Introduction

On 22nd February, the merger between Lucid Motors, an electric vehicle producer, and Churchill Capital IV Corp., a special purpose acquisition company, was announced. With a pro forma valuation of $24bn, this deal is the largest merger between an EV company and SPAC so far. In the past year alone, reverse mergers with SPACs have taken public electric vehicle makers Nikola, Lordstown Motors, Fisker, Canoo, and Arrival, as well as charging infrastructure companies such as EVgo and ChargePoint. Lucid Motors continues the trend of electric vehicle producers going public without any actual revenue or production. Even though Lucid, along with its peers, has attracted such a lofty valuation, it remains to be seen whether the company will be able to live up to its investors’ expectations and prove itself as an established car-makers.

About Lucid Motors

Founded in 2007 by Bernard Tse and Sam Weng, Lucid Motors started by building batteries and powertrains for other vehicle manufacturers under the name of Atieva. In October 2016, after hiring ex-Tesla and Mazda executives, the company changed its name to Lucid Motors and announced its pivot to the electric vehicle production business. A prototype of its first car, Lucid Air, was presented in December 2016, though its production has not started yet and is expected to begin in 2021. In 2019, Lucid Motors closed a $1.3bn round of funding for a huge 67% stake of the company from the Public Investment Fund of Saudi Arabia and initiated the first phase of construction of its manufacturing plant in Casa Grande, Arizona. Over the four construction phases, Lucid Motors expects to increase the production capacity of the plant from 34,000 to 365,000 cars per year. The manufacturing of Lucid Motors’ second product, which was announced under the name of “Project Gravity”, is expected to take off in 2023.

The market for electric cars has become crowded, with many companies having gone public and others raising significant financing while being private. This, it is becoming increasingly important for every EV maker to differentiate its products not only from conventional manufacturers but also from electric competitors. Lucid Motors has four primary areas of differentiation: post-luxury positioning, more efficient batteries, in-house developed powertrain, and a partnership with Electrify America.

Lucid claims that long-established luxury brands in the automotive industry, such as BMW, Audi, and Mercedes, do not appeal to the modern generation that highly ranks technology and sustainability. On the other hand, Tesla, which was the first to combine technology and sustainability in a car, is not true luxury according to Lucid’s management. Lucid’s post-luxury positioning is reflected in its expected price, with prices ranging from $69,900 for the basic Pure model to $161,500 for the all-inclusive Dream Edition model. In comparison to similar Tesla’s Model 3, which starting price points range from $37,790 to $54,990, Lucid’s cars are indeed going to be priced much higher.

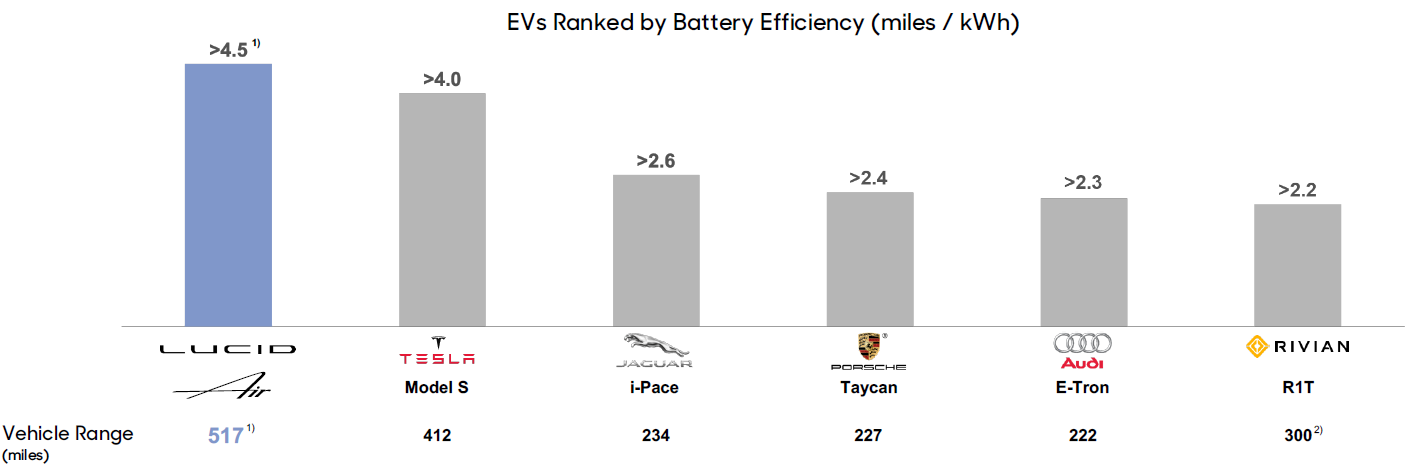

Figure 1. Comparison between Lucid Motors and other EV producers by battery efficiency

Source: Lucid Motors Investor Presentation, February 2021

The battery represents the most important part of electric vehicles, and its efficiency might be a real game-changer in the highly competitive electric segment of the automotive industry. Lucid Motors claims to have the most efficient batteries in the market. Its comparison with other companies is presented in Figure 1. More efficient batteries allow one to drive without the need to recharge longer, as well as charge the vehicle faster for the same driving range. Besides, Lucid’s battery packs are used by racing teams in the world’s premier EV racing series (Formula E), and the company expects its applicability in various fields such as aircraft, military, heavy machinery, agriculture, and marine, which could provide another substantial stream of revenue to Lucid.

Another important novelty that Lucid brings to the market is the Lucid Electric Advanced Platform (LEAP), which is an innovative powertrain that is going to be used for both product lines that are already under development (Lucid Air and Project Gravity) and all the vehicles Lucid might come up with in the future. Hence, fully in-house built LEAP provides a strong ground for the future development of new product lines and gives Lucid a strategic advantage over its competitors.

Lastly, Lucid’s partnership with Electrify America allows Lucid to enjoy wide coverage of charging stations in the US without a need to invest heavily in such stations. The charging stations of Electrify are also comparatively more powerful when compared to those of Tesla, with Electrify offering 900v while the Tesla Supercharger Network only offers 400v. Wide coverage and fast charging, especially combined with more efficient batteries, might make Lucid’s cars substantially more attractive for price-insensitive clients that highly value convenience and speed of charging.

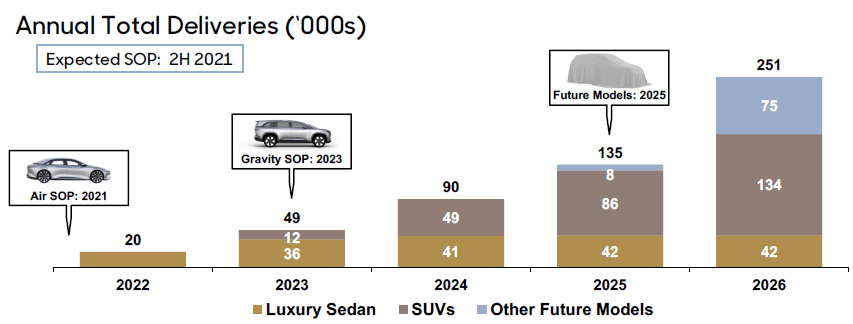

Figure 2. Production volume projections for Lucid Motors

Source: Lucid Motors Investor Presentation, February 2021

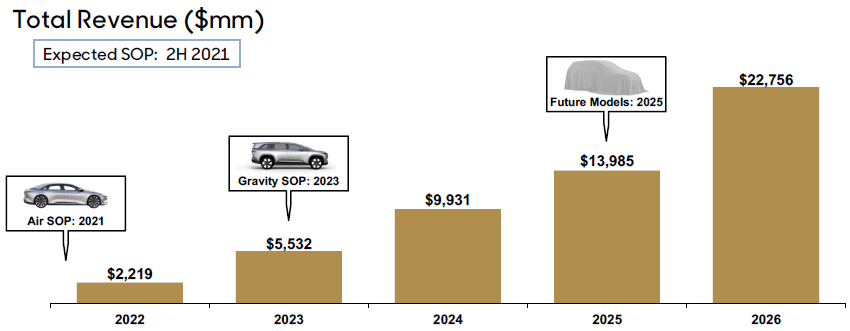

Figure 3. Revenue projections for Lucid Motors

Source: Lucid Motors Investor Presentation, February 2021

As was mentioned before, Lucid is still a pre-production and pre-revenue company. However, the company has issued significantly optimistic projections of its future production volumes and revenues, which are presented in Figure 2 and Figure 3, respectively. In its first full year of production, Lucid aims to deliver 20,000 cars and earn revenues of $2.2bn. In the 4 years after that, the company hopes to ramp up production to 251,000 units and earn revenues of $22bn.

Lucid Motors is usually named as one of the main Tesla competitors, and it is not surprising. Lucid’s product offering, at least in the next few years, will be focused on cars in the two main segments of the consumer automotive market: sedans and SUVs. Even though Lucid aims to offer luxury models, it is hard to predict whether this positioning will be able to set it apart from the crowd. Besides, there is no shortcut for making cars, and thus one needs to wait for a few years until any definitive conclusions can be drawn about Lucid Motors’ ability to capitalize on its technological breakthroughs, scale its vehicle manufacturing, and become a visible player in the automotive market.

Industry Analysis

The electric vehicle market (EV) has grown tremendously during the last decade. In 2010, only 17 thousand electric cars were sold. However, between 2014 and 2019 the industry averaged a 60% expansion rate. Although its growth has slowed down since then, the total market still grew about 6% in 2019. Thus, it is not controversial to say that the EV companies are one of the largest growth markets in the automotive industry. Tesla, which can already be considered one of the automotive titans, has seen its market capitalisation soar to as much as $830bn as of February 2021. Its valuation has overtaken that of its market peers such as Toyota and Ford, despite only delivering 367.5 thousand vehicles in 2019. Putting it into perspective, Toyota, valued at $206bn, processed 10mn deliveries in the same year. So high is the investor confidence in EVs that even Tesla imitators, such as Nikola and Lucid Motors, who have yet to produce a single commercial vehicle, have attracted billions of dollars of funding.

Arguably, the sales figures behind the industry sales suggest that the EV market has entered a mass adoption stage. Although electric vehicles constituted only 2.6% of global car sales in 2019, the trend is favourable. Per International Energy Agency, 140mn EVs are expected to hit the road by 2030. Demand for cars with the internal combustion engine (ICE) slumped in 2020 – of course the coronavirus contributed heavily to the trend. The ICE market shrank by as much as 15% in 2020, while EV sales remained similar to 2019’s status quo. Further, with almost majority of electric cars bought and used in China (47% of a 7.2 m stock of EV’s in 2019), its quick recovery from COVID lockdowns is bound to increase EV sales down the road.

That said, national governments have had a significant impact on the industry’s development from the very start. Emission standards have been regularly increased, forcing the conventional car manufacturers to induce significant adoption costs. Further, corporate governance issues, such as Volkswagen’s emissions scandal, only accelerated the political willingness to favour EV’s. A prominent example of political support for EVs is from China, whose government recently prolonged its national-wide subsidy until 2022. Also, investment in charging infrastructure features prominently in the EU’s Recovery Fund. Out of 1.83 B euro which makes up for EURF and the 7-year budget, 30% is set to be directed at reaching the bloc’s climate goals. That will most likely benefit the EV market prospects for the upcoming years.

For all the benefits of buying electric counterparts – tax reductions, subsidies – the technology is still lacking. Despite the cost of producing batteries dropping by 85% since 2010, and Tesla’s range increasing to 360 miles, these gains are offset by lacking infrastructure and extended charging times. For example, you are able to tank an ICE-powered car fully in 5, while a Tesla supercharger requires 45 minutes for a full charge. This is a significant competitive disadvantage, especially for long-distance journeys. Hence, Lucid’s promise to rival Tesla’s Model S range and extend it to 500 miles sounds appealing. That said, such innovations are needed across the board. Until now, no manufacturer has been able to rival Tesla technologically – despite attempts by household names such BMW or Volkswagen to do so. Investment in infrastructure and further improvements in technology are necessary to increase the still lacking competitiveness of EVs.

Deal Structure

The deal to take Lucid Motors public has been completed through the process of reverse merger via a special purpose acquisition company. This year alone, 128 SPAC IPO’s have raised a record $38 bn globally (as of 10th of February). Lucid merged with Churchill Capital IV (CCIV), set up by a long-standing banker Michael Klein. Currently a board member at Credit Suisse, he has also been a Vice President of Citigroup. He is one of the most active SPAC players, with seven SPACs raised to date.

Source: Lucid Motors Investor Presentation, February 2021

The transaction raised a gross value of $4.5bn ($4.4bn net of fees) for Lucid Motors. $2.07bn was raised from the SPAC while another $2.50bn was raised from a PIPE. The transaction valued the pre-existing equity of Lucid Motors at $11.75bn, giving the firm a post money valuation of around $16bn. What makes this transaction interesting is that the SPAC investors were able to purchase shares at $10/share, while PIPE investors had to purchase shares at $15/share. Thus, if taking into account founder and public warrants, the SPAC will own around 16% of the combined company, while PIPE investors will hold around 10%. The difference in the purchase price of shares makes it difficult to assess the pro-forma valuation of the firm. On one hand, if the entire share capital of Lucid is multiplied by the $10/share SPAC purchase price, the firm has a pro-forma valuation of around $16bn. On the other hand, if the $15/share PIPE value is used, the pro-forma valuation is $24bn.

Public Listing Rationale

The agreement between Lucid Motors and the SPAC Churchill Capital IV Corp to take the company public is the largest deal yet between a blank-check company and an electric vehicle start-up. The deal will help accelerate the trajectory of Lucid’s vision to redefine luxury, performance, and efficiency for electric vehicles and will strengthen its position in this rapidly growing market.

The $4.4bn financing from the transaction will be used for three main purposes: accelerating the launch of its initial models, expanding manufacturing capacity, and building its peripheral business lines. Firstly, with the funds from the deal, Lucid will be able to accelerate the launch of Lucid Air, a $169,000 luxury all-electric sedan, expected to debut at the end of the year. The funds raised will also be used to expand the company’s existing factory in Arizona, currently only operational for pre-production builds of the Lucid Air with a limited capacity of 34,000 units per year. The company plans to expand the $700 million factory across three phases over the coming years and eventually build up to a capacity to produce 365,000 units per year. Lastly, the additional capital will help Lucid realize its vision to supply electric vehicle technology to third parties, including other automotive manufacturers, as well as offering energy storage solutions in commercial, utility and residential sectors. Lucid also owns several retail locations in California and Florida and new funding will help to continue to expand the company’s retail and service operations throughout the US in 2021.

Lucid Motors joins a growing cohort of early stage electric vehicle companies to go public via a SPAC without having generated their first revenues. Going public via an IPO requires written disclosures to focus on historic financial performance. But when a company merges with a SPAC it is allowed to publish revenue and profit projections for the next several years. This is hugely advantageous for companies like Lucid Motors who have yet to start production because they can show and market their future up-side. The uncertainty of the reaction of traditional investors to an IPO from such early-stage companies selling a vision without a record of sales growth has led these electric vehicle start-ups to turn to SPACs. Furthermore, a SPAC involves a small select group of investors with an incentive to make a transaction happen – sponsors of SPACs usually have founder shares which automatically give them up to 20% of a SPAC upon a business combination. This makes it more likely that sponsors will over-pay for firms and allow pre-revenue, speculative companies like Lucid to raise cash at high valuations.

Market Reaction

The deal announcement follows weeks of speculation amongst investors ever since Bloomberg first reported that Lucid and Churchill were in talks on January 11th . Anticipation amongst investors lead to a dramatic 472% run-up in shares of Churchill in the weeks before the deal announcement. Speculation about the merger spread on Reddit and other social media platforms as traders pointed to myriad bits of information to infer a deal was imminent. However, shares fell by 46% to $30 after the deal was confirmed on the 22nd of February. The shares recovered slightly close to $35.21 a share, down 38.6% since their peak. Investors are likely to have been disillusioned by the announcement about the delay in deliveries of Lucid’s debut car – from this spring to the second half of the year. There was also confusion regarding the valuation of the firm, leaving many investors puzzled whether the firm was valued at $12bn, $16bn, or $24bn. Both these factors are likely to have caused the significant volatility in the stock prior to and after the announcement.

Advisors

Citi is serving as the sole financial advisor to Lucid Motors. BofA Securities and Guggenheim Securities are serving as M&A advisors to Churchill and Guggenheim Securities rendered a fairness opinion to Churchill in relation to the transaction.

0 Comments