USA

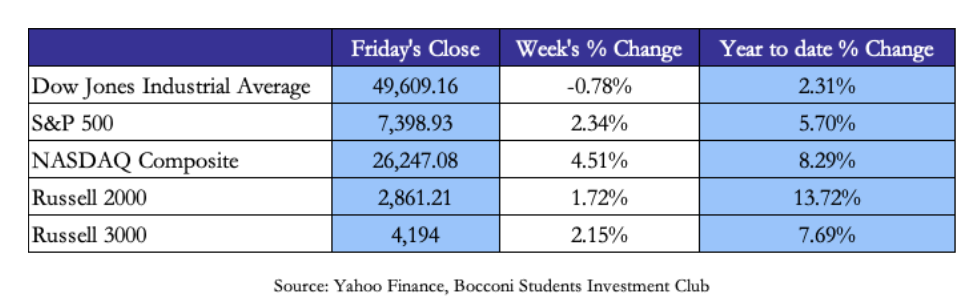

US equity markets closed the week with the S&P 500 and Nasdaq Composite both hitting fresh all-time highs on Friday, propelled by a stronger than expected April jobs report and continued AI earnings momentum, with the Nasdaq surging 4.51% on the week and the S&P 500 gaining 2.34%: marking the sixth consecutive winning week for both indices. The Dow lagged with a marginal +0.22% gain, dragged by Thursday’s broad sell-off.

The week followed a sharp intraday pattern: Monday opened with oil spiking above $112 (Brent) as Iran launched drones and missiles at the UAE and Washington confirmed it had sunk Iranian vessels in the Strait, sending the Dow down over 500 points. By Wednesday the mood had completely reversed, with the S&P 500, Nasdaq and Russell 2000 all simultaneously closing at all-time highs after Axios reported the US and Iran were nearing a one-page memorandum of understanding to end hostilities. Thursday erased those gains as Iran accused the US of breaching the ceasefire after American destroyers struck targets in the Strait: every major sector declined, led by Energy (-1.95%) and Industrials (-1.66%), with the S&P 500 retreating to 7,337 and the Dow falling to 49,597. Friday recovered sharply as nonfarm payrolls came in at 115,000, well above the 55,000–65,000 consensus, with unemployment steady at 4.3%, sending the S&P 500 up 0.84% and the Nasdaq up 1.71% to record closes.

On the earnings front, the AI trade continued to dominate, with strong top-line and data center growth reinforcing the fundamental narrative, even as valuation sensitivity remained elevated across parts of the sector. AMD beat on both revenue ($10.3bn vs $9.9bn expected) and EPS ($1.37 vs $1.25), with Data Center revenue up 57% year-over-year; Intel surged 13% to an all-time high on reports of Apple chip-manufacturing talks, taking its year-to-date gain to over 175%. Rocket Lab soared 24% on a revenue beat, Fluence Energy surged 40% on strong results, while Cloudflare tumbled 22% after issuing a weak Q2 forecast and announcing roughly 20% workforce cuts. Palantir reported record Q1 revenue of $1.63bn and raised full-year guidance to $7.64bn, above the $7.28bn consensus, yet fell on valuation concerns. With around 75% of S&P 500 companies having reported, 84% have beaten EPS estimates and aggregate earnings growth is tracking near 28% year-over-year.

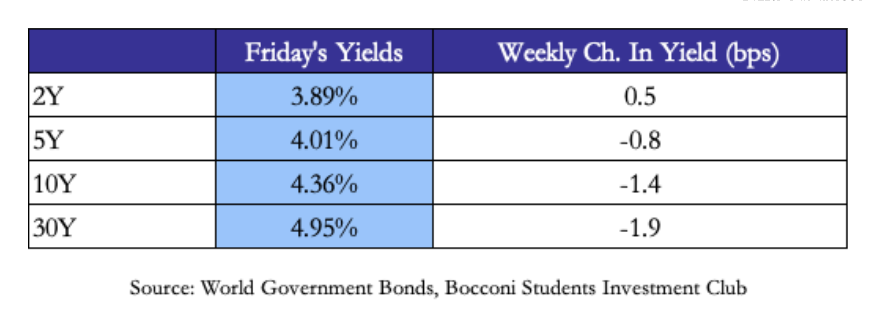

On rates, US Treasuries ended the week broadly stable: the 10Y at 4.36%, 2Y at 3.89%, 30Y at 4.95%, after oscillating sharply with each geopolitical headline. The week’s key fixed income backdrop remained the April 29 FOMC meeting: the Fed held at 3.50%–3.75% with four dissenters, the most since 1992, with Miran pushing for a cut and Kashkari, Hammack and Logan opposing the statement’s easing bias. The meeting marked Powell’s final as Chair, with his term ending May 15; he confirmed he will remain on the Board as governor through January 2028. Kevin Warsh cleared the Senate Banking Committee the same morning, setting up full Senate confirmation ahead of the June 16–17 meeting. Markets are divided on what a Warsh Fed means for the rate path, particularly around the balance between inflation credibility and growth sensitivity at the front end of the curve.

On rates, US Treasuries ended the week broadly stable: the 10Y at 4.36%, 2Y at 3.89%, 30Y at 4.95%, after oscillating sharply with each geopolitical headline. The week’s key fixed income backdrop remained the April 29 FOMC meeting: the Fed held at 3.50%–3.75% with four dissenters, the most since 1992, with Miran pushing for a cut and Kashkari, Hammack and Logan opposing the statement’s easing bias. The meeting marked Powell’s final as Chair, with his term ending May 15; he confirmed he will remain on the Board as governor through January 2028. Kevin Warsh cleared the Senate Banking Committee the same morning, setting up full Senate confirmation ahead of the June 16–17 meeting. Markets are divided on what a Warsh Fed means for the rate path, particularly around the balance between inflation credibility and growth sensitivity at the front end of the curve.

Europe and UK

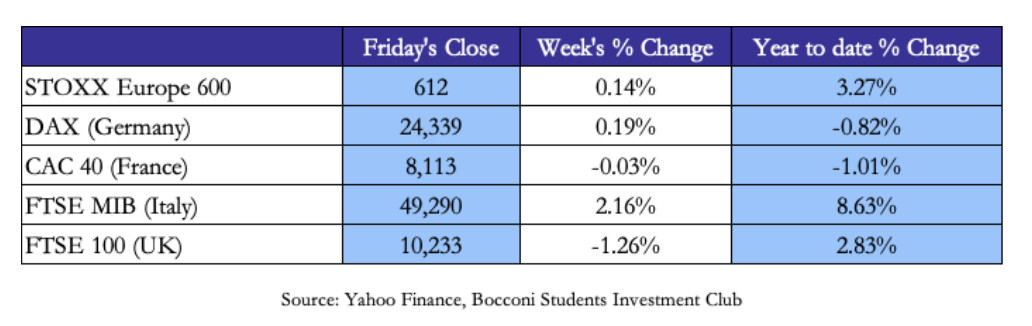

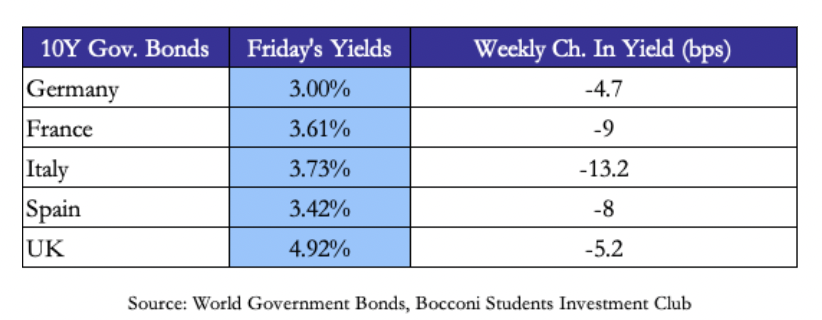

European equities ended a mixed week, with performance highly dispersed. The FTSE MIB led with a 2.16% gain on banking strength and BTP spread compression, the DAX added 0.19%, while the CAC 40 was flat (-0.03%) and the FTSE 100 slipped 1.26% as energy heavyweights sold off on mid-week ceasefire optimism that dragged Brent below $97. European sovereign yields fell sharply, reversing the prior week, as oil’s mid-week plunge reduced near-term inflation expectations faster than nominal yields adjusted, contributing to a modest firming in real rates: Italian BTPs tightened 13.2 bps to 3.73%, French OATs fell 9 bps to 3.61%, German Bunds eased 4.7 bps to 3.00%, with UK Gilts declining 5.2 bps to 4.92%.

The macro backdrop remains increasingly stagflationary. Eurozone inflation reached 3.0% in April: its highest in two years, while euro area GDP growth has been revised down to 0.9% for 2026 as the war weighs on real incomes, business confidence and commodity markets. The ECB held rates unchanged at 2.0% at its April 30 meeting, with Lagarde acknowledging the Governing Council is “certainly moving away” from its baseline scenario; markets are now pricing three ECB rate hikes in 2026, with the first as early as June. In the UK, CPI rose to 3.3% in March, driven by motor fuels, with annual energy price inflation hitting an estimated 10.9% in April versus -3.1% in February; the BoE held at 3.75% but projected inflation peaking between 3% and 3.5% in Q2–Q3 2026, with an 8-1 vote split signalling growing internal pressure for a hike. The shared dilemma for both central banks is stark: the energy shock demands tighter policy to prevent second-round effects, yet simultaneously depresses the growth outlook and limits their room to act aggressively.

The macro backdrop remains increasingly stagflationary. Eurozone inflation reached 3.0% in April: its highest in two years, while euro area GDP growth has been revised down to 0.9% for 2026 as the war weighs on real incomes, business confidence and commodity markets. The ECB held rates unchanged at 2.0% at its April 30 meeting, with Lagarde acknowledging the Governing Council is “certainly moving away” from its baseline scenario; markets are now pricing three ECB rate hikes in 2026, with the first as early as June. In the UK, CPI rose to 3.3% in March, driven by motor fuels, with annual energy price inflation hitting an estimated 10.9% in April versus -3.1% in February; the BoE held at 3.75% but projected inflation peaking between 3% and 3.5% in Q2–Q3 2026, with an 8-1 vote split signalling growing internal pressure for a hike. The shared dilemma for both central banks is stark: the energy shock demands tighter policy to prevent second-round effects, yet simultaneously depresses the growth outlook and limits their room to act aggressively.

Rest of the World

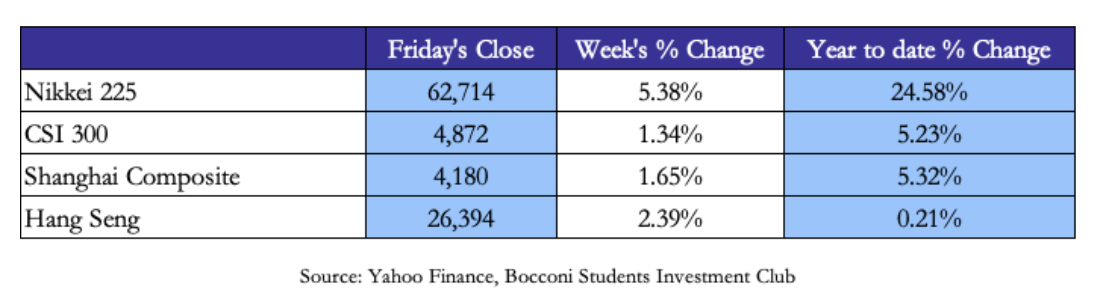

Asian equity markets delivered the week’s most impressive performances. Japan’s Nikkei 225 surged 3,320 points on Thursday: the largest single-day point gain in the index’s history, closing at a record 62,833.84 as Tokyo markets reopened after Golden Week and compressed a full week of global AI earnings repricing into one session; trading value on the Tokyo Stock Exchange Prime Market reached ¥10.8 trillion, the highest of the year. SoftBank soared over 18%, Advantest gained nearly 7% and Tokyo Electron surged 9%, with the rally driven by AMD’s blowout results and surging AI infrastructure optimism. The Nikkei is now up ~22% year-to-date, with semiconductor and AI infrastructure stocks accounting for an increasingly concentrated share of index gains.

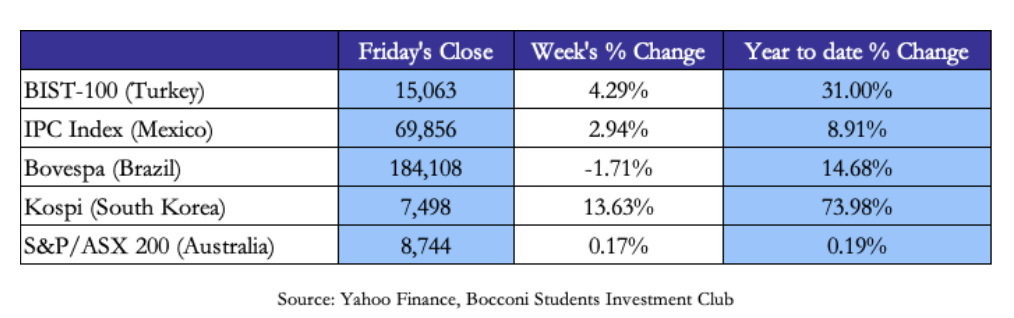

South Korea’s Kospi surpassed 7,000 for the first time in its history on Wednesday, with Samsung Electronics crossing the $1 trillion market cap threshold, only the second Asian company after TSMC to do so, pushing Korea’s total equity market cap past Canada’s to become the world’s seventh largest. The Kospi closed at a record 7,490, up 1.43% on the week and roughly 74% year-to-date, driven entirely by its semiconductor complex. Mainland China was more subdued, with the CSI 300 +0.80% and Shanghai Composite +0.79%, while the Hang Seng gained 2.39% on improving sentiment around the peace deal trajectory.

South Korea’s Kospi surpassed 7,000 for the first time in its history on Wednesday, with Samsung Electronics crossing the $1 trillion market cap threshold, only the second Asian company after TSMC to do so, pushing Korea’s total equity market cap past Canada’s to become the world’s seventh largest. The Kospi closed at a record 7,490, up 1.43% on the week and roughly 74% year-to-date, driven entirely by its semiconductor complex. Mainland China was more subdued, with the CSI 300 +0.80% and Shanghai Composite +0.79%, while the Hang Seng gained 2.39% on improving sentiment around the peace deal trajectory.

FX and Commodities

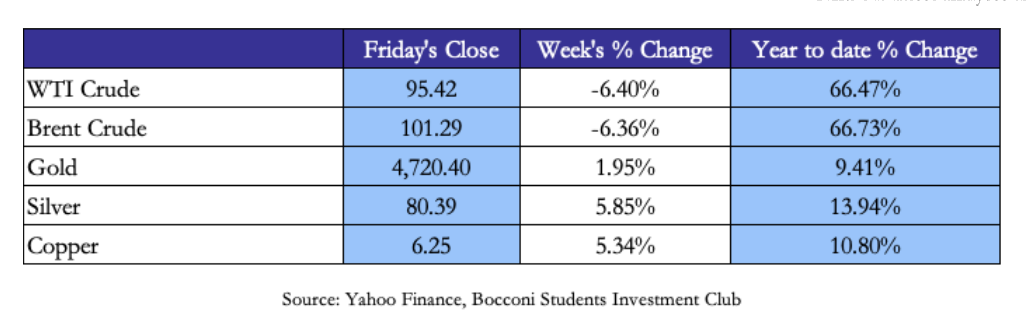

Crude oil posted weekly losses exceeding 6%, with Brent settling at $101.29 and WTI at $95.42, as markets progressively priced in a growing probability of a negotiated Strait of Hormuz resolution. The intraday moves were violent: WTI briefly plunged to $88.71 and Brent to $96.77 on Wednesday (a 13% intraday crash) as Axios reported the US and Iran were nearing a one-page MOU, before recovering as Trump said a deal was not certain and fresh exchanges in the Strait reignited escalation fears on Thursday. The IEA warned the conflict is removing approximately 14 million barrels per day from global supply, with any post-conflict production recovery expected to lag by six to eight weeks after access conditions normalise. Despite the week’s decline, Brent remains up over 59% year-to-date. Natural gas edged slightly higher to $2.79.

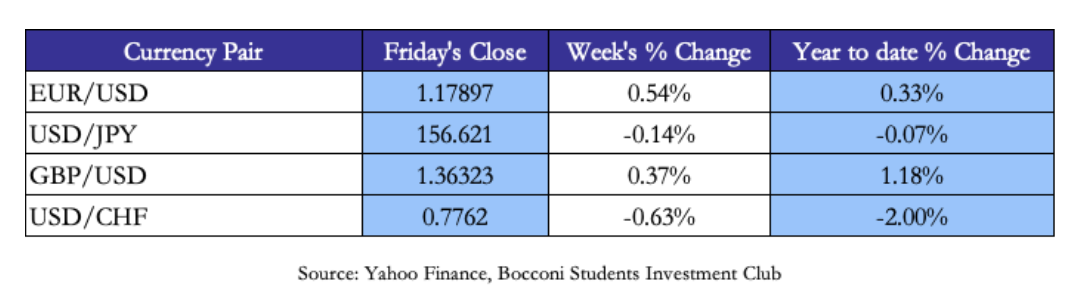

The US dollar softened modestly as ceasefire optimism eroded safe-haven demand. EUR/USD slipped to 1.127, weighed by the eurozone’s stagflationary risk premium, while GBP/USD edged to 1.356. The standout FX move was the yen: USD/JPY briefly breached 160, a level widely seen as a trigger for official intervention, before rebounding sharply to close around 156.84, supported both by suspected BoJ intervention and the central bank’s hawkish tone at its May meeting, where three members pushed for a move toward a 1.0% policy rate. Gold dipped modestly to $4,720, as the decline in oil reduced inflation expectations faster than nominal yields adjusted, modestly firming real rates, while mid-week de-escalation reduced the geopolitical risk premium.

The US dollar softened modestly as ceasefire optimism eroded safe-haven demand. EUR/USD slipped to 1.127, weighed by the eurozone’s stagflationary risk premium, while GBP/USD edged to 1.356. The standout FX move was the yen: USD/JPY briefly breached 160, a level widely seen as a trigger for official intervention, before rebounding sharply to close around 156.84, supported both by suspected BoJ intervention and the central bank’s hawkish tone at its May meeting, where three members pushed for a move toward a 1.0% policy rate. Gold dipped modestly to $4,720, as the decline in oil reduced inflation expectations faster than nominal yields adjusted, modestly firming real rates, while mid-week de-escalation reduced the geopolitical risk premium.

Silver and copper outperformed strongly, with silver gaining 5.85% and copper 5.34%, reflecting industrial demand expectations tied to AI infrastructure build-out and post-conflict reconstruction prospects.

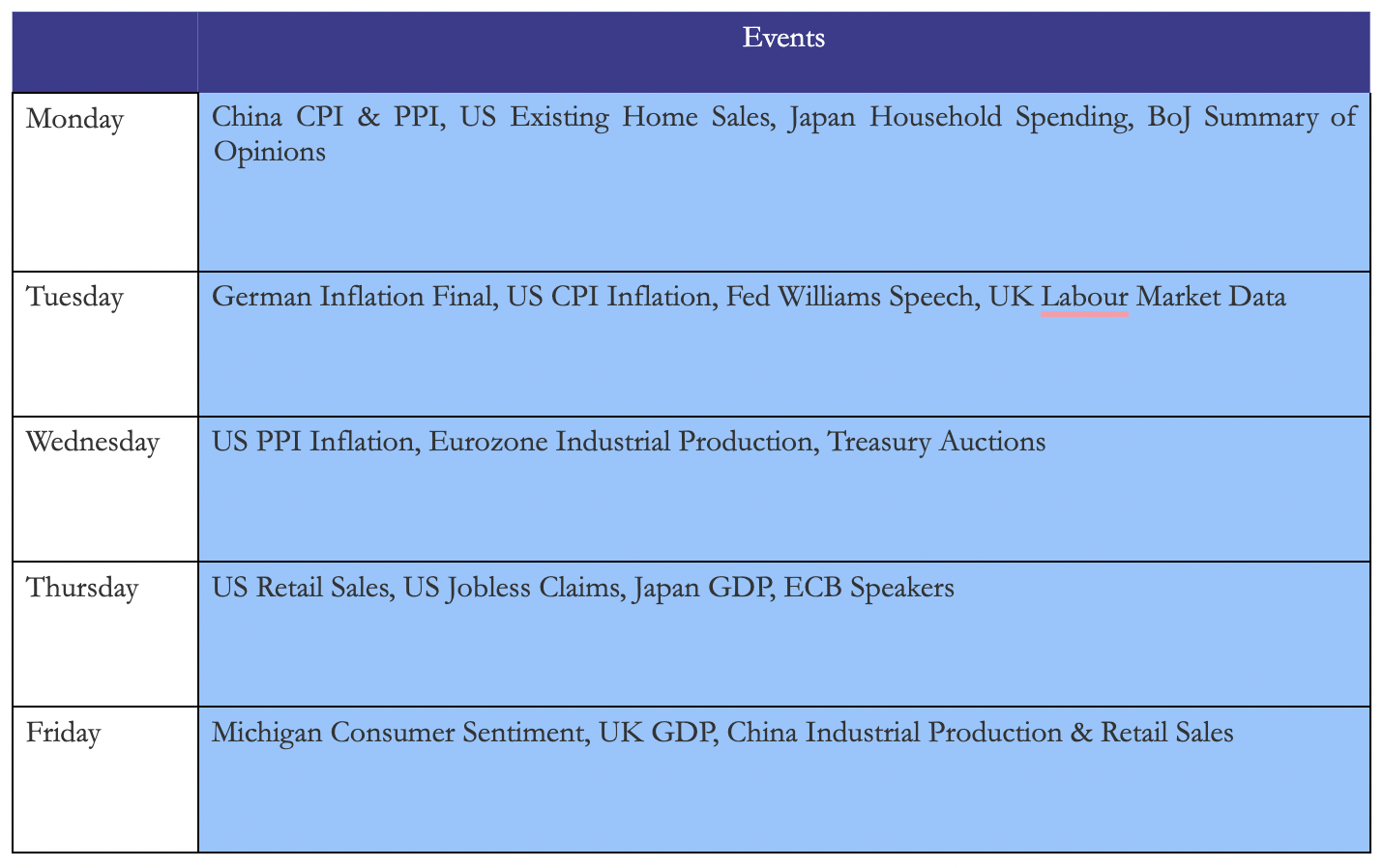

Next Week Main Events

Next week’s macro calendar is dense and consequential. Tuesday’s US CPI print will be the most watched release: the first inflation reading since oil prices began pulling back, it will set the tone for Fed expectations under the incoming Warsh chairmanship. US PPI on Wednesday and Michigan Consumer Sentiment on Friday complete the domestic inflation picture. In Europe, German inflation finals and Eurozone industrial production will feed directly into the ECB’s June rate decision, while UK labour market data and GDP will test the economy’s resilience under elevated energy costs. In Asia, Japan GDP and the BoJ Summary of Opinions will confirm or soften the hawkish shift signalled at the May meeting, and China’s CPI, PPI and retail sales will offer the clearest read yet on whether deflationary pressures are easing. Throughout the week, any development on the Strait of Hormuz negotiations remains the dominant wildcard, with the potential to immediately reprice energy, inflation expectations and central bank paths across all regions simultaneously.

Brain Teaser #49

A fund manager runs a portfolio of 10 uncorrelated stocks. Each stock independently has a 60% probability of beating the market in any given year. What is the probability that the majority of the portfolio (more than 5 stocks) beats the market in a given year? And what is the probability that all 10 stocks beat the market simultaneously?

Brain Teaser #50

You have a 3-litre jug and a 5-litre jug, with no measurement markings. You have access to unlimited water. How do you measure exactly 4 litres?

0 Comments