USA

U.S. equities extended their rally this week, with the S&P 500 (+0.9% w/w) and the Nasdaq Composite (+1.1% w/w) both closing at fresh record highs, as investors looked through a still-challenging macro backdrop and focused instead on a crucial earnings test for mega-cap tech. The week made one point especially clear: the market is no longer rewarding AI spending indiscriminately, but is increasingly differentiating between companies that are already monetizing their investment cycle and those that are still asking investors for patience. In this respect, Alphabet and Apple were among the clearest winners, with the former benefiting from strong cloud momentum and the latter from solid results, a more measured capex profile and a new $100 billion buyback authorization, while Meta came under pressure after raising its spending plans further.

Macro data also helped sustain the bid for risk. U.S. GDP grew at a 2.0% annualized pace in Q1, up from 0.5% in Q4, while the ISM manufacturing index held at 52.7, confirming that activity remains in expansion territory. Even so, the underlying message was more nuanced: growth is holding up, but price pressures remain uncomfortable, with the ISM prices index jumping to 84.6, its highest level since April 2022. That mix did not derail equities, however, as easing oil prices into Friday and continued earnings strength allowed investors to maintain a constructive view on the broader market.

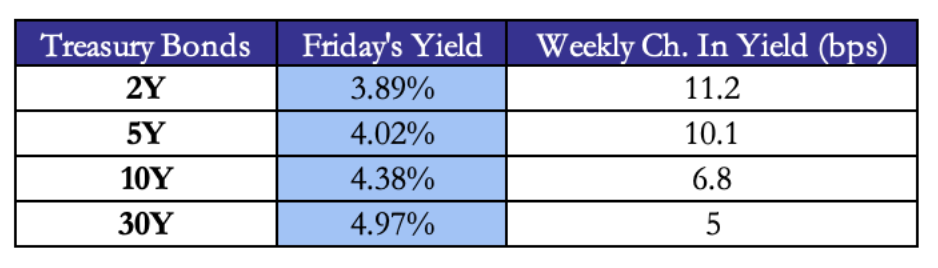

U.S. Treasuries told a more cautious story than equities this week. While stocks were able to look through the still-mixed macro backdrop and focus on earnings resilience, the bond market drew a different conclusion from the same set of information: if growth is holding up and inflation risks remain alive, the Fed has little reason to validate an easy easing path. That was ultimately the key message investors took from Wednesday’s meeting. The FOMC left rates unchanged at 3.50%-3.75%, but Powell did not offer a meaningfully dovish signal, instead reiterating that policy is not on a preset course and that future decisions will remain data dependent.

U.S. Treasuries told a more cautious story than equities this week. While stocks were able to look through the still-mixed macro backdrop and focus on earnings resilience, the bond market drew a different conclusion from the same set of information: if growth is holding up and inflation risks remain alive, the Fed has little reason to validate an easy easing path. That was ultimately the key message investors took from Wednesday’s meeting. The FOMC left rates unchanged at 3.50%-3.75%, but Powell did not offer a meaningfully dovish signal, instead reiterating that policy is not on a preset course and that future decisions will remain data dependent.

In that sense, rates were driven less by any single market move and more by the growing sense that the Fed is becoming harder to place on a simple cuts-only trajectory. The macro data released earlier in the week had already shown an economy that remains resilient, but for Treasuries that resilience was not reassuring: it implied that the Committee can afford to stay patient, especially with energy-related inflation risks still clouding the outlook. The result was a rates market that spent most of the week repricing toward a more cautious Fed, before stabilizing somewhat as oil prices pulled back into Friday.

This meeting also carried broader institutional significance, as it marked Powell’s final press conference as Chair. Powell said he intends to remain on the Board after the end of his chairmanship, which offers some continuity, but investors are already beginning to think about what a transition to Kevin Warsh could mean for the reaction function of the Fed. That uncertainty did not change policy this week, but it added another layer of ambiguity for the front end of the curve, especially at a moment when the central bank is trying to balance resilient activity, renewed inflation pressure and an increasingly complicated geopolitical backdrop.

Europe and UK

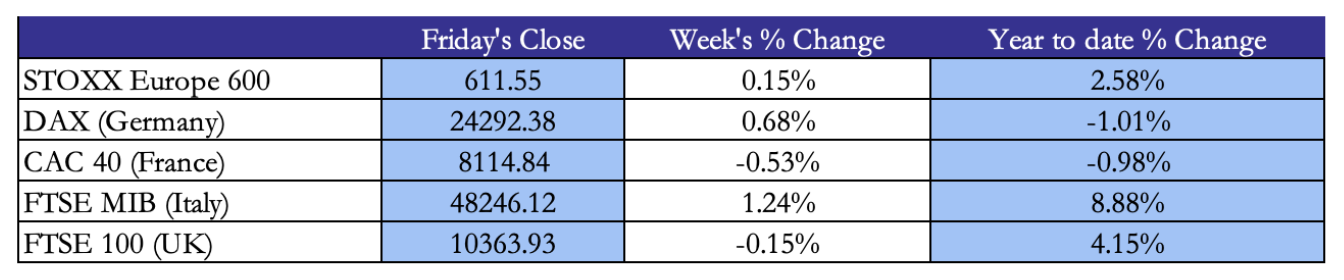

European equities closed the week on a surprisingly resilient footing, even as the macro backdrop became markedly less comfortable. The STOXX Europe 600 rose 0.15%, with the DAX (+0.68%) and especially the FTSE MIB (+1.24%) outperforming, while the CAC 40 (-0.53%) and the FTSE 100 (-0.15%) lagged. The dispersion suggested that investors were still willing to hold risk, but in a far more selective way than the headline performance alone would imply.

That resilience came despite a clearly worsening macro mix. The ECB left rates unchanged on 30 April, but its message was notably stern: the war in the Middle East has made the outlook significantly more uncertain, creating upside risks to inflation and downside risks to growth through higher energy prices. That warning landed just as euro area data confirmed a more uncomfortable backdrop, with Q1 GDP rising only 0.1% q/q and flash inflation accelerating to 3.0% in April. In that sense, European equities spent the week looking through a stagflationary scare rather than trading on any genuine improvement in fundamentals.

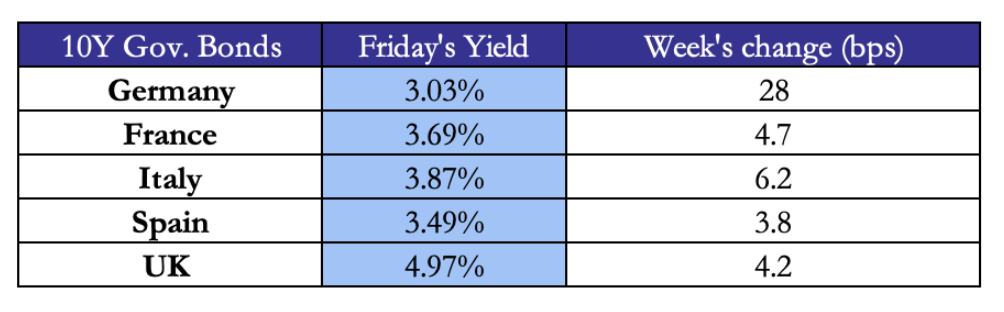

European sovereign bonds painted a much less relaxed picture than equities. The week’s move higher in yields reflected a market increasingly concerned that the energy shock linked to the Middle East — and, crucially, the persistent uncertainty around the Strait of Hormuz — could keep imported inflation elevated even as growth weakens. That concern was validated by the ECB’s 30 April meeting, where rates were left unchanged but the Governing Council explicitly warned that the conflict was raising near-term inflation through higher energy prices while simultaneously weighing on growth. In other words, the ECB did not tighten policy, but it did little to preserve the idea of a benign easing backdrop.

European sovereign bonds painted a much less relaxed picture than equities. The week’s move higher in yields reflected a market increasingly concerned that the energy shock linked to the Middle East — and, crucially, the persistent uncertainty around the Strait of Hormuz — could keep imported inflation elevated even as growth weakens. That concern was validated by the ECB’s 30 April meeting, where rates were left unchanged but the Governing Council explicitly warned that the conflict was raising near-term inflation through higher energy prices while simultaneously weighing on growth. In other words, the ECB did not tighten policy, but it did little to preserve the idea of a benign easing backdrop.

In the UK, the message was similarly cautious and arguably even more explicit. The Bank of England kept Bank Rate at 3.75%, but the 8–1 split, with one member voting for a hike, underlined how uneasy policymakers have become about inflation persistence. The MPC stated that the outlook for global energy prices is highly uncertain and that policy will need to ensure this shock does not become embedded more broadly. Against that backdrop, the rise in European and UK yields looked less like a mechanical rate move and more like a repricing of central-bank tolerance for another energy-driven inflation wave.

Rest of the World

Rest of the World

Asian equities were mixed this week, with Japan emerging as the region’s main market story. The Nikkei 225 fell 0.34%, as investors focused less on domestic earnings and more on the interaction between monetary policy, currency stress and higher energy prices. The yen briefly weakened beyond the closely watched 160 per dollar level before rebounding sharply, in a move widely interpreted by markets as reflecting official support for the currency or at least a credible threat of intervention. At the same time, the BoJ left rates unchanged, but the meeting still carried a hawkish undertone, as three board members argued for moving the policy rate toward 1.0%. For Japanese assets, the combination of suspected yen support, a more divided central bank and renewed uncertainty around the Strait of Hormuz left sentiment noticeably more cautious.

In China, the tone was firmer but not especially strong. The CSI 300 rose 0.80% and the Shanghai Composite gained 0.79%, while the official manufacturing PMI edged down only slightly to 50.3, suggesting that activity remained in expansion territory. By contrast, the Hang Seng fell 0.78%, reflecting a softer tone in Hong Kong amid lingering geopolitical and energy-related uncertainty. Overall, mainland equities looked more resilient than Japanese and Hong Kong markets, but the data still pointed to a recovery that remains steady rather than decisive.

FX and Commodities

FX and Commodities

FX markets reflected a week in which geopolitical risk and central-bank caution interacted very closely. EUR/USD ended almost unchanged at 1.1721, suggesting that the euro was not the main vehicle through which investors expressed concern. Instead, the clearest move came in the yen, with USD/JPY falling 1.44% as the Japanese currency rebounded sharply after the pair moved beyond the closely watched 160 level, reinforcing expectations of official support. The Swiss franc also firmed modestly, while GBP/USD rose 0.32%, even as the BoE maintained a cautious tone and warned that higher energy prices could keep inflation pressure alive. More broadly, the week’s FX action suggested that the dollar was not uniformly dominant; rather, markets used intervention-sensitive and safe-haven currencies to price a more uncertain global backdrop, especially after both the ECB and the BoE made clear that the shock from the Middle East was complicating the path for future rates.

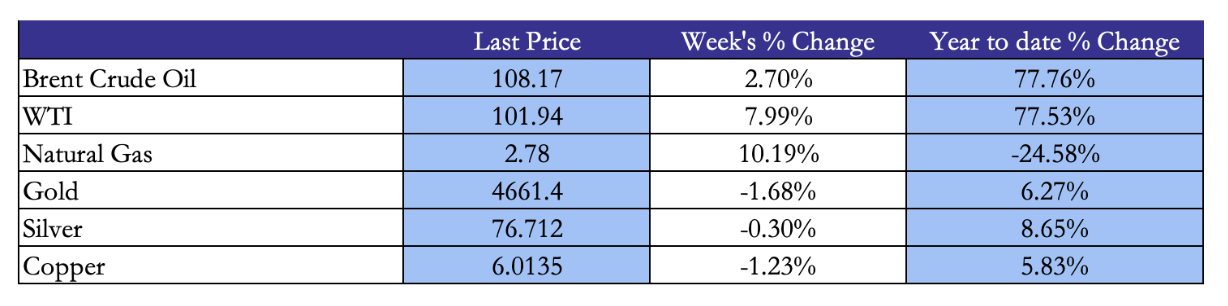

Commodity markets remained the clearest transmission channel for that uncertainty. Concerns around the Strait of Hormuz continued to support the energy complex, with Brent crude rising 2.70% and WTI gaining 7.99% on the week, even after oil retreated from its intraday highs into Friday. Natural gas also moved higher, underlining how broadly the market was repricing energy-related risk. By contrast, metals told a more nuanced story: gold fell 1.68%, suggesting that its geopolitical safe-haven bid was at least partly offset by a firmer rates backdrop, while silver and copper also edged lower, consistent with a market that was becoming more cautious on global growth as well as more concerned about inflation. In that sense, commodities this week did not simply reflect geopolitical escalation; they also reinforced the more hawkish tone that has recently emerged across major central banks.

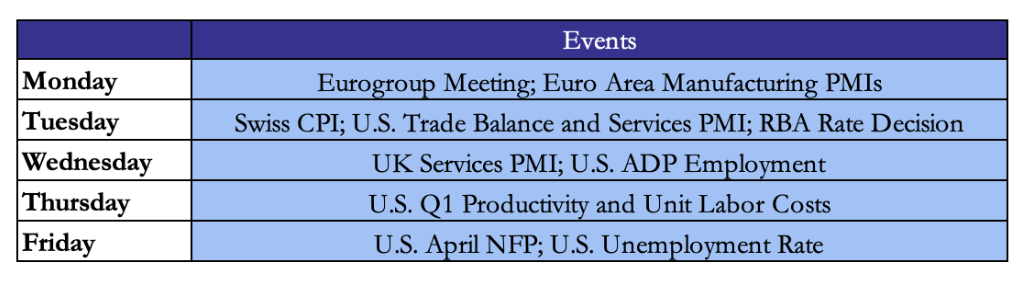

Next Week Main Events

Next Week Main Events

Next week, markets will remain focused on the U.S.-Iran talks mediated by Pakistan, although the tone remains fragile after Trump said he was not satisfied with Tehran’s latest proposal. At the same time, Washington has internally framed the conflict as having effectively ended, a move that helps the administration argue it does not need fresh congressional approval under the 60-day War Powers framework. Still, the situation remains far from normalized: the Strait of Hormuz is still closed and the U.S. naval blockade remains in place, meaning that any progress or setback in negotiations could continue to move energy prices, inflation expectations and front-end rates.

On the macro side, the main focus will be on the U.S. labour market, with JOLTS on Tuesday and the April payrolls report on Friday likely to shape expectations for the Fed. In between, Q1 productivity and labour costs on Thursday should also be watched closely, especially after last week’s more cautious central-bank tone.

Brain Teaser #47

Eight points are chosen independently and uniformly at random on the circumference of a circle. What is the probability that all eight points lie within some semicircle?

Brain Teaser #48

You are given five identical-looking chains, each made of three gold links. It costs 1 coin to open a link and 1 coin to close a link. What is the minimum cost required to assemble the five chains into one single necklace?

0 Comments