Introduction

Since the 2008 Crisis, several events have undermined the global trust in the major financial benchmarks. Above all, the London Interbank Offered Rate (LIBOR) had its reputation impaired, and its role weakened.

The spike in its value after the collapse and bail-out of leading banks posed doubts about its applicability in derivatives pricing. After, the manipulation scandal raised concerns about its reliability. Eventually, the lowering in the transaction volumes of its underlying market has induced suspicions about a possible cessation of its publication.

Against this background, several international institutions have begun a joint work for addressing these issues. In this study, we will illustrate the major steps of this process. After analyzing the reasons of LIBOR’s weakness, we will illustrate the most recent attempts to make it more resilient to manipulation and market stress, together with the introduction of new rates, one of which is set to become the new benchmark for the USD market.

LIBOR: the reference rate and the manipulation scandal

During the 60s, US banks started settling their branches in London. Locating dollars deposits (Eurodollar) outside their jurisdiction, they expanded their business. The US dollar was already the most important currency in the World: countries as Russia and China needed it for the sole fact that oil was traded only in US dollars. At the time, regulatory restriction on deposits in the US helped the flourishing of this market, which benefited firstly from the presence of interest rate ceilings on deposits at banks in the USA, a condition that became even more onerous as rates started rising worldwide; secondly, from the stricter prudential control on the US banking sector as compared to the London one, which imposed higher deposit insurance premiums while holding more non-interest-bearing reserves. Therefore, international banks could offer more attractive interest rates and lower borrowing costs locating their activity in London rather than in New York.

In this context, in 1969, Mr. Minos Zombanakis, a Manufacturer’s Hanover’s Greek banker, signed an $80m loan for the Shah of Iran, charging a rate linked to market conditions. He named this rate “LIBOR”, which stands for London Interbank Offered Rate. LIBOR soon became the rate paid on Eurodollar deposits.

Specifically, LIBOR now represents the term at which the World’s largest and most financially sound institutions can obtain funding on a short-term basis for a given currency. When computing LIBOR, the credit risk premium plays a fundamental role: if the bank’s default risk surges, so the rate and vice versa. Therefore, it is reasonably believed that a more solid bank will submit a lower rate than a bank considered less stable. But this is not to say LIBOR embeds only this risk. Every interest rate is the sum of different premiums:

- a risk-free premium, that is the time value of money;

- a term premium, it increases with the duration of the maturity of the instrument and represents the premium for the access to a liquid asset at the time of the loan;

- a credit risk premium, a compensation for the risk of default: it depends on this perceived risk of the counterpart and, in secured funding, on the quality of the collateral;

- a funding liquidity premium, related to the demand for funds;

- a market liquidity premium linked to the facility to trade the instrument in the market.

Since 1986, the British Banker Association (the “BBA”) began collecting LIBOR quotes from banks that operated in this market to furnish an average rate. At that time, its fixing was not limited anymore to Eurodollar transactions, but extended to the British pound and the Japanese yen. Until 1998, submitting banks were asked:

“At what rate do you think interbank term deposits will be offered by one prime bank to another prime bank for a reasonable market size today at 11 am?”

Then, the question changed into:

“At what rate could you borrow funds, were you to do so by asking for and then accepting interbank offers in a reasonable market size just prior to 11 am?”

With this variation, the focus of the question passed from an offered rate to a transaction rate. Nevertheless, each determination was hypothetical and subjective: banks were not obliged to tie their measurements to transactions data; therefore, their bids reflected what they could do, not what actually happened. Also, there was no given definition of “reasonable market size”.

Despite the arbitrary nature of the rate, the increasing volumes of transactions and the facility to use it in syndicated loans gave it the status of benchmark/reference rate. Applying a reference rate to financial contracts, and so linking their payoffs, conveys several benefits: contractual standardization limits asymmetric information about the value and thus the transaction costs. For example, it is useful for derivatives trading in the bilateral over-the-counter market. In essence, this market lacks a centralized exchange bearing the counterpart default risk, which has to be supported by the operators. Consequently, to provide the best possible conditions to trade, reference rates are introduced for standardized information, which reduces search costs and improves the matching mechanism. Of course, the larger amount of information tends to reduce profit margins (lowering bid-ask spreads), but the increased volumes of trades overcome this disadvantage. Benchmarks rates, once established, can attract market participants in a real agglomeration effect, a positive cycle moved by the willingness of reaping the information-related benefits of the benchmark. This mechanism leads to economies of scope and scale, which are also reflected in the lower fixed costs associated with contractual protocols, back-office operations, and venues for trading and clearing.

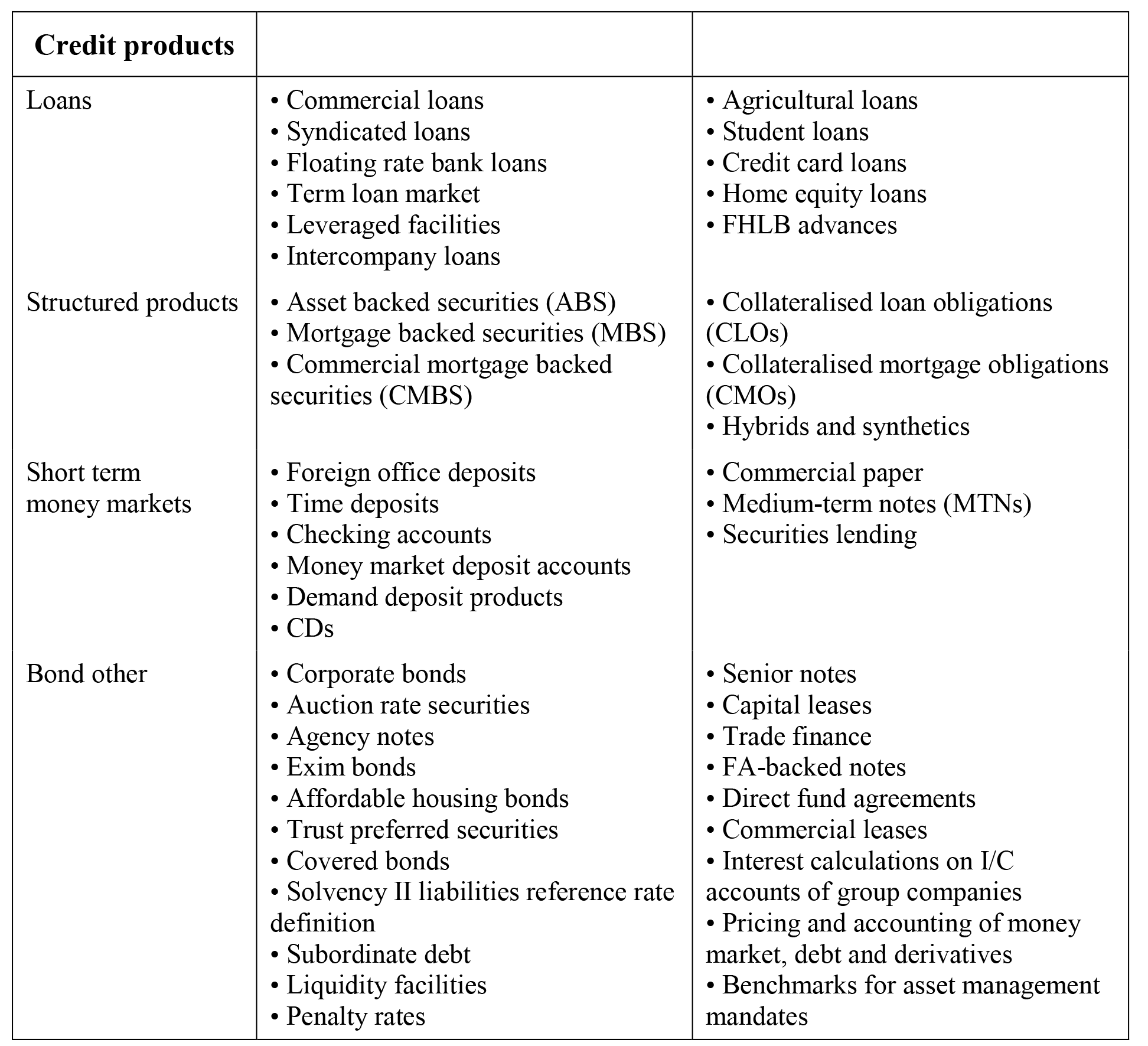

Reference rates are also utilized in risk-management: traders and assets-liabilities managers can isolate rate fluctuations (that are sources of risk), transferring them to the counterpart. In this way, they provide solutions to risk reallocation in the financial system. It derives that the choice of what reference rate to use is determined by what kind of risk we want to avoid and to what extent we need to be hedged. For example, banks use LIBOR because it is based on unsecured funding that comprises both the risk-free rate and the default risk premium, which is the real bank’s funding cost. It is common, when lending for a long-term period at a floating rate, to fund the loan with short term funds borrowed in the unsecured market, which is pegged to LIBOR. Charging the same rate to the long-term loan plus a spread is a simple way to hedge against interest rate risk and make a profit. This mechanism has been extended to several forms of lending: the table below displays the types of credit products nowadays pegged to the rate.

Some operators would instead prefer rates that do no embed the banks’ funding cost: if the issuer is a corporation, its bonds should be linked to its sector’s risk. In the same way, pricing a swap with LIBOR could not be the optimum choice, as a risk-free interest rate should be preferable. Indeed, the application of LIBOR has also been extended to derivatives contracts: the deep liquidity of the underlying market and the yet frequent referencing in other products conveyed derivatives trader the possibility of quickly build hedging strategies, despite the presence of a credit-risk premium. Therefore, it has been adopted in interest rate swaps (IRS), forward rate agreements (FRA), interest-rate options, cross-currency swap and interest-rate futures. Being more and more important, it started being employed to assess the present net value of future cash-flows, a common practice in swap pricing, accounting, calculating counterparty risk or determining collateral amounts.

Credit products referencing interest rate benchmarks. Source: Financial Stability Board

And this is not enough, because financial analysts utilize it in risk management, assets-liabilities management, performance measurements, compensation schemes, credit rating and company accounting practices. These considerations extend to the other IBORs; after LIBOR, new benchmarks with similar characteristics were introduced. If LIBOR is prevalently referred to USD, GBP and CHF products, so EURIBOR and TIBOR are for respectively EUR and JPY contracts.

To give an idea of the extensive usage of LIBOR, in 2012 the Federal Stability Board in Reforming Major Interest Rate calculated a gross notional exposure of roughly $150tn, $30tn, $6.5tn and $30tn of contracts referencing USD, British Pound Sterling, Swiss Franc and Japanese Yen LIBOR respectively. At the end of 2016, the exposure to USD LIBOR increased to around $20tn, whereas U.S. Gross Domestic Product was $18.57tn, more than ten times lower. The table above, extracted from the Second Report of the Alternative Reference Rate Committee, reports the exposure of USD contracts per asset class. It is easy to notice the predominance of derivatives, accounting for 95% of the amount. Among them, overnight index swaps (OIS) are the most referenced ($81tn), followed by interest rate options and forward rate agreements ($34tn each), cross-currency swaps ($18tn), interest rate options ($12tn) and interest rate futures ($11tn).

The effects of the adoption of a financial benchmark are not limited to what we have just seen: indeed, some other relationships have been highlighted in recent times. For example, risks reallocation reduces the banking sector’s costs; thus, it increases the propensity to lend. At the same time, borrowers must bear more risk; therefore, the demand could decrease. If the supply outpaces the demand, the loans’ price (i.e. the rate) lowers: indeed, this could interfere with the monetary policies undertaken by governmental institutions. A similar effect could arise also in other cases. A distortion between monetary policy and reference rates can be entailed by cross-border factors: since a fixed rate reflects the particular market condition at a specific time, it could not be entirely representative of the state of another similar market at a delayed time, thus impairing the effects of the monetary policy actions based on that precise rate. Pegging loans to LIBOR means linking the broader lending market with the one which provides the rate, that is connecting the former’s financing conditions with those of the underlying market. So, the behavior of the latter could interfere with that of the wider one. If a rise in credit premium is determined by a higher perceived risk in the interbank market, the economy will sustain higher funding costs because of a circumscribed phenomenon, which could have no relations with the broader environment. For example, liquidity and credit premiums usually become more volatile during market stress, increasing the riskiness of those products which are linked to them. Also, there could be problems under a financial stability point of view: since a large volume of financial contracts is pegged to reference rates, a loss of confidence about its value could interrupt transactions, impairing liquidity and generating systemic risk. The system could also suffer from mispricing: if the banking sector risk is understated, the contracts referencing it will spread out the misalignment mounting unrecorded financial risk. Moreover, an additional problem occurs when Exchange-Traded derivatives are priced with non-risk-free rates: this kind of contracts trades through a clearing house, that assumes the counterpart credit risk in return for an amount of money (the margin). Therefore, they do not incorporate this premium. Pricing them with rates that, conversely, does it.

The Rigging Scandal

On April 16, 2008, The Wall Street Journal published an article pointing suspicions about possible manipulation of LIBOR: traders and bankers were questioning if banks had underreported the rate submission during the turmoil of the financial crisis. According to the text, the first doubts arose yet in November 2007 during a Bank of England meeting, where some members expressed concerns about the truthfulness of the quotes. The month after, The Wall Street Journal reported the results of an investigation highlighting anomalies in LIBOR’s values. Since January 2008, the rates reported by Citigroup, WestLB, HBOS, J.P. Morgan Chase & Co. and UBS were not anymore aligned with the prices of credit default swaps (CDS) on the same banks. CDS are financial contracts that insure the buyer against the default of a debt-issuer. Thus, their price varies as the probability that an institution will renege on its debt.

As even LIBOR incorporates this risk premium, their values should move mainly in tandem. Effectively, they used to, until the misalignment. The Wall Street Journal analysis was built in this way: they considered each day the lowest LIBOR quote and the risk premium (as measured by the CDS) of the bank submitting it. Then, they computed the risk-free market rate as the difference between these two. Thus, they considered each bank’s CDS rate: the sum of this one and the risk-free rate was considered as a reliable estimate of LIBOR. The submitted quotes and the calculated ones should have coincided, but, indeed, they did not: Citigroup reported rate was 0.87 percentage points lower than the hypothetical rate, 0.43 for J.P. Morgan, 0.57 for HBOS, 0.42 for UBS and 0.7 for WestLB. Besides, according to the same study, other anomalies occurred:

- In the first four months of the year, USD LIBOR average was 3.18%, but all the submissions lingered within a tiny range of 0.06 percentage points, believed too small to be realistic.

- On March 10, 2008, WestLB credit default swaps were trading at nearly two times Credit Suisse Group’s ones, but the following day, WestLB reported the same LIBOR rate as the Swiss bank.

- On April 16, 2008, UBS submitted a 2.73% 3-months LIBOR rate but was offering to pay a 2.85% rate for the same tenor in the commercial-paper market, another form of unsecured debt.

In other words, there were some elements to s

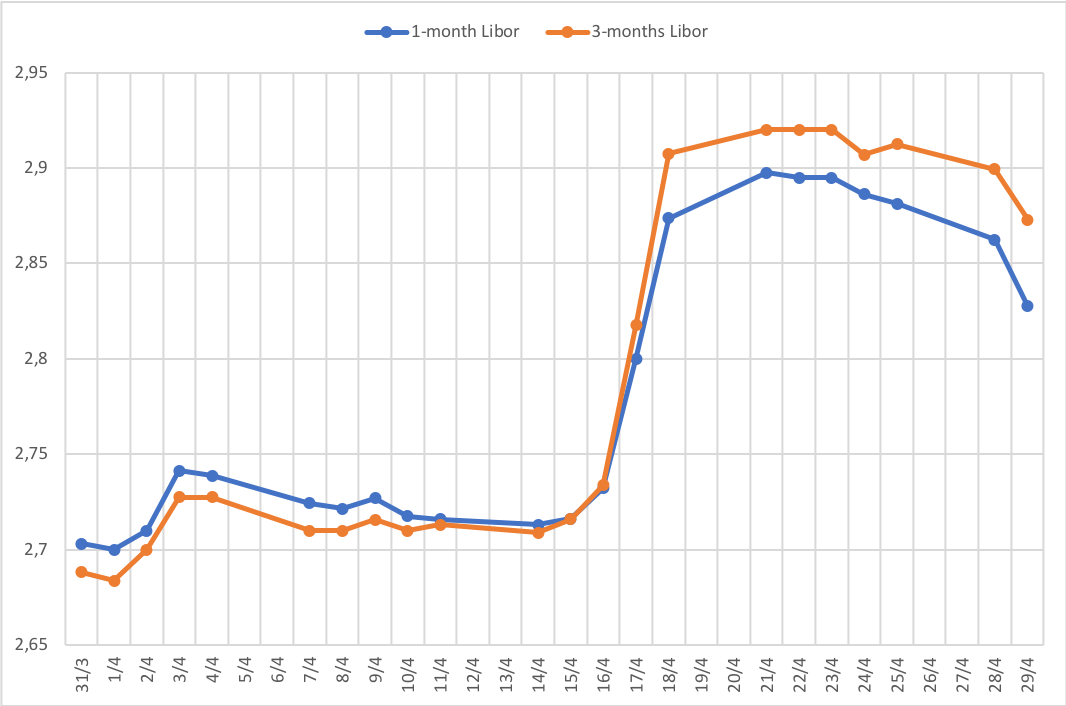

uppose the banks were lowballing their borrowing costs. Indeed, the British Banker Association replied that financial stress made several indicators act differently from the past; therefore, there was no point in believing the default-insurance market-priced bank’s borrowing costs better than LIBOR. However, as we can see from the graph below, on April 17, the day after the first article, LIBOR surged by 837bps, and on April 18 by 900bps, prompting other concerns about possible manipulation.

The April 17 LIBOR spike. Source: Federal Reserve Bank of St. Louis

In the following period, a real scandal mounted: while academics were looking for statistical evidence of misreporting, investment funds claimed to have been cheated on bond returns and several class actions were filed by U.S. municipalities and homeowners. The Wall Street Journal reported the U.S. leaders in mortgage lending Fannie Mae and Freddie Mac could face more than $3bn losses in uncollected payments. Finally, on June 27, 2012, the Commodity Futures Trading Commission, along with the United States Department of Justice and the Financial Services Authority, fined Barclays Bank £59.5bn for breaching the Financial Services Authority’s Principles. Wiretappings proved traders to collude for fixing a lower or higher LIBOR value. Specifically, senior managers were concerned about the bank’s creditworthiness, and they instructed subordinates to low-balling LIBOR and Euribor. Traders then submitted rigged quotes to Thomson Reuters, breaching Principle 5 (The “proper standard of market conduct”). The misconduct was amplified by the internal compliance’s failure to address the issue and by the absence of an adequate risk management system, causing the bank to breach Principles 2 and 3. Later, UBS was fined $1.5bn and Deutsche Bank $2.5bn for the same reasons.

The scandal that mounted after the first allegations of misreporting is strictly linked to the high number of usages and implication which LIBOR has. As a matter of fact, the extensive referencing in derivatives contracts is an incentive to try to manipulate the rate to profit from trading positions: even less than a basis point adjustment can have a massive impact on its exposures. Additionally, the market stress that occurred after the collapse of Lehman Brothers posed serious difficulties to banks looking for funding, and this was another incentive to belie: a lower rate would have improved the bank’s reputation and lowered its borrowing costs. It is essential to notice that banks could benefit from different sources of information that help to measure the risks and benefits of misreporting accurately: firstly, they knew the real rate at which interbank lending occurs. This rate, at the time, was not necessarily revealed to the public. Secondly, they know their real LIBOR exposure and the payoff given by eventual manipulation.

Since then, a process of revision has started, and institutions have collaborated on a dual task: on the one hand, to make LIBOR more resilient to attempts of manipulation, on the other, to look for alternative reference rates.

0 Comments