USA

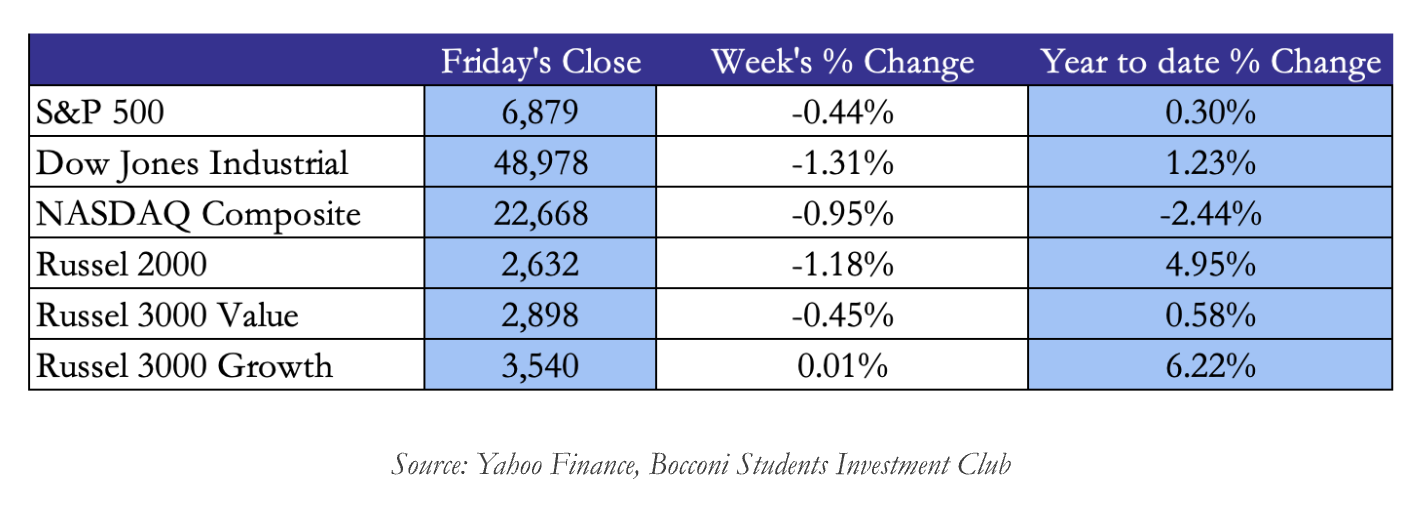

US capital markets opened the week lower due to tariff uncertainty. The Supreme Court on Friday 20th ruled Trump’s use of International Emergency Economic Power Act (IEEPA) to enforce tariffs as illegal. The ruling overall appeared to be relatively priced in by the markets as Vix still remained within 1 standard deviation of its average. Trump swiftly responded invoking section 122 of the 1974 Trade Act, which allows for Presidents to impose levies up to 15% for up to 150 days on all countries before needing Congress’ approval. The need for the US Administration to resume its tariff collection scheme ties to its primary balance conundrum, the US Tax Foundation estimates that tariffs had already raised more than $160 bn since Liberation Day, the loss of this source of revenue could potentially widen an already challenging deficit.

On Monday a research report concerning the disruptive capabilities of AI to various industries and the broader economy amplified the worries about AI driven disruption risks. On Wednesday as the lead of the pack NVIDIA Corp (NASDAQ:NVDA) reported earnings, the result was an earnings beat, however the stock price didn’t move significantly. Some analysts have raised concerns over the cash flow generation state of the company; some have pointed out to the lack of forward guidance and some other have stated that when you’re the biggest company in the world it’s difficult to please the market. NVDA followed the market’s negative trend on Friday losing 4.04% from the previous day’s close.

On Friday investors saw a hotter than expected Producer Price Inflation reading. The headline PPI increased 0.5% MoM ahead of estimates of 0.3%, the upshift was mainly driven by services prices which rose 0.8% MoM. On an annual basis, PPI inflation came in at 2.9%. Some components such as domestic airlines and healthcare, which are considered when calculating the PCE price indexes increased solidly last month. The PPI came in as a surprise as highlighted by the selloffs on Friday and complicates significantly the estimation of a policy path for the upcoming FOMC meetings. The current base case for a cut is highlighted as the June meeting with the ZQN6 contract trading at 96.54, however many analysts have shown discomfort and aren’t expecting a cut in the first half of the year.

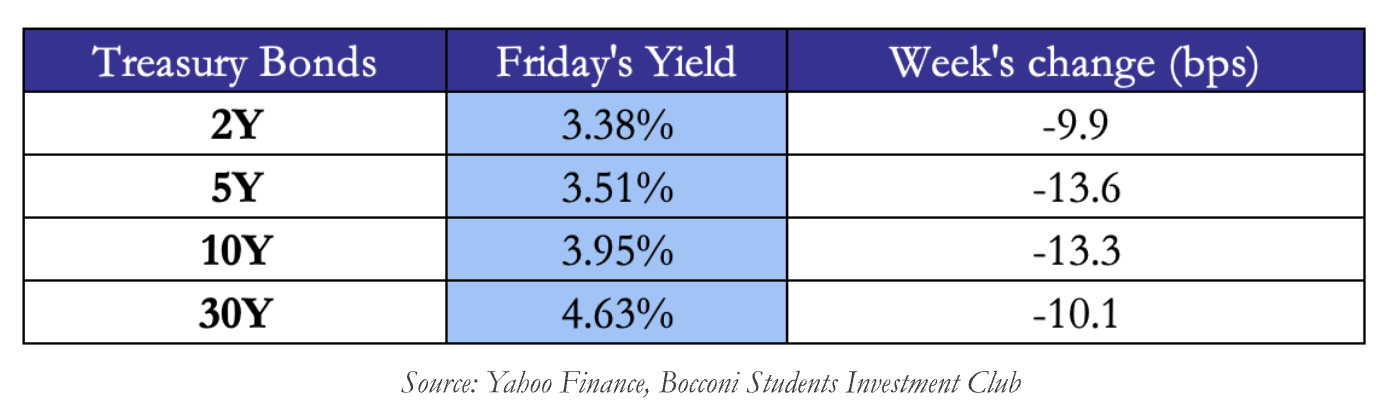

US Treasuries advanced during the week, with the 10Y yield below 4% for the first time since November. The effect was a bullish flattening of the curve as investors sought safety following the week’s broad risk-off sentiment. Investment grade corporate bonds also saw some modest gains, however, underperforming Treasuries. High yield corporate bonds performance was mixed amid AI-related volatility. Interestingly during the week, the average rate for a 30-year fixed mortgage fell under the 6% threshold, the lowest level since September 2022, with lenders and real estate agents saying the drop could lure more buyers into the market and spur a jump in refinance applications for homeowners who bought when rates were higher.

US Treasuries advanced during the week, with the 10Y yield below 4% for the first time since November. The effect was a bullish flattening of the curve as investors sought safety following the week’s broad risk-off sentiment. Investment grade corporate bonds also saw some modest gains, however, underperforming Treasuries. High yield corporate bonds performance was mixed amid AI-related volatility. Interestingly during the week, the average rate for a 30-year fixed mortgage fell under the 6% threshold, the lowest level since September 2022, with lenders and real estate agents saying the drop could lure more buyers into the market and spur a jump in refinance applications for homeowners who bought when rates were higher.

Europe and UK

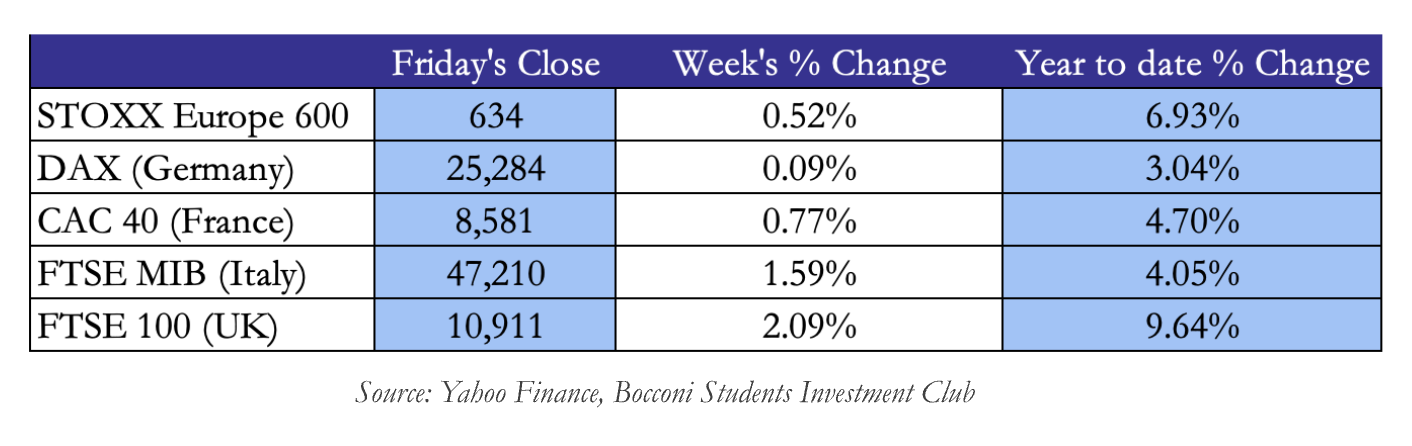

The pan-European index, STOXX Europe 600, touched new highs, continuing the global trend of diversification from US Tech Equities and strong corporate earnings spurring the rise. The upswing was driven by gain in the Utilities, Communications sector, and Technology services.

In Germany the Ifo Business Climax Index rose to 88.6, reaching its highest level since last summer. The higher confidence was broad among the survey, with both manufacturers and service providers reporting higher confidence.

In France, the reading from the main confidence indicator fell to 97 from 99 in January, signalling a lack of optimism for the economy which has, in the meantime, found a PM in Sebastien Lecornu and has approved the budget earlier this month.

Italy continues its historical rally, almost reaching historical highs seen in early 2000s, during the week the biggest gainers were Stellantis [BIT:STLAM] and Nexi S.P.A. [BIT:NEXI] while the worst performers were Brunello Cuccinelli [BIT:BC] and Leonardo [BIT:LDO]. Interestingly during the week shares in Banco Monte Dei Paschi [BIT:BMPS] and Mediobanca [BIT:MB] fell sharply following the presentation of the multi-year strategy for the combined group which unsettled investors due to the lack of detail in terms of the full merger.

UK’s index, FTSE 100, had a steady increase during the week following BOE governor Andrew Bailey’s dovish statement, possibly supporting another interest rate cut in March, as the inflation level is reaching the target. It’s interesting to note that in a research on G10 central banks, the BOE appears to be the least cohesive board with the most dissents following the post-pandemic inflation rise. Chief Economist Huw Pill stated the day after that the BOE should not be too reassured by the falls in headline inflation as underlying price pressure continues to exist.

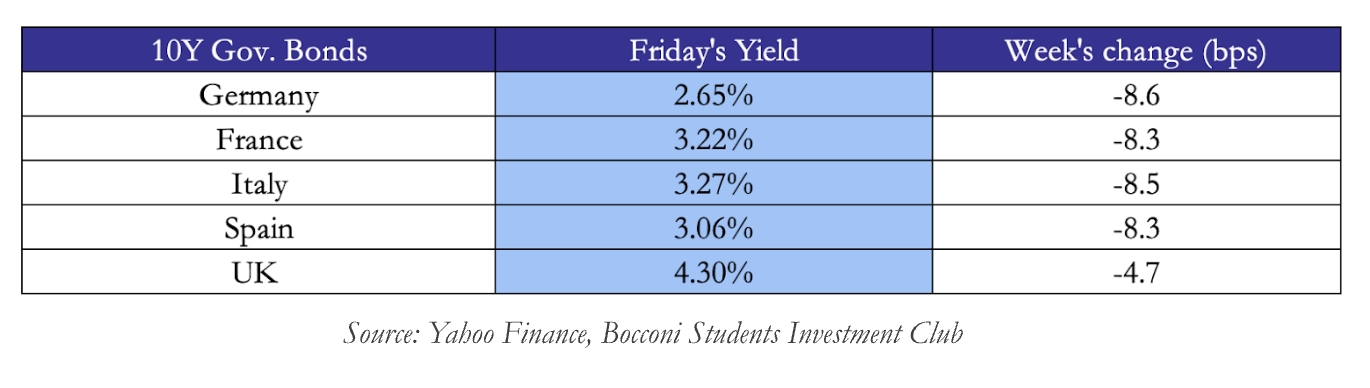

The week was characterised by mixed inflation data across the Eurozone. In Germany the annual inflation rate slowed to 1.9% compared to the previous 2.1%. The French consumer price index rose by 1.1% YoY, with the median expected rate of 0.7%. In Spain the reading for annual inflation edged up to 2.5%, compared to the previous 2.4% and the expected 2.3%. Overall, the Eurozone harmonised prices rose only 0.4% in January, the lowest level since December 2020. The positive outlook on inflation and the diversification from the dollar helps understand why investors are buying European sovereign.

The week was characterised by mixed inflation data across the Eurozone. In Germany the annual inflation rate slowed to 1.9% compared to the previous 2.1%. The French consumer price index rose by 1.1% YoY, with the median expected rate of 0.7%. In Spain the reading for annual inflation edged up to 2.5%, compared to the previous 2.4% and the expected 2.3%. Overall, the Eurozone harmonised prices rose only 0.4% in January, the lowest level since December 2020. The positive outlook on inflation and the diversification from the dollar helps understand why investors are buying European sovereign.

Rest of the World

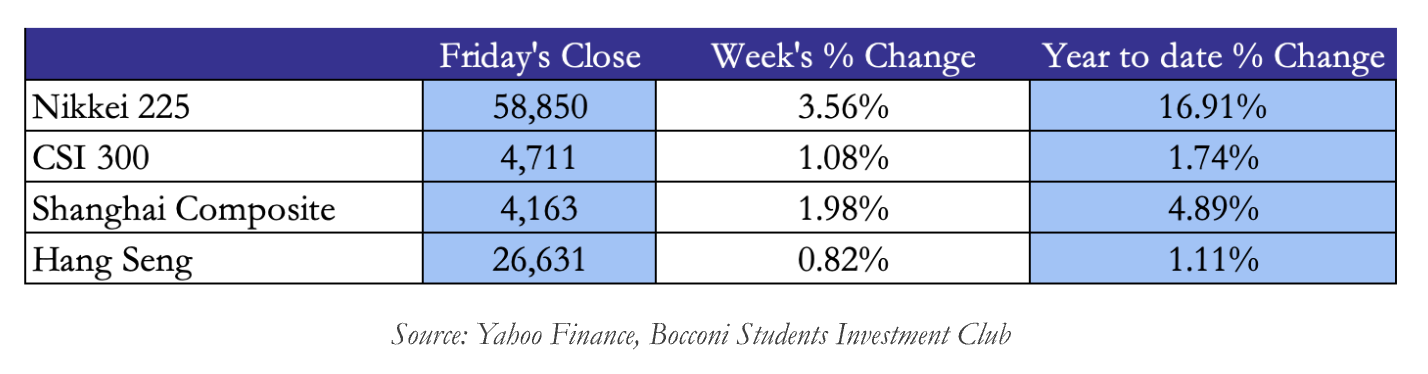

Asian Equities posted gains over the week with the Nikkei 225 gaining 3.56% over the week. The index reached new highs as investors are continuing to show optimism on LDP leader Sanae Takaichi which has achieved super majority in the House of Representatives in early February (316 over 465 seats). Over the week, Ex-BOJ chief Kuroda called for a rate hike and tighter fiscal policy and the Japanese Finance minister Katayama have warned the parliament that the government is invigilating over the most recent yen slide.

One common theme in the most recent year in the markets has been analysing EM markets excluding China. Since the performance of the two has diverged significantly and is driven by completely different catalysts. During the week the Chinese onshore index, CSI 300, advanced by 1.08% and the Shanghai Composite Index rose by 1.98%, in Hong Kong the reference index Hang Seng inched up by 0.82%. Travel and consumption data over the lunar year tourism period has provided mixed signals about consumer sentiment. Furthermore, the People’s Bank of China has announced, due to an appreciation of the CNY over USD reaching 3-year highs, that it will cut the FX forward reserve ratio from 20% to 0% for financial institutions conducting foreign exchange forward trading with the objective of encouraging dollar buying to aid its exports operations.

Looking at EM Ex-China, the picture is completely different. In Southeast Asia the South Korean reference index, Kospi, posted an extraordinary 7.50% rise over the week continuing its rally. Semi-conductor companies have seen an increase in AI data spending over the recent year and the supply for DRAM and NAND chips has tightened lifting their revenues, causing the shares of Samsung electronics [SKR:005930] and SK Hynix [SKR:000660] to climb enormously over the year. The rise has also been supported by an increase in auto shares in the region. The ASX 200 increased by 1.29% led by an increase in non-energy minerals producers.

Looking at EM Ex-China, the picture is completely different. In Southeast Asia the South Korean reference index, Kospi, posted an extraordinary 7.50% rise over the week continuing its rally. Semi-conductor companies have seen an increase in AI data spending over the recent year and the supply for DRAM and NAND chips has tightened lifting their revenues, causing the shares of Samsung electronics [SKR:005930] and SK Hynix [SKR:000660] to climb enormously over the year. The rise has also been supported by an increase in auto shares in the region. The ASX 200 increased by 1.29% led by an increase in non-energy minerals producers.

In South America the Bovespa and IPX Index have inched lower on a relatively flat week, however its rally since the beginning of 2025 has been remarkable, the former gaining more than 50% and the latter over 40%. The fundamentals in the regions remain healthy and the weaker dollar has boosted their exporting economies. Furthermore, in Brazil investors are starting to formulate some hypotheses on the next elections which will take place on October 2026, and some have stated that there could be an election premium to be harvested.

FX and Commodities

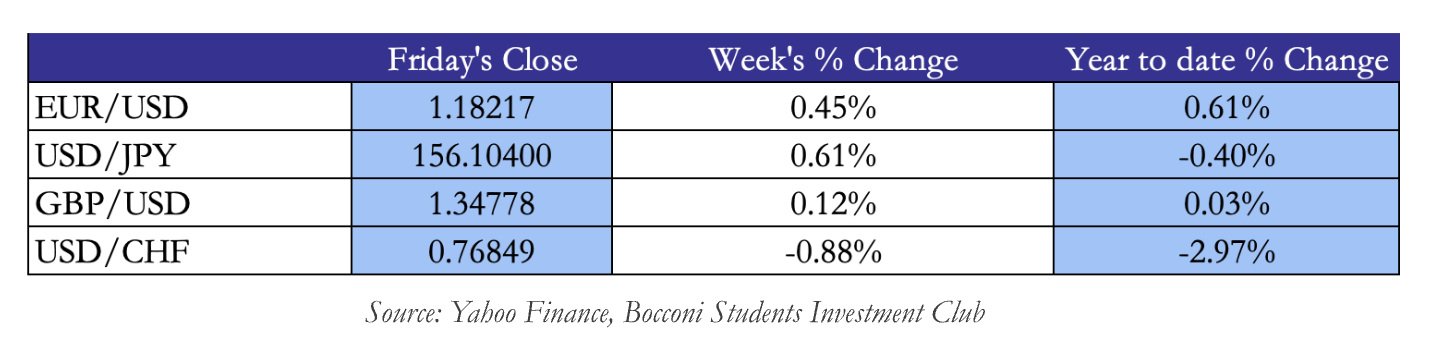

FX markets saw moderate moves during the week with the US dollar index slipping 0.06% over the week. The EUR/USD inched up by 0.45% closing at 1.18217 supported by low inflation and strong performance by both European stocks and sovereign bonds. The USD/JPY rose by 0.61% causing some concerns among the Japanese Ministry of Finance over Yen weakness. The GBP/USD inched up by 0.12% closing at 1.34778, with a very minimal change since year start. Finally, the USD/CHF closed at 0.76849 marking a decline of 0.88% over the week highlighting the consistent capital flows redirected into safer economies such as Switzerland’s.

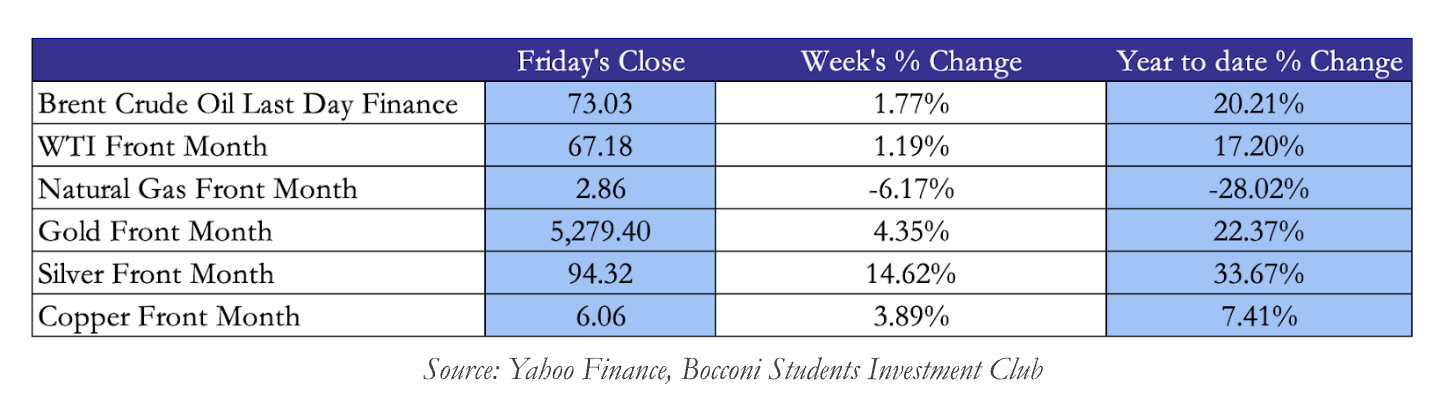

Looking at metals contracts, the market delivered a positive performance this week. Following the whole drama between the Supreme Court and the US administration together with a hotter than expected PPI Gold and Silver posted important gains throughout the week, the former gaining 4.35% and the latter 14.62% over the week. Copper front month rose by 3.89%, regardless of the slowdown in Chinese manufacturing typical of the Lunar year period; relevant as China is the biggest consumer of copper in the world. The rise can be explained by the sentence on the tariffs, which doesn’t affect the 50% tariff on raw copper entering the US, but does affect tariffs on other goods originating in China or India, possibly increasing the future demand for copper. Needless to say, that uncertainty on tariffs still looms over global markets and it particularly affects copper demand expectations.

Looking at metals contracts, the market delivered a positive performance this week. Following the whole drama between the Supreme Court and the US administration together with a hotter than expected PPI Gold and Silver posted important gains throughout the week, the former gaining 4.35% and the latter 14.62% over the week. Copper front month rose by 3.89%, regardless of the slowdown in Chinese manufacturing typical of the Lunar year period; relevant as China is the biggest consumer of copper in the world. The rise can be explained by the sentence on the tariffs, which doesn’t affect the 50% tariff on raw copper entering the US, but does affect tariffs on other goods originating in China or India, possibly increasing the future demand for copper. Needless to say, that uncertainty on tariffs still looms over global markets and it particularly affects copper demand expectations.

Energy contracts on the other hand have seen an important increase on Friday’s trading day amid concerns over the US and Iran geopolitical situation, with the diplomatic efforts aimed at easing tensions over Teheran’s nuclear program failed on Thursday. At the time of writing the US has struck Iran with missiles and therefore has started its military attack, it could be good practice for the reader to formulate an opinion on the possible movements on crude oil and natural gas contracts when markets will open again next week. Finally, Natural Gas Front Month contract slipped by 6.17%, with expectations of a warmer weather incoming. The U.S.–Iran conflict can now test whether Qatar’s LNG supremacy is built on resilience or on Iran’s continued constraint.

Next Week Main Events

Next Week Main Events

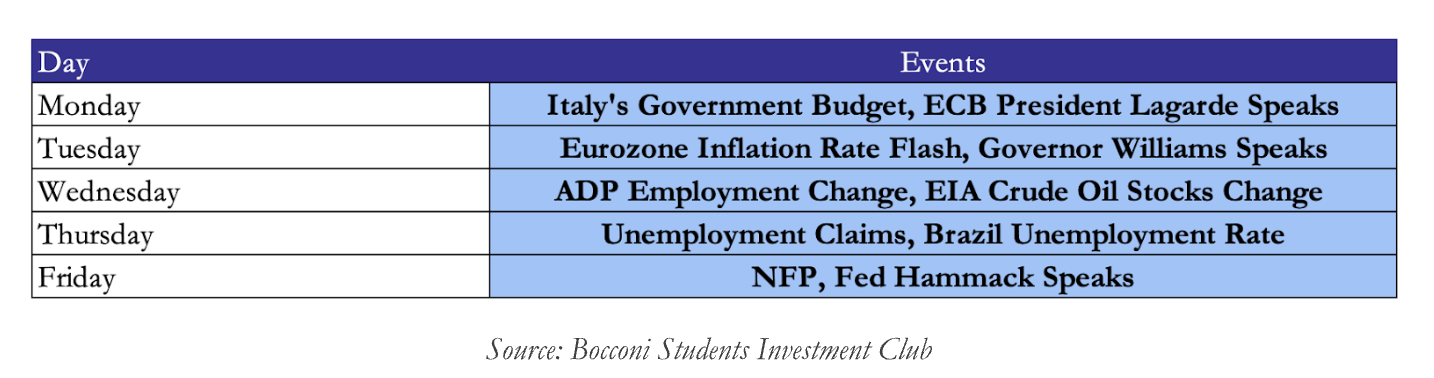

According to headlines, following the US strike on Iran, markets are in a brace position ahead of what is expected to be a volatile week. On Monday Italy presents its government budget together with GDP growth data. Tuesday will bring the Eurozone inflation rate and a speech by Governor Williams very relevant to understand the Fed’s view on the current easing cycle. On Wednesday there will be the ADP employment change and the EIA Crude Oil stock changes. Thursday will show the US Unemployment claims with a consensus around 216 thousand. We close the week with the NFP and bank of Cleveland president Beth Hammack speech, very interesting as she stated two weeks ago that rates should be on hold for some time.

Brain Teaser #43

There are 25 horses, each of which runs at a constant speed that is different from the other horses’. Since the track only has 5 lanes, each race can have at most 5 horses. If you need to find the 3 fastest horses, what is the minimum number of races needed to identify them?

Solution: This problem tests your basic analytical skills. To find the 3 fastest horses, surely all horses need to be tested. So, a natural first step is to divide the horses to 5 groups (with horses 1-5, 6-10, 11-15, 16-20, 21-25 in each group). After 5 races, we will have the order within each group, let’s assume the order follows the order of numbers (e.g., 6 is the fastest and 10 is the slowest in the 6-10 group). That means 1, 6, 11, 16 and 21 are the fastest within each group.

Surely the last two horses within each group are eliminated. What else can we infer? We know that within each group, if the fastest horse ranks 5th or 4th among 25 horses, then all horses in that group cannot be in top 3; if it ranks the 3rd, no other horse in that group can be in the top 3; if it ranks the 2nd, then one other horse in that group may be in top 3; if it ranks the first, then two other horses in that group may be in top 3.

Brain Teaser #44

One hundred prisoners are given the chance to be set free tomorrow. They are all told that each will be given a red or blue hat to wear. Each prisoner can see everyone else’s hat but not his own. The hat colors are assigned randomly and once the hats are placed on top of each prisoner’s head they cannot communicate with one another in any form, or else they are immediately executed. The prisoners will be called out in random order and the prisoner called out will guess the color of his hat. Each prisoner declares the color of his hat so that everyone else can hear it.

If a prisoner guesses correctly the color of his hat, he is set free immediately; otherwise he is executed. They are given the night to come up with a strategy among themselves to save as many prisoners as possible. What is the best strategy they can adopt and how many prisoners can they guarantee to save?

0 Comments