Pembina Pipeline Corp (NYSE:PBA) – market cap as of 05/05/2017: $17.38bn

Veresen Inc. (TSE:VSN) – market cap as of 05/05/2017: C$5.81bn ($4.26bn)

Introduction

On May 1, 2017, Pembina Pipeline Corp. announced that it had agreed to buy smaller rival Veresen Inc. for about C$9.7bn, either paid through stock or cash, creating one of Canada’s largest energy infrastructure companies.

This is the latest deal in a sector that has been consolidating in the face of low commodity prices and high costs, whereby Pembina Pipeline Corp. seeks to create an integrated business across the energy infrastructure value chain. The new entity will benefit from a range of synergies and the ability to compete for future investment opportunities and execute on a larger, more complex suite of opportunities amid an increase in hydrocarbon output from North America and the need for massive projects to handle it.

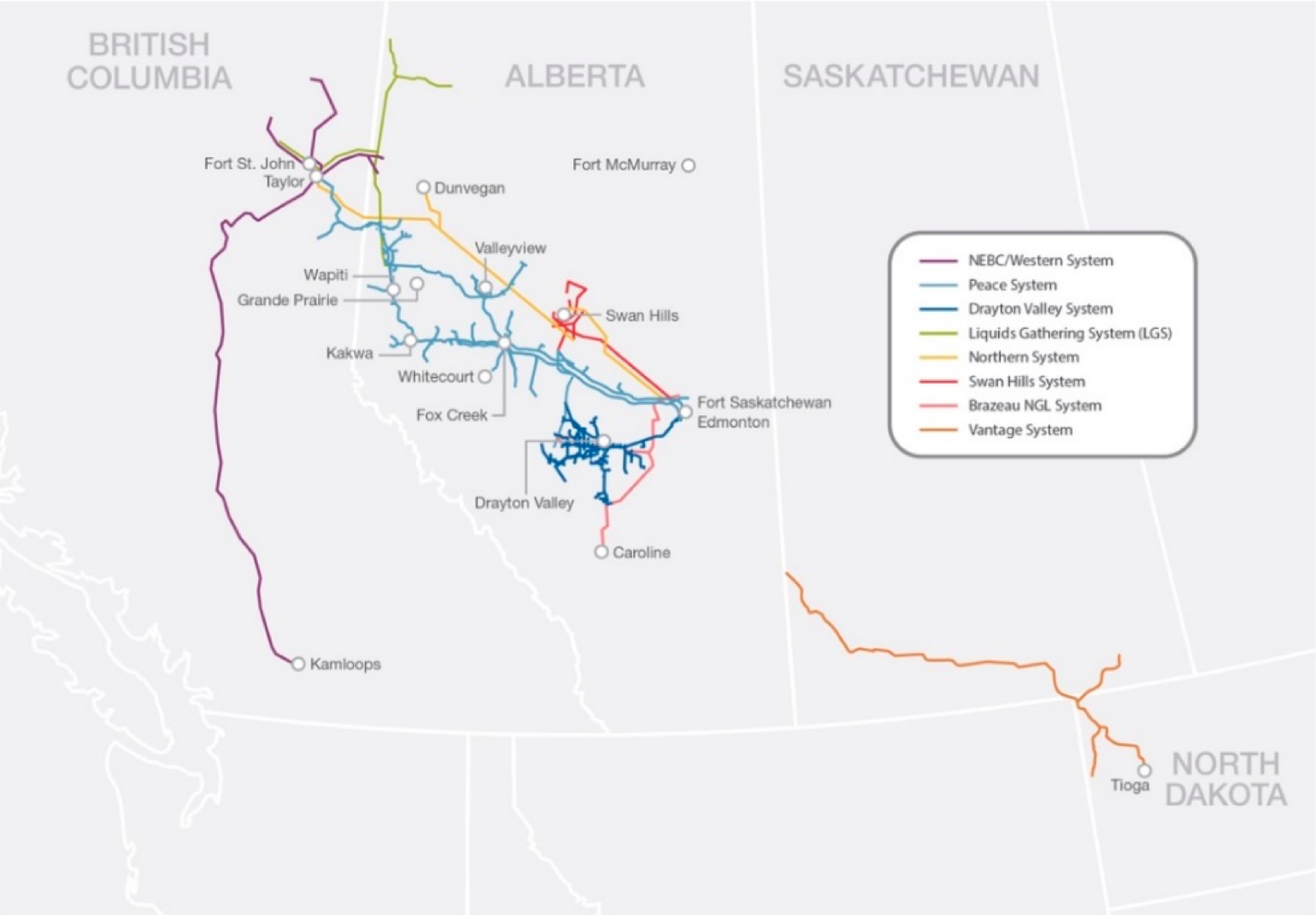

About Pembina Pipeline Corporation

Pembina Pipeline, founded in 1954, is a transportation, midstream, and gas service provider headquartered in Calgary, Alberta. Pembina owns and operates pipelines that transport conventional and synthetic crude oil, heavy oil, oil sands products, condensate and natural gas liquids produced in western Canada and North Dakota. The Company also owns and operates gas gathering and processing facilities, and an oil and natural gas liquids infrastructure business.

Source: Pembina Pipelines

As for FY2016, Pembina has generated C$4.3bn ($3.15bn) in Revenues and Gross Margin stood at C$1.76bn ($1.29bn), which shows a significant impact of production costs (approximately 59% of Revenues); nonetheless, a metric which is encouraging is the EBITDA of the company as it stood at C$1.2bn ($880m). Along with cash flow from operating activities at C$986m ($723bn), a 12% increase YoY, these figures signal Pembina has good cash flow generation and is therefore able to create value for all its stakeholders. This further stands out as it is operating in a depressed industry as the Oil one. As foreseeable, Capex are high at C$1.7bn ($1.25bn) and Financial Debt, C$4.8bn ($3.52bn) for FY2016, accounts for approximately 32.1% of total Assets.

About Veresen Inc.

Veresen is a diversified Calgary (Alberta) based energy infrastructure company founded in 1997, that owns assets in pipelines, midstream, and power. The pipeline business deals with the 3,000 km pipeline extending from Western Canada to the Midwest United States. Its midstream business includes gas extraction facilities near Chicago, Illinois, where the power business is implemented across different regions in both Canada and United States.

Diversification among businesses has been achieved also through a series of acquisitions and Veresen’s business lines include multiple entities: (1) pipeline comprises interests in Alliance Pipeline, the Ruby Pipeline and the Alberta Ethan Gathering System; (2) midstream interests comprise Verense Midstream Limited Partership (which owns a stake in Aux Sable and, through an equity chain, also owns a Natural Gas Liquid –NGL– extraction facility near Chicago and other NGL extraction and processing infrastructures). Veresen is also developing Jordan Cove LNG, a 7.8 million tons per annum natural gas liquefaction facility proposed to be constructed in Coos Bay, Oregon, and the associated Pacific Connector Gas Pipeline.

Prior to the announcement of the acquisition by Pembina Pipeline, Veresen has been implementing multiple acquisition of other power businesses since its foundation, including ownership interests. In 2010, Veresen acquired Swift Power, a hydroelectric power company. In 2014, Veresen announced the acquisition of a 50% convertible preferred interest in the Ruby Pipeline for $1.425bn.

In FY2016, Veresen showed an improvement compared to FY2015 in terms of adjusted net income. As of FY2015, Veresen’s adjusted net income was $59m, compared to $57m in FY2015. Its distributable cash also increased from $310m in FY2015 to $356m in FY2016. Veresen’s future growth in EBITDA seems to be robust, as forecasted to have a run-rate between $725m-$825m, where the EBITDA in 2016 pro-forma power divestiture was $577m. The significant EBITDA growth is expected to drive down the leverage level.

Industry Overview

During the last two years, the energy industry has been characterized by a great deal of uncertainty driven by sustained low prices in 2015, which led to extremely complex market conditions and to a “survival” mindset: starting early 2016, when oil prices reached their record low, capex and headcount have been substantially downsized by many industry players, while borrowing bases dramatically shrank and bankruptcies and debt restructurings proliferated.

These worsened market conditions have been influencing some structural features of the industry, such as the degree of consolidation and the length of its projects. Oil and gas companies shifted towards short-term capital lighter investments and this seems to be confirmed by the $620bn worth of projects which are expected to be cancelled or deferred by 2020. This may imply an energy supply shortage, posing serious threat to global security and industry-wide growth. In order to deal with this crisis, oil and gas companies have lightened their cost structures and enacted large-scale consolidation plans to better face market trends and manage capital requirements more efficiently. Consolidation impacted both upstream and midstream operations, which have been equally affected by market turbulence, downswings in prices and, eventually, financial distress and bankruptcies. On the other hand, in the downstream sector, refined products exports have continued to rise (with an unexpected upturn caused by the opening of new markets), not as strongly as 2015, but still generating satisfying results.

In 2017, an increase in M&A activity, the OPEC’s agreement on production cuts and President Trump’s words on indirectly funding the energy industry by means of some focused tax hikes such as an increase in the federal tax on gasoline all constitute positive signals for the industry.

In particular, Canadian energy companies have been a successful example of this upward trend and this is clearly shown by an increase in the 2016 M&A activity with respect to the 2015 one, which accounted for about $46bn worth of oil and gas deals. It is worth noting that the overall consolidation trend let to a significant concentration in the Canadian market: the 5 largest companies operating in the region indeed accounted for a combined 50% market share.

Deal structure

The Boards of the two companies have unanimously agreed on the merger terms, whereby Pembina will acquire Veresen for an Enterprise Value of C$9.7bn ($7.11bn), including debt and preferred shares. The transaction is expected to close in late Q3 or early Q42017. Besides the approval from the boards of directors of the two companies, the transaction is subject to the approval of 66% of Veresen’s common shareholders.

What is interesting about the transaction, as per Pembina’s press release, is that the bidder is offering two alternative types of consideration: either $18.65 cash or 0.4287 of Pembina common share per each Veresen share. Both considerations are subject to some conditions, namely: a maximum cash consideration of $1.523b or 99.5m Pembina commons shares. According to these limitations, each Veresen shareholder would be entitled to receive, at max, $4.8494 in cash and 0.3172 Pembina shares for each Veresen ordinary share held.

Given the terms of the transaction, Veresen shares are valued at a 21.8% premium to the 20-day average price of $15.31; the premium further rises to 22.5% if the implied share value is compared to the $15.23 closing price on April 28, 2017. Upon completion, Pembina shareholders will approximately hold 80% of the combined entity and Veresen shareholders are expected to own the remaining 20%.

Deal rationale

The rationale for the deal seems straightforward: Pembina Pipeline Corp seeks to consolidate in the face of low commodity prices and high costs. With prices yet to rebound from a two-year slump, pipeline companies have been under pressure to merge as they wrestle with overcapacity and sliding tariffs. Investors have doubted the sector’s ability to generate returns, with no major projects on the horizon beyond a few currently approved ones.

As other recent acquisitions in the Canadian oil and gas industry, this deal constitutes a defensive strategy that will combine energy processing, transportation, and distribution businesses so to provide increased value.

One of the key aspects of the deal is that such a combination will give Pembina access to Veresen’s natural gas pipelines and processing infrastructure. Indeed, most of Pembina’s natural gas liquids, condensate, crude oil and heavy oil assets have a physical connection or are able to be connected with Veresen’s gas midstream infrastructure. The entity that will result from this acquisition will benefit from a strong position in Western Canada’s Deep Basin, Duvernay and Alberta Montney shale basins. As a result, the combined entity will own 5.8 billion cubic feet/day of gas in its processing infrastructure across Western Canada by 2018.

Furthermore, the combination will enable the two firms to better compete and substantially diversifying its respective asset bases amid continued downward pressure on oil prices and margins, making Canadian oil sands a risky business. Nevertheless, the nature of the oil and gas transportation business is such that it may prove to withstand many of these pressures better over time than the producers themselves.

Market Reaction

On the day of the official announcement, Veresen’s shares experienced a surge of about 19%. Moreover, its stock kept rising modestly until converging to a price around C$18.50, signaling investors’ confidence in the potential of the acquisition. On the acquirer’s side, however, Pembina’s stock displayed small fluctuations around the mark of $38/share, indicating neither appreciation nor negative expectations from market participants.

Advisors

Pembina was advised by CIBC World Markets Inc., whereas Scotiabank acted as financial adviser to Veresen.

0 Comments