[edmc id=1641] [/edmc]

[/edmc]

US

This week has been full of economic data. The most relevant are the following:

– Final GDP growth for 4th 2013 quarter q/q is 2,6%, still mainly driven by inventories.

– Flash manufacturing PMI is at 55.5, a bit lower than expectations. However, this suggests a manufacturing production expansion over the next months.

– Consumer confidence is high, as the CB Consumer confidence index reached 82.3, the highest level since the middle of 2008. The UoM (University of Michigan) consumer sentiment index is stable.

– Unemployment claims have been quite low, but this doesn’t take into account the participation rate, which has not improved yet since the last BLS report.

– Pending Home Sales m/m had a huge surprising drop at -0.8% (vs a market consensus of +0.1%). As a leading economic indicator, it could be worrying if next month it doesn’t improve.

Regarding the stock markets, it seems the end of the strong bull market we had for the past year. On Wall Street, the Nasdaq biotechnology index slumped nearly 3 percent drop. The biotech sector is down 7 percent for the week and down about 13 percent for the month. The S&P has declined a by -0,48% while the Dow Jones gained a little 0.13%.

U.S. Treasury bond prices rose broadly Wednesday as a mixed durable goods report eased worries that the Federal Reserve may raise interest rates sooner than many investors expect.

Eurozone

This week data for Eurozone have been “roller coasting”. The beginning of the week surprised investors with a positive PMI for France, hitting a two-and-half year high of 51.6, although a weaker result for Germany (whose figures fell at a three-month low of 55) softened the happiness. The flash estimate of 53.2 for the whole area still communicates a cementing recovery after a problematic period. This improving condition is confirmed by the unexpectedly high level of government debt issuance, in particular by peripheral countries, which are enjoying low borrowing costs due to decreasing yields in their bonds (one name: Portugal). The decline in Eurozone interest rates is mainly due to positive expectations for future growth and weak inflation plus a likely loosening intervention by the ECB.

This positive start of the week sustained the quotation of the Euro, which during the first two days of the week reached the significant value of 1.39 against USD. However, the remaining part of the week did not follow the same pattern. In fact, as you can see from the chart, on Wednesday the Euro started to decline due to renewed fears about the brim situation in Crimea. Moreover, the slow fall was sustained by the dovish signals that the president of the Bundesbank, Jens Weidmann, gave about the possibility to support the purchase of government debt by the ECB under some conditions (Quantitative Easing). The intervention of the central bank chaired by Mario Draghi seems more and more likely: negative data on Friday about inflation in Germany and Spain implemented the fear that the Eurozone could drift toward a Japanese-style stagflation. Spain in particular saw a decline of 0.2% in March on an annual basis, against analysts’ expectations of a surge. Those data make more probable the expected negative data of rising prices at 0.6% for the entire Eurozone. Following this sad end of the week, the value of the common currency has started pricing the really likely expansive monetary policy that, sooner or later, the ECB will perform in order to tackle the peril of deflation.

Looking at the entire week the Euro has declined by 0.27% against dollar. In our opinion, if negative data about inflation will be confirmed on Monday, the Euro will continue to decrease in value. Therefore, short EUR/USD is the suggested alternative. However, considering the long run, this strategy could be painful. Even if Draghi intervenes, the refi-rate is not the main driver for the value of our currency. On the contrary, the value of the Euro is prominently sustained by the current account surplus that is characterizing the Eurozone. In addition, the positive hopes about a fast and strong recovery of European economy add support and strength to the value. To sum up, some analysts strongly believe that the value of the Euro will actually increase in one-year time. Therefore, after Monday figures, you should buy it, and keep it for some months.

Source: FT

UK

On Tuesday many contrasting data about UK Inflation was released. Consumer Price Index y/y, despite hitting the forecast of 1.7%, gained substantial press coverage as the lowest CPI since 2010. Core CPI y/y was 1.7%, beating the expectations of 1.6%. Producer Price Index input and output, which measure the supply-side inflation, were instead well below forecasts. However, it is important to point out that PPI is rather volatile and its estimates often far from the actual value.

Housing Price Index (HPI) soared to 6.8% y/y (instead of the expectations of 5.7%), increasing worries about a housing bubble. House prices were particularly strong especially in London and in Wales. As the picture below shows, the HPI itself is neither excessively high, nor growing too quickly, and this gives credit to longer than expected low interest rates in UK.

Retail Sales growing 2% m/m (instead of a -0.9% forecast) gave clear-cut signal to UK economy, in addition to the 0.7% q/q growth of GDP. Yet, these positive news were offset by a Trade Deficit of £22.8 bln, almost £10 bln more than expected.

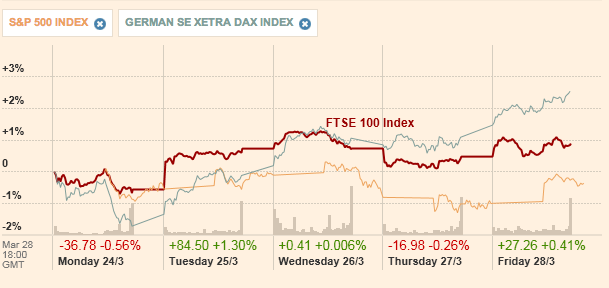

The FTSE100 gained 1% this week, performing better than the S&P but worse than the DAX and the NIKKEI225.

Source: FT

Yields were almost the same as the previous week, with the 10y Gilt at 2.73.

Pound instead appreciated against all major currencies (EUR, USD, JPY), partially rebounding from the previous month weak performance.

Next week most important data will be Construction, Services and Manufacturing PMI. Halifax and Nationwide HPI, in addition to Mortgage Approvals will also be important to evaluate if the rising houses prices will keep their momentum.

Japan

The week just past brought very important macroeconomic data from Japan. This centred on inflation indicators: chiefly, the Japanese CPI went up on February to 1.5% from January’s reading of 1.4%. Such mild increase is still good news for Japan’s central banker Mr. Kuroda, who has set forth a target of price increases in the range of 2% annually that has yet to be reached. However, a consumption tax hike to be introduced in April risks stifling these promising developments, especially as this week’s figures on overall household spending in February were disappointing at -2.5%. Indeed, should such figures persist after the tax hike, the success of Mr. Abe’s policy will be likely to be severely questioned. Just as in the last week, foreign investors continued pulling out funds from Japanese equities, albeit at a slower pace. Moreover, this week saw outflows even from Japanese bond markets totalling nearly ¥400 bn.

The yen held firm during this week, closing at 102.79 ¥/$ from a start of 102.25. Japanese equities enjoyed instead a better performance as the Nikkei 225 went up by 3.32%, settling at a level of 14,696. In particular, positive inflation data allowed a rebound of the index of more than 200 points on Thursday. Concurrently, yields paid by the government on 10-year bonds went up slightly by 3bp to 0.63%. We believe that the biggest test of the success of Mr. Abe’s economic policy, which will also be reflected in financial markets, will be the introduction of the sales tax hike next month, so that Japan will be the setting of possibly much higher volatility than the one we have observed now as the persistence of inflationary expectations will be tested against a likely drag down in consumer spending.

China

On Monday, a small, rural bank turned out a customer’s request to withdraw 200,000 yuan (more or less $32,000). The event was sufficient to make people think that the bank was about to go bankrupt, and panic sparked in the area, with depositors queuing to collect their savings. The first thing in their mind was, most likely, that they were safer under the mattress than in a bank. In fact, there is no deposit insurance system in China, while financial institutions are bearing much more risk than they actually show. (Don’t forget to read our special report on Shadow Banking in China, which comprehensively addresses this issue!)

Jiangsu Sheyang Rural Commercial Bank was the most hit from the bank run. Official from the bank tried to calm depositors, but their efforts were worthless. Only after three days, when People’s Bank of China and local governors stepped in, the situation turned quiet again.

After a disappointing Manufacturing PMI of 48.1, the economy may realistically grow at a rate around 7.5%, which stands for a significant slowdown in the economy. Expectations of new stimulus from PBoC have increased: is the central bank really going to cut the banks’ reserve requirement ratio? Cutting the RRR practically means injecting new liquidity into the system, and this is not what the economy needs now. We believe that the government should and will more structural measures… but these require time. Hence, it is likely that the market will be eventually disappointed in the short-run. We are indeed bearish on stocks.

[edmc id=1642]Download as pdf[/edmc]

0 Comments