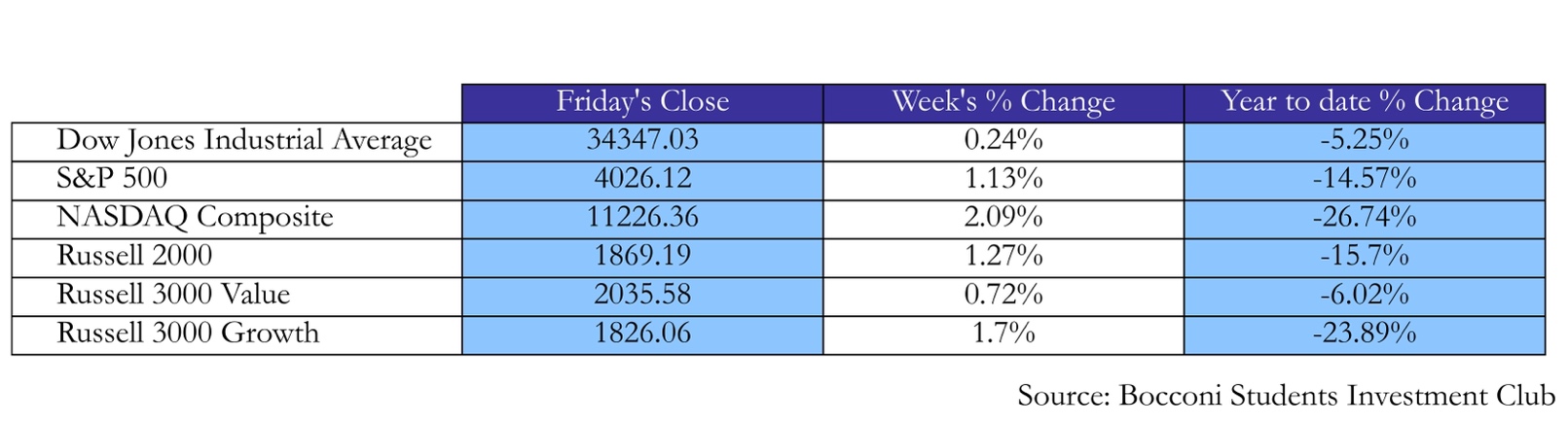

US

The week started off with a substantial drop in the DOW Jones Index during the last hour of trading on Monday amid worries around commentary by Fed officials and reports of protests spreading in China. These worries were the main drivers of Tuesday’s markets as well with the S&P slipping 0.2%, the Nasdaq composite losing 0.6%, and the Dow gaining 0.01%. There was additional uncertainty around Fed Chairman Powell’s speech at the Brookings Institution, the last major one before the December 13th – 14th policy meeting. The 10-year Treasury yield increased by 0.05% from Monday to 3.75%, whilst the two-year was at 4.47%.

On Wednesday Powell signaled that a half percentage hike in December was likely and implying a slowdown in the pace of tightening, this resulted in the Dow Jones Industrial Average rallying by 700 points, and the S&P 500 and Nasdaq Composite recorded increases by 3.1% and 4.4%. This means that November ended with the three indices having a second consecutive month of gains. On Thursday, the markets experienced less volatility after Wednesday’s rally, and the ten-year Treasury fell to 3.53%.

Friday’s trading activity was initially heavily impacted by the non-farm payrolls release with 263,000 jobs being added which was significantly higher than the consensus on Wall Street of around 200,000. The hourly earnings increased by 0.6% for the month, and the labor force participation rate decreased to 62.1%, meaning that the wage pressures are remaining high and might do so for a longer time as there will be higher competition for workers. After the release of the report, traders expect a 4.95% federal funds rate in June up from 4.84% prior to it, and the odds of another 0.75 percentage-point rate increase rose by 7% to 30%. US markets then traded higher during the session and closed slightly up with a plus of 0.1% for Dow Jones Industrial Average, down 0.12% for the S&P 500, and down 0.18% for the Nasdaq Composite. The best-performing sectors during this week were healthcare, communication services, and consumer discretionary with respective changes since Monday of 2.32%, 2.52%, and 2.35%.

EU

European stocks closed higher with Stoxx 600 up 0.63%, DAX up 0.29%, and CAC 40 closing with a 1.04% gain, on Wednesday after the ease in inflation in Europe. Other stock markets in Europe such as Austria’s, Netherlands’ and Portugal’s ended higher, with Spain remaining flat.

Eurozone inflation was at 10% YoY, 0.4 percentage points below expectations, and after a print of 10.6% in October. Core inflation in the eurozone remained steady alongside expectations, and the harmonized index for consumer prices decreased by 0.1%. This slight easing in inflation simultaneously occurred in the major economies in the eurozone except for France, in which the inflation rate remained at 7.1%. Germany’s inflation came out at 11.3% down 0.3%, Italy’s at 12.5% down 0.1%, and Spain’s at 6.6% down from 7.3% in October. Germany’s unemployment rate was at a seasonally adjusted 3%.

On Wednesday, the European Commission decided to stick to its proposal from September to stop the payment of €7.5bn to Hungary in the 2020-2027 time period following Hungary’s lacking reforms in light of the “rule of law” dispute. The EU council can vote on this matter until December 19th.

On Friday, the EU member states reached an agreement for the implementation of a $60 cap on purchases of Russian oil, after Poland had initially delayed it after demanding a lower level. This cap will be adopted by G7 countries and will impact Russian oil exporters who would then require tankers without Western insurance. The level of the price cap is therefore lower than the $70 initially proposed by the European Commission. 10-year bond yields in Europe closed this week at 1.82% for Germany, 2.27% for France, 2.81% for Spain, and 3.69% for Italy, with the BTP-Bund spread at 191bps. 2-year government bonds in the eurozone also closed higher.

UK

UK stocks ended the session on Friday down 0.03% for the FTSE 100, after the US nonfarm payrolls report. In the UK, high street sales of the Black Friday week were published which showed a 4.26% increase to the week before compared to the equivalent week last year which saw a sales increase of 38.98%. On Tuesday, the Bank of England discussed UK mortgage data. Approvals have dropped more than expected to 59,000 in October compared to the estimated 66,000. Another housing market data point, the mortgage lender nationwide’s monthly survey got released in November. It showed a house price drop of 1.4%, the annual house price growth cooled down from 7.2% to 4.4%.

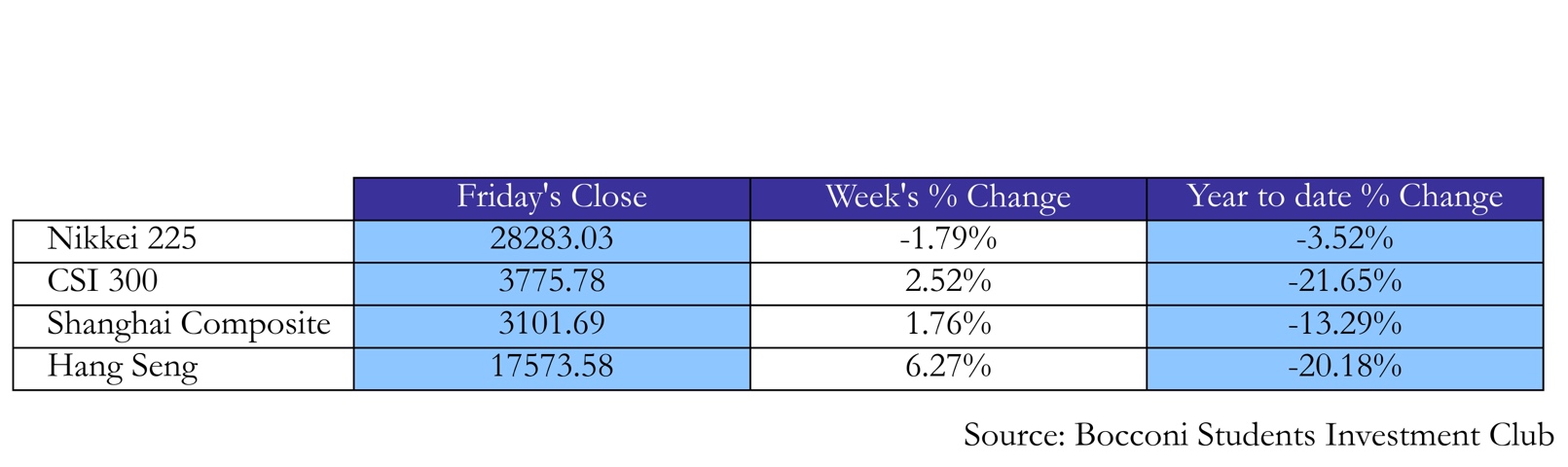

Rest of the world

On Monday, as signs of unrest against the zero-Covid policies appeared in China, Hong Kong’s Hang Seng and China’s CSI 300 dropped 4.2% and 2.5% in early trading, respectively. On Tuesday, most major benchmarks in Asia rose: the Shanghai Composite Index by 2.3% and Hong Kong’s Hang Seng by 5.2%. Cities in China such as Guangzhou have moved slightly away from the strict zero-Covid policy, resulting in increased expectations for economic growth. The Hang Seng Index ended November with its strongest rally since the dot-com bubble with a gain of almost 27%. The CSI 300 index reported a 9.8% increase for November.

On Tuesday, Japan’s unemployment rate was released, coming in at 2.6%, which was higher than the expected 2.5%, albeit unchanged from October. On Friday, Japan’s Topix lost 2.1% as the yen is in a five-day rally, due to expectations of possible slower Fed interest rate increases that would reduce the interest rate differential. Japan’s Industrial Production reported a 2.6% fall month-on-month for October, which fell short of expectations. Production is expected to increase in November and December. The Nikkei 225 closed down 1.59% on Friday.

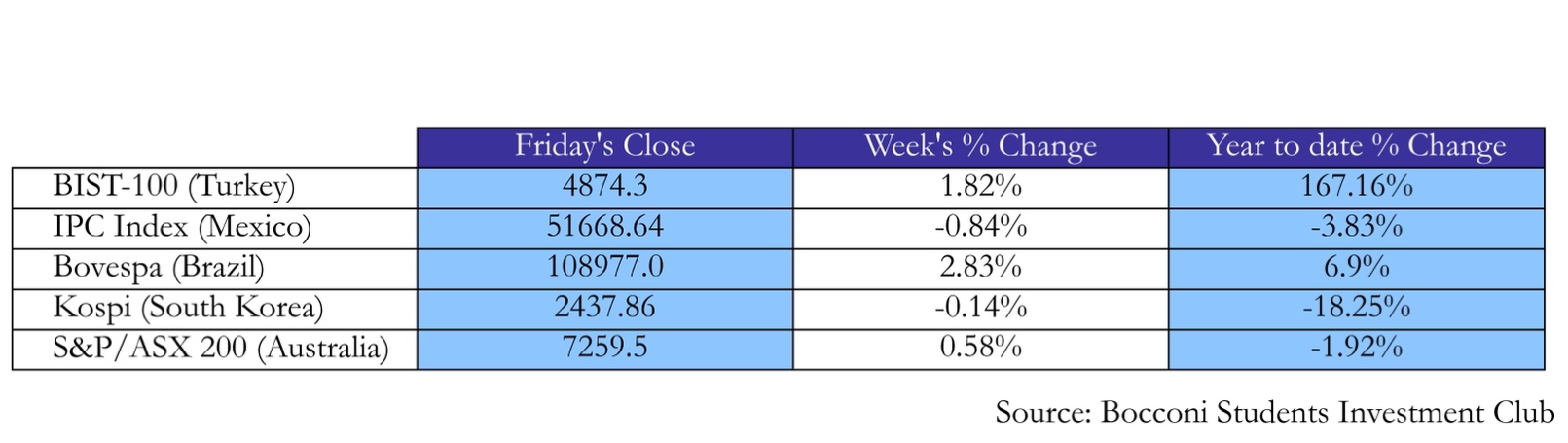

In Turkey, the BIST-100 Index returns were 1.82% this week. During the month of November, Turkish stocks rallied 22.54% in U.S. dollar terms. This rally was caused by Turkey’s central bank’s decision to further cut interest rates on November 24th despite reporting a year-on-year inflation rate of 84.65% in November which exceeded the 83.7% expected. Turkey has witnessed the slowest rate of growth in GDP since 2020, exports rose by 3% last month while imports increased by 31% due to the devaluation of the Lira.

Russia’s S&P Global Manufacturing PMI for November rose to 53.2 compared to 50.7 a month prior and higher than the expectations of 50.3. Wednesday’s release of Russia’s unemployment rate for October remained unchanged at 3.9%.

In Canada, the labor market experienced growth of 10,000 jobs in the month of November in line with expectations, a significant decrease from October’s 108,000 number. The employment rate among women between 25 and 54 years reached its peak with 81.6% since the start of the data collection. Next week’s interest rate decision by the Bank of Canada is expected to be a 25-basis point increase in the key lending rate.

FX and Commodities

In the foreign exchange markets, the US Dollar fell across the board due to the higher likelihood of lower interest rate differentials. EURUSD closed on Friday with an increase of 1.42% at 1.05, GBPUSD rose 1.73% to 1.23, while USDJPY, USDCNY, USDCAD, and USDCHF fell respectively. The DXY Index ended November with the worst month in years. On Friday, Latin American currencies dipped after the strong jobs report. MXN decreased 1.5% against the dollar, due to the EU’s Russian crude ban and ahead of the OPEC+ meeting on December 4th. PEN fell 0.2% after the Peruvian congress approved the impeachment proceedings against its President. After South Africa’s President Cyril Ramaphosa’s presidency came under question on Thursday, South Africa’s Rand bounced back on Friday.

For commodities, WTI crude futures were trading at $80 on Friday ahead of the OPEC+ meeting. OPEC+ is expected to stick to its last production target. Oil surged 5% this week due to China’s relative loosening on its zero Covid policies. US natural gas futures fell 5% this week due to a later restart of Freeport’s LNG export plant, increasing supply domestically. The average gas output for the contiguous United States increased to 99.5bcfd in November compared to 99.4bcfd in October. Chicago wheat futures were down at $7.4 at the start of December due to strong supply, especially by Russia. Gold futures showed their largest gain on a single day since April 2020 after a 3% rise on Thursday.

Next Week’s Main Events

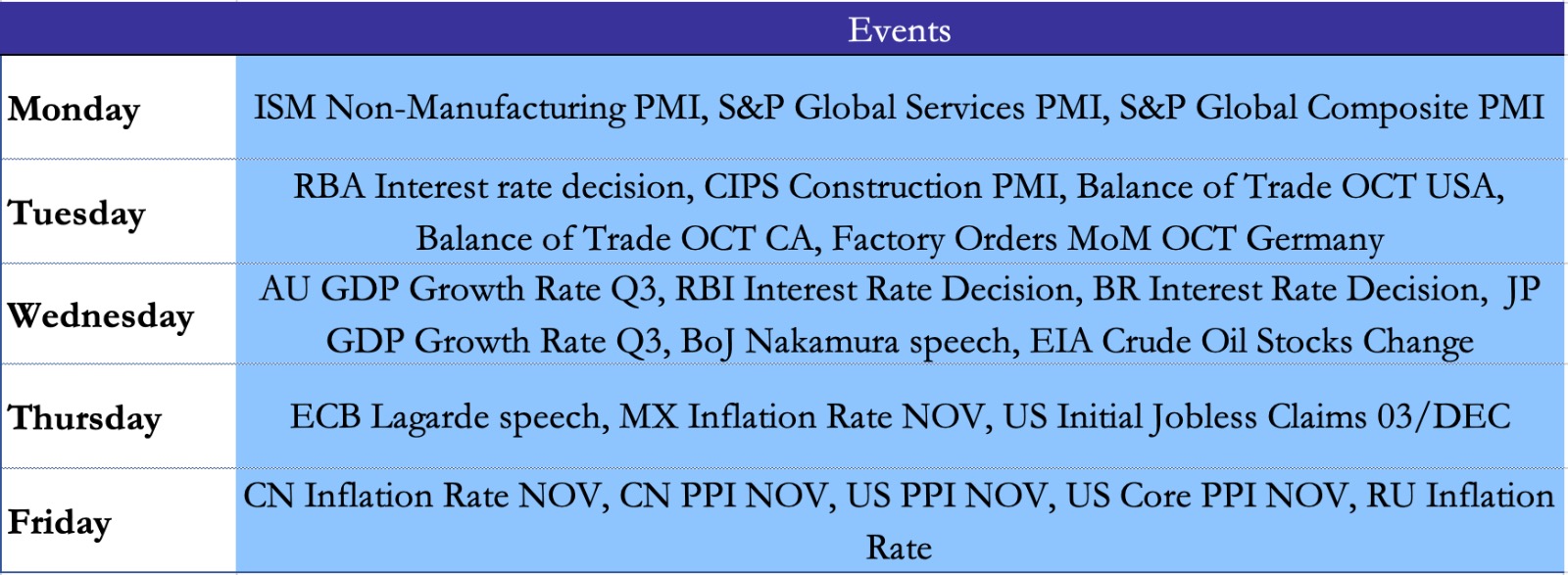

Next week’s main events will include the ECB President Lagarde speech, UK Composite PMI, the ISM Non-Manufacturing PMI, RBA Interest Rate Decision, Germany Services PMI, UK Construction PMI, China Trade Balance, India Interest Rate Decision, the BoC Interest Rate decision, US Crude Oil Inventories, Japan GDP Q3, US Initial Jobless Claims, US PPI. The expectations for US PPI are 0.2% month on month. Japanese GDP Q3 is expected to be -0.3% QoQ.

Brain Teaser #33

A palindrome is a word that doesn’t matter if you read it from left to right or from right to left. Examples: OMO, lepel and parterretrap.

How many palindromes can you make with the five letters  and

and  under the conditions:

under the conditions:

– each letter may appear no more than twice in each palindrome,

– the length of each palindrome is at least 3 letters.

(Any possible combination of letters is considered a word.)

Source: Dutch Mathematical Olympiad 2006

Solution: For solving this problem, we will differentiate between two cases.

- The number of letters in the palindrome is even.

Considering that, we can have 5, 4, 3, or 2 letters in the first half of the word, producing palindromes that are 10, 8, 6, or 4 letters long, respectively. As the order in which we arrange the letters matters, we will have  possible arrangements for the first part of the 10-letter palindrome,

possible arrangements for the first part of the 10-letter palindrome,  arrangements for the 8-letter one, 60 – for the 6-letter one, and 20 – for the 4-letter one. In total, there will be 320 possible palindromes.

arrangements for the 8-letter one, 60 – for the 6-letter one, and 20 – for the 4-letter one. In total, there will be 320 possible palindromes.

- The number of letters in the palindrome is odd.

Because each letter may appear no more than twice, we cannot build an 11-letter palindrome. Instead, we can construct palindromes from 9,7, 5, and 3 letters. This time, we will select the central letter in one of the five available ways. By applying the same reasoning as in the first case, we can find 320 methods to create palindromes of odd sizes.

Summing up the answers from the two cases, we get 640 possible palindromes.

Brain Teaser #34

Let  be the probability that, in the process of repeatedly flipping a fair coin, one will encounter a run of 5 heads before one encounters a run of 2 tails. Given that can be written in the form

be the probability that, in the process of repeatedly flipping a fair coin, one will encounter a run of 5 heads before one encounters a run of 2 tails. Given that can be written in the form  where

where  and

and  are relatively prime positive integers, find

are relatively prime positive integers, find

0 Comments