Viacom Inc. (NYSE: VIA) – market cap as of 15/09/2019: $10.61bn

CBS Corporation (NYSE: CBS) – market cap as of 15/09/2019: $16.48bn

Introduction

On August 13, 2019, CBS and Viacom agreed to recombine in an all-stock merger, which will create a multiplatform premium content company set to become one of the leading content producers and providers with a global scale.

Formerly a division of CBS, Viacom was spun-off in 1971 amid changing regulatory provisions that prohibited television networks from owning cable TV systems or syndicating their programs in the US. After a merger in 2000 that ultimately failed in 2006 due to internal rivalry between the heads of CBS and MTV Networks, this marks the third attempt at a merger in the last three years.

The deal comes after years of intrigue and legal battles, as exemplified by the vicissitudes of April 2018, when CBS had approached Viacom with an all-stock offer that valued Viacom slightly below its market value. Immediately after Viacom rejected the deal, CBS sued its majority owner National Amusements, which is also the majority owner of Viacom, accusing its president of abusing her voting power in the company and forcing a merger that at the time was supported by neither CBS nor Viacom.

The merger to which both CBS and Viacom have agreed in August 2019 will create a company with more than $28bn in combined annual revenues, which is expected to deliver about $500m in annualized savings through synergies within 12 to 24 months after the transaction is closed. The resulting $47bn entity will be called ViacomCBS and is set to compete in an industry that has been drastically upended by Netflix. This strategic move reflects a trend in which US media and telecoms groups have hurtled towards consolidation in recent years, with the biggest players seeking to defend against the $119bn-market cap streaming giant.

About Viacom Inc.

Headquartered in New York, Viacom Inc. is a leading media conglomerate that creates entertainment content worldwide and is owned by National Amusement Inc., a theatre and mass media holding company. Viacom services reach approximately 700m households in over 160 countries, crowing it the 9th largest media conglomerate in the world with recorded revenues of $12.9bn and assets worth $23.2bn in 2018.

Viacom operates through two main segments: Media Networks and Filmed Entertainment. The Media Networks segment is mainly focused on the supply of entertainment content and related branded products through online platforms and more than 300 television channels, the most famous of which are Nickelodeon, MTV, and Comedy Central. On the other hand, the Filmed Entertainment segment is involved in the production, acquisition, and distribution of films under the Paramount Pictures, Nickelodeon Movies and MTV Films, which are exhibited in theatres, sold for home entertainment, and licensed to television and digital platforms.

Historically, Viacom originated as a spin-off from CBS in 1971 amid changing regulatory provisions from the Federal Communications Commission (FCC) that prohibited television networks from owning cable TV systems or syndicating their programs in the US. Fast forward 30 years and in the year 2000 Viacom merged with its former parent CBS Corporation for $49bn. However, in 2006 Viacom effectively reversed the Viacom-CBS merger by splitting the company into two publicly traded companies due to stock price stagnation, an internal rivalry between the heads of CBS and MTV Networks, and to liberate the growth potential of both MTV and Paramount.

The main driver of Viacom’s profitability has been Paramount’s strong momentum. It has recently registered its tenth consecutive quarter in which its YoY operating income has improved, while strong licensing and very positive home entertainment results led to further revenue growth.

In terms of Viacom’s recent financial performances, in Q2 2019 it generated net revenues of $3.4bn and a net income of $544m, determining a profit margin of 16.2%, marking a 13% increase in net revenue and a 44% increase in net income from its Q1 2019 performance. Focusing on an annual basis, the company generated revenues of $12.9bn in 2018, registering a 2.4% YoY decrease; net income has also decreased, as the company generated a profit of $1.7bn, from $1.9bn in 2017. To conclude, its profit margin for 2018 was 13.3%, only slightly decreasing from the 14.1% margin it had recorded in 2017.

About CBS

The company was founded in 1986 and is headquartered in New York. It operates as a mass media company worldwide, mainly in four segments: Entertainment, Cable Networks, Publishing, and Local Media. The Entertainment segment produces, acquires and distributes a schedule of news, public affairs, sports and TV series, while also operating online content networks for both information and entertainment. The Cable Networks segment offers subscription program services, such as original series, films, documentaries, and sports-related programs. The Publishing segment distributes consumer books in printed, digital, and audio formats. To conclude, the Local Media segment owns 29 broadcast television stations and operates local websites, including content from its television stations.

CBS’ recent strong performance has been driven by further investments in the premium content and direct-to-consumer streaming services businesses. CBS’ direct to consumer services, CBS All Access and Showtime, fuelled a 13% increase in affiliate and subscription fee revenue for Q2 2019. Content licensing is another key growth driver in which CBS has built a lucrative model, which is based on must-have programming for its distribution channels and content for third-party platforms.

Regarding its recent financial performance, in Q2 2019 CBS reported its best-ever second-quarter results in terms of revenues, operating income and EPS. It generated $3.8bn in revenues and recorded a net income of $440m, determining a profit margin of 11.5% and marking a 10% increase from Q2 2018, when it recorded $3.5bn in revenues. In annual terms, the company ended 2018 on a very positive note, fully recovering from the dismal performance obtained in 2017 and returning to the profitability levels reached in 2015 and 2016. In 2018, CBS generated $14.5bn of net revenues, with a 6% YoY increment, and a net profit of $1.9bn, up from the $357m of 2017. In 2018, the profit margin surged to 13.1% from the dismal 2.6% achieved in 2017.

Industry Overview

The entire US Media and Telecoms industry has been at the center of a wave of change and consolidation in the last 50 years. In the early 1970s, there were about 2,800 cable systems with about 7.5m subscribers. This resulted in obvious fragmentation of the industry, plus, the absence of adequate infrastructure reaching some major communities and a tough regulatory environment did not foster development.

On the other hand, the environment we see today is a completely different one with a few major players that have gained scale and size as new streaming services from Netflix and Amazon have completely changed it.

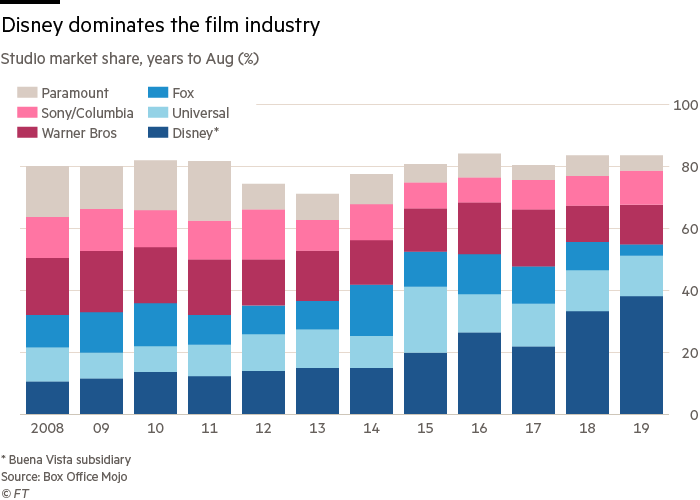

After its acquisition of 21st Century Fox at a record $71bn, Disney is expected to produce roughly 30% of all primetime scripted broadcast TV series and holds 42% of the entire US film industry box office.

Warner Bros has been absorbed by AT&T in its $80bn acquisition of the parent company, Time Warner and Comcast ended up owning Universal, leaving Viacom’s Paramount, Sony, and Lion’s Gate as possible targets in a rolling up industry.

At the same time, media conglomerates are trying to resist the disruption brought by giants such as Netflix and Amazon Prime Video with their subscription-based content, bringing millions of subscribers and sources of data that could unveil new customer needs and allow cross-selling opportunities.

Besides these two incumbent players, Disney is expected to launch its streaming service in November 2019, with profitability expected by 2024; Apple is joining the industry with a range of shows provided through a subscription that starts from $4.99, approximately half of an average Netflix subscription. AT&T is also ready to exploit its Time Warner library of content for a streaming service, adding to the list of other players pushing in the same direction.

Source: Financial Times, Box Office Mojo

Besides the number of major competitors, one should also think about how the streaming service has deeply changed the business model of a traditional media company. Nowadays, cancelling your subscription and going for a competitor has become easier and easier, without the need for engaging with customer service or investigating alternative offers.

It is reasonable to assume that the industry is also getting more competitive despite the consolidation wave due to higher capital requirements invested in the production of creative content and global distribution. The efforts required to participate have reached record levels, from investments in movies and TV series productions to those in marketing and retaining subscribers. The example of Netflix happens to be one of the most important, as the company has invested approximately $13bn in creative content production and $2.4bn in marketing, which is roughly what HBO invests in program budgeting.

Higher maintenance costs are also a concern, as demonstrated by Disney, which spent $2.6bn in the acquisition of a majority stake in BAMTech, a streaming technology provider. Media giants will now have to improve customer service, billing, which will no longer be outsourced, and invest heavily in technology experts, data scientists, product designers and software developers.

In general terms, the number of pay-tv subscribers worldwide is projected to exceed the 1bn mark by 2020, up from around 920m in 2014. The US, a developed and saturated market, offers little growth potential: in fact, pay-tv subscriptions are projected to fall there. The growth is expected to come from developing regions such as the Asia Pacific region and Latin America, where the expanding middle class on one side, and the developing infrastructure on the other, will offer a generous and steepening demand.

Deal Structure

After the merger, the Board of Directors will include 13 persons, among whom 6 will come from CBS, 4 from Viacom, two National Amusement, Inc. designees and the President and CEO of ViacomCBS, Mr Bob Bakish, already CEO of Viacom.

Existing CBS shareholders will own 61% of the combined entity, with the remaining 39% to Viacom (percentages calculated on a fully diluted basis of shares). According to the terms of the merger agreement, Viacom Class A and Class B voting and non-voting shares will be converted into a 0.59625 Class A voting shares and Class B non-voting shares of CBS.

The merger has been approved by unanimous vote by both the Board of CBS and the Board of Viacom; furthermore, National Amusement, Inc., holder of 78.9% of Class A voting shares of CBS and 79.8% of Class A voting shares of Viacom, agreed to deliver sufficient consents to allow for the approval of the transaction.

The entire merging process is still subject to regulatory approval and other closing conditions. It is expected to close by the end of 2019.

Deal Rationale

After numerous failed attempts to merge over these past years, National Amusement Inc., owner of 80% of both CBS and Viacom, will finally get its way and unite the two companies. Facing fierce competition from reinforced broadcast television networks and Over-The-Top (OTT) media companies, CBS and Viacom have decided to join forces, yet again, seeking to strengthen their position through a greater scale that will bolster Viacom and CBS in all areas of their business. Indeed, as a result of the merger, the two companies expect to gain leverage in negotiations over fees with distributors, boost content creation, enhance the distribution and advertising opportunities, and pursue further M&A activity.

Sumner Redstone once said: “content is king” and by merging the companies, top management expects to follow that guideline and invest more than $13bn a year in content creation; thus becoming one of the largest content spenders. The merger aims to boost advanced advertising technology and ad-supported streaming videos in a landscape where ad-free options like Netflix and HBO are the norm. Indeed, thanks to Viacom’s Vantage, an advertisement targeting platform, the newly merged company would benefit from putting into work that kind of technology across all its assets and gain data from CBS’ stable audiences that could help advertisers optimize their advertisement campaigns. This new advantaged position may end up being even more profitable as advertisers are expected to spend as much as $67.23bn on U.S. TV ads in 2019.

In a recent press release, Viacom stated that the combined firm would have appealing growth prospects and greater financial scale with a considerable amount of free cash flow, which would permit steady and meaningful investment in programming and innovation. Additionally, ViacomCBS would support its commitment to maintaining a modest dividend payment. Moreover, top management believes the deal will be EPS accretive, estimating $500m in synergies within 12 to 24 months following closing and holding firm in the idea that it will provide additional strategic benefits. Finally, ViacomCBS considers that the combined company will benefit from a solid investment grade rating thanks to a solid balance sheet characterized by strong cash flows. The flip side is that the deal will increase CBS’s exposure to traditional television. Additionally, the merged company could be in danger of overleveraging as CBS’s $9.2bn outstanding debt will be added to Viacom’s $8.2bn debt load.

Nevertheless, ViacomCBS would still be a minor player, with a market capitalization of around $30bn, significantly lower than industry giants namely Walt Disney at $245bn or Comcast at $193bn. In order to compete, as Shari Redstone explained: “We would want to look at something after that to… develop more scale as we move forward”. Hence, ViacomCBS expects to further scale through acquisitions and bulk up to the size of its rivals.

Market reaction

Shares of Viacom surged 2.4% from $28.53 to $29.21 and shares of CBS increased from $48.04 to $48.70 in a 1.4% gain after the merger was announced.

Since then both stocks have plummeted to $26.04 per share of Viacom and $43.82 per share of CBS. The market welcomed the deal at first, but some growing concerns have been raised during the past weeks concerning eventual excessive debt and exposure to the ill-looking traditional television industry. Indeed, some analysts consider that the deal is negative for the companies as it will prompt CBS to invest heavily in an expensive and risky direct-to-consumer offering in a crowded market. However, others believe the stocks are a buy, citing the deletion of leadership overhangs, higher ad sales force with greater digital inventory, the opportunity for incremental synergies and the chance of EPS accretion.

Financial & Legal Advisors

Centerview Partners LLC and Lazard Frères & Co served as financial advisers to the CBS board. Paul, Weiss, Rifkind, Wharton & Garrison LLP served as CBS’s legal counsel.

Lion Tree Advisors LLC and Morgan Stanley & Co served as financial advisers to the Viacom board. Cravath, Swaine & Moore LLP acted as legal counsel to the Viacom board.

Evercore served as financial advisor to National Amusements. Cleary Gottlieb Steen & Hamilton LLP acted as National Amusement’s legal counsel.

0 Comments