Introduction

The U.S. housing finance system revolves heavily around government-sponsored enterprises (GSEs), and historically implicit and now explicit government guarantees through Fannie Mae [OTCMKTS: FNMA] and Freddie Mac [OTCMKTS: FMCC]. These entities have historically stabilized and facilitated mortgage lending by providing liquidity and guaranteeing mortgage-backed securities (MBS). However, following their dramatic bailout and conservatorship during the 2008 financial crisis, debates around their future particularly the possibility of privatization have resurged.

Parallel to this narrative, Rocket Companies emerges as a transformative force reshaping real estate through aggressive acquisitions and technological innovation. This article explores both the legacy institutions of Fannie Mae and Freddie Mac, alongside the disruptive rise of Rocket Companies, highlighting critical turning points and strategic decisions shaping the future of U.S. real estate.

Mortgage Market Overview

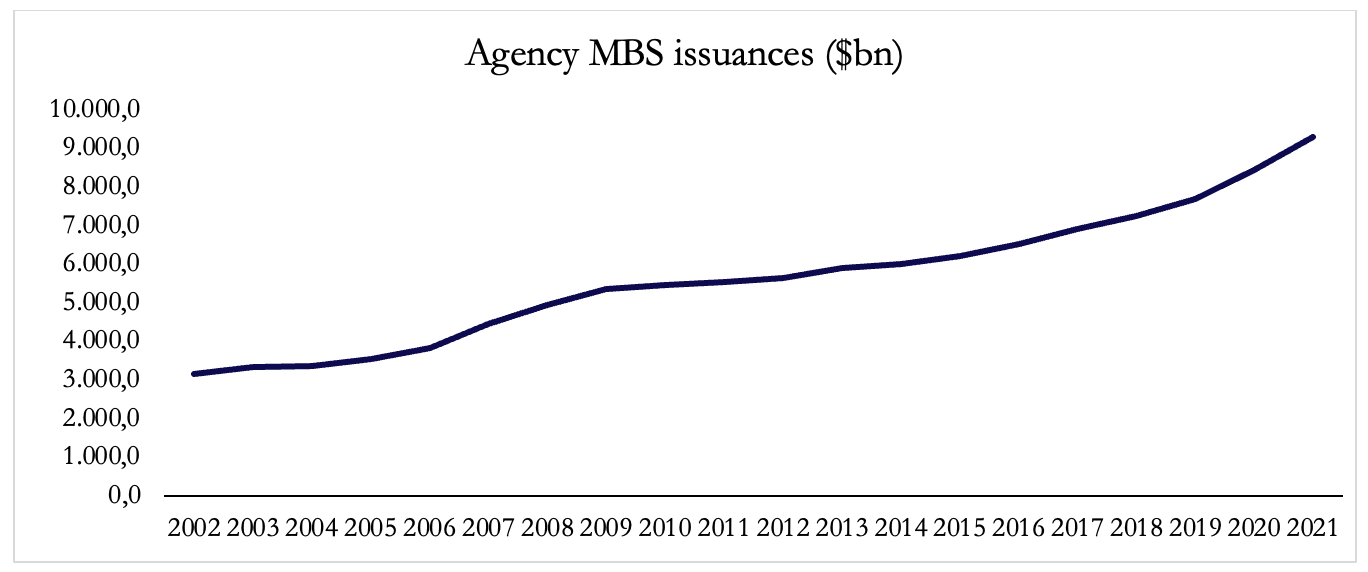

Mortgages are a unique facet of the overall fixed income market, As the Treasury market represents the debt of the U.S. government, the mortgage market represents U.S. household mortgage debt. Mortgages were one of the first products to be securitized, Securitization began in the mid-1980s with residential mortgages but over time grew beyond its original roots to affect just about every fixed income market. Large pools of mortgages combined into a single security are known as mortgage-backed securities (MBS).

Since every mortgage security is a pool of possibly hundreds of individual home loans, each such pool may have unique credit characteristics depending on the location, credit score of buyers etc. There are some features to standardize mortgages. The first is that they are government backed by government. Agency mortgage-backed securities (MBS) are backed by government-sponsored entities Freddie Mac and Fannie Mae, which guarantee a large share of U.S. mortgage loans. To qualify, loans must meet certain standards, including size limits that vary by market. Before the 2007 financial crisis, these guarantees were only implicit, but when the government placed the agencies into conservatorship, they became explicit.

Despite evolving regulations, support for Agency-backed mortgages remains strong due to their critical role in the housing market.

One key feature of the U.S. mortgage market is that homeowners can prepay or refinance their mortgage at any time without penalty. Refinancing means using a new loan—usually at a lower interest rate—to pay off an existing one. For example, if a homeowner has a 30-year fixed-rate mortgage at 5% and interest rates fall to 3%, they may choose to refinance to reduce monthly payments. If rates rise, they have no obligation to refinance and can continue benefiting from their lower rate. This flexibility creates an option-like feature for homeowners: they benefit when rates fall but are protected when rates rise.

For investors holding mortgage-backed securities, this optionality creates uncertainty. Unlike a standard bond with fixed payments and maturity, a mortgage bond can be paid off early if the homeowner chooses to refinance. When interest rates drop, investors may lose higher-yielding cash flows as loans are prepaid and they’re forced to reinvest at lower rates. This limits price appreciation compared to traditional bonds. If rates rise, the mortgage behaves more like a long-term bond, as homeowners have no incentive to prepay. This negative convexity exposes investors to interest rate risk, so they typically demand higher yields to compensate for this asymmetry.

Finally, before delving into the companies further it is interesting to look at how Freddie Mac and Fannie Mae take out debt. These agencies not only guarantee mortgages but also hold an enormous portfolio of mortgage debt on their balance sheets. To fund these assets, the agencies issue debt into the broader market, known, not surprisingly, as Agency debt. The Agency debt market is $2.7 trillion currently and includes debt from smaller government entities, such as the farm credit agency.

Unlike the Treasury market, the Agency debt market is composed of a wide variety of bonds ranging from plain bonds, known as bullets, to more complex structures, known as callables. Callables are essentially the same concept as the mortgage bonds described earlier, but instead of the homeowner, it is the agency that has the right, but not the obligation, to prepay the bond to the investor.

Freddie Mac & Fannie Mae

Fannie Mae [OTCMKTS: FNMA] and Freddie Mac [OTCMKTS: FMCC] play a key role in keeping the U.S. housing finance system running smoothly by ensuring that mortgage lenders always have access to funding. By buying mortgage guarantees from banks and other lenders, they provide those lenders with fresh capital to issue more home loans. Importantly, neither entity originates mortgages; instead, they purchase loans and guarantee them. Fannie Mae and Freddie Mac either retain the mortgages on their balance sheet or bundle them into mortgage-backed securities (MBS), which are sold to investors. By guaranteeing timely payments on these MBS, the two companies make investing in mortgages more attractive and secure, ultimately expanding the housing market. Besides enhancing liquidity, this also plays a role in promoting affordable housing by lowering borrowing costs for homebuyers and renters. During times of financial stress, their continued support in the housing market can help stabilize the entire housing market.

The overarching policy goal in the United States has long been to support homeownership by enabling borrowers to access mortgages on generous terms, typically meaning 30-year fixed-rate loans with interest rates just above Treasury yields. Hence, Fannie Mae was established in 1938 during the Great Depression by Congress to help boost homeownership. Freddie Mac was chartered in 1970 by Congress as a private company, and in 1968, Fannie Mae was also converted into a private company while still retaining an implicit government backstop. Over the decades, a hybrid system emerged where the government neither guaranteed mortgages nor left the two companies entirely to privatization.

Fannie and Freddie were so-called government-sponsored enterprises (GSEs), allowing the banks to swap risky loans for government-sponsored securities. The crux was that these securities were never government obligations that were fully backed, although the heavy regulation and the perception of them made them seem like they were.

During the financial crisis

Fannie Mae became the largest U.S. company by assets, and both entities were regulated by the Federal Housing Finance Agency (FHFA). The trust in the two companies solidified, and investors believed that if something were to happen, the government would step in to prevent a failure. That proved to be accurate during the 2008 financial crisis. Before the crash, the U.S. housing and mortgage markets had become increasingly distressed. Despite maintaining high standards in their core guarantee business, Fannie Mae and Freddie Mac had invested in subprime MBS via their investment arm. By June 2008, their combined capital stood at just around 1% of their exposure, an insufficient buffer to absorb the losses ahead. Their stock price had also fallen from $60 in July 2007 to below $10 by July 2008. Both companies had accumulated massive losses from credit defaults and poor investments, and the financials showed that. By the time the crisis was in full swing, they were ultimately deemed too large and interconnected to fail.

The government called a bailout to preserve the flow of conforming mortgages, support refinancing during a housing downturn, and prevent broader financial instability in the U.S. and globally.

Without government intervention, concerns over the creditworthiness of debt instruments issued by GSEs could have triggered a systemic crisis as the volume of the assets held by the lenders was immense. By September 2009, both companies had been placed under conservatorship under the FHFA, and the regulator took control of the management to stabilize operations and guide their path toward solvency. The U.S. Treasury agreed to provide financial support via Senior Preferred Stock Purchase Agreements. Under this bailout, the Treasury committed a total of $187.5bn in exchange for a ten percent annual dividend and warrants to acquire 79.9 percent of each company’s stock at no cost. While technically structured as equity, this infusion of capital functioned much like loans with a principal and an annual interest rate of ten percent. As their stock prices fell below $1, they were delisted from the New York Stock Exchange but continued to be traded over the counter (OTC). As the crisis lingered in the housing market, the following years were difficult for Fannie and Freddie, and they could not generate the income to pay the ten percent dividend. Forced to draw more support from the Treasury, this became a vicious and unsustainable cycle.

In 2012, the Treasury and FHFA implemented the Third Amendment to the bailout agreement. Instead of paying this fixed dividend, both companies would now transfer their entire net income to the Treasury, whether more or less than the dividend amount agreed upon. What became known as the “net worth sweep” initially relieved the companies from the burden of the fixed dividend payment and soon revealed the side effect of preventing them from building up capital reserves. As the housing market recovered and profitability returned to Fannie and Freddie, they were barred from retaining their earnings, making it impossible to repay the principal amounts or prepare an exit from the conservatorship. That year, they earned $16 billion in combined net income after dividend payments, all of which was swept to the Treasury. Shareholders who had held on during the crisis and were now being left out became agitated and started filing lawsuits. While they did not work out in the intended way, they drew attention to the fact that the government had been repaid more than it initially invested. By the end of 2014, Fannie Mae had paid $134.5 billion in dividends to the Treasury compared to $116.1 billion in draws, while Freddie Mac had paid $91 billion against $71.3 billion drawn. Fast forward to 2021, when the companies were finally allowed to retain their earnings again to build capital. However, they were still not permitted to pay back the principal amounts owed to the Treasury, which continued to count as part of their obligations.

Recent developments

In late 2024 and early 2025, the conversation around Fannie and Freddie intensified once again, largely due to renewed investor interest. By January 2025, Fannie’s stock had soared 227% following the election of President Trump. The catalyst of this surge was the hedge fund manager Bill Ackman, who publicly revealed his stake in the company on his social media in December 2024. His strategy was to buy shares at depressed prices in anticipation of future privatization, arguing that the government would eventually unwind its ownership under President Trump’s deregulation movements. Ackman had made a similar bet over a decade earlier, though at the time, it proved premature. This time, he might still be early, as any transition is expected to be a lengthy and politically sensitive process. Nevertheless, his announcement caused a spike in share prices and renewed speculation about the companies’ future.

The balance sheets of Fannie and Freddie reveal that both still owe more than their equity currently accounts for, and they are still far from paying off their Treasury “debt.” However, supporters of privatization argue that if dividend payments to the government are treated as repayments of the original support, the companies have already covered their debts. Fannie Mae borrowed $119.8 billion and has paid back $181.4 billion, while Freddie Mac borrowed $71.6 billion and has returned $119.7 billion. Under this accounting interpretation, the path to privatization appears more feasible, and the firms seem closer to being viable independent entities. On the other hand, the primary argument against privatization is that the government would not want to miss out on the remaining $341bn of taxpayer money. This might be the only viable way to ever return the companies to privatization and potentially the world’s largest IPO with Fannie Mae. Instead of a full write-down, the senior preferred shares could also be converted into common equity, thereby maintaining taxpayer value while unlocking the potential of a public offering.

From an enthusiastic point of view, Ackman predicts that both companies could go public in Q4 2026, with share prices at approximately $31, which would represent a return of roughly 1,200 percent from his average purchase price of $2.40. He also estimates that the privatization could generate around $300 billion in profits for the government. Other hedge funds, such as Discovery Capital Management, which has held the shares for over a decade, and PointState Capital, a holder of preferred stock, are similarly positioned and have similar interests in the matter. Nevertheless, the final hurdle remains the trust issue. Releasing Fannie and Freddie into full privatization without any form of government guarantee could severely undermine confidence in the mortgage sector. Given the size and systemic importance of the GSEs, any misstep could shake an already fragile housing market. The government must tread carefully, as the question of who has priority, taxpayers, investors, or market stability, is delicate and consequential.

Rocket Companies: The Emergence of a New Real Estate Juggernaut?

While Fannie Mae and Freddie Mac have long provided foundational stability to the U.S. housing finance system through government-sponsored mortgage guarantees, their recent struggles and uncertain path toward privatization have created an opportunity for private sector innovation. Stepping into this evolving landscape is Rocket Companies, a firm leveraging technology and aggressive acquisitions to redefine homebuying and mortgage servicing. Rocket’s disruptive strategy aims not just to complement but potentially replace traditional lending models dominated by entities like Fannie Mae and Freddie Mac, signalling a transformative shift toward integrated, tech-driven real estate platforms.

A powerful new player emerging in the housing industry, one that could soon rival Zillow’s dominance. Rocket Companies, best known for its mortgage lending through Rocket Mortgage, is rapidly expanding its reach across the real estate ecosystem through a series of major acquisitions.

These moves hint at a bold strategy: to unify the entire homebuying journey under one brand.

Rocket Companies, founded in 1985 by Dan Gilbert as Rock Financial, started as a traditional mortgage lender. It was one of the first to embrace online lending in the late ’90s, helping it stand out in a crowded market. After briefly being part of Intuit, the company was reacquired by Gilbert and later rebranded as Quicken Loans. In 2015, it launched Rocket Mortgage, marking a shift toward a fully digital mortgage experience. By 2020, Rocket Companies went public and now oversees a portfolio of businesses including Rocket Mortgage, Rocket Homes, and Rocket Loans.

Rocket Mortgage has become a go-to choice for homebuyers, thanks to its tech-forward approach and consumer-friendly features. Here are some of the key benefits:

- Low Down Payment Option: Through its ONE+ program, eligible buyers can put just 1% down, with Rocket covering the other 2%. Mortgage insurance is included at no extra cost.

- Down Payment Assistance: First-time buyers in select metro areas can qualify for up to $7,500 in grants to help with down payments and closing costs.

- Fast, Tech-Driven Process: Thanks to a proprietary AI platform, Rocket can close loans about 2.5x faster than the industry average.

After its rebrand from Quicken Loans, Rocket heavily focused on consumer-facing marketing—it became a household name during the Covid-fueled refinance boom and, by 2021, became the largest mortgage originator in the United States. However, between 2021 and 2023, refinance volume collapsed by over 85% and Rocket’s originations fell from $351bn in 2021 to a mere $78bn in 2023. To turn around its recent poor performance, Rocket is playing a new hand. Earlier this year, Rocket announced a $1.75bn all-stock deal to acquire Redfin, following closely on the heels of a $9.4bn deal to acquire mortgage servicing giant Mr. Cooper. The vision is clear—Rocket is aiming to create a seamless, vertically integrated real estate experience where buyers can browse listings, get financing, and manage their loans all in one place.

The acquisition of Redfin, a real estate listing app, gives Rocket immense capabilities at the top of the funnel. With roughly 50m monthly users along with a national brokerage infrastructure, Redfin allows Rocket to capture potential homebuyers before they even begin looking for loans. Although Redfin has struggled with profitability, reporting a net loss in 2024 of over $164m, its strong brand recognition and rich housing data brings Rocket one step closer to offering a fully integrated homebuying journey to consumers. However, Rocket must be weary as building a US super app is easier said than done. Zillow had announced plans to create one in 2022, which it projected could deliver $5bn in revenue and a 45% adjusted EBITDA margin by 2025. Last year, it only managed results half of these projections.

Rocket’s acquisition of Mr. Cooper is the crown jewel of this new strategy. Through the acquisition, Rocket gains access to a $1.6tn mortgage servicing portfolio and a 6.7m customer base. The most important aspect to consider is the steady, recurring cash flow that Rocket will generate from Mr. Cooper’s loan servicing business. Rocket’s core origination business came under pressure between 2021 and 2023 on the flipside, Mr. Cooper’s servicing stability generated $1.4bn in net income in 2023. The deal also significantly lowers Rocket’s customer acquisition costs: instead of spending millions on advertising, the company gains millions of built-in customer relationships that it can build upon.

Jay Bray, CEO of Mr. Cooper, predicted this wave of consolidation. Speaking in late 2024, he pointed out that survival in the industry now requires scale, innovation, and a strong balance sheet.

“You’ve seen consolidation already,” Bray said. “If you think about this industry going forward, you’re going to need a balanced business model. You’re going to need the capability to invest in technology, to use everybody’s favourite two initials: AI. That requires scale, that requires capital, that requires a healthy balance sheet.”

Rocket CEO Varun Krishna also emphasised the long-term value of the Mr. Cooper deal, particularly its role in extending Rocket’s customer relationships far beyond just the initial mortgage.

“Servicing is a critical pillar of homeownership alongside home search and mortgage origination,” Krishna said. “With the right data and AI infrastructure we will deliver the right products at the right time. That’s how we build lifelong relationships, by proactively unlocking benefits and meeting needs before they arise.”

Rocket’s recent acquisitions are paving the way for a new type of real estate and mortgage powerhouse. If these deals close as anticipated, Rocket will handle about one in every six mortgages in the U.S. through Rocket Mortgage. In addition, the company will have control over title and closing services through Amrock, and offer home and auto insurance, as well as personal finance tools through Rocket Money. With these moves, Rocket will be able to reach millions of Americans across various platforms. This highly integrated, data-driven strategy focused on leveraging technology to establish long-term customer relationships shares many parallels with Amazon’s business model.

Furthermore, Rocket’s approach is not just about scale, but about redefining convenience in real estate. While competitors like CoStar have spent heavily to promote their platforms—such as the $1 billion Homes.com campaign—some industry voices argue that Rocket is executing a more disruptive strategy by quietly buying up the entire infrastructure of residential real estate.

Amanda Orson, CEO of real estate startup Galleon, observed, “It’s becoming increasingly clear that Zillow’s true competition isn’t CoStar it’s Rocket… They’re buying the full residential real estate stack.”

By uniting home search, financing, and servicing, Rocket is positioning itself to guide homeowners from their first online listing view all the way through decades of mortgage payments. It’s a bold move one that could change not just who dominates the industry, but how the entire process of buying and owning a home is experienced.

Conclusion

The future of the U.S. housing finance system sits at a crossroads. On one side are legacy institutions like Fannie Mae and Freddie Mac, still navigating their post-crisis conservatorship and facing growing pressure to return to privatization. On the other is Rocket Companies, a bold, tech-driven disruptor redefining how Americans buy, finance, and manage their homes. While GSEs continue to underpin mortgage market stability, Rocket’s integrated approach signals a shift toward consumer-centric innovation. Whether the future favours government-backed continuity or private-sector reinvention, one thing is clear: the housing market is entering a new era one shaped as much by regulation as by disruption.

References

[1] W. Scott Frame, Andreas Fuster, Joseph Tracy, James Vickery, “The Rescue of Fannie Mae and Freddie Mac”, 2015

[2] SIFMA. (2024). US Mortgage-Backed Securities Statistics. [online] Available at: https://www.sifma.org/resources/research/statistics/us-mortgage-backed-securities-statistics/

0 Comments