When we analysed luxury stocks, we stressed that the industry has faced a downturn, probably due to a kind of sector rotation. The same phenomenon has affected European banks and utilities in the opposite way. In this article, we focus on banks, proposing some ideas on how to trade them. In particular, we decided to concentrate on Italian retail banks: the choice is backed by the fact that they seem to be among the most volatile and, so, they are the best evidence for testing our ideas. In addition, major European banks are included in the sample to make the comparison easier.

Among the different factors that may affect banking stocks prices, we focused on two trends: on the one side, we considered the spread normalisation; on the other side, we concentrated on short-term drivers.

Spread normalisation

The spread between Italian 10y BTP and German 10y BUND has incredibly diminished recently, due to the better general economic situation in Europe; consequently, banking stocks have raised: indeed, banks hold a huge portion of national public debts and an increase in the price of those assets is immediately reflected in their values. Now, we asked ourselves if the reaction is standardised or not… And the answer is clearly not!

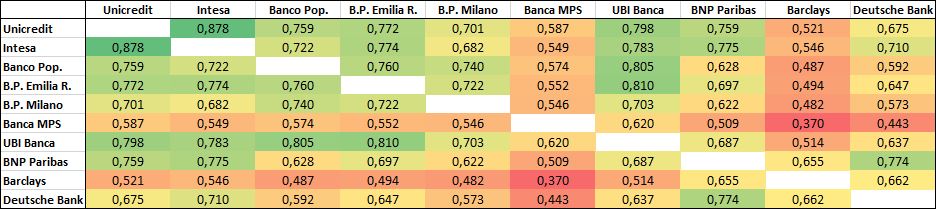

Source: BSIC

As we can see in the table above, correlation between banking stocks is high, with a mean of 0.588, but there are significant differences. The stocks that show the highest correlation with the sample are the biggest Italian banks (Unicredit and Intesa SanPaolo), while Barclays and Banca Monte dei Paschi di Siena (henceforth, Banca MPS) have the lowest levels. For the British institution, it is reliable to think that it may be caused by a sample construction bias (most of banks are Italian), while the second is affected by its own troubles. Since we have taken into account a quite relevant period (more than 2 years) relative to the short time-horizon of our study, it is feasible to assume that this behaviour has become quite structural.

After that, we did something more interesting: we computed the betas of these banks: however, instead of taking the market as benchmark, we calculated their coefficients against the spread between BTP and BUND, which seems to be a good measure for short-term confidence. Here we are: (part of) our trade idea is to play the spread, either up or down!

Of course, some banks are very reactive, being more exposed to the national situation: especially, we noticed that Banca Popolare dell’Emilia Romagna (henceforth, BPER), Unicredit and Banco Popolare are the stocks with the most negative 2y betas (given the negative relation, the lower the spread, the better for the banks). On the opposite side, Barclays and Deutsche Bank are less reactive to spread movements (because they are not Italian and they are “more universal” banks probably). We think, therefore, that we could combine different “spread betas” to build a hedging strategy.

Short-term catalysts

Now, we can move to another factor: the need of identifying a short-term catalyst for banks stock prices. Before the crisis, the main metrics to analyse and valuate banks were dividends and ROE: indeed, banks were quite clear dividend-paying companies and there was visibility on their expected earnings. Nonetheless, things are much different now: many banks have stopped to pay dividends and have been facing losses (mainly due to impairments of assets and non-performing loans) for the last years. In this context, the focus has moved towards solvency instead of profitability and P/BV has become one of the main tools used to valuate banks. P/BV is usually regressed against ROE; nevertheless, we tried to find something more short-term oriented, and taking into account that annual results for 2013 of several institutions will be released in the next weeks, we decided to focus on the Net Interest Margin %. This analysis seems to work well only for companies of the same country, probably due to their similar structures: for example, Italian banks are less profitable and less cost-efficient than other European credit institutions. Therefore, we performed the analysis for Italian banking stocks and obtained the following results.

The regression study would suggest, for instance, going long Banca MPS and BPER, while shorting Intesa SanPaolo: quite risky in our opinion, since Intesa is the preferred stock of international investors right now and it has showed to have an enormous strength relative to the index. Furthermore, this kind of analysis, despite being academically interesting, is often imperfect practically: it depends on several variables that can be modified easily. However, the important point is that it allows us to understand that expected Net Interest Margin can be a good market mover.

After that, given the market reaction to the announcements of capital increases of popular banks, we strongly believe that the likelihood of additional capital needs should be included in the analysis. Actually, BPER is only the last bank to disclose that it is evaluating that option, while Banca MPS, Banco Popolare and Banca Popolare di Milano have already discussed it with shareholders.

Trade ideas

That said, we tried to put everything together. Banks have recovered strongly since the beginning of February and are now approaching relative maximums; among them, popular banks have outperformed the market. However, it was just a speculative rally, also fuelled by the closure of huge short positions on the stocks, in our opinion. Anyway, we think that popular banks can be a good buy opportunity with a time horizon of some months: in fact, new industrial plans and rumours about changes in governance structure, along with successful capital increases, may pave the return of investors; but they could be shorted right now.

The most evident situation is Banca Popolare di Milano. The stock reached a maximum at 0.65 on March, 6th: that was, in our opinion, a perfect point to open a short position on the popular bank. Our targets are: 0.586 as a first intermediate goal by the end of March; 0.521 as a more ambitious area, to be reached by mid April.

Banco Popolare is in a similar situation: the stock is evidently overbought and needs to consolidate at lower levels. Moreover, we should remember that the share plunged after the announcement of the capital increase, before recovering in the following weeks. This is an important point to bear in mind: once the correction will end, popular banks are likely to restart growing, but there may be further negative impact once the subscription price will be announced. Indeed, despite the fact that a right issue should be economically neutral for long-money investors (if they exercise their rights), its launch can be painful for short-term traders.

Also BPER reached a maximum on the 6th, but the retracement has already been strong in this case, due to the statement, released on Friday, about chances that a capital increase will be necessary; but, if our view comes out to be correct, there will be further collapse in the next weeks.

Moving to a medium-term view (i.e., after the correction wave), we would stress the following: also taking into account the capital increase risk, we still prefer big, well-capitalised banks for long positions. Unicredit and Intesa SanPaolo (our top choices), along with UBI Banca, are likely to offer the best risk-return profile, being highly reactive to spread changes at the same time.

Anyhow, our negative view on the stocks of the industry is extended also towards these big institutions in the very short-term, implying that annual results will not be accepted very well by markets. Nonetheless, considering Unicredit for instance, it seems that the downside risk is still lower than that of popular banks, even though the bank is the most exposed to Ukraine – Russia turmoil.

[edmc id=1453]Download as pdf[/edmc]

0 Comments