Legacy Betting Industry: the Post-PASPA Landscape

For the better part of the last three decades, sports betting in America existed in a legal paradox. The games were everywhere, but the ability to wager on them legally was restricted to a single state. PASPA – the Professional and Amateur Sports Protection Act of 1992 – did not make sports gambling a federal crime; it prohibited states from authorising it, freezing Nevada’s monopoly in place while the rest of the country bet illegally or not at all.

That changed on May 14, 2018, when the Supreme Court struck down PASPA in Murphy v. NCAA, returning the decision to the states. The floodgates opened quickly: six states went live before the end of 2018, another nine launched in 2019, and the pace accelerated through the pandemic years as state governments – starved of tax revenue – rushed to legalise. By 2024, 40 states had authorised sports wagering in some form, with online access available in 30 states and Washington DC. Total handle grew from $4.6bn in 2018 to over $149bn by 2024 – a 32-fold increase in six years.

But the structure this created was not the product of considered federal policy. It was the outcome of 35 legislatures acting independently, each extracting maximum value from operators who had no choice but to comply. Two features of that structure define the economics of the industry today.

The first is the tax burden. Because each state controls its own regime, operators face a range running from 6.75% in Nevada to 51% in New York – an eight-fold difference in the cost of doing business for an identical product. New York is the defining case: when its online market launched in 2022 at a 51% rate, operators objected but launched anyway, because walking away from twenty million potential customers was not a realistic option. The state collects over $200mm per quarter in betting taxes. The operators absorb it. Critically, this dynamic worsens over time – states use low rates to attract operators, then raise them once those operators are embedded and cannot credibly exit. Illinois raised its top rate to 40% in 2025. New Jersey and Maryland followed with increases the same year. Licensing fees – $10mm in Pennsylvania, $25mm in New York – add a further fixed-cost barrier before a single bet is placed.

The second is regulatory fragmentation. Each state runs its own approval process for new products, bet types, and markets. Several ban wagering on in-state college teams; others restrict player props; some require physical retail partnerships as a condition of online access. What is nominally a single national product must be maintained as dozens of distinct regulatory filings, with permanent legal and compliance infrastructure in every state simultaneously. This overhead does not scale – it is a fixed cost duplicated across every market, creating a structural floor below which smaller operators simply cannot survive.

The combined effect is an industry that grew explosively in volume but was handicapped from birth: fragmented by state, taxed most heavily in its largest markets, and burdened with compliance costs that only operators of significant scale could absorb. It is this structure – more than any product advantage – that drove the market toward the duopoly that defines it today.

Economics of the Incumbent Duopoly: DraftKings & FanDuel

The U.S. betting market is effectively a duopoly, where the two incumbents – DraftKings [NASDAQ: DKNG] and FanDuel [NYSE: FLUT] – hold a combined 75% market share. The remaining 25% is divided among a fragmented group of smaller players that lack the scale to compete and turn a profit – a structure reminiscent of the OTT streaming wars and the consolidation that followed, with the best capitalised platforms offering the best product and user experience winning the majority of the market. With $7bn of revenue in 2025, FanDuel leads the market, commanding a 40% market share, while DraftKings controls 35% of the market, with gross revenues of $6.1bn.

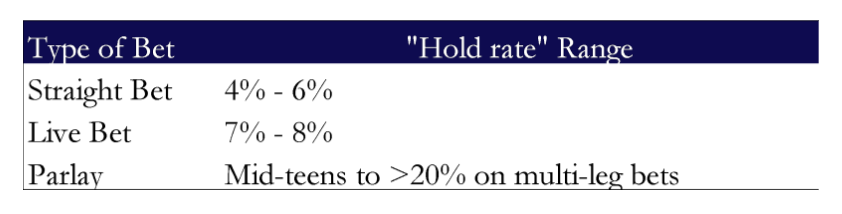

The betting business model is driven by two key factors: handle, the total dollar value of bets placed on the platform, and the hold rate, the percentage of bets that the platform retains. Based on the annual filings of the two largest incumbents, the average hold rates in the industry are between high-single-digits and low-double-digits, depending on the pricing, types of bets in the handle, and sports performance. For the purposes of understanding the position of the incumbents compared to prediction markets, the hold rates ought to be understood with reference to the type of bet. Due to the simple principles of probability, parlays will pay more than live bets, while live bets will pay more than straight bets (bets made before the event). Drawing upon shareholder meetings and management commentary from the annual reports, the following hold rate ranges can be inferred:

Making some assumptions about the hold rates for normal bets and parlays, it can be estimated that parlays account for 12-30% of the total handle, which shows a moderate reliance on these higher-yielding bets to generate revenue. Parlays are something unattainable for prediction markets, which rely on transaction fees that rarely reach above 5% and usually hover around 2%. As a result, on the same dollar volume, incumbents can expect to make 2-3x what prediction markets would.

On the cost side, however, incumbents are highly disadvantaged. As discussed above, taxes often constitute the bulk of the total operating expenses. Due to their variable nature, taxes limit the operating leverage these businesses can gain. The second-largest cost centre is the Sales & Marketing cost, which often accounts for over 20% of revenue, drives handle size, and ensures the incumbents retain market share. While this is the largest lever to switch between growth and profitability, due to the threat of new entrants, it is often non-negotiable. The main operating leverage can be found in the technology costs related to engineering and product design, and the general administrative costs, which together account for less than 20% of revenues. This rigid cost structure, driven by taxes and marketing needs, and the great scale needed to drive profitability through leverage on the G&A costs, largely explains why the market is so concentrated between the two incumbents.

The Structural Challenges

The economics described above and regulatory risks that go hand in hand with this business model make the betting market particularly challenging to operate in.

The state-by-state tax regime does not just compress margins – it makes them structurally unreliable. As illustrated above, the political dynamic runs consistently in one direction: states attract operators with reasonable rates, then raise them once those operators are embedded and cannot credibly exit. Of course, local governments have to consider the point at which operating in their state will no longer be worth paying Uncle Sam its cut, so the hikes will not go on indefinitely. Nevertheless, rates in some states still allow for plenty of increases and the legacy incumbents are far from safe on that front.

The model is also highly dependent on a small number of sporting events. The NFL alone drives a disproportionate share of annual handle, leaving both incumbents heavily exposed to scheduling disruptions, labour disputes, and the outcomes of a handful of high-profile games. That concentration carries a regulatory dimension that is easy to underestimate. The relationship between professional sport and legal betting remains unsettled; several high-profile cases of players gambling on their own sport have already prompted investigations across the NFL, NBA, and MLB. If a major league were to restrict wagering on its events, whether driven by integrity concerns or player pressure, the impact on handle would be immediate and severe, with no diversified revenue base to absorb it.

Taken together, the cost structure and regulatory risks create a hostile operating environment and make the incumbents structurally exposed to disruptors unburdened by the official rules. Today, these seem to be coming in the form of prediction markets.

The History of Prediction Markets

Prediction Markets (PMs) aren’t a new phenomenon. They first arose in 1988 in a bar in Iowa, where three economics professors created the Iowa Electronic Market to track election polls. Although only a small volume of 16,498 total trades by 192 individuals were executed in the first market of the 1988 presidential election, the platform was accurate in predicting the election results (Bush won), setting a precedent for what was to come. Over the next five presidential elections, IEM beat polls 74% of the time as more and more people registered and started trading. In 1992, the website received a no-action letter from the CFTC, allowing it to operate strictly academically, with no advertising, and trades capped at $500, setting precedent for what was to come.

PredictIt was launched in late 2014 by the Victoria University of Wellington, receiving a no-action letter a couple of days before (modelled on the IEM letter). The letter allowed PredictIt to operate as a not-for-profit market for political event contracts without registering as a designated contract market, provided it met strict conditions: a maximum of 5,000 traders per contract and max. $850 investment per participant per contract, non-profit, no brokerage commissions, KYC via third-party provider, only academic/research purpose advertising, and finally markets limited to political elections and economic indicators. PredictIt created the first regulated prediction market in the U.S., where traders could earn money, some up to tens of thousands a month. By charging a 10% gross profit plus a 5% withdrawal fee, PredictIt was also earning revenue. As a result, many of the contract prices were less accurate than IEMs, as the profit fees reduced arbitrage incentives. In 2022, the CFTC withdrew PredictIt’s no-action letter (they did not specify why), forcing the platform to shut down. After a legal battle in 2023, the platform was allowed to relaunch, which happened in early 2025. Today, it operates as “the pioneer in real-money political prediction markets” but is now a small player in a much more competitive landscape.

Kalshi and Polymarket are the two largest operators of prediction markets today, but their history is fundamentally different. Kalshi decided to go down the regulated path, becoming the first-ever CFTC-regulated, for-profit designated contract market (DCM) for event contracts in U.S. history when launching in 2021. They launched with markets on economic indicators like CPI, unemployment, or the Fed funds rate decisions, but got blocked by the CFTC from listing political event contracts in 2023 (contrary to the public interest under the CEA’s §40.11). Kalshi sued, and in October 2024, it was allowed to revive the markets, just in time for the presidential election, opening the floodgates for legalized election betting, sports contracts, and other event categories. Since then, their user base grew 50x year-on-year and their trading volume 100x. Sports betting is the largest prediction market, representing 90% of activity, and single events such as the Super Bowl trigger >$1bn in trading volume. Today, Kalshi is valued at roughly $11bn after their Series E, has formal partnerships with CNN, CNBC, and the NHL.

In contrast to Kalshi, Polymarket initially operated without regulatory approval. After being founded in 2020, the CFTC launched a formal investigation in October 2021, resulting in Polymarket paying a $1.4mm civil penalty for “operating an unregistered derivatives facility offering illegal binary options swaps”, requiring it to block U.S. users, but still being able to operate abroad. Polymarket was built on the Polygon blockchain, allowing near-instant settlement with very low transaction costs. This removed the need for a central counterparty, allowing for rapid global expansion. Polymarket’s growth was parabolic through the 2024 U.S. election cycle. Volume jumped to $9bn in 2024 (48x year-on-year), around 300,000 new traders signed up in 2024, and a record $3.5bn was wagered on the U.S. presidential election (Trump vs. Harris) in 2024. As of October 2025, Polymarket is valued at around $9bn after an investment by the Intercontinental Exchange [NYSE: ICE] (the parent company of the NYSE).

How do Prediction Markets work?

Unlike the traditional sportsbook model, prediction markets operate under an exchange-based model. Here, the platform never takes the other side of the trade but rather acts as an intermediary between buyers and sellers, charging a transaction fee for each trade. Someone who buys “Yes” is matched with someone who sells “No” (or vice versa). This model is the same as for the NYSE or any other derivatives exchange.

The core mechanic is built around a binary question, for example: “Will SpaceX IPO by 30/06/2026”. If this contract trades at $0.63, this means the market collectively estimated a 63% chance of this event happening. If it actually occurs by the specified date, the contract pays out $1 to each trader holding a “Yes” share and $0 for each “No” share. Importantly, these contracts are liquid and can continuously be traded as prices adjust in real time. Thus, a trader does not have to wait until the actual occurrence of the event, but can exit his position before, making a profit on the increase in value. For example, if one buys a “Yes” contract for $0.20 but due to new news emerging it appreciates to $0.80, the trader can sell each contract for a $0.60 profit. Binary contracts were the origin of prediction markets, but new types of contracts have also emerged. Categorical contracts offer independent markets with multiple possible outcomes; for example, “Who wins the Super Bowl?”, where each team winning would have its own independent market with unique odds. Secondly, continuous markets are based on numerical levels. For example, “Will Bitcoin be above $X in 15 minutes?” offers many answer possibilities like $70,000, $75,000, and so on.

The structural difference to the sportsbook model is the fee structure. Traditional bookmakers take the other side of the trade performed, therefore incorporating a house edge of around 4.5% on each bet. This distorts the true probability of an event occurring. In prediction markets prices are set by market participants like informed traders, arbitrageurs, and hedgers. This is why prediction markets tend to be more accurate than sportsbook-derived odds: the pricing mechanism is designed to aggregate information, not to protect a house margin.

Still, it is important to differentiate between the use case and the actual usage of these markets. Prediction markets argue that they are a tool for corporate risk hedging (for example, regarding regulatory outcomes), policy forecasting, and simply for private individuals to hedge everyday transactions, such as filling the car with gas. Information aggregation (“wisdom of crowds”), disperses information held by lobbyists, researchers, and politicians and incorporates it into prices, resulting in real-time probability estimates. Unfortunately, this logic is very utopian. Prediction markets have largely turned into gambling sites. This is evident as 85-90% of Kalshi’s fee revenue and 40% of Polymarkets (the largest category) depend on sports betting. Prediction markets are primarily retail speculation vehicles dressed in derivatives clothing.

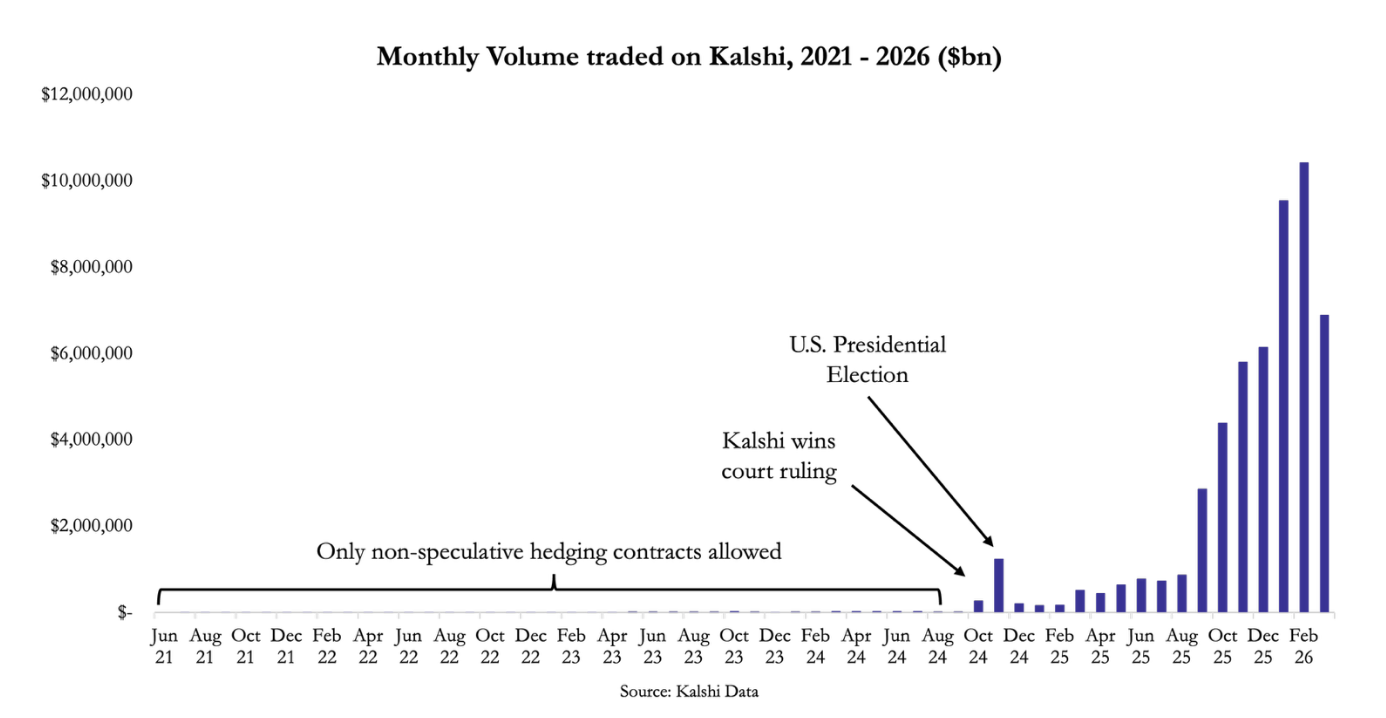

As evident in the chart showing the monthly notional trading volume on Kalshi, from launch through most of 2024, activity remains negligible, with only marginal volumes, indicating limited user adoption and low liquidity because the website only offers non-speculative hedging contracts. At this point users can bet on CPI figures, but not bet on politics, war, or sports events. Only after Kalshi starts offering these services, most notably betting on the U.S. presidential election, volume begins to pick up, solidifying the “gambling” hypothesis.

As evident in the chart showing the monthly notional trading volume on Kalshi, from launch through most of 2024, activity remains negligible, with only marginal volumes, indicating limited user adoption and low liquidity because the website only offers non-speculative hedging contracts. At this point users can bet on CPI figures, but not bet on politics, war, or sports events. Only after Kalshi starts offering these services, most notably betting on the U.S. presidential election, volume begins to pick up, solidifying the “gambling” hypothesis.

Regulation Scrutiny

Prediction markets in the U.S. are treated as derivatives, since their payoff structure relies on the occurrence of an event. This places the broader universe of macro-driven swaps under Commodity Futures Trading Commission (CFTC) jurisdiction. This is distinct from Securities and Exchange Commission (SEC) scope, which covers security-based swaps, where the contract is tied to a specific company or asset. This regulatory split is particularly influential for institutional platforms, as they must reckon with “Core Principles” that call for increased market surveillance and financial integrity. Among other guidelines, Core Principle 3 requires exchanges to list contracts not “readily susceptible to manipulation.” However, contracts staked on the actions of a single individual, such as the number of tweets written by Elon Musk by the end of the week or mention markets, undoubtedly carry high manipulation risk.

The regulatory hostility toward prediction markets can be traced back to the historical struggle to separate financial instruments from “bucket shop” gambling. Most common in the early 20th century, bucket shops were illegal brokerages that bet on the movement of stocks and commodities with no underlying asset. Although they would mimic the activity of legitimate brokerages, they would “bucket” orders by keeping funds rather than executing trades. The American courts responded with the “intent to deliver” test to determine the legality of a contract. The legal precedent cemented the regulatory perception that financial instruments untethered from an underlying asset would contribute to the gamification of financial markets, emblematic of casino-like habits among consumers. In the years following, the 2000 Commodity Futures Modernization Act (CFMA) deregulated the over-the-counter (OTC) swap market. This market amassed to a $600tn swap market, contributing to the era of deregulation leading up to the 2008 financial crisis. It created the impression that the U.S. financial system had become excessively speculative, inciting political backlash that culminated in the Dodd-Frank Act. The Dodd-Frank Act introduced provisions, such as Section 5c(c)(5)(C) to the Commodity Exchange Act (CEA), which outlawed five categories “contrary to public interest”: activity unlawful under federal or state laws, terrorism, assassination, war, and gaming. What followed was a familiar pattern. Companies like NADEX and PredictIt would launch prediction platforms and slowly gain early traction before running into regulatory bottlenecks. Foreign markets, such as Intrade, attempted to fill the gap of demand but fell short due to U.S. regulatory policies. By 2010, the regulatory stance had become more firm.

The KalshiEX LLC v. CFTC litigation signalled hope for prediction markets to operate legally. In the landmark court case, Kalshi filed for congressional control contracts to be listed on their platform. This would allow users to speculate on which party would control Congress just months before the 2024 presidential election. The CFTC blocked these contracts because they resembled election gambling and fell into the gaming outlawed category. Kalshi challenged this decision in pursuit of expanding into broader categories under the Administrative Procedure Act. In September 2024, the U.S. District Court ruled in favor of Kalshi. The courts upheld the finding that elections were indeed distinct from gaming under the plain text of the CEA. In timed fashion, their federally approved status raked in $1.27bn by November 2024, of which $1.13bn or 89% came from political contracts. On the other end, Polymarket’s rise to popularity was born directly from U.S. regulation. July 2025 marked Polymarket’s return to U.S. markets, after their $112mm acquisition of QCX, a CFTC approved exchange. This clearance coincided with a major boom in events betting, akin to what experts call a gold rush in the predictions business.

However, the era of supportive regulatory policy may be coming to an end. Under the new leadership of CFTC Chairman Michael S. Selig, he aims to promulgate clear rules to actively regulate prediction markets. The CFTC has submitted an amicus brief to the Ninth Circuit reaffirming the CFTC jurisdiction over event contracts. The brief reinterprets that “[s]tates cannot invade the CFTC’s exclusive jurisdiction over CFTC-regulated designated contract markets (“DCMs”) by re-characterizing swaps trading on DCMs as illegal gambling.” The result is a regulatory fight that looks very different from what it did a year ago. The attention no longer surrounds whether these markets are federally prohibited, but whether courts will back the agency’s jurisdictional position against a mounting wave of state challenges in Nevada, Tennessee, and Massachusetts.

Impact on Wall Street

Recent geopolitical events, such as the extraction of former Venezuelan President Maduro and the military action in Iran, have caused a massive increase in concerns related to insider trading on prediction market platforms. Unlike traditional financial markets, where insider trading is clearly defined and regulated, prediction markets lack well-established legal frameworks. One of the main challenges is the vast range of contracts available, making monitoring difficult. Additionally, it is harder to prove insider trading due to the specificity of events and the short timeframes involved, especially compared to securities markets. Platforms like Kalshi and Polymarket have already taken action by banning certain users, including individuals allegedly betting on non-public information such as unreleased online content or government-related events. In response, U.S. policymakers have begun exploring regulations aimed at restricting or banning the use of insider information in these markets.

On the other hand, Polymarket founder Shayne Coplan believes that insider trading is a key feature of prediction markets that should stay around. Coplan has stated that he believes insider trading on these platforms allows the public to gain access to so-called “insider” news, democratizing media coverage faster and more accurately. Economist Robin Hanson, a professor whose research inspired many prediction markets, echoes Coplan’s views, believing that these markets serve as tools for the populace to better understand what is going on in all facets of the world. The regulation of prediction markets has fallen under the guidance of the CFTC, which, in March of 2026, published regulations to more specifically outline the rules markets must adhere to, as well as an invitation for public comment on current rules that may need modification. Since the beginning of the Trump administration, the CFTC has been slow to overregulate the industry. It has stated its belief that the format of prediction market bets makes them far more like financial derivatives than gambling, therefore identifying prediction contracts as such. It has also stated that all contracts must be filtered for manipulation likelihood before they are posted in order to prevent fraud and insider trading, such as that which occurred with a Super Bowl 2026 bet that there would be a streaker during the game, after which an individual placed the bet and then became the streaker himself.

On Wall Street, prediction markets are creating both threats and opportunities for investors. Intercontinental Exchange recently launched a tool, in partnership with Polymarket, which normalizes and distributes data from the online prediction market to institutional investors. Bitwise Asset Management, Roundhill Investments, and GraniteShares are all interested in launching prediction market ETFs, offering exposure to betting on political elections and campaigns in 2026 and 2028. With the short timeline that prediction markets usually offer, these contracts could be very attractive to hedge funds and quant funds looking for liquidity across their portfolios, however, with the massive amount of money that would be bet by institutional investors, this creates serious concerns over election fraud and other market manipulation risks.

It is clear how prediction markets would be attractive to derivative or options traders with an easy to navigate system, allowing them to place bets on specific financial metrics. While in the past, when options traders would look to bet on unemployment or inflation rates, they would have to identify stocks they believe would adjust accordingly based on reports, analyze how this would impact the price of the asset, and place their bets. On prediction markets, it is as simple as answering yes or no to “Will unemployment increase?” by a given deadline. In addition to this simplification, they offer traders access to a larger number of bets that could be used to hedge against traditional positions from macro events to specific stock price adjustments. Arbitrage traders could even capitalize on different mispricing between prediction market estimates and crypto exchanges by taking advantage of the small amount of time it takes for updates to travel between cities. Many investment strategists believe that prediction markets will serve as valuable tools to hedge against macro shifts or political outcomes that would impact their current positions. Regardless, prediction markets are becoming financial instruments that are going to stick around, as consumers use them to circumvent gambling restrictions and companies like Robinhood [NASDAQ: HOOD] are racing to integrate them into their existing platforms.

As prediction markets’ pricing system aggregates the odds that the market assigns to a given outcome, this metric could be incredibly valuable to politicians to gauge approval of policy, managers to assess demand, investors to understand market sentiment, and more. In the 2024 U.S. Presidential Election, early voter results moved over prediction markets within minutes before major news networks could even change their data, pricing in information before the news could report on it. As a result, news outlets have begun using prediction markets as a measure of sentiment to build their own reports on, demonstrating the impact the markets are having. This same idea could impact the way investors trade stocks as well. If a company is facing regulatory hurdles, awaiting a ruling, their stock price may be trading at a discount based on how investors believe this will impact the business, but cannot isolate the implied odds of the ruling itself. However, with a prediction market, investors could see which way people believe the verdict will go, more accurately pricing in this risk.

Prediction markets have the potential to reshape how M&A transactions are priced in public equity markets. In a traditional deal, once an acquisition is announced, the target’s stock typically jumps to a discount or premium, reflecting the offer price, known as the merger arbitrage spread, which reflects the market’s estimate of deal failure risk or value that could be added on to the current price if the deal goes through. Research from the Fed shows that the median target stock jumps 27% upon announcement but trades at a persistent 3.5% spread to the offer price, with arbitrageurs earning that spread by absorbing deal risk from investors who want out. The problem is that this spread is just a rough estimate which bundles regulatory, political, and financing risks, as well as shareholder approval risk into a single implied probability that is difficult to breakdown. Prediction markets could completely change that discount or premium since each contract price directly represents the market’s real-time probability estimate of a discrete event. Applied to M&A, a prediction contract on “Will this deal receive regulatory approval?” would isolate specific risks, making them separately tradable, allowing sophisticated investors to price political or antitrust risk independently from the underlying equity. An example of this is Polymarket’s contract pricing on an Ethereum [Coinbase: ETH] ETF approval rose from 35% to 78% ahead of an SEC filing leak, moving adjacent to a 12% surge in ETH’s price, demonstrating that prediction markets can lead traditional financial markets in pricing regulatory outcomes rather than simply copying them. As these platforms grow and institutional participation increases, this spread could compress, making prediction market contracts an anchor probability that forces equity prices to converge toward true deal value faster and more precisely than today’s blunt spread-based pricing allows. Prediction markets could also be quicker than equity markets to signal critical catalysts. Consider an insider aware that his company will announce a merger that will be perceived positively by investors. While investing directly in the equity markets is strictly prohibited by law, being long a correlated contract on prediction markets isn’t. This would not only extend the scope of concerns regarding insider trading but could also work as a prime indicator for equity investors: if correlated bets on PMs indicate a positive catalyst incoming (driven by insiders), public markets may react before official announcements.

Conclusion

As demonstrated throughout this article, the legacy betting platforms face structural weaknesses related to the tax burdens and operating model, which make them susceptible to disruption. Prediction markets are those disruptors. In just a couple of years, their volumes surpassed the handles of FanDuel and DraftKings. Unburdened by the regulatory requirements, they continue to thrive and take market share. This trajectory, however, largely relies on the supportive stance of the CFTC controlled by the Trump administration. The resolution of the legal status of prediction markets in the post-Trump regulatory environment will likely determine the fate of the legacy players and the disruptors. For now, it’s safe to conclude that the more sophisticated market participants are likely to keep shifting from legacy betting sites to the more liquid and efficient PMs. However, this shift is not guaranteed to continue unchecked, as increasing regulatory scrutiny could significantly alter the competitive landscape. Should stricter oversight be imposed, prediction markets may face similar cost and compliance burdens that currently constrain legacy operators. Even so, their structural advantages in liquidity, pricing efficiency, and market-driven probabilities suggest they will remain a compelling alternative. Ultimately, the long-term balance between incumbents and disruptors will be determined by how regulators choose to define and govern these markets.

0 Comments