in. Consequently, they are very little correlated with the overall growth of the economy. Two examples of those are health-care and utilities. In fact, since the demand for drugs and power is usually quite stable and not very elastic with respect to income, companies that operate in these sectors tend to have not too bad results during recessions and quite stable results during expansions. On the contrary, cyclical sectors are the segments more exposed to the trend of the economy. Indeed, sectors such as financials and consumer discretionary typically have very good performance if the economy does well but they perform really poorly during recessions. Therefore, the rationale of sector rotation is the following: when growth estimates are strong, investors should tilt their portfolios towards cyclical sectors in order to maximize the benefit of economic growth; otherwise, if investors fear an economic slowdown or even a possible recession they should increase the exposure to defensive sectors in order to limit the losses and to reduce the volatility of their investments.

The US stock market is experiencing its longest bull market since World War II. In fact, it didn’t have a 20% or more decline since March 9, 2009 and in the meantime it has risen more than 300%. Since valuations have become so high, now investors are paying lot of attention to possible threats that could potentially put an end to the positive trend of the last years. In this respect, the Quantitative Easing of the FED that pushed up the stock market after the recession of 2008 has finally come to an end and interest rates have already started to rise. Furthermore, the growth estimates for the world economy are not so bright and the deep tensions between China and USA regarding trade policies could even worsen the forecasts. Indeed, recently investors tend to overreact to bad news that arrive into the market because they fear the beginning of a market correction, which would make the current high valuations unsustainable in the future. A very clear example of this phenomenon is the recent drop of the S&P500 due mainly to some disappointing quarterly results of a few companies.

Therefore, since investors are worried about a slowdown of the economy and the beginning of a correction in the stock market, exploiting the logic of sector rotation we described above, they are tilting their exposure from cyclical sector towards defensive ones. In fact, as we will show in Part 2, stocks belonging to cyclical sector like Information & Technology, Financials and Materials experienced much bigger slumps than stocks in defensive sectors.

Part 2: Showing Signs of Sector Rotation in the Market

In order to differentiate between cyclical and defensive sectors we need at first an industry classification. In particular, we used the so called Global Industry Classification Standard (GICS), which is an industry arrangement that divide the entire economy in 11 sectors, 24 industry group, 68 industries and 157 sub-industries. It is used as a standard classification method to categorize companies within the US stock market. Out of the 11 sectors of GICS we considered 6 sectors in which the cyclicality is more evident, and we divided them in cyclical and defensive according to the subdivision made in the MSCI Cyclical and Defensive Sectors Indices. Specifically, for cyclical sectors we considered:

- Financials

- Industrials

- Materials

While for the defensive sectors we take into account:

- Health care

- Utilities

- Consumer staples

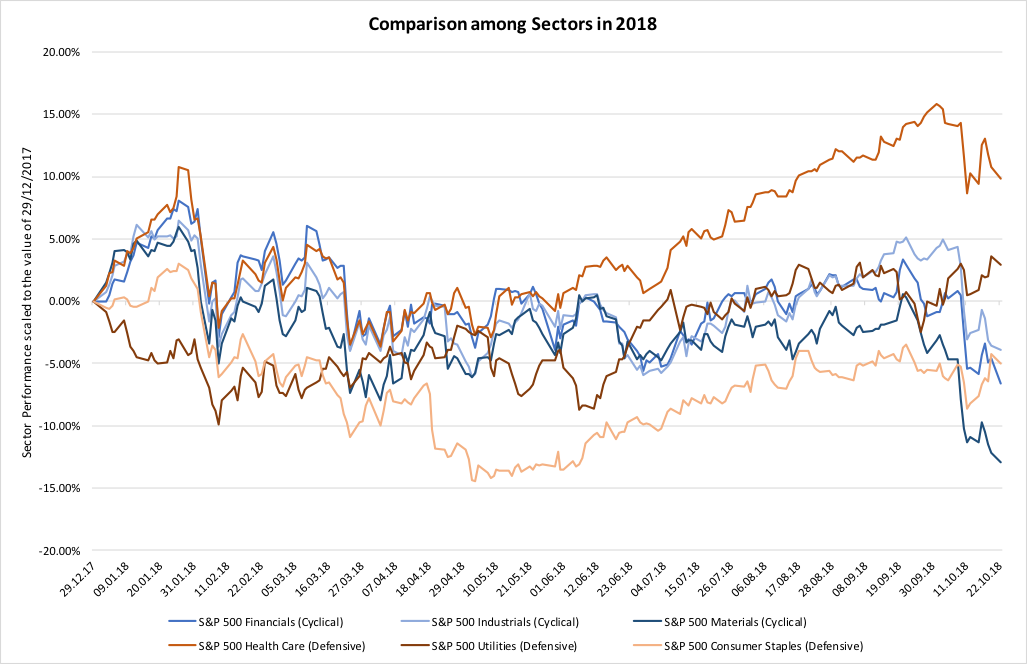

The performance of the corresponding S&P 500 Sector Indices in 2018 is plotted in the graph below (we scaled the data based on the values of December 29, 2017 in order to make the comparison easier):

Source: S&P Dow Jones Indices (Data last updated on 22.10.2018)

As you can see, on average defensive sectors showed better results than cyclical ones in 2018. More interestingly, you can observe that the 6 sectors considered appeared to be quite correlated in the first part of the year while since around the half of 2018, cyclical and defensive started to diverge.

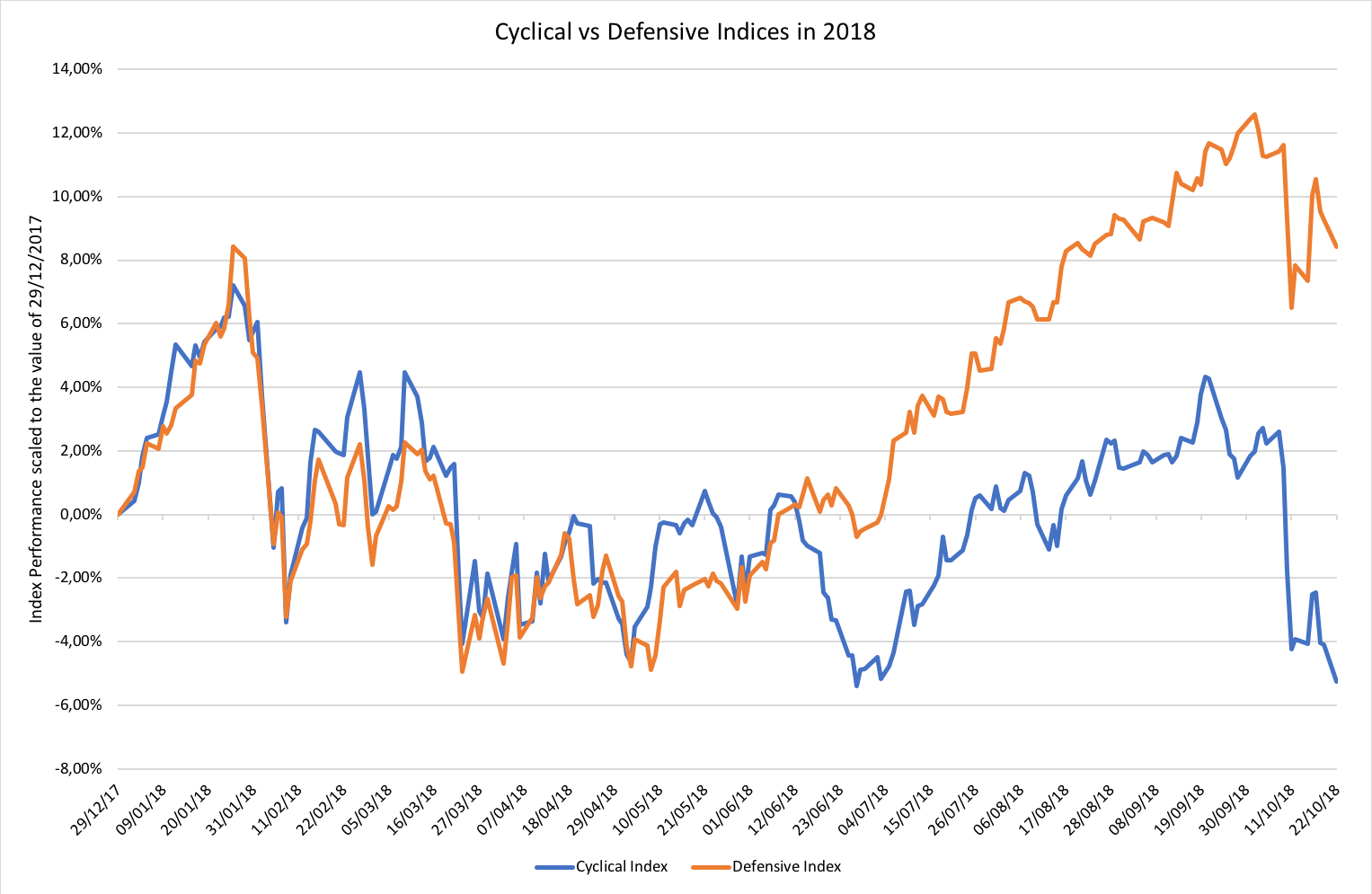

In order to show the evolution of the correlation between cyclical and defensive sectors more clearly, we computed two indices based on the sectors we chose before, representing respectively cyclical and defensive. More precisely, the values of our cyclical and defensive indices have been computed on the basis of the corresponding values of S&P Sector Indices, weighted using the weight of each sector on the S&P 500. In particular, the weight of the i-th sector, for the day t of the period considered, has been computed as follows:

where the weight on S&P500 of cyclical and defensive sectors are simply the sum of the weights on S&P500 respectively of the 3 cyclical and 3 defensive sectors considered. Since the S&P500 is a value weighted index, the weight scheme we followed is equivalent to weighting each sector proportionally to its capitalization.

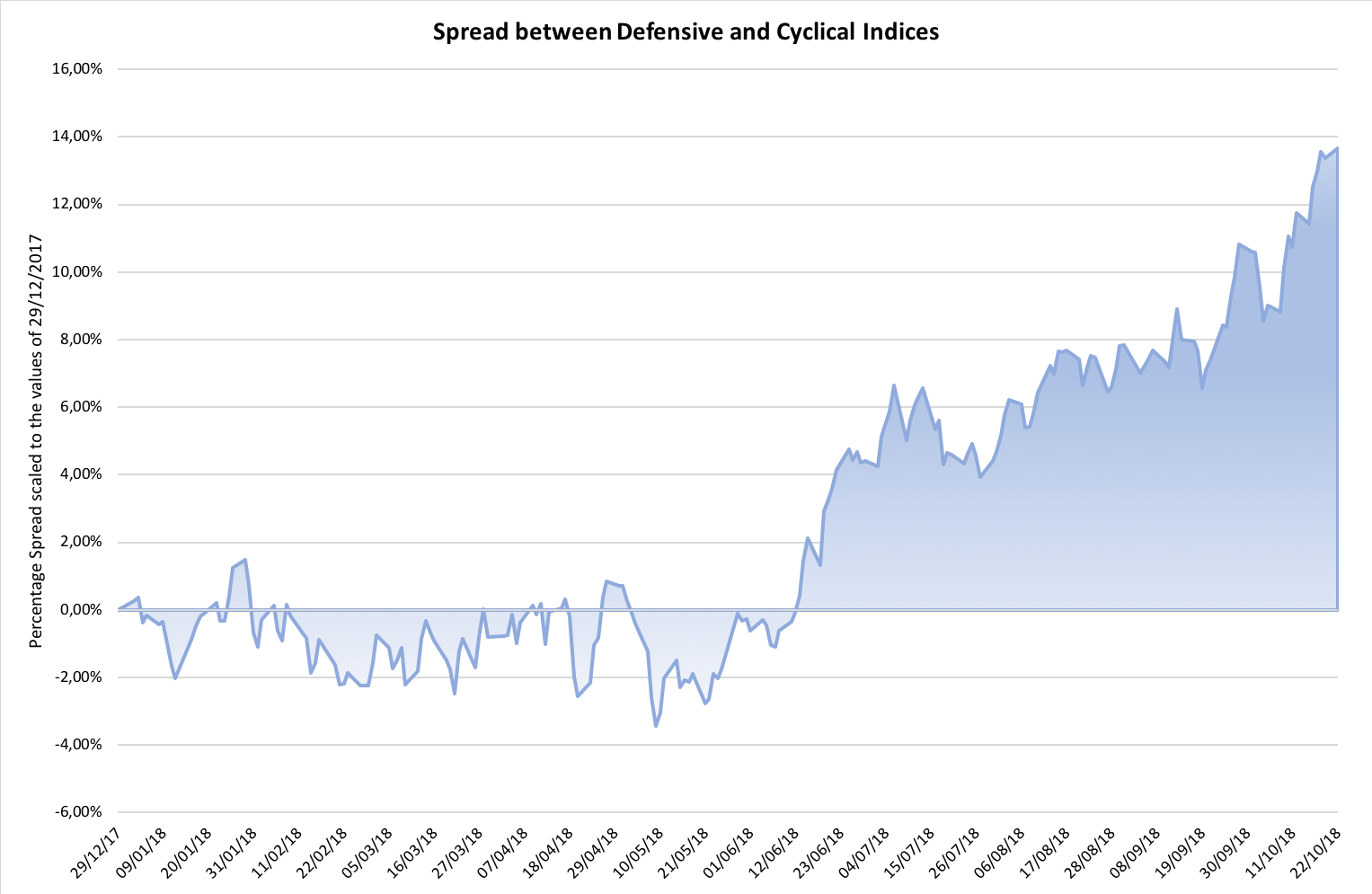

The resulting values of our indices and the corresponding percentage spread between defensive and cyclical are the following (we scaled the data based on the values of December 29, 2017 in order to make the comparison easier):

Source: S&P Dow Jones Indices (Data last updated on 22.10.2018)

Source: S&P Dow Jones Indices (Data last updated on 22.10.2018)

As you can see in the graphs above, the evolution of the two indices is very similar up to the half of the year and then they started to diverge with defensive stocks outperforming the cyclical ones and the spread between them increasing by almost 14%.

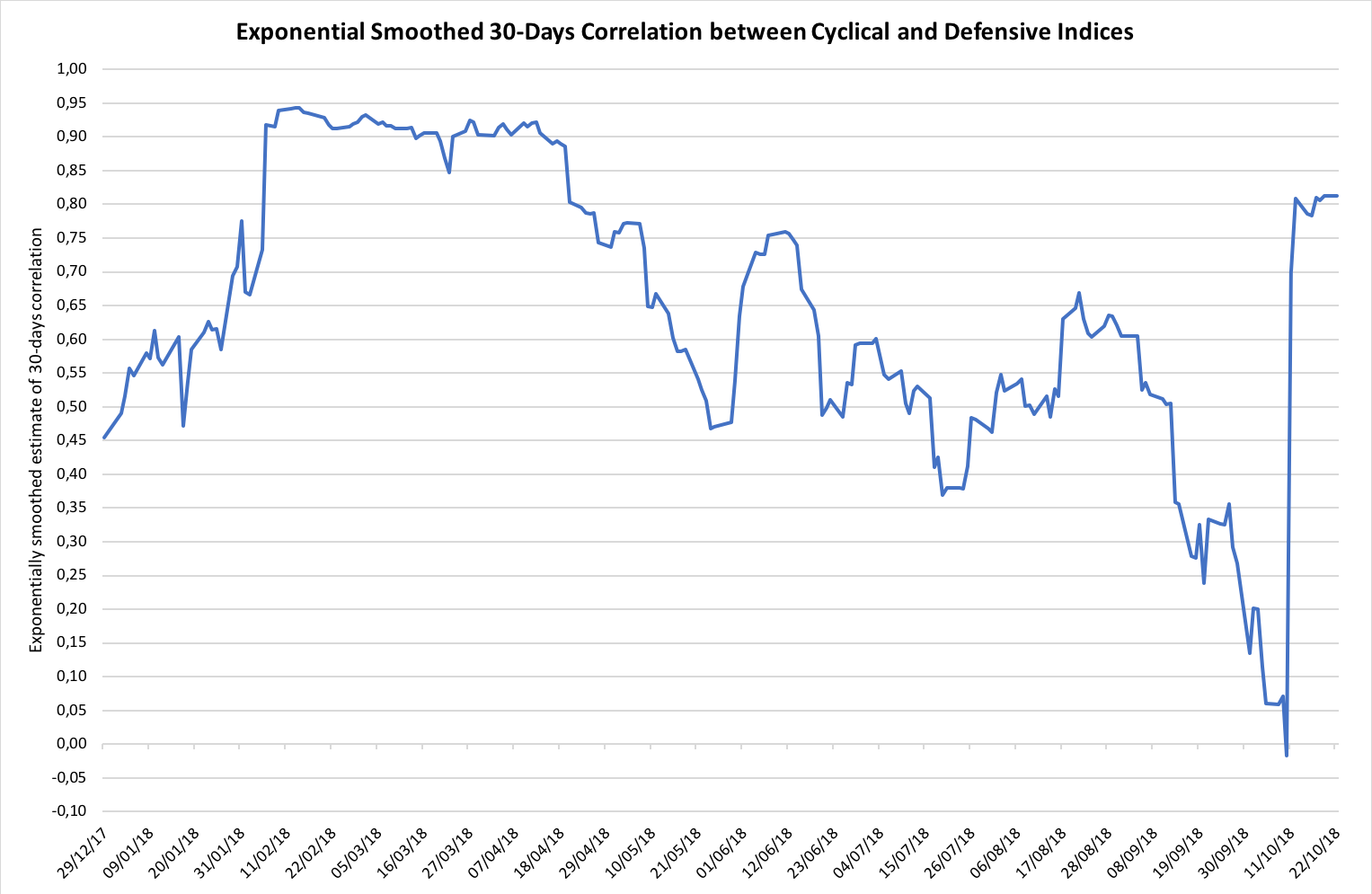

Finally, we computed the correlation between our cyclical and defensive indices. In particular, we computed an exponentially smoothed estimate of the correlation between log returns of cyclical and defensive indices, using a time window of 30 trading days and a smoothing parameter of 0.94. Indeed, we used the following formula:

![Cor_t=\dfrac{\sum_{i=0}^{30}\lambda^ir_{t-i}^{cyclical}r_{t-i}^{defensive}}{\left[\sum_{i=0}^{30}\lambda^i\left(r_{t-i}^{cyclical}\right)^2\right] \left[\sum_{i=0}^{30}\lambda^i\left(r_{t-i}^{defensive}\right)^2\right]}](https://bsic.it/wp-content/ql-cache/quicklatex.com-3096cb871204707fdbe934ec5d69fde7_l3.png "Rendered by QuickLaTeX.com")

where  and

and  are the log returns of the cyclical and defensive indices at time t-i, and λ is the smoothing parameter that we put equal to 0.94.

are the log returns of the cyclical and defensive indices at time t-i, and λ is the smoothing parameter that we put equal to 0.94.

The resulting values for the exponential smoothed 30-days correlation in 2018 are plotted in the following graph:

Source: S&P Dow Jones Indices (Data last updated on 22.10.2018)

As you can see correlation was very high at the beginning of the year, touching peaks of almost 0.95 but then it decreased through the year reaching a minimum slightly below zero on October 10, 2018. However, in the last few days, correlation grew sharply but this could be justified by the recent sell-off in the US stock market. In fact, when such drops happen, investors lose confidence, volatility spikes and correlation among all asset class tend to raise as well. Therefore, the analysis of correlation between cyclical and defensive sectors confirms that investors are tilting their portfolio towards defensive stocks, reducing the exposure to cyclical ones.

Part 3: Exploiting sector rotation

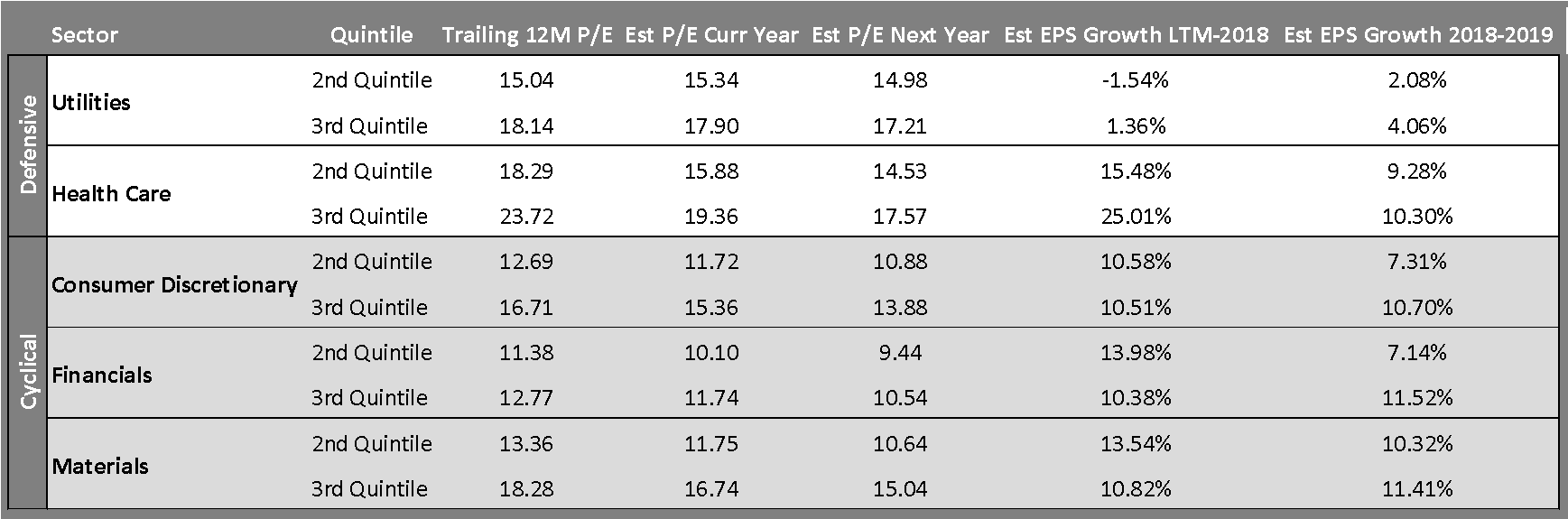

Investors seem to be overreacting to bad news arriving in the market because of the current high valuations coming from the long bull market. As we showed in the previous part, one reaction of investors has been sector rotation. Therefore, we can try to exploit this phenomenon by identifying stocks within cyclical sectors that have been particularly penalized by the rotation but have quite strong fundamentals and growth estimates. Indeed, these stocks appear to be undervalued and they represent a good investment opportunity to an investor with a long enough time horizon. In order to identify such stocks, we considered the Price/Earning (PE) ratio and the growth estimates of earning per share for this year and the next one. In particular, we computed the quintiles for the PE of all companies in each of the 11 GICS sector and we found that the most evident discrepancies between cyclical and defensive are in the middle of the distribution, more precisely in the 2nd and 3rd quintiles. The most relevant results of this analysis are summarized in the table below:

Source: Bloomberg (Data last updated on 25.10.2018)

As you can see, cyclical sectors show lower prices compared to their earnings although earnings growth estimates are not lower (actually they are even higher in some cases) than those of defensive sectors.

At this point we used together with PE and growth estimates other indicators as Price to Book Value, profitability and solvency ratios in order to select single stocks within cyclical sectors that appear to be undervalued with respect to their fundamentals. We identified 4 stocks that could represent interesting investment opportunities: two are in the consumer discretionary sector, one in financials and one in the industrials. Now we are going to give some information about each one of them.

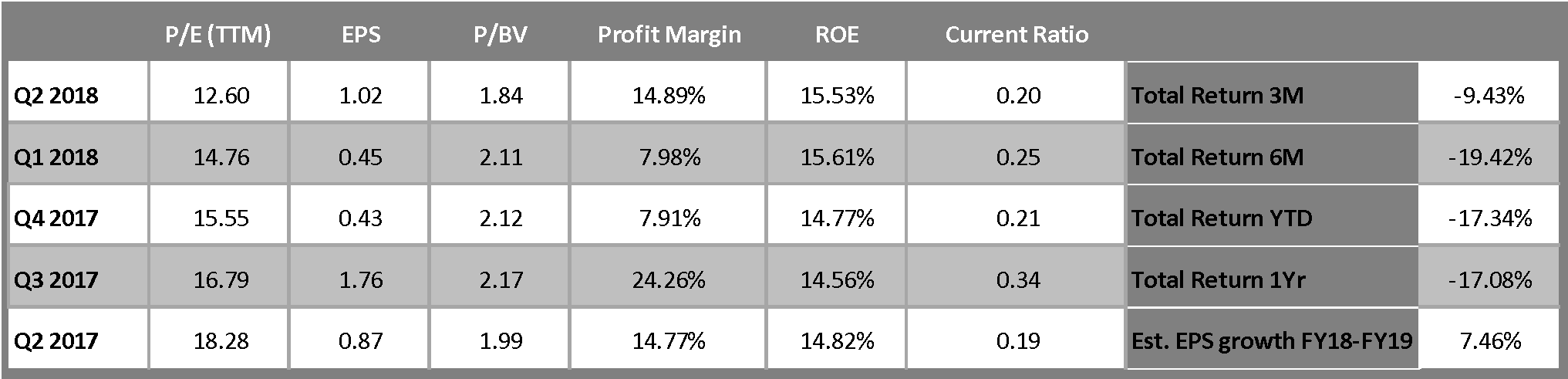

1) Norwegian Cruise Line Holdings Ltd (NYSE:NCLH) – Consumer Discretionary

Norwegian Cruise Line Holdings Ltd is a global cruise company that operates the Norwegian Cruise Line, Oceania Cruises and Regent Seven Seas Cruises brands. With its combined fleet of 26 ships, which encompasses around 54,400 berths, the company travels to 450 destinations worldwide. For Q3 2018, the company reported $5.84bn in revenue which represented a 5.8% YoY increase, beating analysts’ forecasts collected by Thomson Reuters. Net Income rose 28.4% YoY to 1.7bn. The strong performance resulted from a combination of a strong booking environment from NCLH core source markets and the successful implementation of strategies that fitted the customer demand for freedom and flexibility in designing their ideal cruise vacation. Another key driver for earnings was NCLH ability to increase prices which can be seen from the jump in profit margin for the third quarter 2018. However, NCLH stock hit a new 52-week low of $45.02 on October 25th. The sharp price decline mirrored concerns of rising fuel prices and a strengthening dollar that would weigh negative on NCLH earnings. Nevertheless, for FY 2018 NCLH is expected to generate record earnings and growth projections are positive, stemming from a continuing strong demand environment and the solid organic growth of NCLH, e.g. the record-breaking introduction of its new cruise ship Norwegian Bliss in 2018. Looking at the current relatively cheap valuation of NCLH we perceive the stock as an attractive investment opportunity.

Sources: Bloomberg, Thomson Reuters (Data last updated on 25.10.2018)

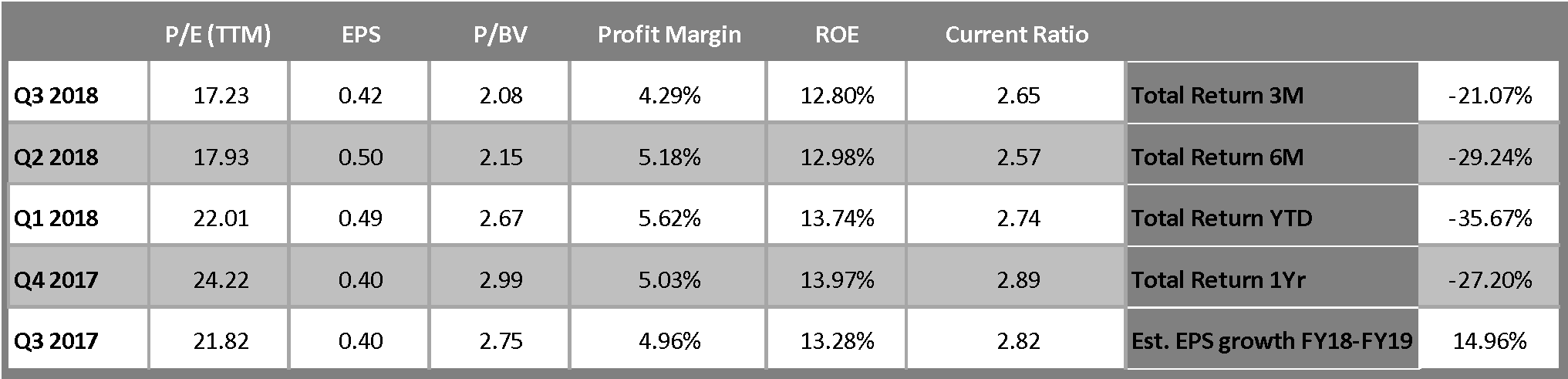

2) LKQ Corporation (NASDAQ: LKQ) – Consumer Discretionary

LKQ Corporation is a leading provider of alternative and specialty parts to repair and accessorize automobiles and other vehicles. LKQ operates in 1,100 locations in North America, Europe and Taiwan where it employs 40,000 people. During Thursday trading session (October 25th) the stock reached a new 52-week low at $23.35. The sharp decline in LKQ share price (-35.67% YTD) reflects investor’s concerns about economic headwinds stemming from freight, fuel and wage inflation. Considering these issues, LKQ guided EPS for FY 2018 lower in their Q3 report, down from a range of $2.25-$2.33 to $2.19-$2.25. However, LKQ is continuously expanding and has projected organic revenue growth in its parts & services business of 4.5-5% for 2018. The company’s margin, which proved to be stable in past quarters, are subject to expansion if the company can leverage its strong organic growth profile. Europe is going to be a key driver in the process of expanding LKQ margin, as the company shows progress in closing the margin gap between the continent vs. North America. To further enhance stockholder value, the company announced on October 25th a $500 million stock repurchase program. Moody’s already stated that this will leave the company’s rating unaffected. Technical indicators, such as the relative strength index which is at 28, indicate that the stock may be oversold. The stock price currently trades at a 38% discount to the Bloomberg consensus one-year target price.

Sources: Bloomberg, Thomson Reuters (Data last updated on 25.10.2018)

Other companies in the Consumer Discretionary industry that show attractive valuations are Royal Caribbean Cruises Ltd, eBay Inc, Wynn Resorts Ltd, Leggett & Platt Inc and Expedia Group Inc

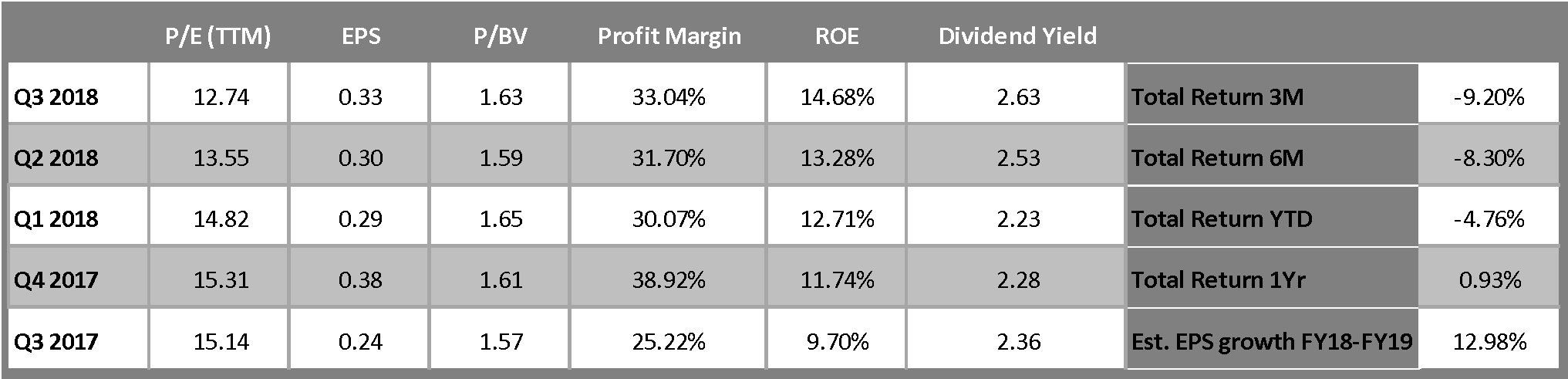

3) Huntington Brancshares Inc (NASDAQ:HBAN) – Financials

Huntington Brancshares Inc operates as holding company for the Huntington National Bank that provides commercial, small business, consumer, and mortgage banking services. The bank has $106 billion of assets and a network of 970 branches and 1,860 ATMs across eight Midwestern states in the U.S. Huntington recently announced its plans to close 70 branches of its network which will cost about $40 million in the fourth quarter and a reposition of $1.1 billion in securities, resulting in a charge of $20 million. The actions are projected to lead to an increase of $13 million in income in 2019 and years after. The actions are part of the Bank’s plan to transform its operations into a more tech-focused bank. 63% of Huntington’s customers are already engaged in its digital platforms and with additional products and services to be offered, this number is very likely to rise. Enhancements will include new interactive services, such as proactive security alerts and additions to the digital hub that will allow customers to interact with Huntington easier and more convenient. Huntington’s reported EPS for the third quarter 2018 ($0.33) beat average analysts estimates ($0.32) its reported net interest margin (3.32%) was in line with the estimated range of 3.31-3.35%. Thus far, the market is quite reluctant for acknowledging the positive prospects of Huntington. The stock declined 6.92% in price this year, compared with a decline of 1.8% in the 3000 Russell Financial Services Index. Shares of Huntington trade at a 21% discount to the analysts’ consensus target price; however, this may change, given a recent trend of buy recommendations (14 buys, 11 holds, 0 sell – Bloomberg data).

Sources: Bloomberg, Thomson Reuters (Data last updated on 25.10.2018)

Our analysis also revealed the following financial stocks as lucrative investment opportunities: Citizens Financial Group Inc, Citigroup Inc, Wells Fargo & Co, American International Group Inc.

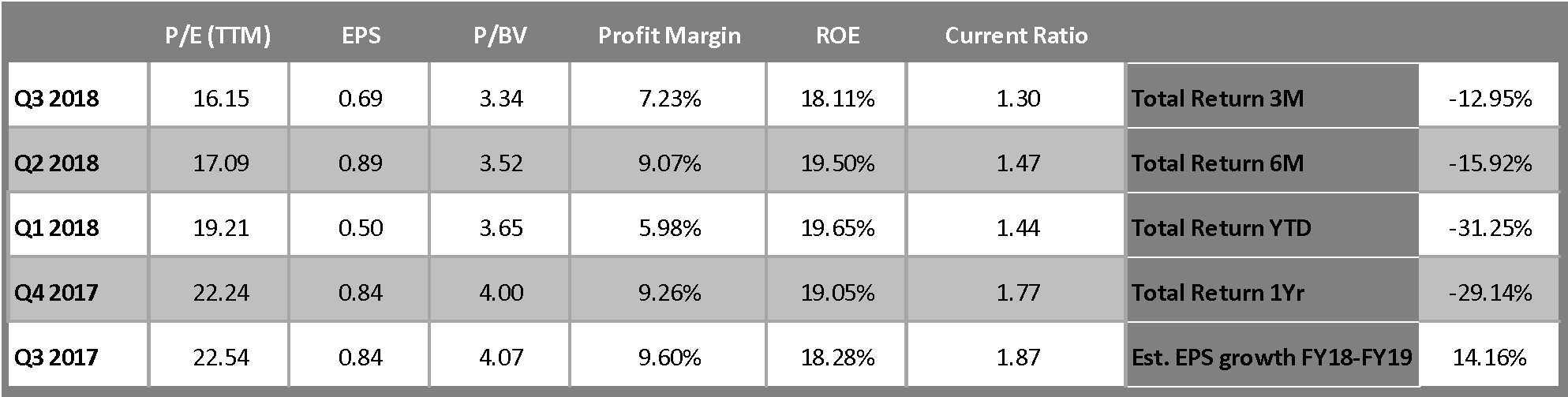

4) Fortunes Brands Homes and Security Inc (NYSE:FBHS) – Industrials

Fortune Brands Home and Security Inc provides home and security products for residential home repair, remodeling, new construction, and security applications. In all its operating segments (Plumbing, Cabinets, and Doors & Securities), Fortune Brands holds market leadership. Fortune Brands experienced a tough year so far. On Thursday, October 25th, the company reported Q3 2018 EPS ($0.69) that were 17% below the prior-year quarter. With both reported EPS and sales well below estimates and with lower adjusted guidance, Fortunes Brands stock traded at a new 52-week low on Thursday. However, the disappointing results are primarily due to one-time events. EPS before charges/gains was actually up 12% at $0.93 for the third quarter 2018. The charges resulted from a shut-down of a manufacturing plant in June. In addition, Hurricane Florence had an estimated negative effect of 7 cent on EPS, of which most will be recovered in the fourth quarter. By closing down the Fiberon acquisition, Fortunes Brands entered the high growth outdoor living category. Given the negative effects of one-time events, the solid growth prospectives – even in times of slower growing US and Canadian housing markets – and its currently attractive valuation (25% below the Bloomberg consensus one-year target price), we see Fortunes Brands as an attractive investment.

Sources: Bloomberg, Thomson Reuters (Data last updated on 25.10.2018)

0 Comments