Tesla Motors, Inc. (TSLA) – market cap as of 23/09/2016: $30.85bn

SolarCity (SCTY) – market cap as of 23/09/2016: $1.93bn

Introduction

On August 1, 2016 Tesla Motors (“Tesla”), US electric cars developer and manufacturer, agreed to acquire SolarCity, US provider of solar energy services, in a $2.6bn deal. Tesla shareholders will receive 1 share of SolarCity in exchange of 0.11 of each of their own shares. The transaction is allegedly expected to create an integrated sustainable energy company and leverage cross-selling opportunities. However, Elon Musk’s – Tesla’s CEO’s – significant ownership in both companies and the presence of interested directors on the boards create a great deal of ambiguity around the transaction, particularly given the not-so-shining financial position of SolarCity.

About Tesla Motors

Founded in 2003 by a group of engineers in Silicon Valley, Tesla Motors is a producer of electric cars, aiming to accelerate the world’s transition to sustainable energy. Tesla owners enjoy the benefit of charging their cars at home, while for long distance journeys, Tesla’s Supercharger network provides them with access to high speed charging, connecting popular routes in North America, Europe, and Asia Pacific.

On June 29, 2010, the company went public on NASDAQ stock exchange and listed its shares at $17: On the first trading day, the shares soared 41%. The new funds allowed the company to grow further, and in 2012 Tesla launched Model S, the world’s first premium electric sedan.

With more than 50,000 vehicles on the road worldwide, Tesla also launched Model X, a crossover vehicle, and presented Model 3, a new vehicle starting just at $35,000.

As of the end of the last reporting year, the company is still losing money. In 2015, Tesla generated $4,046m in revenues (26% y.o.y) and $716m in operating losses (3.8 times as much as the year before). 44% of operating expenses are comprised of expenditures on research and development.

About SolarCity

SolarCity is a vertically integrated company that provides renewable electricity directly to homeowners, businesses and government organizations by taking care of everything from design to monitoring and maintenance. The company installs solar panels for commercial and residential properties on sale or lease terms.

On December 12, 2012 the company went public at 8$ (down from initial range of $13-$15 due to negative market sentiment), but the price rose 47% on the first trading day.

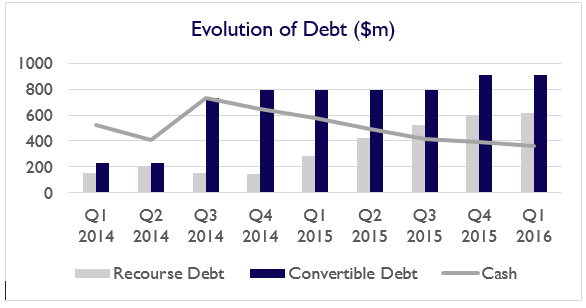

As of June 30, 2016 SolarCity has $5.2bn in solar energy system assets on its balance sheet, contracted to create $3.1bn in future payments on a net present value basis (assuming 6% discount rate). However, SolarCity’s business depends on debt — the company offers homeowners the chance to install solar-power systems with little to no money down, and collects monthly payments instead. Such business model led to the high level of indebtedness.

Source: BSIC

Source: BSIC

Deal Structure

The acquisition of SolarCity by Tesla is an all-stock deal, whose equity value is $2.6bn based on the 5-day volume-weighted average Tesla stock price, as of July 29. The deal values SolarCity’s common stock at $25.37 per share, and its shareholders will receive 0.11 Tesla common shares for each SolarCity share they own.

SolarCity has stated that it expects the transaction to be concluded in the fourth quarter of 2016. Meanwhile the company enjoys a 45-day “go-shop” period, during which it can obtain alternative proposals.

Elon Musk—Tesla’s co-founder and CEO, and SolarCity’s co-founder and chairman—has a personal stake of around 20% in the two companies. Nonetheless, he claimed he was not involved in the valuation of the purchase and will vote in proportion to the voting of the publicly held shares of both companies.

Deal Rationale

The main argument that moved Musk to combine Tesla and SolarCity primarily relies on the creation of a battery system that stores solar energy in homes and businesses thus minimizing their dependence on the power grids run by utilities. In other terms, Tesla’s batteries would end up serving as energy storage units linked to solar panels for households than being plunked into cars. According to Musk’s vision, the next logical step is not just switching from gasoline to electricity but letting consumers both clean up the energy grid and switching to alternative power sources. Furthermore, the consistency of the business models of the two companies is believed to facilitate their integration and the creation of synergies. In fact, Both SolarCity and Tesla share an integrated business model, in which the firms own the means of production.

Market Reaction

There was a lot of scepticism surrounding the deal by industry analysts and market participants alike. On August 1st Tesla’s shares fell by 1.26%, while SolarCity’s shares suffered more, dropping 5.17%. According to many analysts the deal was essentially a bailout for SolarCity, which has been posting negative returns for several quarters. While Tesla is also suffering losses in its operation, the company has the ability of raising capital much more easily than SolarCity, due to a myriad of reasons which include the enthusiasm Musk and Tesla’s vision inspire in many investors.

Considerations

The transaction has been characterized by clear conflicts of interest. Not only Elon Musk is the Chairman and CEO of Tesla and the Chairman of SolarCity, he is also the largest shareholder of the two companies, with a stake greater than 20% in each. Furthermore, the majority of the members of the boards of the two companies are not neutral. Indeed, SolarCity’s board includes Musk’s first cousins Peter and Lyndon Rive, board member of Tesla Antonio Gracias, as well as Tesla’s co-founder Jeffrey Staubel. While, Tesla’s board includes Antonio Gracias, Musk’s brother Kimbal Musk, and Brad Buss – who served as SolarCity’s CFO until he retired. Such boards’ composition leaves just three supposedly neutral directors on each board. However, if we consider that venture capital firm Draper Fisher Jurvetson has a seat at each company then only two directors per board can be considered without conflict.

The conflict of interest is particularly relevant if we consider that Tesla never turned an annual profit while SolarCity dropped its value by 50% in one year. Furthermore, the Altman Z-score, which estimates the probability that a company will go bust, puts at 20 percent the likelihood that Tesla-SolarCity would be bankrupt within three years.

For these and other reasons, many believe that Elon Musk and other conflicted Tesla directors, along with certain SolarCity directors, orchestrated the acquisition to protect their personal interests in SolarCity, and Musk’s legacy in the industry. Although Tesla directors sounded confident in a letter writing “We do not anticipate significant regulatory or other obstacles in consummating a mutually beneficial transaction promptly”, already two pensions funds have filed lawsuits. It is true that those lawsuits are rarely successful, and even when they are, they usually don’t prevent the execution of a deal. However, it will imply at least a delay in the merger.

[edmc id= 4038]Download as PDF[/edmc]

0 Comments