USA

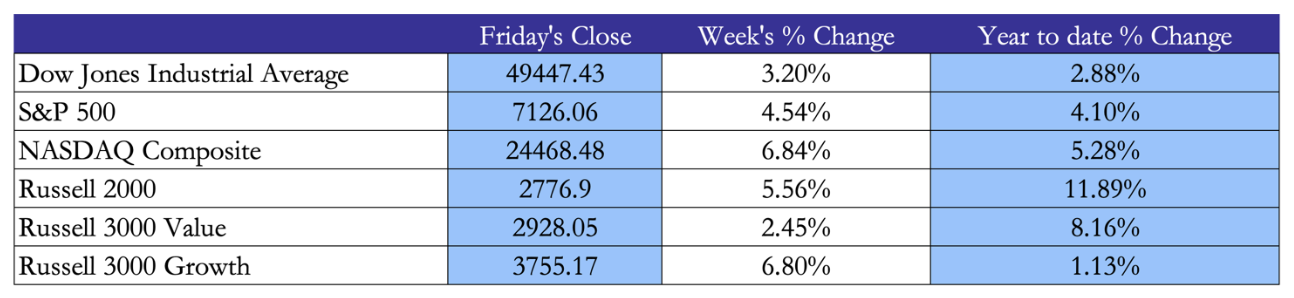

US equity markets had a remarkable week. S&P 500 rose by 4.54% WoW, hitting a new record high on Wednesday, and DJIA grew by 3.20% WoW, jumping nearly 868 points in a single session. Marked by a swift de-escalation in the US-Iran tensions, markets have thus experienced a sharp reversal from the late Q1.

Banks were a major driver of the rally early in the week, as JPMorgan, Citi and Wells Fargo collectively reported over $25 billion in profits in Q1 – the volatility in oil prices due to the Iran war had boosted their trading desks’ revenues. More significantly, on Friday, news broke that Iran had agreed to suspend its nuclear program and reopen the Strait of Hormuz. This instantly led to a wave of risk-on buying, as concerns regarding inflation and growth began to dissipate. This explains the sharp rise in equities that happened on Friday.

It may also be noted that growth performed much stronger than value this week: Russell 3000 Growth rose 6.80% while Russell 3000 Value only 2.45%. This, once again, highlights a reversal from the weeks prior, where inflation fears crushing growth multiples led investors to abandon growth stocks. Tech and cyclical sector equities all gained significantly. While Trump’s naval blockade is still technically in force and the prospects of a final resolution in the Middle East remain unclear, the market clearly chose optimism, pricing in a swift end to the conflict.

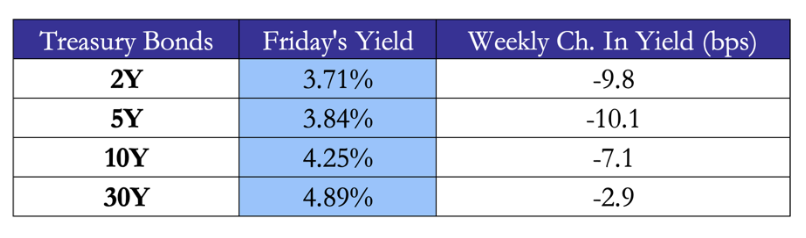

Treasury yields fell across the board this week. The optimistic prospects over Iran caused oil prices and thus inflationary fears to wind down. This means that the Fed has now more room to decrease its policy rates causing markets to invest heavily in US government bonds. The expectations of these sooner rate cuts led to the yield curve’s bull steepening, as the yields on bonds with near-term maturities fell sharper than those with longer maturities. It is important to mention that the longer-term credibility of US Treasuries as a “safe haven” has remained under scrutiny as uncertainties related to Trump’s presidency continue pressuring investors into diversifying their fixed income holdings away from the US.

Treasury yields fell across the board this week. The optimistic prospects over Iran caused oil prices and thus inflationary fears to wind down. This means that the Fed has now more room to decrease its policy rates causing markets to invest heavily in US government bonds. The expectations of these sooner rate cuts led to the yield curve’s bull steepening, as the yields on bonds with near-term maturities fell sharper than those with longer maturities. It is important to mention that the longer-term credibility of US Treasuries as a “safe haven” has remained under scrutiny as uncertainties related to Trump’s presidency continue pressuring investors into diversifying their fixed income holdings away from the US.

Europe and UK

European equities gained significantly too. The STOXX 600 index rose 1.91% WoW, with the German DAX experiencing a strong growth of 3.77%. The Italian FTSE MIB and French CAC 40 also rose between 2-3%, altogether marking a significant recovery from the previous weeks. This was, as in the case of the US, caused by the reopening of the Strait of Hormuz and easing tensions in the Middle East. However, Europe remains more structurally exposed to the potential energy supply shocks from the US-Iran conflict. It relies heavily on oil and gas imports from abroad and its industrial base is highly energy intensive. This explains why European equities experienced a slower recovery than the American ones: investors are still pricing in a higher risk premium in European stocks.

There are several events that additionally impacted European equities this week. Peter Magyar’s election victory in Hungary caused an unprecedented surge in Hungary’s stock, bond and currency markets, as investors expect the new PM’s government to lead a more pro-market economic policy in close cooperation with the EU. Moreover, the EU’s announcement of plans for a significant relaxation of corporate merger rules positively impacted bank equities as the promise will arguably reshape European M&A.

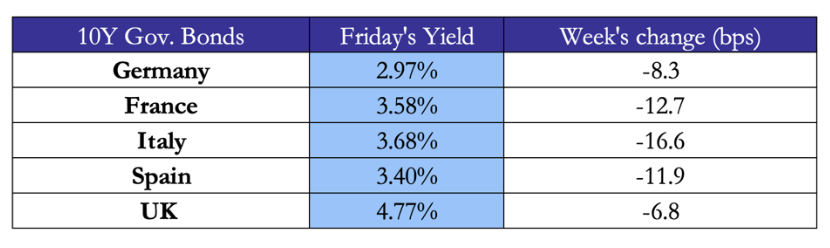

Yields on European government bonds also fell sharply this week, with Italy, France and Spain experiencing the largest falls. This happened for the exact same reason as in the case of US Treasuries: the dissipation of inflationary fears amid falling oil prices led investors to expect potential rate cuts and less risk. It is notable that the yields on “riskier” peripheral bonds – such as those of Italy, France or Spain – fell much sharper than those in Germany or the UK. This can be viewed as a classic risk-on rotation in European fixed income markets, as investors are moving back into the higher-yielding territory that, thanks to the easing of tensions, they become more comfortable with. The UK gilt was more of an exception in this case, tightening by only 6.8 bps as the Bank of England remains constrained by domestic inflation, although UK gas prices dipping below pre-war levels may offer some relief in that respect.

Rest of the World

Japanese equities had a strong week, as the Nikkei is now remarkably 16.16% up Ytd. The “Takaichi factor” remains among the main in driving this growth, as Prime Minister Takaichi continues pursuing a pro-growth fiscal agenda. Additionally, the reopening of the Strait of Hormuz is a particularly favorable event for Japan, which is almost entirely dependent on imported energy.

Meanwhile, the CSI 300 rose 1.99%, but the Shanghai Composite was essentially flat, and the Hang Seng gained 1.03%. The divergence between onshore and Hong Kong markets reflects different investor bases and different risk appetites. China’s situation is complicated. On the one hand, China’s industrial profits for January-February rose 15.2% Ytd, but on the other, the country continues experiencing persistent deflationary pressures, which remain a massive concern for future growth prospects. China also set its 2026 GDP growth target a only 4.5-5%, the lowest number so far, acknowledging its ongoing economic challenges. A notable story from this week also concerns Taiwan’s economic milestone: the island overtook the UK in total stock market value this week, primarily driven by the AI boom and TSMC reporting record profits in Q1.

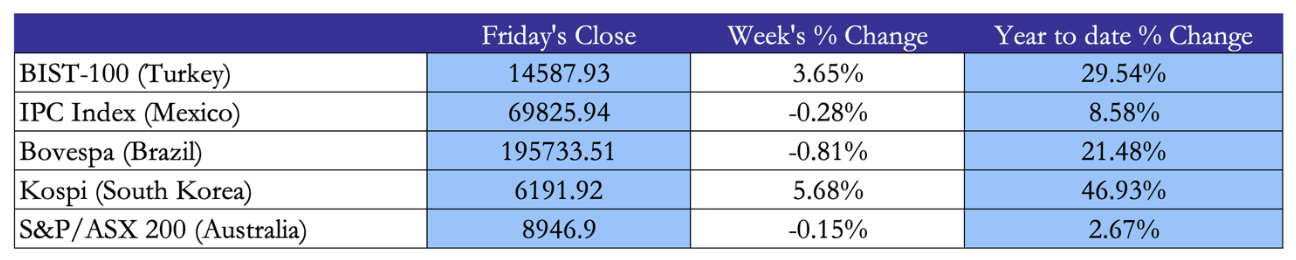

Kospi’s performance stood out in Asia this week with a 5.68% gain. This has been driven by tech and semiconductor equities – the broader AI rally this week has benefited Korea’s markets disproportionately. Latin American markets had a slightly negative week despite the positive global mood, with Brazil’s Bovespa and Mexico’s IPC falling 0.81% and 0.28% respectively. This is not entirely surprising given both have already had a strong 2026, up 21.48% and 8.58%, with some investors likely simply locking in their profits. Turkey performed well too, gaining 3.65% on the week and now up nearly 30% year-to-date despite ongoing inflation troubles. Australia has basically seen no growth, as rising gold and copper prices that could potentially bring about optimism were cancelled out by the sharp drop in oil.

FX and Commodities

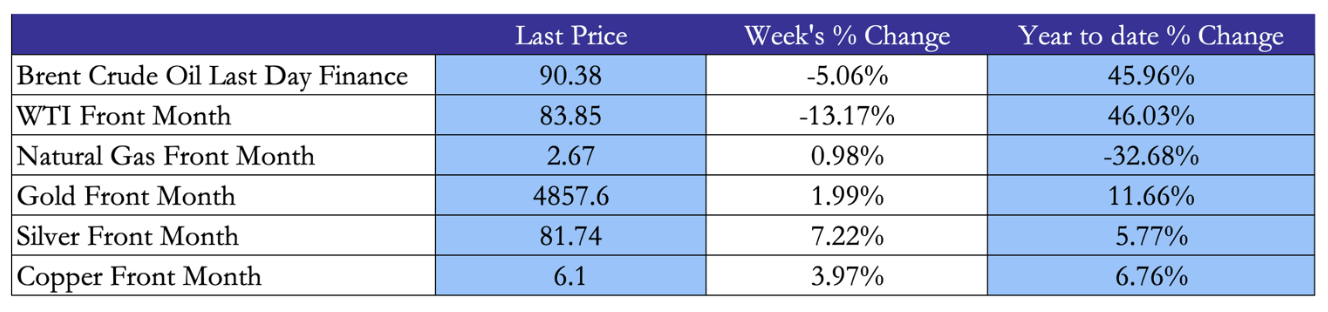

The most significant story of the week is the sharp drop in oil prices after sky-high levels the week prior. Brent crude oil futures fell 5.06% to $90.38 and WTI decreased even more by 13.17% to $83.85. This drop is entirely explained by Trump’s bombshell announcement on Friday and the opening of the Strait of Hormuz – oil markets immediately priced in a return of supply leading to a sharp drop in prices. The IEA also reported that global oil demand fell by roughly 3.4% in March due to high prices and the disruptions of air travel in the Middle East, meaning this demand destruction will weigh on prices further now that supply fears are dissipating. However, oil prices, despite this recent fall are still staggering at roughly 46% Ytd and future movements depend almost entirely on the developments over the Strait of Hormuz.

Also, it must be noted that WTI fell much more than Brent. This is partly because US crude oil exports had hit record-high levels during the crisis as Asian buyers were absorbing all non-Gulf oil supply. With the Hormuz reopening, that premium for US crude is extinguished quickly. Also, the US had been urging US oil companies to increase production, which added on to supply expectations.

Meanwhile, gold continues its rally, up 11.66% Ytd even after several weeks of soaring oil prices. This marks a continuation of the persistent central bank buying and geopolitical uncertainty, including Iran, as many experts have already expressed their concerns regarding the long-term stability of the ceasefire and the Strait of Hormuz reopening. Silver dramatically outperformed gold, up 7.22% this week, benefitting from its safe-haven appeal and industrial demand in such sectors as renewable energy and electronics. Copper too had a strong week, up nearly 4%, reflecting the resilient industrial demand expectations out of China. Being considered as a sort of a barometer of global economic health, its rise suggests this week has been a relief for global investors amid the turmoil.

In currencies, EUR/USD rose 0.79% to 1.1783, GBP/USD rose 0.71% to 1.3526 and USD/CHF fell 0.97%. From these three currencies pairs, it is clear that the dollar is depreciating against most major currencies, losing some of its safe-haven premium as the Iran conflict begins to (or appears to) resolve. The yen, however, remained weak at around 159, as the persistent US-Japan differential is keeping the yen under pressure. Japan still has very low interest rates while the US is at 4.25% on the 10Y.

Next Week’s Main Events

With the Hormuz situation still fluid and markets pricing in a swift resolution, next week’s data releases will be closely watched for signs of how the real economy is holding up.

Brain Teaser #45

You have 12 balls, all the same in appearance. One ball is either heavier or lighter than the rest – you don’t know which. You have a balance scale and exactly 3 weighings to identify the odd ball and determine whether it is heavier or lighter. How do you do it?

Brain Teaser #46

A hedge fund manager claims to have a strategy that beats the market every single year. To prove it, he sends weekly predictions to 1,024 investors – half are told the market will go up, half are told it will go down. After each correct prediction, he repeats the process only with the investors who received the correct call. After 10 weeks one investor has received 10 correct predictions in a row. Should that investor stick to the manager’s strategy?

0 Comments