US

US equities continued to trade sideways in the last week due to the lack of news catalysts. The only major pieces of news out were the number of initial and continuing jobless claims diffused on Thursday and the retail sales figures released on Friday. The anticipation of the former two had pushed the S&P 500 at an intraday all-time high above 2,045, while the real figures later prompted a mild retracement, being solid but slightly worse than last month. However, positive data on retail sales on Friday allowed the index to close 0.33% higher than last week, at a record value of 2038.56. The DJIA gained instead 0.35% to close at 17,635, while the Nasdaq Composite rose by 1.21% to close at 4,688. Both indices are also extremely close to their historical and post-crisis highs respectively.

Not much action was seen in the bond market either; US treasuries yield nearly as much as last week, save for a slight differential of plus two basis points along the 2-to-10-year maturities. The latter yields now 2.33% instead of 2.31% last week.

In the currencies market the US dollar continued its trend of appreciation vis-à-vis the British pound and the Japanese yen; the greenback gained 1.32% and 1.46% respectively with respect to the two. However, the euro pared some of the recent losses to end the week 0.56% higher in dollar terms.

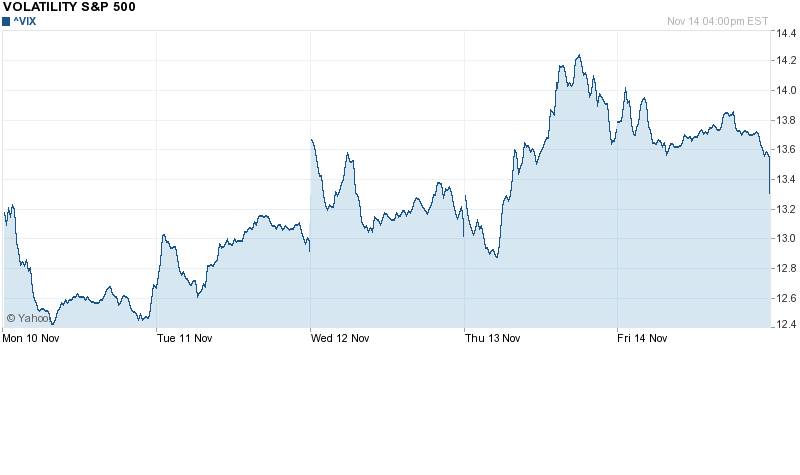

Next week will be much heavier in terms of economic news, as data on industrial production and producers prices are expected at the start of the week, while later will come the FOMC minutes of the October meeting and the data on inflation for October. We do not expect inflation surprises to the upside, but rather moderate figures around last month’s 1.7% number that would be supportive of the current levels of government bonds. Also, the VIX index was slightly on the rise last week, as shown in the chart below. It traded around 12.5 on Monday while it closed at 13.54 on Friday, but it is still way below mid-October levels. Since the index is related to implied volatility on 30-day-maturity options on the S&P 500, last week’s gains are not expected to be erased just yet.

Source: Yahoo Finance

UK

We outlined the current UK market environment in a comprehensive article.

Eurozone

The beginning of the week has seen a general rise in the main stocks indices of the Eurozone on rising confidence by the investors that a European QE is coming thanks to Draghi’s speech regarding the €3 trillion target of ECB’s balance sheet. However, BOE’s speech on Wednesday regarding its concerns about Eurozone’s economic situation that could slowdown UK’s one slowed markets’ hope. Moreover, the indices got drag down by the banks sector’ quarter results where top line operative growth missed the expectations, although showing strong financial solidity: especially in the peripheral countries, this has been interpreted as an implicit lack of confidence in the economy by both loans demand side (businesses) and offer side (banks). IBEX 35 lost -1.76% and FTSEMIB -2.87%, while Eurostoxx 50 -1.85% on that day. Approaching the end of the week, German’s Q3 GDP growth came out in line with the consensus expectations at +0.1% and later Eurozone’s GDP beat the estimates at +0.2% (QoQ) vs +0.1% while CPI was in line at +0.4% (YoY). GDP figures were out for EU countries, and surprisingly the top performer for the quarter was Greece, growing at 0.7% QoQ. Italy has instead come back to recession growing -0.1% QoQ in the quarter: only Cyprus grew performed worse than Italy (-0.4% QoQ).

In the late afternoon of Friday, indices bounced up thanks to the good economic indicators coming from USA.

On the FX side, EUR/USD closed the week slightly edging up to 1.2527.

Japan

This week many interesting topics dominated Japanese Markets.

Since Sunday, speculation has been mounting that Shinzo Abe, prime minister, is planning to call for general election right in the middle of its 4-year mandate. A successful campaign, in fact, would reset the clock on Japan’s election cycle, while improving Mr Abe’s chances of retaining leadership of its party at internal elections coming next September. Markets reacted quite calmly to this news, as they would welcome very well 2 extra years of Abenomics.

The general election suggests that Abe is seeking a popular mandate to delay the second increase in the consumption taxes scheduled for next October. The first one, effective in April, is blamed to be the main causes of the sharp fall in the Japanese GDP, that rely for 60% on household consumption, and of the loss of momentum in the Central Bank’s fight against deflation, that over this period slowed from 1.9% to 1.2%. The preliminary figures for GDP in the third quarter coming out on Monday will give further evidence of the effect of this policy on the economy.

If Markets are worried that consumption taxes will reduce consumption and hurt corporate revenues, this week were supported by the action of the Central Bank, that is proving successful in weakening the Yen, that this week touched 116 against the dollar. In fact they were positive throghout the week and the Nikkei 225, the main equity index, was up 2.7% to 17490.

[edmc id=2102]Download as PDF[/edmc]

0 Comments