USA

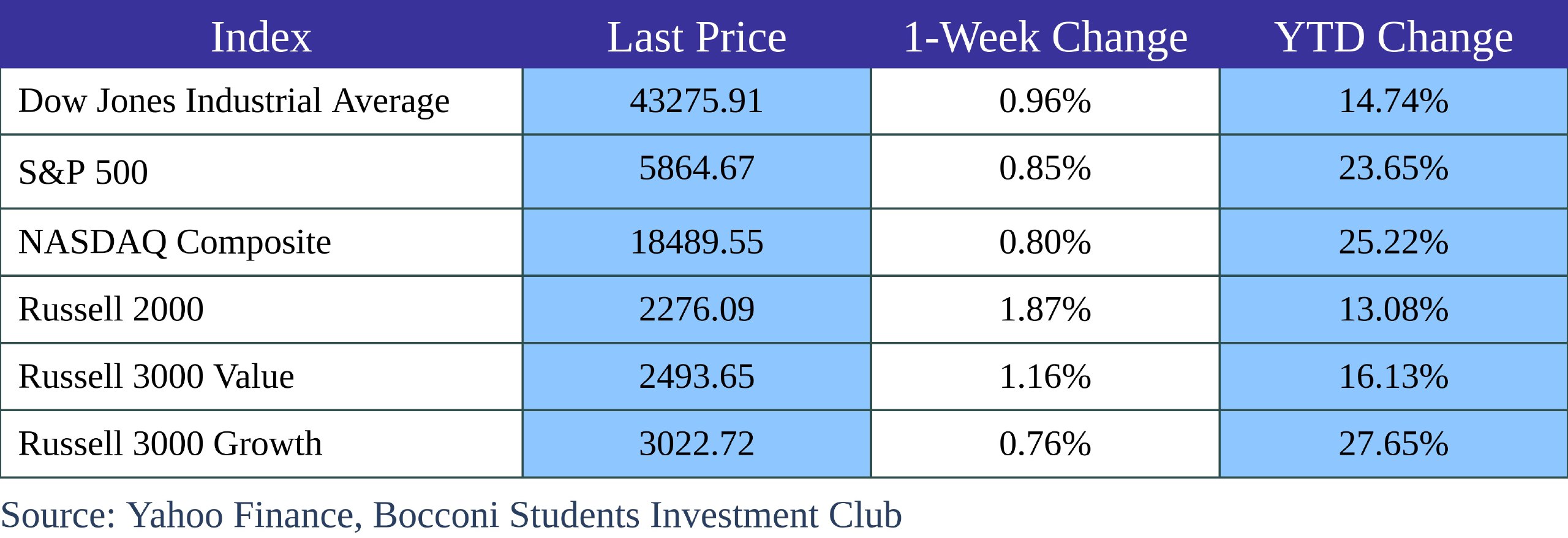

The S&P 500 Index advanced this week, driven by gains in the utilities and real estate sectors. Energy stocks, however, faced losses in tandem with a decline in oil prices, as concerns over potential Israeli strikes on Iran’s oil and gas infrastructure began to subside. In terms of performance, small-cap stocks outpaced large-caps, with the Russell 2000 Index and the S&P MidCap 400 Index outperforming the broader market.

The Nasdaq Composite lagged for much of the week but saw a strong rally on Friday, fueled by robust quarterly earnings from Taiwan Semiconductor Manufacturing. The company’s results revived investor enthusiasm for AI-related stocks, which dominate the Nasdaq. Netflix also boosted the index, reporting third-quarter earnings that surpassed analysts’ expectations in all major metrics, driving its share price up nearly 5%.

Morgan Stanley delivered a standout third-quarter performance in investment banking, exceeding analyst expectations and driving its stock to an all-time high. This strong showing aligns with the broader success seen across Wall Street banks, fueled by a resurgence in corporate debt issuance, IPOs, and mergers. Blackstone also surpassed forecasts, reporting record assets under management of $1.1tn. The firm enjoyed a robust quarter, drawing in $41bn in new capital and deploying $54bn, the highest level of investment activity in over two years. This surge in dealmaking has been underpinned by favorable economic conditions and recent U.S. Federal Reserve rate cuts, creating an optimistic backdrop for investors.

Following their strong Q3 earnings, these financial institutions are leveraging robust investor demand and favorable credit market conditions. JPMorgan issued $8bn in bonds, with investor interest soaring as orders hit $34bn. Goldman Sachs, after reporting a 45% rise in quarterly profits, tapped the market with a $5.5bn bond sale. Similarly, Morgan Stanley raised $5.75bn in bonds, driven by a 32% profit increase and strong trading results. By tapping the bond market, these banks are securing low-cost capital to fuel future growth, strengthen their financial positions, and invest in new ventures, reflecting the strong demand and tight credit spreads currently characterizing the market.

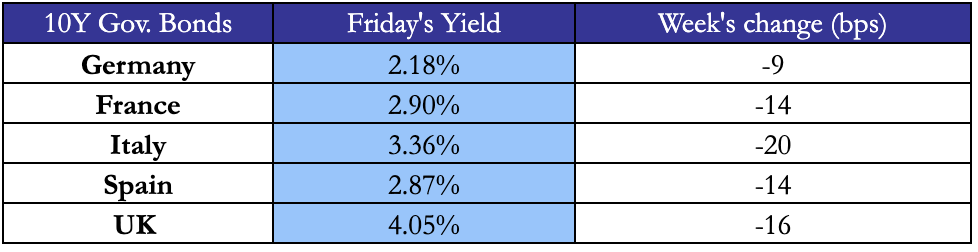

In the bond market, U.S. Treasury yields showed modest fluctuations. After yields on intermediate- and long-term bonds climbed on Thursday, they dipped again following weaker housing data. September saw declines in both housing starts and building permits, signaling a slowdown in construction. Bond prices, which move inversely to yields, rose marginally by the end of the week. The bank loan market was active, reporting a high level of issuance early in the week, primarily for repricing announcements. Investors showed strong demand for discounted, higher-yielding bonds.

From an economic perspective, retail sales in September provided a positive surprise, increasing by 0.4% after a modest 0.1% gain in August. However, industrial production declined by 0.3%, erasing gains from the previous month. This drop was partly attributed to disruptions from Hurricanes Francene and Helene, as well as an aircraft machinist strike at Boeing.

In labor market data, initial jobless claims fell unexpectedly to 241,000 for the week ending October 12, a drop of 19,000 filings from the previous week. Continued claims, however, edged higher by 9,000 to 1.867 million, though still below expectations.

Source: Bocconi Students Investment Club, Financial Times

Overall, while market sentiment was mixed early in the week, positive earnings reports, particularly in the tech sector, helped fuel a late-week rally. Economic indicators provided a mixed picture, with retail sales showing strength but industrial production and housing data signaling some weakness.

Europe and UK

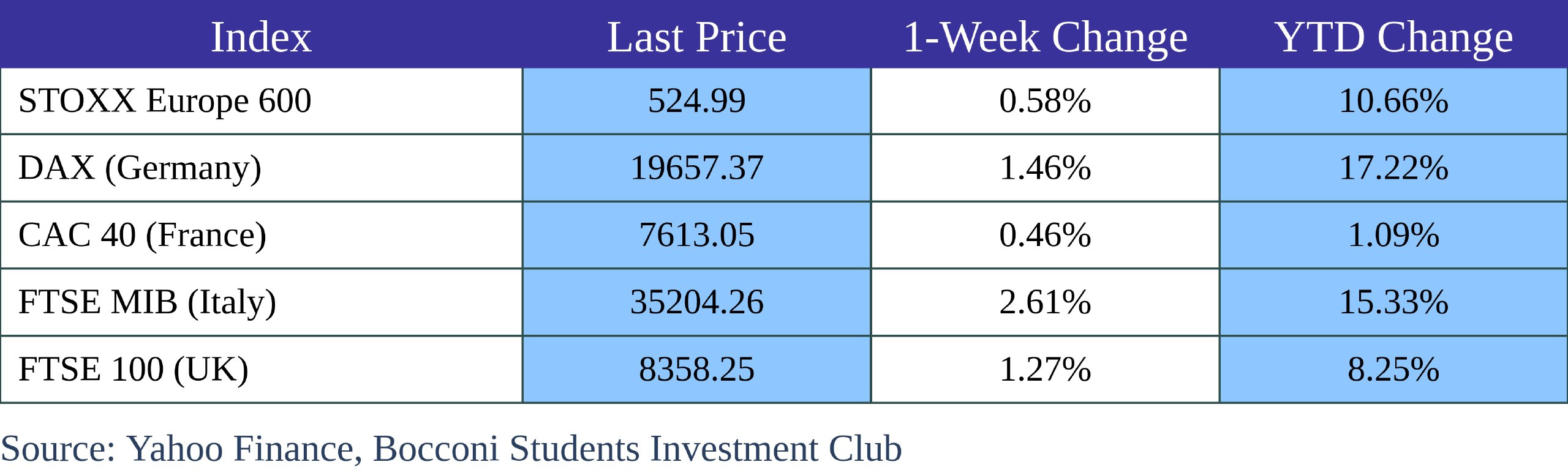

The pan-European STOXX Europe 600 Index ended the week 0.58% higher, lifted by the European Central Bank’s (ECB) second consecutive interest rate cut, which fueled expectations of continued monetary easing. Major European markets showed gains, with Italy’s FTSE MIB rising by 2.61%, Germany’s DAX gaining 1.46%, France’s CAC 40 advancing 0.46%, and the UK’s FTSE 100 increasing by 1.27%.

Tech stocks led the STOXX 600’s performance on Friday, posting a 2% rise, although the sector had experienced a sharp decline earlier in the week. ASML, which accidentally released its Q3 earnings early on October 15, saw its stock drop by 16%. The semiconductor giant posted solid results but reported lower-than-expected net bookings of €2.6 billion and a reduced sales forecast for 2025, which triggered a global sell-off in chip stocks.

Basic resources shares climbed 1.4% as strong copper prices bolstered the sector. Meanwhile, luxury stocks rebounded, with LVMH rising 1.1% after a weak start to the week due to disappointing third-quarter sales. LVMH’s stock fell as much as 7% to a two-year low but recovered slightly by Friday. Other luxury brands, including Kering and Hermes, also helped lift the market, contributing to the 0.4% gain in France’s CAC 40.

As anticipated, the ECB lowered its key deposit rate by 0.25 percentage points to 3.25%, marking the first back-to-back rate cuts in 13 years. ECB President Christine Lagarde noted that the disinflationary trend is progressing as expected, supported by weaker-than-forecast economic activity. While the ECB refrained from committing to a specific rate path, markets are speculating another rate cut in December to bolster the economy.

Eurozone inflation for September was revised to 1.7%, down from the initial 1.8% estimate and well below the ECB’s 2% target. The central bank expects inflation to rise before gradually easing towards its target next year. UK inflation slowed to 1.7% in September, the lowest since April 2021, and below the forecast of 1.9%. Wage growth also cooled, with regular pay (excluding bonuses) rising 4.9% in the three months to August, down from 5.1%, hinting at easing inflationary pressure. A softening labor market, along with declining transport costs, contributed to the drop.

Meanwhile, British retail sales unexpectedly rose 0.3% in September, defying concerns about consumer sentiment ahead of the government’s upcoming budget. Large investors like Goldman Sachs and Amundi have shifted their focus to UK bonds, showing confidence in the UK’s economic outlook and favoring gilts ahead of the new budget announcement.

Source: Bocconi Students Investment Club, Trading Economics

Rest of the World

Japan’s stock markets experienced declines, with the Nikkei 225 Index falling by 1.58% and the broader TOPIX Index down 0.64%. Although the easing of domestic inflation in September was anticipated, it sparked speculation that the Bank of Japan might not raise interest rates again this year. Recent comments from BoJ officials, including Board Member Seiji Adachi, emphasized that while the conditions for monetary tightening were largely in place, the BoJ should proceed cautiously due to global economic uncertainties and domestic wage growth concerns. As a result, the yield on the 10-year Japanese government bond rose to 0.97% from 0.94% the previous week. Inflation eased as expected in September, with Japan’s core consumer price index (CPI) rising by 2.4% year-over-year, down from 2.8% in August, partly due to the reinstatement of electricity and gas subsidies. However, exports fell by 1.7% in September, marking the first decline in 10 months, driven by weaker demand from China. Imports, on the other hand, rose by 2.1%, reflecting the impact of the weakened yen.

In China, stock markets rose after the central bank introduced new support measures. The Shanghai Composite Index gained 1.36%, while the CSI 300 rose 0.98%. However, Hong Kong’s Hang Seng Index dropped by 2.11%. China’s economy grew by 4.6% in the third quarter, slightly below the government’s target of 5%, though industrial production and retail sales showed signs of improvement, with both surpassing expectations in September. Inflation cooled to 0.4%, its lowest level in three months.

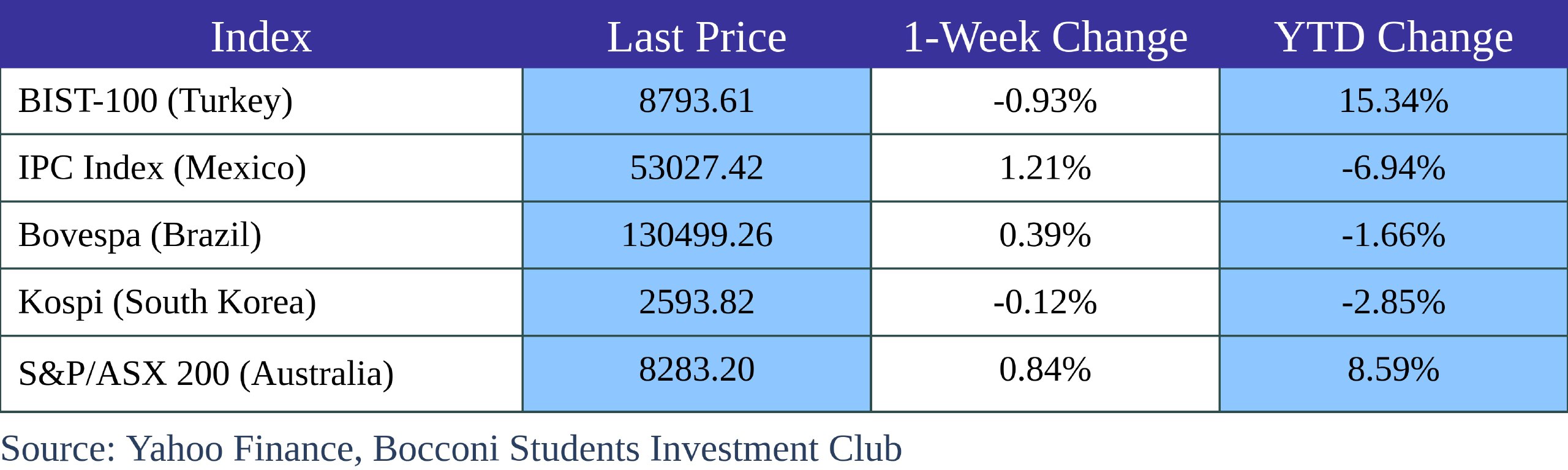

Global equities showed mixed performance on Friday, with gains in Mexico offset by declines in Brazil, South Korea, and Australia. In Mexico, the S&P/BMV IPC index rose by 1.07% at the close, driven by strong performances in the Industrials, Consumer Goods & Services, and Consumer Staples sectors. Meanwhile, Brazil’s Bovespa index saw a decline of 0.22%, primarily due to losses in the Real Estate, Public Utilities, and Consumption sectors. In South Korea, the KOSPI index slipped by 0.12%, closing at 2,593.82. Gains in the semiconductor sector were outweighed by declines in the automotive and biopharma sectors. In Australia, the S&P/ASX 200 fell 0.87%, with the Utilities, Real Estate Investment, and Consumer Discretionary sectors contributing to the overall market decline.

In Turkey, the central bank held its one-week repo auction rate at 50.0%, as expected. While there was a slight increase in inflation trends in September, the central bank anticipates that a slowdown in domestic demand will bring inflation down, reinforcing the belief that disinflation will strengthen over time as tighter monetary policies take effect.

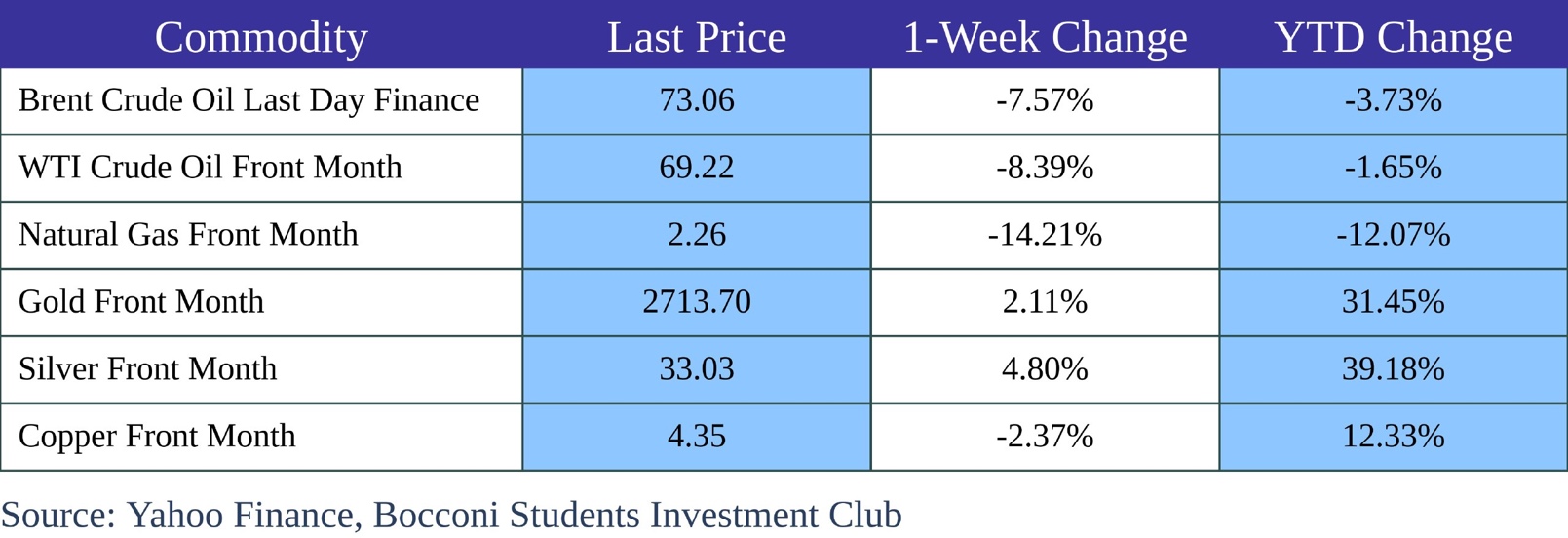

FX and Commodities

The commodities sector posted its second consecutive weekly loss, giving back half of the gains achieved over the previous four weeks. Weakness was seen across energy, industrial metals, and grains, while precious metals like gold and silver continued their rally.

Crude oil, diesel, and natural gas experienced sharp declines due to weaker demand despite ongoing geopolitical supply risks. A lack of significant improvement in China’s economic stimulus efforts contributed to this downturn, while Brent crude returned to neutral territory, trading near mid-$70s. China’s economic policies supporting the housing market and banking sector initially spurred strong gains in commodities like copper and iron ore. However, over half of these gains were reversed as traders questioned the scale of the initiatives. Concerns remain about China’s ability to meet its 5% growth target without stronger fiscal support for consumption and housing prices.

Despite the strength of the US dollar, which rose by 2.5%, gold’s rally remains intact, largely driven by global uncertainties, safe-haven demand, and de-dollarization. Gold surged 0.8% to $2713.70 per troy ounce, marking its largest weekly gain since mid-September and extending its winning streak to six weeks. Over this period, gold has risen by 8.83%, driven by safe-haven demand amidst global uncertainties and expectations of central bank rate cuts.

This week, the US dollar regained strength, reaching a fresh 11-week high despite an earlier pullback driven by easing tensions in the Middle East and a 5% drop in oil prices. Concerns surrounding the upcoming US election provided a boost to the dollar, applying downward pressure on the EUR/USD pair. The euro also faced additional headwinds following another interest rate cut from the ECB. The GBP/USD pair experienced a sharp decline, falling below $1.30 for the first time since August. This drop came in response to data showing that UK wage growth and inflation are cooling, which has increased market speculation around potential rate cuts from the Bank of England. With less than three weeks remaining before the US election, growing uncertainty has sparked a potential resurgence in demand for Swiss franc safe-haven assets. Switzerland’s strong economic performance relative to its Euro-area peers further strengthens the franc’s appeal.

Meanwhile, the yen weakened, trading near the upper 149 level against the US dollar. Japan’s chief currency official, Atsushi Mimura, remarked that the recent yen fluctuations were “one-sided and rapid.” Authorities are closely watching the situation, as the currency approaches levels that triggered intervention earlier this year.

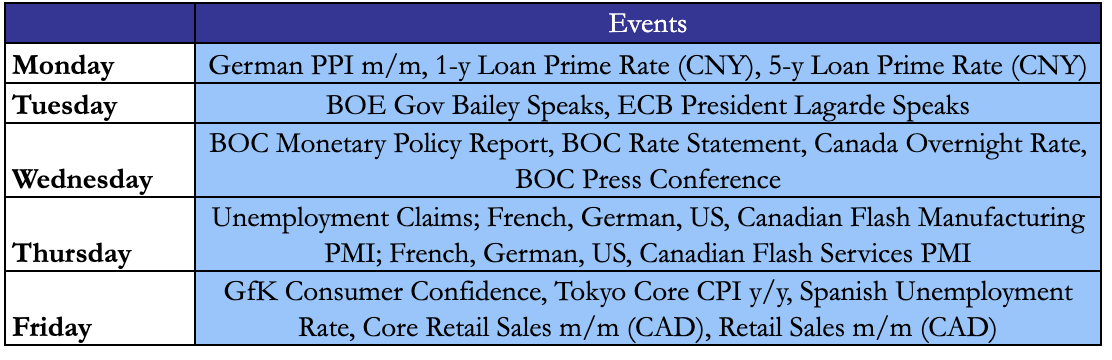

Next Week Main Events

Brain Teaser #24

How many trailing zeros are in 100! (factorial of 100)?

SOLUTION

We know that each pair of 2 and 5 will give a trailing zero. If we perform prime number decomposition on all the numbers in 100!, it is obvious that the frequency of 2 will far outnumber of the frequency of 5. So, the frequency of 5 determines the number of trailing zeros. Among numbers 1, 2, · · ·, 99, and 100, 20 numbers are divisible by 5 (5, 10, · · ·, 100). Among these 20 numbers, 4 are divisible by 5 squared (25, 50, 75, 100). So, the total frequency of 5 is 24 and there are 24 trailing zeros.

Brain Teaser #25

Eight quants from different banks are getting together for drinks. They are all interested in knowing the average salary of the group. Nevertheless, being cautious and humble individuals, everyone prefers not to disclose his or her own salary to the group. Can you come up with a strategy for the quants to calculate the average salary without knowing other people’s salaries?

0 Comments