US

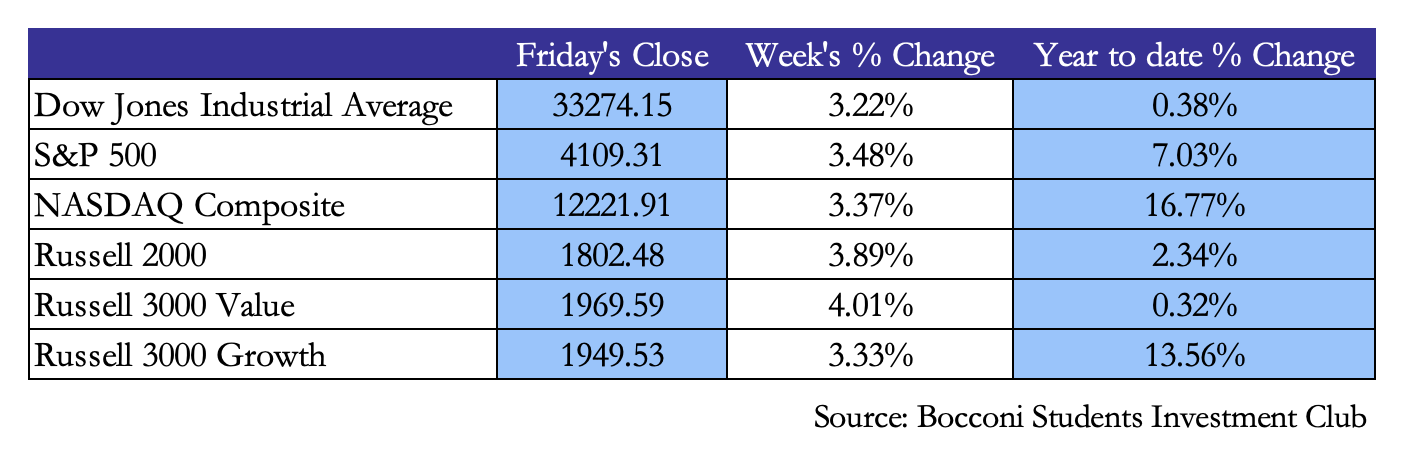

The US stock market closed a very positive week with all the main indices gaining more than 3% from last Friday, bringing all indices positive YTD, with the Dow Jones and the Russel 3000 Value just entering positive territory for the year. The S&P and Nasdaq concluded their third consecutive positive week as traders regained their risk appetite as worries about the banking sector eased, inflation cooled and hope to be close to the end of the Fed’s tightening raised.

The Nasdaq reached its best quarterly gain since the rally of 2020, posting a 16.77% gain YTD with a WoW increase of 3.37%. The rebound in March was strong after a very positive January and negative February and characterized by a “tug of war” with the financial sector, as tech stocks have been the biggest beneficiary of the regulators’ support shown to the financial sector following SVB’s collapse.

The week opened on Monday with strong numbers coming from the banking sector with the KBW Nasdaq bank index up 2.5%, with JP Morgan Chase up 2.9%, Citigroup 3.9% and Wells Fargo 3.4%. The rise in banks’ shares came as regulators confirmed that First Citizens were to take over SVB, a deal that made First Citizens rise 53.7% as the bank has a strong track record of takeovers after the 2008 GFC. President Biden called for tougher supervision on large regional banks on Thursday.

Tech stocks lost some ground on Monday and Tuesday as yields rose and the banking sector worries were calmed by the regulatory stance, with the Nasdaq losing 0.5% on Tuesday, but bounced back strongly on Wednesday with a 1.8% gain.

Fed’s Susan Collins stated that she anticipates one more 25 bps as the Fed still has some road to go to go back to the target of 2% inflation. Markets however are currently pricing in a probability of 5 1.6% that the Fed will keep the target rate in the current range of 475-500 bps in the next meeting on May 3rd and 48.4% that there will be another 25bps raise.

Economic data released on Friday showed a slowing Personal Consumption Expenditure index at YoY growth of 4.6%, below expectations of 5.1%, this fuelled the desire for confirmation that we are close to the end of the tightening cycle, with the S&P and Nasdaq adding 1.4% and 1.7% respectively on Friday.

It remains to be seen whether such a strong market sentiment will remain with next week’s employment report on Friday, which might reignite fears of further hikes should it come out stronger than expected, with consensus at 240K for Non-Farm-Payrolls versus last month’s 311K.

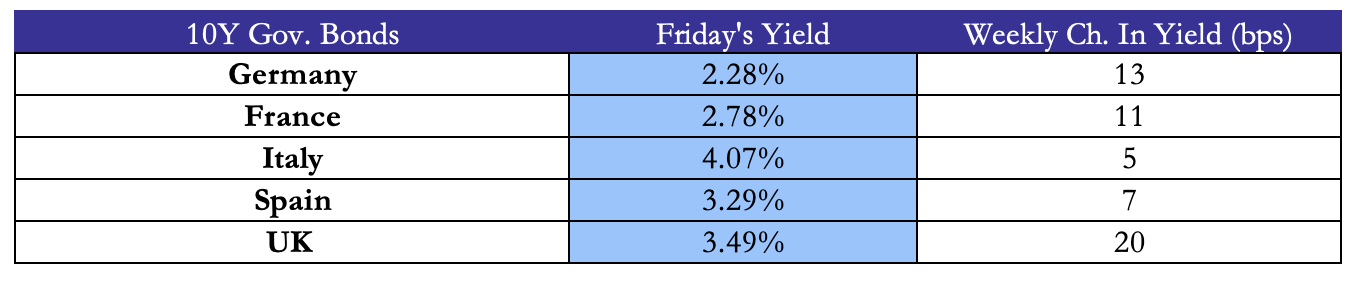

Yields rose for the first time after three consecutive weeks of yields declines.

EU

European markets closed a very positive week with the main indices posting gains well above 4% in Germany, France, and Italy, with the UK’s FTSE 100 adding 3.05%. The European STOXX 600 closed the week up 4.03%, gaining 7.75% YTD.

This performance follows European inflation falling more than expected, with European Consumer Prices cooling down to 6.9% in March after February’s 8.5% read. Economists’ consensus was 7.1%. Despite these positive numbers, analysts do not see the ECB stopping its hikes, forecasting another 25 bps raise in May.

The week opened also in Europe with banks bouncing back from the heavy losses incurred in the last trading sessions, as the STOXX 600 banks index closed 1.1% higher on Monday. Deutsche Bank in particular regained 6.2% following Friday’s beatdown as its CDS reached 200 bps to then ease to 180 bps on Monday. As the European banking sectors booked further gains for 0.7% on Tuesday, Deutsche fell 1.3% after Monday’s strong rally.

On Wednesday UBS’ shares were up 3.7% following the company’s announcement that they would bring back Sergio Ermotti as CEO to manage the Credit Suisse takeover, he further assured investors stating that size will not be an issue for the newly formed banking giant. Shares were up another 4.05% on Friday.

The FTSE 100 closed Wednesday up 1% after UK mortgage approvals raised to 43500 in February from 39600 in January.

On Thursday German inflation came out hotter than anticipated by economists, reading a slowdown to 7.8% in March from 9.3% in February versus an expectation of 7.5%. Spain’s inflation slowed down to 3.1% compared to an expectation of 4%. These mixed numbers will cause dilemmas for the ECB for future hikes, with markets still heavily pointing towards a 25-bps hike.

A huge winner for the week was Petrofac (PFC.L), which closed the week up more than 50% following an announcement on Thursday that the energy company won a huge contract with Hitachi from TenneT.

Rest of the World

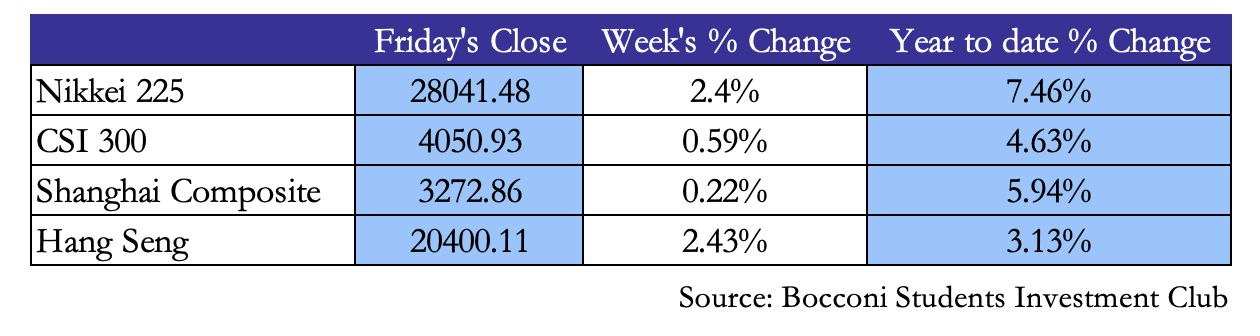

Asian markets were up this week, showing potential signs of recovery from the banking fallout of the past weeks. With the South Korean Kospi (+2.56%), the BSE sensex (+2.55%), the Hang Seng (+2.43%) and the Nikkei 225 (+2.4%) leading the pack out of the major Asian exchanges.

In China the manufacturing Purchasing Manager’s Index came out at 51.9, slightly beating expectations but still representing a slowdown compared last month. Non-manufacturing PMI experienced the highest growth in a decade as economic development in the battered service sector picks up after the reopening of the country, clocking in at 58.2 against 55 expected.

Moreover, on Tuesday, Alibaba announced its biggest restructuring in its 24-year history, as CEO Daniel Zhang spoke of spinning off the company into 6 different units covering e-commerce, media and the cloud, adding that each will explore fundraising or IPOs.

This news, together with rival JD.com announcing plans to spin off its industrial and property unit and listing them on the Hong Kong exchange, has investors hopeful that the tech crackdown enacted by the Chinese government could be coming an end. Wang Qi, co-founder of boutique fund MegaTrust Investment (HK), added that “the new structure may help Alibaba deflect some of the regulatory pressure such as that related to anti-monopoly”.

BABA closed off the week at +17.58% and JD at +8.94%.

Again, on Tuesday, the data regarding Japanese Core CPI in February (the preferred inflation gauge of the BoJ) came out at 2.7%, down from 3.1% in January and below the estimate of 3.5%. The Central Bank has been reluctant to tighten policy and has insisted that high inflation is transient and will fall to 2% later this year as the effect of high commodity prices eases.

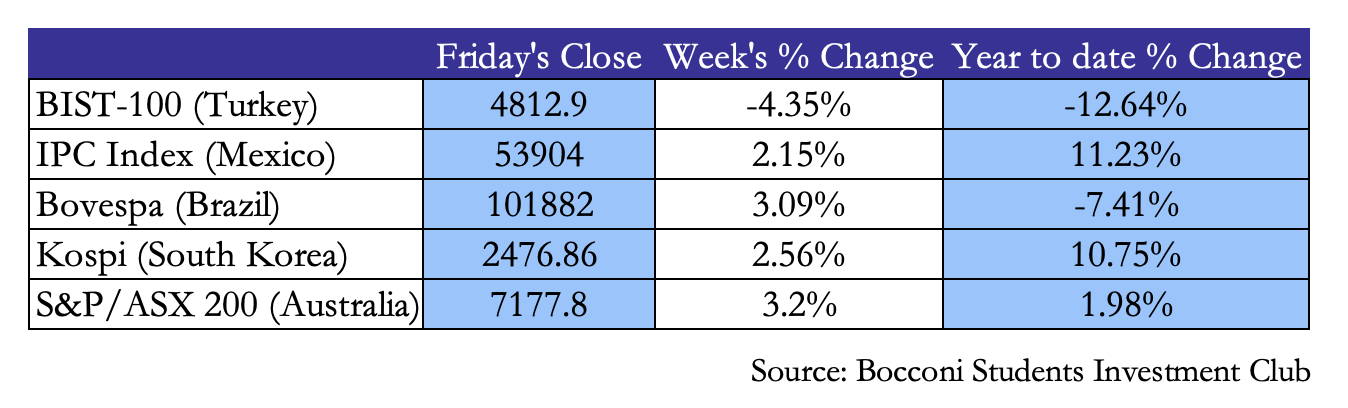

Both the Australian and Canadian markets rebounded back from the disappointing last weeks with respective returns of +3.2% and +3.07%.

Regarding the emerging markets, Mexico’s IPC index continued the last week’s positive streak with a gain of +2.15%, Brazil also bounced back from last week with a gain of +3.09%. Turkey’s equity index, the BIST 100, contracted by 4.35%.

FX & Commodities

As markets now anticipate rate cuts by the end of the year, the dollar index devalued by 0.6% WoW, as it recovered from early week losses. Indeed, with the strong performances of US equity indexes from mid-week onwards, the dollar index climbed 0.4% from its lowest point to closing on Friday.

EUR was trading higher than USD for most of the week as it gained 1.7% on Thursday before finishing 1.2% WoW on Friday. This is due to multiple reasons, but the main ones are: a) on Monday German IFO business climate index beat estimates, propelling EUR higher while b) both a weak US CB Consumer confidence and higher than expected US unemployment weekly claims weakened the USD. Hoewer, the trend reversed on Friday with a strong equity market in the US and lower than expected EU CPI flash estimate y/y.

The earlier than expected economic rebound pushed WTI May futures higher during the week as it closed on Friday with an 8.1% weekly increase, while the Brent Crude May futures topped a 6.4% weekly change. Spot gold price increased 0.5% WoW.

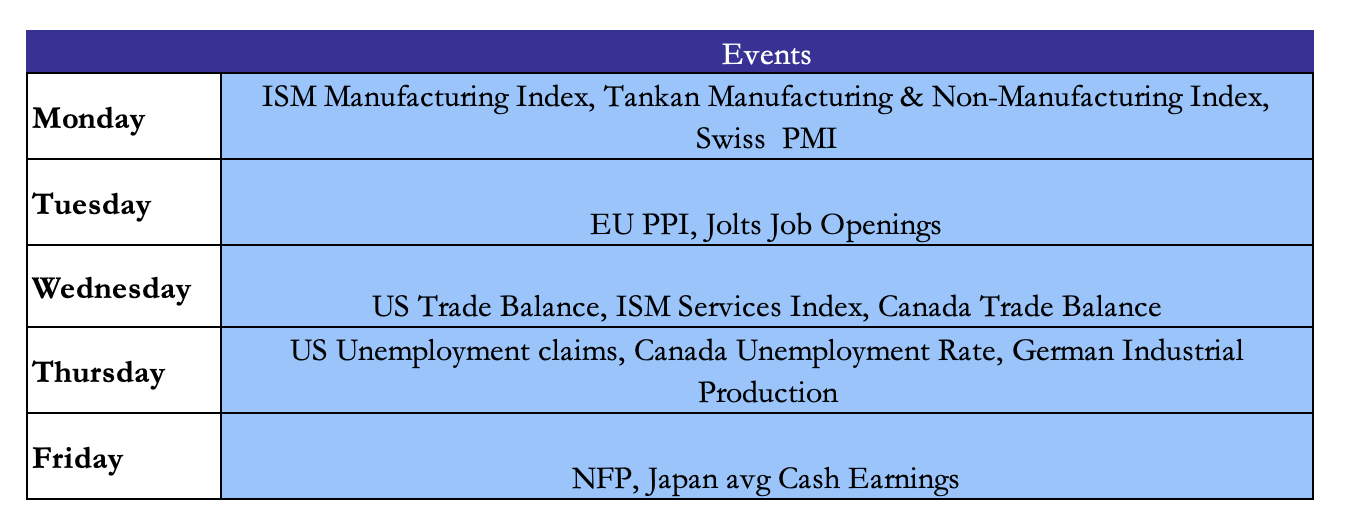

Next Week’s Events

Brainteaser #38

Nine mathematicians meet at an international conference and discover that among any three of them, at least two speak a common language. If each of the mathematicians speak at most three languages, prove that there are at least three of the mathematicians who can speak the same language.

Source: USAMO 1978

Solution: suppose no three mathematicians speak the same language. Then person A can share some language with at most 3 other delegates, because if he shared some language with 4 delegates there would be 3 with the same language. So there are 5 delegates who do not share a language with A. Let one of them be B. Using the same logic, one the remaining 4, let it be C, does not share a language with B. Now A, B, C do not have any common languages.

Brainteaser #39

On a given circle, six points A, B, C, D, E, and F are chosen at random, independently, and uniformly with respect to arc length. Determine the probability that the two triangles ABC and DEF have no common points.

Source: 1983 USAMO – Problem 1

0 Comments