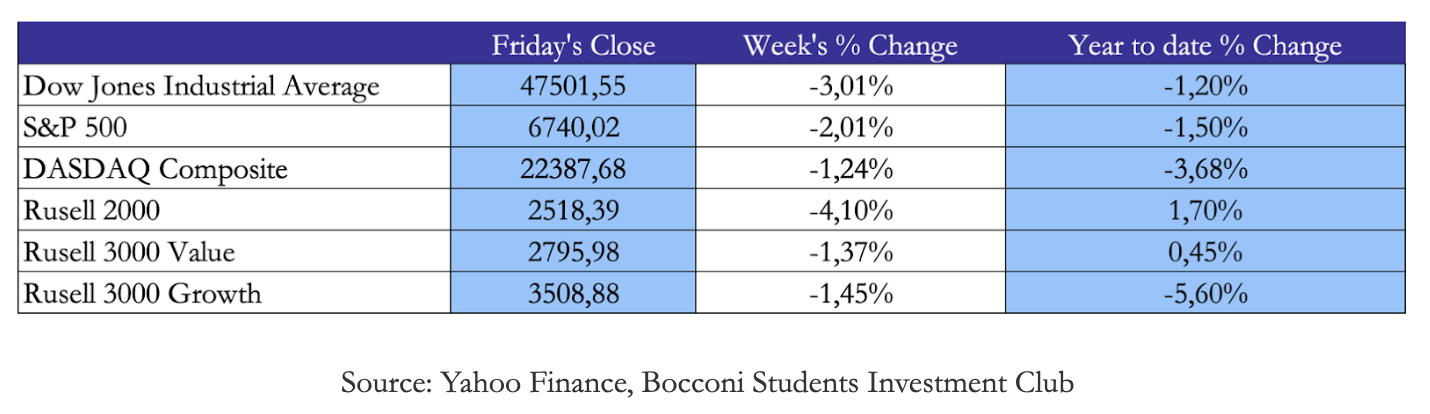

USA

March’s initial market regime is dominated by a sudden and aggressive return of geopolitical risk premiums and supply-side energy shocks. The American equity markets faced a period of pronounced defensive positioning this week, as the optimism that defined the early weeks of the year has been tempered by the reality of a protracted conflict in the Middle East and its implications for domestic inflation and monetary policy. The S&P 500 Index retreated 1.3% on Friday, effectively erasing its year-to-date gains as oil prices spiked to their highest levels since 2024. The major indices faced continued pressure, with the Dow Jones Industrial Average recording a decline of 0.9% or 453 points in a single session, after briefly plunging more than 945 points during intraday trading.

The sectoral performance was starkly divided. Energy and utilities sectors emerged as the primary beneficiaries of the heightened risk environment, buoyed by the sharp appreciation in crude oil and natural gas prices. Conversely, consumer discretionary and communication services sectors were the weakest performers, as investors rotated away from growth-oriented mega caps toward value-oriented defensive positions. Airline stocks suffered some of the most severe losses, with American Airlines dropping 5.2% and United Airlines falling 3.7% as rising jet fuel costs and Middle East travel disruptions threatened forward earnings.

The combination of geopolitical risk and warm inflation data has led market participants to aggressively scale back expectations for Federal Reserve rate cuts. The CME FedWatch tool currently signals a 95% to 99% probability that the Fed will leave the target federal funds rate unchanged at the upcoming March 18 meeting, maintaining the current band of 3.50% to 3.75%. Futures markets are now pricing in just one 25-basis-point cut for the entirety of 2026, a significant shift from the three cuts anticipated just weeks ago.

The combination of geopolitical risk and warm inflation data has led market participants to aggressively scale back expectations for Federal Reserve rate cuts. The CME FedWatch tool currently signals a 95% to 99% probability that the Fed will leave the target federal funds rate unchanged at the upcoming March 18 meeting, maintaining the current band of 3.50% to 3.75%. Futures markets are now pricing in just one 25-basis-point cut for the entirety of 2026, a significant shift from the three cuts anticipated just weeks ago.

Europe and UK

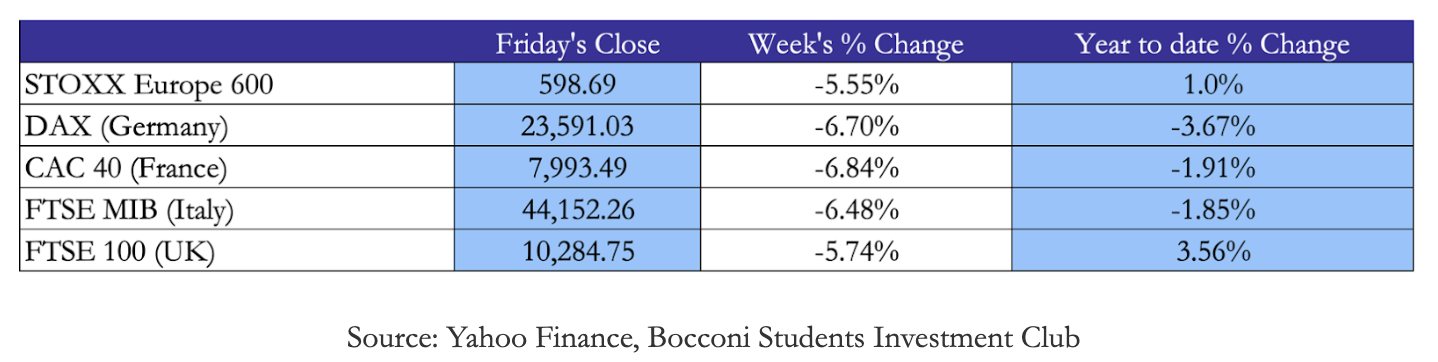

European markets faced a challenging week, characterized by a return to stagflationary concerns as rising energy prices coincided with softening economic activity indicators. The conflict in the Middle East has had a disproportionate impact on European sentiment due to the continent’s reliance on maritime trade through the Strait of Hormuz and its greater exposure to global energy price fluctuations.

The industrial sector has been hit by the dual reality of projected supply chain disruptions and the rising cost of energy. Schneider Electric and Safran saw sharp declines exceeding 5% for the week during the broader sell-off, despite some strong idiosyncratic earnings results in the aerospace sector. Luxury giants LVMH and Hermès saw their shares under persistent pressure as investors weighed the impact of the proposed 15% global U.S. tariff on discretionary demand. Conversely, STMicroelectronics plunged over 5% on Friday, as investors rotated away from the technology sector’s structural growth drivers in favor of defensive positioning.

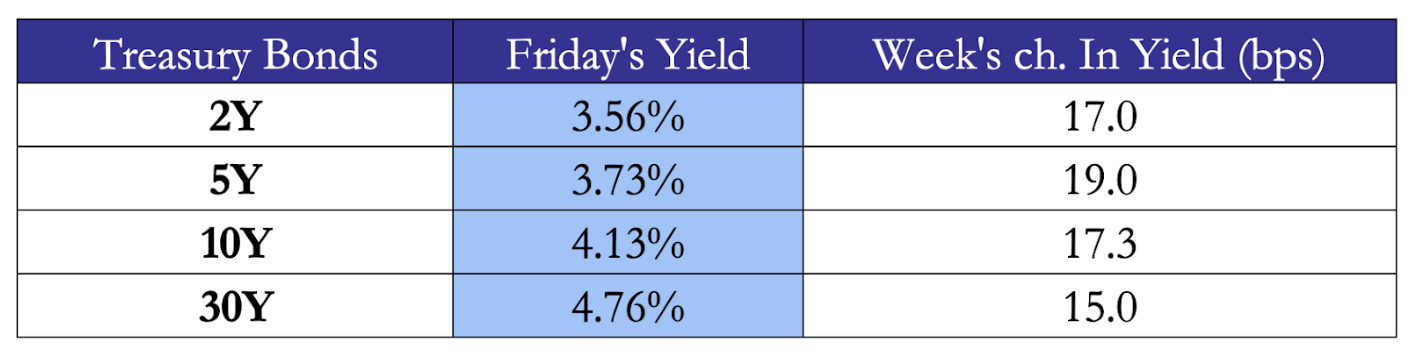

The United Kingdom has entered a period of significant fiscal and monetary uncertainty. The 10-year gilt yield surged to 4.57% by the end of the week, driven by rising inflation risks and a reassessment of the Bank of England’s (BoE) policy trajectory. Before the escalation of Middle East tensions, markets had priced in an 80% chance of a rate cut at the March 19 meeting; however, that probability has plummeted to less than 20%.

The United Kingdom has entered a period of significant fiscal and monetary uncertainty. The 10-year gilt yield surged to 4.57% by the end of the week, driven by rising inflation risks and a reassessment of the Bank of England’s (BoE) policy trajectory. Before the escalation of Middle East tensions, markets had priced in an 80% chance of a rate cut at the March 19 meeting; however, that probability has plummeted to less than 20%.

Fiscal projections from the Office for Budget Responsibility have added to the cautious tone. The 2026 UK growth forecast was revised down to 1.1% from 1.4% in November, even before accounting for the full impact of potential energy shocks. While the government has highlighted a reduction in borrowing by nearly £15 billion compared to a year ago, the rising cost of debt interest remains a significant headwind for the UK’s fiscal health.

Rest of the World

Rest of the World

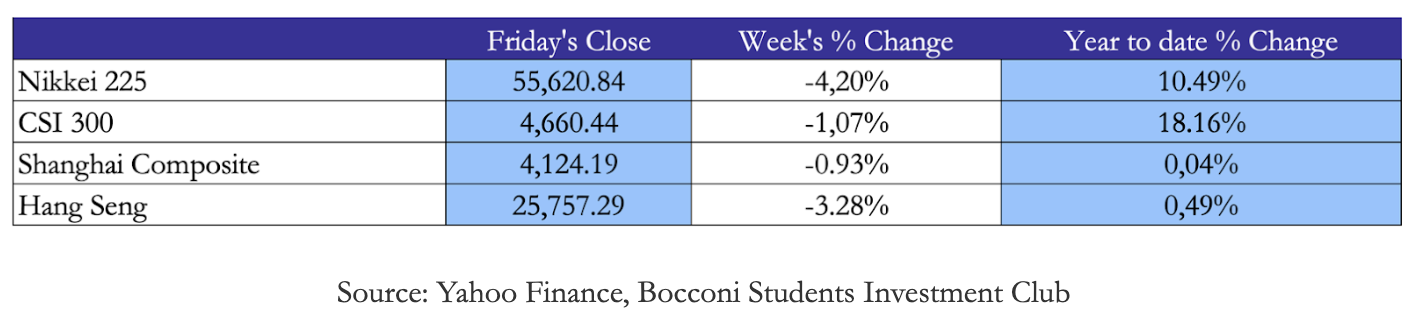

Japan’s equity markets displayed resilience to end the week, with the Nikkei 225 closing Friday at 55,620.84, maintaining its position above the significant 55,000 threshold. This bullishness is deeply tied to the “Takaichi factor.” Following a landslide election victory in February, Prime Minister Sanae Takaichi has secured a supermajority for the LDP, giving her a clear mandate to pursue a “responsible yet aggressive” fiscal policy.

Chinese markets ended the week on a positive note as the National People’s Congress (NPC) opened in Beijing. The Shanghai Composite Index rose 0.4% to close at 4,124.19, while the Hang Seng Index jumped 1.6% on Friday. The government set a GDP growth target for 2026 of 4.5% to 5%, the lowest such target in decades. This shift is interpreted as a move toward prioritizing “quality growth” over raw output, with a heavy emphasis on technological innovation and national independence. Policy focuses remain on AI self-sufficiency and the implementation of the 15th Five-Year Plan, which sets the stage for the next phase of China’s development.

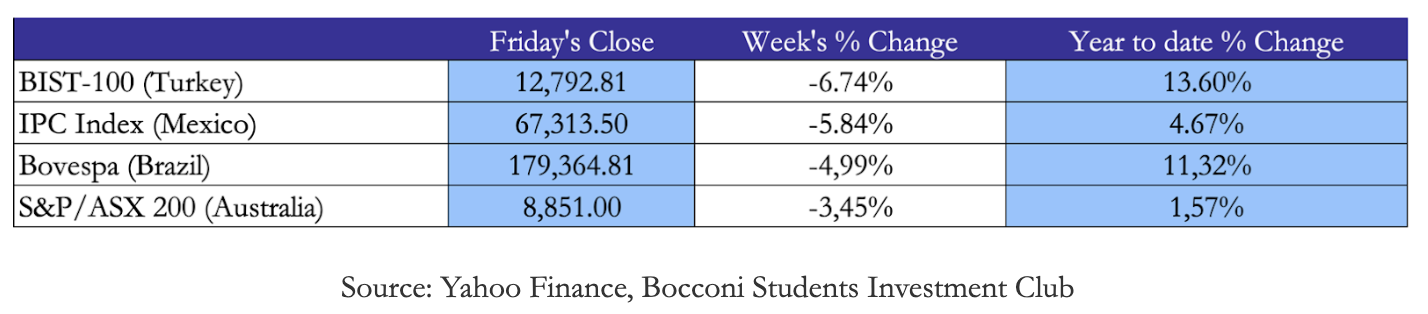

In Latin America, a similar pattern of resilience followed by volatility was observed. Mexican and Brazilian equities had a strong start to the year, with Brazil’s Ibovespa and Mexico’s IPC rallying 18% and 11% respectively in local currency terms. However, the week saw a broad retreat as global risk aversion drove domestic yields higher. The Ibovespa fell 0.6% on Friday as financial and industrial heavyweights were pressured by rising borrowing costs.

In Latin America, a similar pattern of resilience followed by volatility was observed. Mexican and Brazilian equities had a strong start to the year, with Brazil’s Ibovespa and Mexico’s IPC rallying 18% and 11% respectively in local currency terms. However, the week saw a broad retreat as global risk aversion drove domestic yields higher. The Ibovespa fell 0.6% on Friday as financial and industrial heavyweights were pressured by rising borrowing costs.

FX and Commodities

FX and Commodities

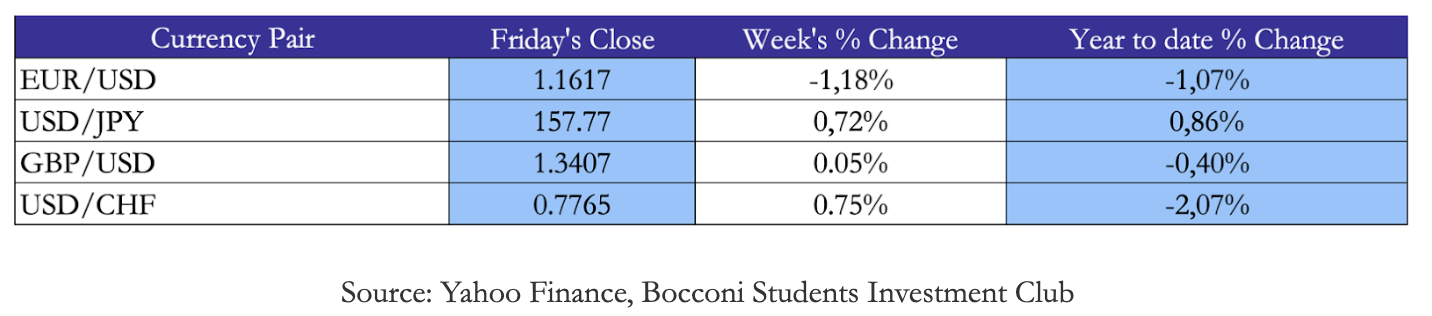

In the foreign exchange markets, the U.S. dollar has strengthened against almost all major currencies. The Dollar Index (DXY) climbed toward the 99.00 level, driven by a “net-short squeeze” in speculative positioning. The euro and British pound both retreated against the dollar, closing at 1.16 and 1.34 respectively. The Japanese yen has been under significant pressure, weakening toward the 157.80 level as the yield differential between the U.S. and Japan continues to widen and energy import costs drain the yen’s resilience.

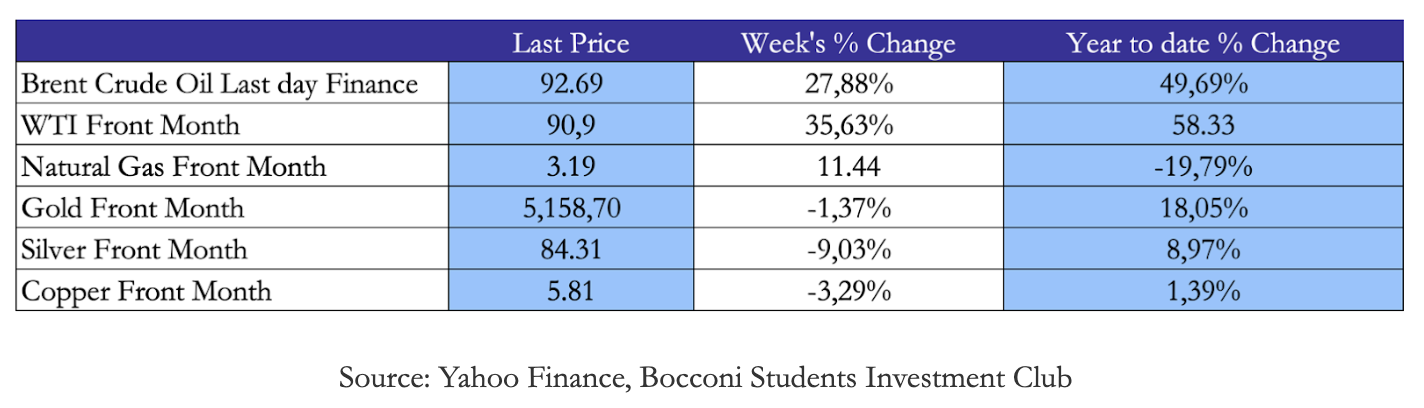

The energy complex has undergone a violent repricing as the Strait of Hormuz remains effectively closed by Iranian naval operations. The passageway, which handles 20% of the world’s oil and LNG shipments, has seen traffic reduced to a handful of vessels. Brent crude spiked to nearly $93 per barrel, its highest level since 2024, representing a 20% increase since the conflict began. WTI crude similarly surged to over $91 per barrel. Natural gas prices have been more mixed but remain elevated, with European gas forwards trading near €53 per MWh. The shutdown of major Iraqi oil fields due to storage capacity limits has further constrained global supply, creating a “perfect storm” for energy-driven inflation.

The energy complex has undergone a violent repricing as the Strait of Hormuz remains effectively closed by Iranian naval operations. The passageway, which handles 20% of the world’s oil and LNG shipments, has seen traffic reduced to a handful of vessels. Brent crude spiked to nearly $93 per barrel, its highest level since 2024, representing a 20% increase since the conflict began. WTI crude similarly surged to over $91 per barrel. Natural gas prices have been more mixed but remain elevated, with European gas forwards trading near €53 per MWh. The shutdown of major Iraqi oil fields due to storage capacity limits has further constrained global supply, creating a “perfect storm” for energy-driven inflation.

Next Week’s Main Events

Next Week’s Main Events

As markets enter the second full week of March, the focus will shift from immediate geopolitical panic to the evaluation of the longer-term economic fallout.

Brain Teaser #42

In a primitive society, every couple prefers to have a baby girl. There is a 50% chance that each child they have is a girl, and the genders of their children are mutually independent. If each couple insists on having more children, what will eventually happen to the fraction of girls in this society?

Solution:

Consider 100 couples.

- In the first round, 50 girls and 50 boys are born. 50 couples (those with girls) stop.

- In the second round, the remaining 50 couples have another child: 25 girls and 25 boys are born. 25 more couples stop.

- In the third round, 12.5 girls and 12.5 boys are born.

As shown, at each generation of birth, the ratio of boys to girls is exactly 1:1. The “stopping rule” merely changes the distribution of family sizes, not the underlying probability of each birth.

Brain Teaser #43

A plane flies from point A to B and then back from B to A, with a constant speed and no resistance. Later, the plane flies the same distance there and back, but with wind blowing from A to B, increasing the planes speed from A to B equally much as it reduces the planes speed from B to A. Does the full trip take longer, shorter or equal amount of time on the second fare?

0 Comments