Introduction

A leveraged buyout is the acquisition of a company, either privately or publicly held, using borrowed funds to pay for the purchase price of the company. The main actor of a leveraged buyout transaction is a private equity firm or group of private equity firms, which will own the equity of the acquired company after the purchase has been completed. The acquisition of the target company is financed through a combination of equity capital and debt instruments; debt will constitute most of the purchase price, typically from 50% to 70%. As a result, the cash flow generated by the acquired company is used to pay interest and principal on the outstanding debt. Multiple financing sources are commonly used to finance LBOs and the main can be listed in the following descending order of seniority: Debt, Mezzanine capital and common equity. This article, besides providing an overview on the financing structure of an LBO, will focus on the less well-known mezzanine capital and its usage in controversial practices employed by PE firms.

LBO Financing Structure

Senior-secured debt constitutes the most senior and therefore cheapest form of financing. It mostly consists of bank debt which typically makes up 30-50% of the capital structure and it will usually also include a revolving credit facility (“Revolver”) to fund working capital needs. A revolver is used by companies to the credit limit when they need cash and it is repaid when excess cash is available (there is no repayment penalty). Bank debt, other than revolving credit facilities, generally takes two forms: Term Loan A, amortized evenly over 4 to 7 years, and Term Loan B, which involves only minimal or no nominal amortization over 5 to 8 years, with a large bullet payment in the last year. Bank debt has the lowest cost-of-capital but compared to other sources of financing it has more onerous covenants and limitations, such as financial maintenance covenants. Covenants generally restrict a company’s flexibility to make further acquisitions, raise additional debt, and make payments to equity holders (e.g. dividends). Moreover, bank debt typically requires full amortization (payback) over five to eight years.

As the next component, second-lien debt can be employed to receive more low-cost funding. It is a subtype of senior-secured debt and only subordinated to first-lien debt. Its importance has grown over recent years and, indeed, leveraged buyouts were the largest driver of second-lien loan volume growth. Second-lien loans can be used to partially replace unsecured HY bonds for several reasons, including the favorable call profile typical of leveraged loans relative to bonds, which provides issuers with significant flexibility to address their capital structure in the future. It is mostly provided by private debt funds and investment banks.

High-yield debt, typically unsecured and subordinated, is named so because of its peculiar high interest that compensates investors for holding such risky debt. Subordinated debt may be raised in the public bond market or the private institutional market, carries a bullet repayment with no amortization, and usually has a longer maturity than bank debt (8 to 10 years). HY debt usually also has different types of covenants, the incurrence covenants, which only take effect if the borrower is taking a specified action. Interests is paid in cash, same to the previous presented forms of debt.

Mezzanine capital, which will be in the focus of this article, ranks last in the seniority of a company’s outstanding debt, and is often financed by private debt funds and hedge funds in search for high yields, especially in nowadays’ low-interest rates market. Mezzanine financing is sometimes referred to as quasi-equity, or equity-like debt. Mezzanine capital can be primarily found in the form of high-yield debt coupled with warrants (options to purchase stock at a predetermined price), known as an “equity kicker”, to boost investor returns to levels proportional with risk. Furthermore, it often allows to pay interest in the form of additional debt (PIK), which will be explained later in more detail.

Finally, common equity represents the most junior tranche of the capital structure and is provided by private equity funds (called financial sponsors) and in some cases supplemented by the target company’s management (management buyout or management buy-in). Equity capital is typically around 20-35% of the notional value of the capital structure. Equity holders require a large projected internal rate of return on investment, typically in the range of 20% to 40%, because the company is so heavily leveraged at acquisition.

Mezzanine capital

Mezzanine capital is a financing method for businesses and private equity firms, ostensibly similar to subordinated and unsecured debt but closer to equity in nature thanks to some distinguishing features. First, it is subordinate to other forms of debt when it comes to obligations of the borrower, which means should the company go bankrupt or get liquidated, mezzanine capital holders are the last ones, before the equity holders, to get reimbursed. Therefore, to attract investors, it has to yield a higher return, standing usually at around 10-20%. Secondly, it often includes an alternative for the lender, an option to purchase common stocks, called “warrant”. As a result, interest is not the sole source of return, which will be discussed in further depth. Thirdly, financing can be structured both as a debt (PIK notes, convertible debt) and as preferred stock, giving options on how to reflect it on the balance sheet.

There are 3 main ways a Mezzanine holder generates return:

- Interest, usually at a fixed rate; can be in the form of cash interest or “payment-in-kind” (PIK) interest. In the latter form, the interest owed is accrued and becomes part of the principal owed. Therefore, it is paid with additional debt.

- Equity “kickers”, which are tools for lenders to turn, in whole or in part, their investment into equity. One such tool is the aforementioned warrant, working identical to a stock option. It is mostly independent from the debt put through, which does not decrease as a result of the options being exercised. Warrants are usually exercised in the event of a big stock transaction, like entry of new investors or an IPO. Another one is the conversion feature, which allows the lender to convert the debt into equity, which results in an increase in the number of shares outstanding and a decrease in the debt owed to the lender. A third tool is co-investment, essentially the right to buy a minority stake alongside the majority shareholder, such as a Private Equity fund. This tool is utilized widely during LBOs.

- As prepayment protection, a repayment premium is usually added to the outstanding amount if the mezzanine debt is refinanced in the initial years.

Due to its high costs, mezzanine capital ist mostly used in risky transactions to attract more aggressive investors. It is widely used by PE firms in LBOs, along with other securities, to finance large or risky acquisitions as the amount of more senior debt is limited. Furthermore, companies might use mezzanine funding not only for large acquisitions but also for risky growth projects. Another area of use is real estate, where it is used by developers to secure additional funding for development projects.

From both the lender’s and borrower’s perspective, Mezzanine has its upsides and downsides. To the lender, Mezzanine offers the advantages of equity investment in the form of high returns. Additionally, the equity kickers provide a way of changing your position in the financing structure, acting as a tool to participate in high growth. However, mezzanine is a very risky type of debt and therefore it does not offer much protection against total bankruptcy. It also generates returns very late due to long maturities and the usage of PIK interests.

For the borrower, one significant advantage of mezzanine capital in the form of debt is that it offers an equity-like investment without the need to pay dividends, which are, unlike the interest payment, not tax-deductible. Moreover, the opportunity to defer interest payments, thanks to PIK interests, provides a high degree of flexibility to the borrower. Contrary, the potential dilution arising from the exercise of equity warrants has to be mentioned as a drawback. Particularly during high growth, debt holders will have an incentive to participate in the firm’s ownership, resulting in an increase in shares outstanding, therefore a decrease in the current shareholders’ ownership percentage. Furthermore, the high interest rate presents a heavy burden.

Payment-in-kind

Payment-in-kind refers to mezzanine instruments that pay interest or dividends to investors of bonds, notes, or preferred stock in forms other than cash. Usually, the payment of interest is made by issuing additional debt. Therefore, the interest is capitalized and added to the principal at the end of each period. Upon maturity or refinancing, the total amount of the original loan plus the accumulated PIK debt issued is repaid.

For PIK loans, the choice between PIK interest and PIK interest can be mandatory or optional. So-called true or mandatory PIKs require a payment of interest solely in-kind or according to a predetermined split between in-kind and cash. More interesting instruments for the borrower are the so called PIK toggles, known as “pay if you want”. It allows the borrower to change the proportion of interest payment that is paid in cash and in-kind every period. When a borrower toggles the interest towards PIK, the interest rate also rises significantly. PIK toggles support a highly variable rate of payment and, depending on the contractual terms, often both parties are allowed to change loan terms midway. Sometimes certain conditions must be fulfilled to pay interest in-kind. Therefore, they are referred to as “pay if you can”. The interest on PIK loans, especially with mandatory PIK, is substantially higher compared to conventional debt in order to compensate for the high risk and to make this financing instrument attractive for the lender. Because of this, such loans are pretty expensive for the borrower. The re-emergence of PIKs underscores how investors are increasingly being asked to accept higher degrees of risk and more onerous terms from bond or loan issuers as soaring prices of higher-quality assets in recent years have deeply depressed yields.

Issuing PIK instruments is an option for many companies that experience cash flow or liquidity problems but have the capacity to issue additional debt. They are especially attractive to companies preferring not to make cash outlays, such as during a leveraged buyout or during a growth phase of the business. In order to protect their liquid assets, companies pay their liabilities with the help of new liabilities. This allows financially distressed companies to find some relief in the more immediate term and free up some cash for other, more necessary areas.

Nonetheless, the PIK mechanism is seen as very controversial. On the one side, it is very risky for investors. The loans do not generate any cash flow before maturity. They are unsecured, meaning that they are not backed by a pledge of assets, and subordinated to conventional debt and only senior to equity. They tend to lead to a total loss in the event of a default. On the other side, companies issuing PIKs are in the danger of becoming overleveraged. Adding interest to the firm’s existing debt load might solve temporary liquidity problems, but it can increase the debt burden massively and only pushes the obligation into the future. On top of that, it is not easy to refinance PIK loans due to the inherent risks and if it is possible it comes at a high cost due to repayment premium. Moreover, the major critique point is the usage of capital raised as PIKs are often used to finance dividend recapitalizations.

Leveraged dividend recapitalization

Dividend recapitalization is a type of recapitalization that involves the issuing of new debt, that is then used to pay a dividend to private investors or shareholders. Therefore, the recapitalization directly impacts the company’s capital structure since it increases its leverage by reducing equity financing in relation to debt financing. Since banks are not inclined to lend money for the sole purpose of paying out dividends, dividend recaps are mostly financed through high yield or mezzanine debt, and especially PIK loans. Additionally, as PIK allows to pay interest in a form other than cash, the cash that has been saved can be used to pay further dividends. A variation of dividend recapitalization is called leveraged share buyback and involves a company repurchasing some of its own shares by issuing debt.

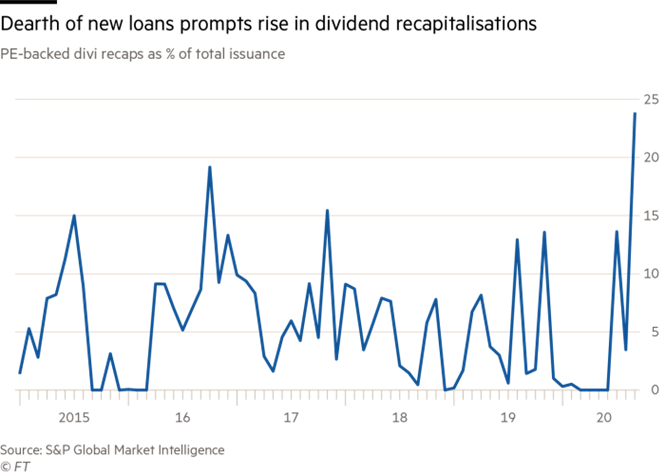

Private equity investors often use the dividend recap technique to receive cash earlier and to increase their return. Furthermore, they can be used as a tool to optimize the funding structure of the portfolio company if the company has low leverage. As a further advantage, interest payments are tax deductible. As of September 2020, almost 24% of money raised in the US loan market had been used to fund dividends to private equity owners, up from an average of less than 4% over the previous two years.

Source: Financial Times

In general, this strategy can have several beneficial scenarios. First, It can be used by a PE firm to exit an investment. In such a case, dividend recapitalization is a viable alternative to conventional exit routes such as a sale of the stake to another private equity firm or an IPO. Secondly, it can be used to recover an initial investment. The reason being that there are situations when an investor wishes to recover its initial investment without losing its stake in a company. Thirdly, it is a way to avoid using earned profits for dividends. If the company needs capital for its growth strategy, leveraged dividend recaps can eliminate the necessity to use its earned profits to distribute dividends to shareholders.

Dividend recaps are mostly used by private equity firms, but the usage is controversially discussed. The debt to pay the special dividend, in addition to not funding the portfolio company’s growth, weighs further on its balance sheet in the form of leverage. Significant new debt might become a drag in adverse market conditions, following the company’s exit. The higher probability of default on financial obligations may potentially lead to financial distress and, ultimately, to bankruptcy. The practice is generally not looked upon favorably by creditors and shareholders who are not entitled to receiving a special dividend, as it reduces the credit quality of the company while benefiting only a select few. There are several cases where dividend recaps had negative effects on the portfolio companies such as Phones4u, a former British mobile phone retailer. In 2014, while the company was part of the portfolio of BC Partners, the PE investors raised more than £200 million with PIK toggles in the debt market to pay out to themselves a special dividend. While the PE firm received back 130% of its initial investment, Phones4u was left with a 4x leverage with respect to EBITDA that forced the company into bankruptcy just one year later. Another case is Edscha, a German car parts maker. Carlyle levered the company in 2005 and paid itself €60m of dividends. After the financial crisis in 2009, the company with a 139-year history filed for bankruptcy. It was finally split-up and sold to competitors.

However, research shows that those deals have not led to a higher proportion of bankruptcies. But dividend recaps are controversial because they allow private equity owners to extract profits quickly and eliminate risk from a deal, while often leaving portfolio companies in a more precarious financial position. Due to pressure coming from the financial world, private equity firms are more cautious and undertake thorough due diligence to ensure that the company is suitable for dividend recapitalization and possesses sufficient capacity to take on more debt on its balance sheet. Lastly, as long as interest rates will stay low and investors will continue to provide capital, no reversal of this trend is in view.

0 Comments