Introduction

When it comes to pizza restaurant franchises, Domino’s [NYSE: DPZ] is a household name across the world. Trading at a current stock price of $476, it is down 6.5% in the last six months. Despite many sell side analysts revising their target price downwards for Domino’s over the last year, due to the competitive nature of the fast food restaurant industry and the company missing new store estimates, Warren Buffet’s Berkshire Hathaway announced a $550m stake in the company earlier this month in its most recent 13F filing. With Domino’s missing targets of new store openings over the last year, it raises the question as to why the hallowed stock picker has taken such an outsized position in the company, whilst selling out of the majority of his other positions such as Apple [NASDAQ: AAPL] and Bank of America [NYSE: BAC], in favour of building a sizable cash position.

Business Model

Domino’s diversified revenue streams are crucial in maintaining its position as a global leader in the fast-food industry. With operations spanning over 90 countries, Domino’s revenues can be broken down into five business units:

- US Company Owned Stores

- US Franchise Royalties and Fees

- US Franchise Advertising

- Supply Chain

- International Franchise Royalties and Fees

Each of these plays a strategic role in strengthening and maintaining Domino’s market leadership and contributes to its revenues as explained below:

U.S. Company-Owned Stores (c. 8.4% of revenue in 2023)

Domino’s operates 288 company-owned stores, which, beyond simply contributing to cash flow through sales, also help strengthen Domino’s credibility as a franchisor. These stores are test sites for new technological advancements, promotional strategies and operational improvements. These are refined and optimised for effectiveness and scalability before rolling out across its extensive franchise network.

US Franchise Royalties and Fees (c. 13.5% of revenue in 2023)

Domino’s derives consistent cash flows from its 6,566 US franchised stores through a stable revenue model that includes a weekly 5.5% royalty fee on gross sales and technology fees paid by franchisees. This model is underpinned by a consistently high franchise agreement renewal rate of 99% in 2023, reflecting strong franchisee confidence and alignment with the brand.

US Franchise Advertising (c. 10.6% of revenue in 2023)

Domino’s collects a 6% advertising fee from US franchisees, temporarily reduced to 5.75% in 2023, to fund national and local marketing efforts. These contributions support media buys, promotional production, public relations and market research through Domino’s National Advertising Fund Inc. (“DNAF”). By driving brand visibility and increasing franchisee sales, these campaigns indirectly enhance cash flow through higher royalty revenues, aligning franchisees’ success with the company’s financial performance.

Supply Chain (c. 60.6% of revenue in 2023)

Domino’s operates 22 US supply chain centres and additional facilities in Canada, supporting over 7,400 stores by producing and delivering fresh dough, food and supplies. Franchisees voluntarily purchase from these centres due to their efficiency, cost-effectiveness, and consistent quality. Profit-sharing agreements return 50% of pre-tax profits to franchisees who source all supplies from Domino’s, helping attain volume growth while aligning incentives to maintain robust partnerships.

International Franchise Royalties and Fees (6.9% of revenue in 2023)

Domino’s generates revenue from royalty payments averaging ~3% of sales and technology fees across 90+ countries, leveraging a capital-light model. Most international stores are managed by master franchisees, who pay upfront franchise fees, ongoing royalties, and technology fees. These agreements include growth clauses requiring store expansion, ensuring consistent revenue growth with Domino’s brand power supporting each new opening. This model delivers steady cash flows with minimal operating expenses and leverages the master franchisees’ local market expertise and capital investment.

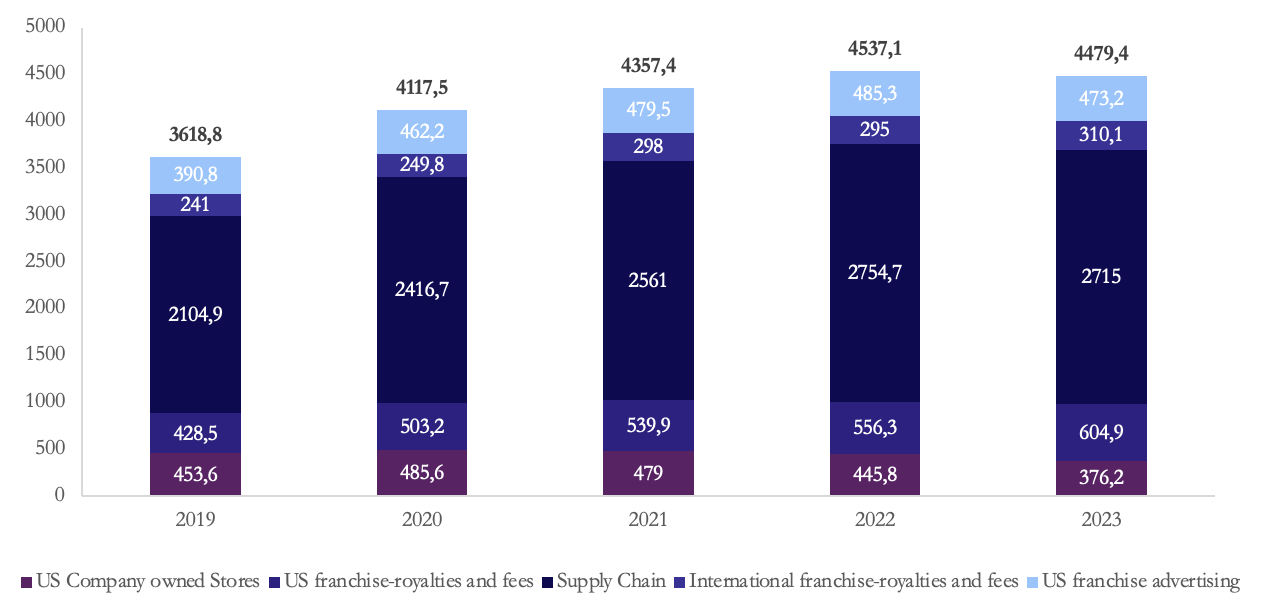

Over the past five years, each of these five business units has experienced slight fluctuations in its contribution to Domino’s overall revenue. Despite these variations, they have collectively driven steady growth, with a minor downtick observed in 2023, depicted in the graph showing historical revenue by business unit ($m):

Thesis #1: Hungry for MORE yielding results

One of Domino’s key strategies at the heart of their long-term plan is their “HUNGRY FOR MORE” strategy. “MORE” represents their four strategic pillars; Most Delicious Food, Operational Excellence, Renowned Value, Enhanced By Best-In-Class Franchisees. The first point represents not only the need to produce high quality food but to also showcase their product through marketing and innovation. Operational Excellence, shows their aim to focus on efficiency, consistency and reliability to deliver great service. Renowned Value is Dominos’ desire to have a strong market presence and to continue expanding in the market, and the final point is to constantly expand and improve their franchisees. These 4 strategic goals by Domino’s all aim to drive MORE sales, stores and profits for the company.

This strategy was first executed in Q4 2023, where each store experienced profit growth to $162K in EBITDA in 2023, a $23K increase compared to 2022. On top of this, in the US alone, Domino’s added over 60 new franchisees and opened 168 net U.S. stores, which are both increases compared to previous years. Internationally, Domino’s succeeded in reaching a net store growth of 702 units in 2023.

Looking ahead for the next 5 years, Domino’s aims for a 7%+ growth in global retail sales, and aims to open 1,100+ net new stores annually worldwide, so 5,500 over the next 5 years. Regarding profit, the company aims to increase operating profit at 8%+ annually.

Same stores sale growth is the primary driver of Domino’s global sales growth; in Q1 2024, global retail sales growth was +7.3%, with the US same stores sale growth at +5.6% and internationally being +0.9%. With overall US stores sales growth being +7.8%, it is evident sales growth was largely driven through growth in pre-existing stores. When comparing the first three fiscal quarters in 2024 to 2023, global retail sales growth was +6.5%, with US same store sales growth being +4.5% and internationally this figure is +1.1%. This indicates Domino’s global sales growth success comes from high performance of its existing stores, suggesting the stores are being run efficiently and consumer demand remains strong.

Recently, Domino’s have experienced a slowdown in new stores; with Q1 2024 net store growth being 164, which has now subsequently dropped in Q3, where growth is only 72 stores. They are expected to fall short around “175-275” units below its 2024 goal of 925+ units internationally. This is driven by closure of stores in Japan and France, where they are expected to close 5% (net) of stores, around 100-120 stores. This is expected to have a positive impact on earning and Domino’s plan to reinvest these earnings into marketing and advertisement. Despite this, same store sales remain strong, especially domestically with Domino’s having a +4.5% same stores sales growth in the first three quarters of 2024 in the US, far larger than the previous figure of +1.0% in the same period in 2023. The stock’s overreaction to missing new store targets, we believe will be surmounted by resilient same store sales growth that we have seen so far this year.

Thesis #2: A Resilient Business Model in a Cutthroat Industry

The competitive dynamics of the pizza industry have intensified, with segment trends pointing to a full-fledged price war that is squeezing margins across the sector. At the heart of this battle is the relentless pursuit of value-driven customers, a trend that has forced players to adopt aggressive pricing strategies to maintain market share.

Unlike some competitors that aggressively lower prices or offer unsustainable promotions like free delivery, Domino’s has taken a more refined approach. By strategically adjusting its key price points, the company has focused on maintaining a strong relative value proposition rather than engaging in a full-scale price war. One of Domino’s key strengths lies in its operational efficiency and high order volumes, which allow it to sustain competitive pricing without sacrificing profitability. This approach enables the company to prioritise profit through scale rather than narrow margins. Instead of racing to the bottom on price, Domino’s continues to differentiate itself by balancing innovation and value, ensuring its offerings remain compelling to cost-conscious customers. Domino’s supply chain efficiency and high order volumes serve as a strong buffer against price-related headwinds caused by macroeconomic factors, such as geopolitical conflicts or trade policies like tariffs. While such challenges may strain competitors, Domino’s market leadership—accounting for over 20% of market share—provides a significant advantage. This dominant position allows the company to absorb external pressures more effectively, minimizing the impact on its bottom line.

Another way size plays to Domino’s advantage is through its marketing efforts, a cornerstone of its strategy. With the ability to invest significantly more than competitors, Domino’s consistently reinforces its dominant market position. This is particularly impactful in an industry where consumer preferences and brand loyalty are fiercely contested. By maintaining a strong and consistent presence across advertising channels, the company not only captures attention but also strengthens its connection with value-driven customers, ensuring its leadership remains firmly established. Initiatives like “MOREflation,” offering “more for less” during periods of rising costs, and “Boost Week,” featuring 50% discounts to attract new and repeat customers, demonstrate a calculated effort to drive volume without undermining long-term profitability. Through these strategies loyalty redemptions doubled in the first half of 2024 compared to the previous year, with particularly strong growth in carryout orders. This demonstrates the success of the updated program in attracting new users, increasing order frequency, and enhancing customer loyalty. Partnerships with platforms like Uber Eats have expanded reach to younger, urban demographics willing to pay for convenience, while reimagined promotions such as “Emergency Pizza 2.0” highlight adaptability and innovation. The redesigned loyalty program further exemplifies this customer-centric approach. By lowering the spending threshold and introducing flexible reward tiers, Domino’s has made rewards more accessible, encouraging repeat purchases and deepening engagement with value-driven customers.

Another key aspect of Domino’s strategy is its strong focus on carryout, a channel that aligns closely with shifting consumer preferences and economic realities. In a time where economic pressures drive consumers to seek cost-effective dining options, carryout has emerged as an attractive alternative to delivery, allowing customers to avoid additional fees such as delivery charges and tips. By adapting to these shifting preferences, Domino’s not only meets customer expectations but reinforces its reputation as a brand attuned to its clients’ financial realities. This strategy synergizes with the aforementioned marketing initiatives. By tailoring its loyalty program to better serve carryout customers—lowering spending thresholds and introducing flexible redemption tiers—Domino’s has further enhanced its appeal, fostering deeper customer engagement and loyalty. This strategic focus not only addresses immediate client needs but also positions Domino’s as a brand that consistently adapts to changing market dynamics, reinforcing its long-term leadership in the industry.

Valuation: Discounted Cash Flow Analysis

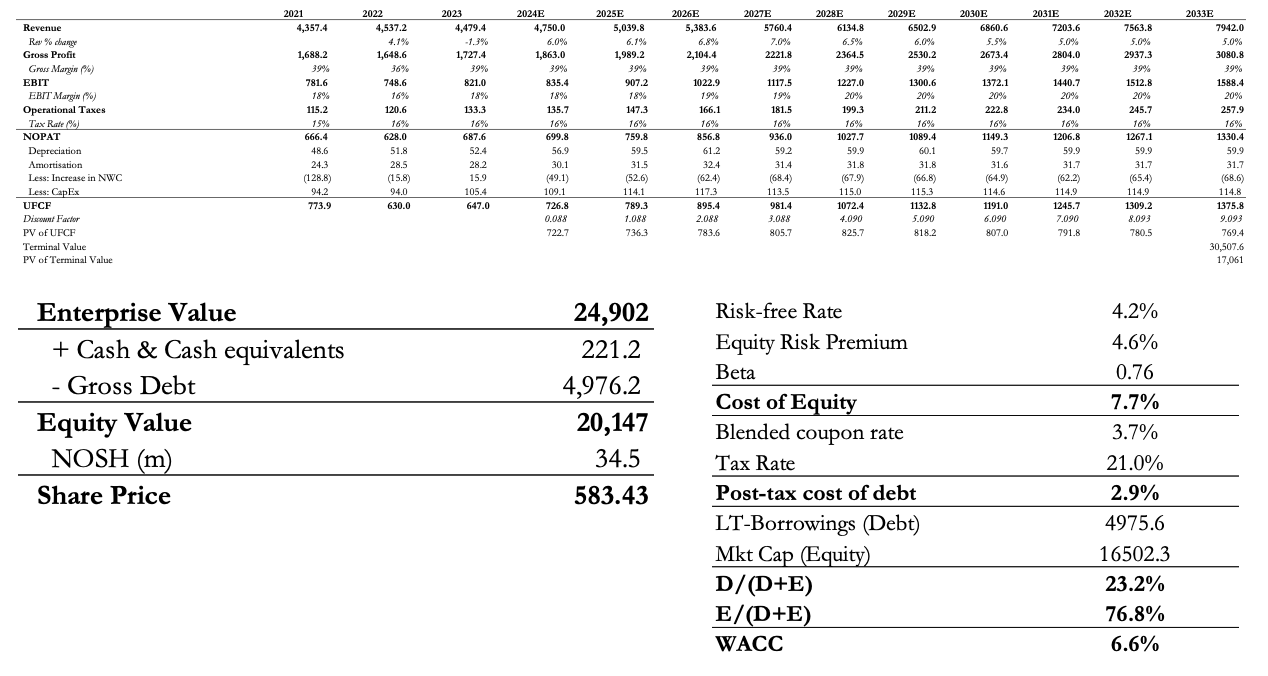

Under our base case, we observe an intrinsic target price of $583 representing a 24% upside to its current share price of $496, through our discounted cash flow (DCF) analysis. This is assuming a valuation date of 29th November, a weighted average cost of capital of 6.6% and a terminal growth rate of 2.0%, which are broadly in line with sell side consensus. Our base case assumptions are outlined in the operating model build below, with all figures in USDm apart from share price data:

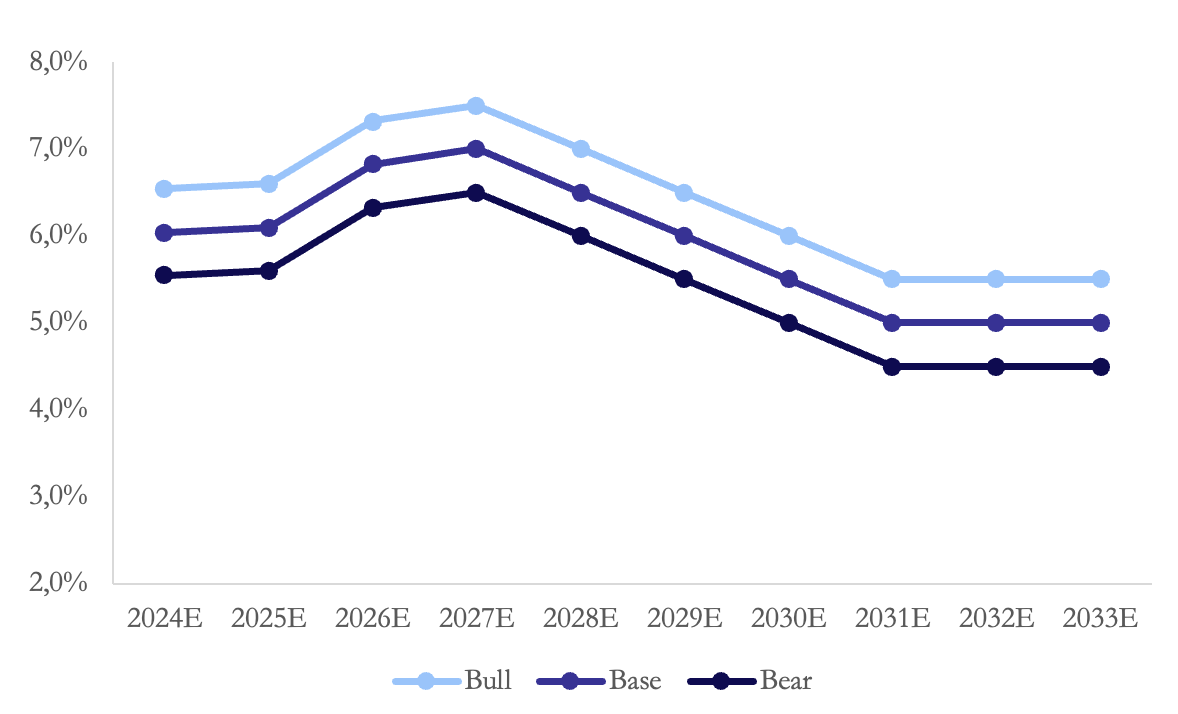

Under our bullish case, we find a target price of $606 marking an upside of 29% to the current market price, whilst in our bearish case, we find a target price of $561 with an upside of 21% to the current trading price. Our assumptions between our cases change for our year-on-year revenue growth as shown in the graph below:

The table below shows our share price sensitivity with respect to the chosen weighted average cost of capital and to the terminal growth rate:

Even under different, conservative revenue growth cases, terminal growth rate assumptions and weighted average cost of capital assumptions, we find that the stock is intrinsically undervalued and that there is significant upside.

Valuation: Trading Multiples

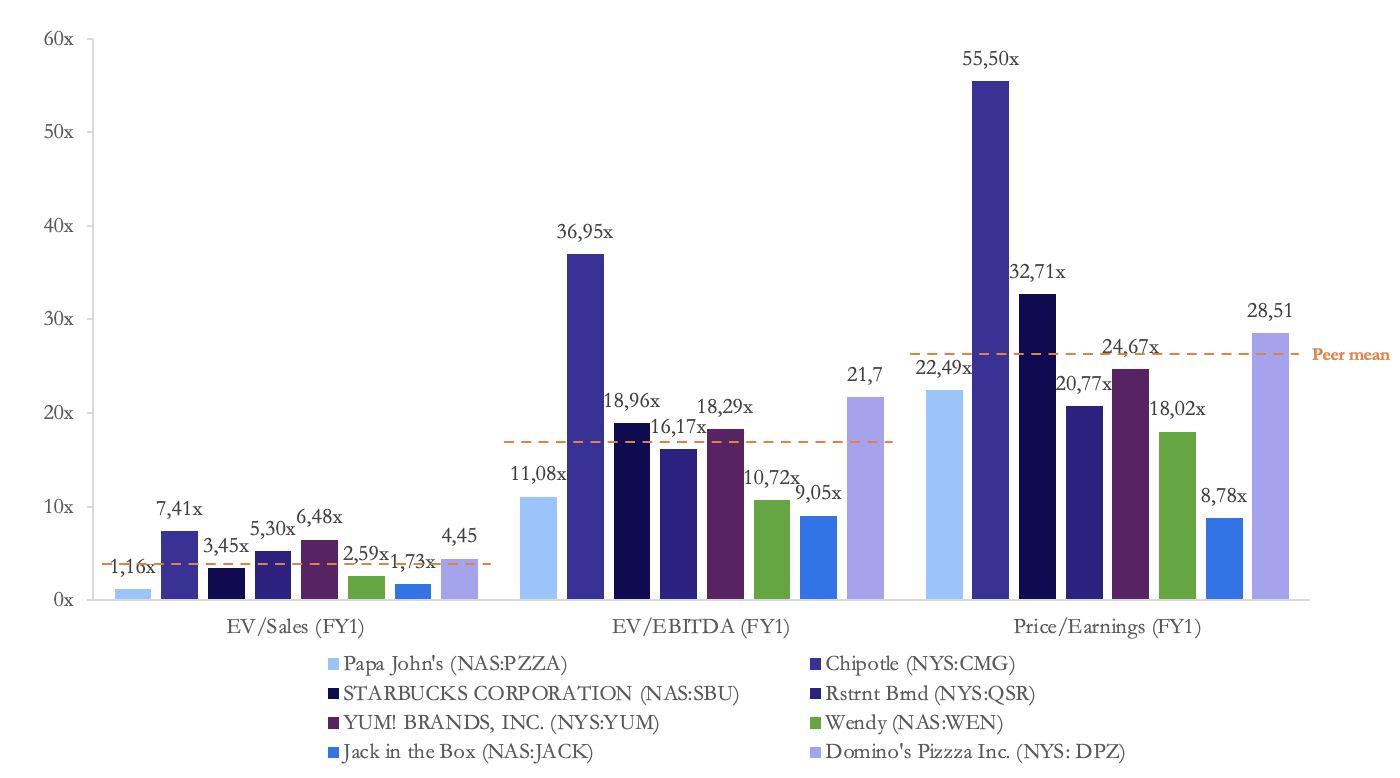

Papa John’s [NASDAQ: PZZA] is a close competitor in the pizza industry but operates on a smaller scale. With a market capitalization of $1.63bn, it is significantly smaller than Domino’s. While Domino’s has twice the revenue of Papa John’s, this stems from Domino’s expansive international supply chain and greater global presence. Domino’s trades at a significantly higher EV/EBITDA multiple, reflecting its superior market position and revenue generation.

Chipotle [NYSE: CMG] is a fast-casual dining chain offering high-quality, fresh Mexican cuisine. The company owns and operates all its restaurants, with 3,200+ locations across the US, Canada and Europe. With a market capitalization of $84.5bn and an EV of $79.5bn, Chipotle trades at an EV/Sales multiple of 7.24x and an EV/EBITDA multiple of 34.95x, both significantly higher than Domino’s. These high multiples reflect Chipotle’s premium positioning and strong growth prospects, driven by its commitment to quality and efficient expansion strategy. Domino’s, while trading at lower multiples, excels in supply chain efficiency and global penetration in the QSR segment.

Starbucks [NASDAQ: SBUX] is a globally renowned quick-service restaurant specialising in coffee, pastries, and other food items. With a market cap of $116.2bn and EV of $123.8bn, Starbucks trades at an EV/Sales multiple of 3.42x and an EV/EBITDA multiple of 18.40x. These multiples reflect its strong global presence, commanding 37% of the coffee market and its premium brand positioning. While Domino’s focuses narrowly on pizza delivery and takeout, Starbucks benefits from a diversified product portfolio, in-store customer engagement, and higher average spending per customer, driving its superior valuation metrics.

Restaurant Brands [NYSE: QSR] operates globally through brands like Burger King and Popeyes. Its market capitalization is significantly higher than that of Domino’s at $44.2bn due to owning a couple of big fast-food chains. However, Domino’s outperforms Restaurant Brands in revenue efficiency, given its tighter focus on the pizza segment and higher revenue per store.

Yum! Brands [NYSE: YUM] is a global leader in the quick-service restaurant (QSR) industry, owning iconic brands like KFC, Pizza Hut and Taco Bell. With a market cap of $37.8bn and EV of $48.2bn, Yum! Brands trades at an EV/Sales multiple of 6.68x and an EV/EBITDA multiple of 18.82x. These multiples reflect its diverse portfolio of over 55,000 restaurants across 155 countries, enabling it to dominate multiple segments of the QSR market. While Domino’s focuses exclusively on pizza, Yum! Brands benefits from its diversified operations, contributing to its broader appeal and higher valuation metrics.

Wendy’s [NASDAQ: WEN] is a US-based quick-service restaurant chain specializing in fast-food hamburgers and other menu items like chicken sandwiches, salads and breakfast offerings. With a market cap of $3.7bn and EV of $5.8bn, Wendy’s trades at an EV/Sales multiple of 2.61x and an EV/EBITDA multiple of 11.16x. These lower multiples reflect Wendy’s smaller scale, with 6,500 restaurants across 29 countries and slower revenue growth, which stood at $562m as of Q2 2023. While Wendy’s continues to expand globally, Domino’s outperforms Wendy’s in revenue efficiency, global presence and operational scalability, leading to higher valuation metrics for Domino’s.

Jack in the Box [NASDAQ: JACK] is a smaller player with a market capitalization of $900m. Its financial metrics, including revenue and enterprise value, are significantly lower than Domino’s. Domino’s trades at higher multiples, supported by its larger scale, robust supply chain and industry-leading margins.

In conclusion, Domino’s Pizza demonstrates a strong position within the quick-service restaurant (QSR) industry due to its focused business model, robust supply chain and global reach. While trading at lower multiples than diversified and premium-positioned peers like Chipotle and Starbucks, Domino’s outperforms smaller competitors like Papa John’s, Wendy’s, and Jack in the Box in revenue efficiency and operational scale. Compared to multi-brand operators like Yum! Brands and Restaurant Brands, Domino’s valuation reflects its narrower product focus but superior efficiency in the pizza segment. These differences in business models, scale, and market strategies explain the varying valuation multiples across the competitive landscape.

Conclusion

Despite the slowdown in new store openings, Domino’s has shown strong same store sales growth, which has historically and continues to be driving Domino’s top line. We believe pessimism amongst the market is unfounded considering strong demand driving this sales growth is likely to stay, despite supply chain issues in certain international markets delaying new store openings. This has been bolstered by various initiatives such as the recent rollout of their new loyalty plan that has proved to be far more successful than previous ones. Despite an industry that some analysts believe is offering homogeneous products and is a race to the bottom, Domino’s beats its competitors in sustaining competitive pricing whilst keeping high margins by balancing innovation and value. Programs such as “MOREflation” and “Boost Week” will continue to help Domino’s drive volume and retain customer loyalty. With these thesis points in mind, our DCF analysis suggest significant upside to this stock at current market prices. Whilst our multiples analysis does show that the stock currently trades at a slight premium to the average of its peers, we believe that if Domino’s is able to successfully turn the narrative around by continuing strong same store sales growth and bouncing back from the supply chain holdups that delayed international store openings, the stock can trade at the higher end of the range of its peer groups.

0 Comments